An iron condor is one of the most actively used neutral options-selling strategies, where traders make profits when the market remains calm instead of making big moves. The iron condor gained popularity in the early 2000s with traders beginning to rely on structured, multi-leg option trades to provide regular income.

It is quite popular since it targets high probability, controlled risk, and constant premium collection, particularly in sideways and low volatility markets. Simply speaking, it represents a trading mentality in which you profit on non-direction but not on direction.

What is an Iron Condor?

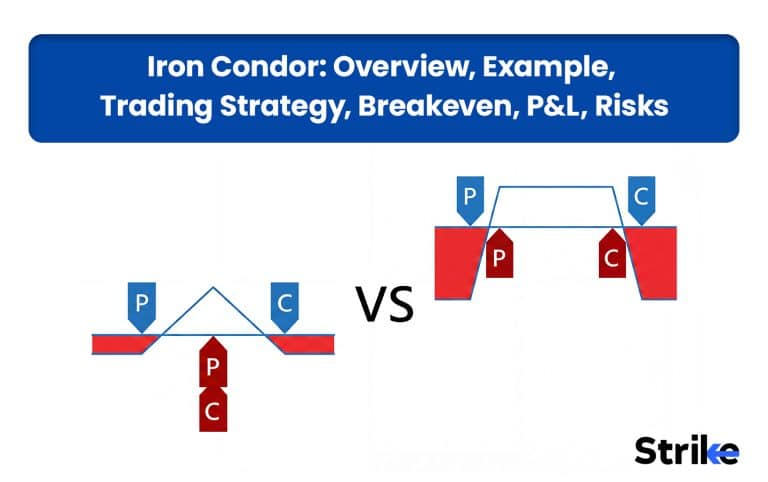

An iron condor is a non-directional options-selling trading strategy where traders make profit when the market stays within a defined price range. This strategy is created by combining two vertical spreads: a bear call credit spread and a bull put credit spread, both of the same expiry.

If the market stays sideways, both the spreads expire worthless and the option seller earns the premium.

How an Iron Condor Works

An iron condor works by selling out-of-the-money call and put options and buying further out-of-the-money call and put options for hedges. This creates a price range or a zone of profit in the market. When the price stays within this range, traders make profit.

When the price moves beyond the range, it gives limited loss because of hedges. The unlimited loss of option selling is covered by the profits in option buying, limiting the loss.

Short Iron Condor

A short iron condor is a net credit, the most used non-directional option strategy where traders get profit when the market doesn’t move in either direction with strong momentum and remains sideways.

To create a short iron condor strategy, execute the order in the following ways.

- Sell an out-of-the-money (OTM) call

- Sell out-of-the-money (OTM) put

- Buy a further out-of-the-money (OTM) call

- Buy a further out-of-the-money (OTM) put

As we are selling inner strikes and buying outer strikes, a strategy is in net credit.

The risk/reward and breakeven in this strategy can be calculated by the simple formula discussed below.

| Risk & Reward of Short Iron Condor | |

| Max Profit | Limited to the net premium received |

| Max Loss | Limited to (spread width – premium received) |

| Upper Breakeven | Short Call Strike + premium received |

| Lower Breakeven | Short Put Strike – premium received |

Long Iron Condor

A long iron condor is a net debit, non-directional option strategy where traders get profit when the market moves in either direction with strong momentum instead of staying within the range. A long iron condor is just the opposite of a short iron condor.

To create a long iron condor strategy, execute the order in the following ways.

- Buying an out-of-the-money (OTM) call

- Buying out-of-the-money (OTM) put

- Selling a further out-of-the-money (OTM) call

- Selling further out-of-the-money (OTM) put

As we are buying inner strikes and selling outer strikes, a strategy is in net debit.

The risk/reward and breakeven in this strategy can be calculated by the simple formula discussed below.

| Risk & Reward of Long / Inverted Iron Condor | |

| Max Loss | Limited to the premium paid |

| Max Profit | Limited to (spread width – premium paid) |

| Upper Breakeven | Upper strike + premium paid |

| Lower Breakeven | Lower strike – premium paid |

Reverse Iron Condor

“Reverse iron condor” is nothing but another name for “long iron condor,” created to trade volatility and earn profits from directional trades.

Why Use a Iron Condor Strategy?

An iron condor is one of the best strategies to earn regular income from the market, especially when the markets are sideways, which most of the time they are. Instead of predicting the market trend, an iron condor works on probability, time decay, and volatility behavior.

There are five core benefits why traders use the iron condor strategy. These core benefits are briefly discussed below.

- Defined Risk & Reward: Unlike unlimited loss in option selling, this strategy has a fixed risk to reward.

- Collect Premium Immediately: You receive the net credit instantly when you enter the trade. If price stays within the selected range, you keep the premium after the expiry.

- High Probability of Profit: As markets are 60-70% of the time, they remain sideways. The probability of profit is relatively high as you are selling OTM options.

- Benefits from Time Decay (Theta): The value of an option reduces as expiry approaches. If the price remains within your predicted range, options will expire worthless because of theta, and option sellers will earn the premium.

- Benefits from Low Volatility (Vega): If the volatility drops after the entry, the premium will lose its value fast, giving gains. Also, during the period of low volatility, the market remains sideways, giving a suitable market condition for an iron condor.

However, it is important to know that an iron condor is less about collecting premium and more about selecting the right conditions to collect it safely.

When to Use a Iron Condor?

There are two scenarios when you can use the iron condor strategy. The scenarios are during sideways markets and during high-volatility times.

- During a sideways market: The strategy works best when the market or stock is trading in a range with low momentum, without any clear direction.

- During high volatility periods: This strategy also works great when the volatility (IV) is high but expected to decline. During the period of high volatility, the premiums are generally high, and traders can get better premiums and a wider range to trade. Once the volatility drops, premiums quickly lose value, increasing the profit potential.

Avoid trading iron condors during the signs of expansion, momentum, or uncertainty driven by news or events.

How Option Greeks Affects Short Put Condor?

The behavior of a short iron condor is deeply influenced by four major option greeks, which is delta, theta, gamma, and vega. Understanding these Greeks and their effect on option premium is very important before trading a short iron condor professionally.

- Delta: Delta represents directional risk. During the formation of a short iron condor, the delta stays neutral. If the price stays within the selected range, delta remains near zero. Once the price starts moving in either direction, the neutrality of delta shifts and starts giving losses. If the delta moves beyond ±0.10 or ±0.15, your position gets exposed to directional risk. That’s when traders either close the position or roll one side to rebalance the delta again near zero.

- Theta (time decay): It is the main profit engine for an iron condor. As we are net option sellers, the position benefits from the passing of time. As every day passes, theta decays, options lose value, and traders gain profit. As expiration approaches, theta accelerates.

- Vega: Vega represents volatility risk. A short iron condor has a negative vega because if volatility drops, premium shrinks, and traders make a profit. However, if Vega gets positive, the premium expands and the seller makes a loss. Even though the price remains steady, a spike in volatility can show MTM loss.

- Gamma: Increases risk near expiry and measures how fast delta changes with price. As we are net option sellers, we are short on gamma; we prefer gamma to stay lower. But when gamma gets high, the loss accelerates as gamma directly affects delta. The risk of gamma rise is high near expiry; that’s why traders exit early before expiry.

A short iron condor looks safe at entry, but its real risk begins after the market starts moving. You lose when delta shifts and gamma accelerates faster than theta can pay you.

How to Trade using Iron Condor Strategy?

There are six major steps to trade using the iron condor strategy. These steps are briefly discussed below.

- Identify the Market Condition: Select the sideways market condition with low momentum, as an iron condor is a range-bound market strategy. Avoid periods with major upcoming news or events, as they can trigger sharp moves and break the range.

- Select the Expiry: The premium and speed of theta decay depend on the days of expiry.

| DTE (Days to Expiration) | Characteristics |

| 7–14 DTE | Faster theta decay, but high gamma risk—sharp moves can impact the position quickly |

| 30–45 DTE (Most Preferred) | Sweet spot—good premium, manageable gamma, and enough time for adjustments |

| 60+ DTE | Higher initial premium, but slower decay and longer exposure, increasing overall risk |

- Strike Selection: Strike selection can be done either based on support/resistance or using delta. Sell OTM call above resistance and sell OTM puts below support and buy further OTM calls and puts as hedges. Using delta, sell the strike with delta between 0.15 and 0.25 and buy further OTM for hedges.

- Managing Strike Difference: If the gap between sold strikes is wider, the probability of winning will be high, but the premium received will be lower. Whereas if the gap between sold strikes is smaller, the probability of winning will be lower, but the premium received will be higher. Try to balance the risk and reward instead of chasing big premiums or high-probability setups.

- Execution: Execute all the orders simultaneously as a single order to avoid leg risk. Avoid using market orders for multileg options strategies to avoid losses due to bid-ask spread.

- Trade Management: Make adjustments if the price starts moving beyond your decided range to reduce the losses.

How to Adjust an Iron Condor

The adjustment in an iron condor is needed when the price starts moving towards one side of the range. The goal of the adjustment is to reduce risk, rebalance the position, and avoid large losses.

There are five major ways to adjust an iron condor. The ways are rolling t

- Roll the Unchallenged Side: This is the most popular adjustment where the unchallenged side is closed and a new spread is added closer to the current price. For instance, if the price is moving upward, your call side is at risk, but the put side is safe. Close the put-side spread and create a new spread near the current price. This helps earn extra premium, which indirectly reduces the loss.

- Roll the Challenged Side Further: When the price moves in one direction, shift the challenge spread further OTM. For instance, if the price is moving up, shift the call-side spread future OTM. This creates more room for price to move but often requires paying some debt. This adjustment is done before the price completely moves beyond the selected levels.

- Convert it to an Iron Butterfly: In this adjustment, you close the unchallenged side in profit and add a new spread closer to the current price so that both short strikes align at the same level, effectively converting the position into an iron butterfly. This increases the premium collection.

- Hedge With Directional Trade: When the price breaches beyond the decided level, close the challenged spread and buy an option in the direction of the move. This adjustment is comparatively advanced and requires experience.

- Exit the trade: When the market is clearly trending and loss is manageable, just exit the trade; don’t do any adjustments.

Iron condor rewards traders who manage risk most consistently, size positions most carefully, and stay disciplined when the market tests their strikes. Master the process, and the profits follow.

What Are the Breakeven Points in an Iron Condor?

Breakeven points in an iron condor are price levels at which the profit turns into a loss. An iron condor has two breakeven points, one on the upper side and one on the lower side.

To find out the price level for breakeven, use a strike price along with the net credit received.

- For a lower breakeven point: Short Put Strike − Net Premium (credit) Received

- For an upper breakeven point: Short Call Strike + Net Premium Received

The gap between two upper and lower breakeven points is your trading range. The wider the range, the higher the probability of winning but less premium. A narrow range gives a lower probability of winning but a higher premium.

What are the Maximum Profit and Loss of an Iron Condor?

An iron condor has fixed maximum profit and maximum loss, which are predefined during the time of entry.

- Maximum Profit: The max profit in an iron condor is the net premium you have received when entering the trade (max profit = net premium received). However, you will get the max profit only when the market expires within your selected range; if it expires outside the range, it can reduce your profit or lead to loss.

- Max Loss: The maximum loss in an iron condor is also limited due to hedges (the long call and long put) and is calculated based on the width of the spread (Max Loss = Width of the spread − Net credit received). Max loss happens when the market moves significantly beyond the breakeven point. The sold option starts giving you losses, while the long option starts giving profit, limiting your max loss regardless of how far the price moves beyond the breakeven point.

An iron condor offers limited profit and limited loss, making it a risk-defined options strategy. It works best in sideways markets where the price remains within the selected range until expiry.

How to Backtest Iron Condor Performance?

The performance of an iron condor can be backtested by simulating the historical trades with specific rules and past market data. This helps traders assess how a strategy would have performed over time, allowing for statistical validation before committing real capital.

However, simulating historical trades manually is difficult and time-consuming because options data involves multiple variables like strike selection, implied volatility, time decay, and adjustments.

There are different backtesting software available that automate the simulation, such as Opstra, Stockmock, QuantsApp, etc.

These software stimulate historical trades baked on real market data and apply stop-loss, adjustment, and exit rules easily. Analyze performance metrics like win rate, drawdown, and expectancy.

According to tastytrade, a research-based trading platform demonstrates that an iron condor has a 65%–75% probability of profit, depending on strike selection (often using 16–30 delta options).

What are the Variants of Iron Condor?

There are three major variants of iron condors based on the view of the market. These variants are created by modifying spread width, shifting strike placement, or combining multiple condors to suit different market conditions.

Broken-wing iron condor

A broken-wing iron condor is an asymmetric iron condor strategy, where one side’s spread is wider than the other side’s, creating an asymmetrical risk-to-reward structure. Unlike a normal iron condor, the risk in a broken-wing iron condor is intentionally increased on one side to collect a higher premium.

A broken-wing iron condor is mainly used by traders with a directional bias, where they are willing to take more risk on one side for extra premium. Let’s understand using a real-time payoff chart.

Here, the put-side risk is higher compared to call-side risk due to the wider spread, but for that, you are getting more premiums. The net credit in this strategy is larger than a standard condor would produce.

| Side | Action | Strike | Option Type | Spread Width | Risk Level |

| Put Side | Buy | 23500 | PE | ||

| Put Side | Sell | 23800 | PE | 300 pts | Higher |

| Call Side | Sell | 24200 | CE | ||

| Call Side | Buy | 24400 | CE | 200 pts | Lower |

In the above setup, we are directionally biased towards bullish, because the put-side spread is wider (300 points) and carries more risk compared to the call-side spread (200 points), which carries less risk.

- If the market stays between 23800 and 24200, we gain maximum profits.

- If the market moves sharply above 24200 (a bullish move that we were expecting might happen), we will lose less because we have higher premiums to collect from the put side.

- If the market falls sharply below 23800 (a bearish move that we were not expecting might happen), we will lose large due to the wider spread on the put side.

The reason for structuring a broken-wing iron condor is to collect a higher net premium while aligning the trade with a bullish market view.

Directional iron condor

A directional iron condor is a directional-biased strategy where, instead of just skewing the width of the spreads, traders shift the entire profit zone away from the current market price towards the expected move. In this the risk-to-reward structure is symmetrical, but the profit zone is no longer centered around the current price.

- Bullish Directional: All four strikes are moved above the ATM. The short put is already in-the-money territory at initiation, and the profit zone sits above the current price. You need the stock to rally to land in your tent.

- Bearish Directional: All four strikes were pushed below ATM. The short call is already ITM at initiation. You need the stock to drop.

Let’s understand using a real-time payoff chart.

Here, we can clearly see that the entire iron condor is shifted away from the current market price (approximately ₹23998) towards the upper side, suggesting a bullish bias.

| Side | Action | Strike | Option Type | Spread Width | Risk Level |

| Put Side | Buy | 23900 | PE | ||

| Put Side | Sell | 24100 | PE | 200 pts | Equal |

| Call Side | Sell | 24500 | CE | ||

| Call Side | Buy | 24700 | CE | 200 pts | Equal |

The setup we created gave us a maximum range towards the upside. The maximum profit will occur when the market moves upward and expires between 24100 and 24500. If price moves below the current market price (₹23998) or upper breakeven point (₹24600), the losses will be similar on both sides due to equal spreads.

Double Iron Condor

A Double Iron Condor is created by combining two iron condors at different strike ranges, allowing the trader to capture premium from a wider price range instead of a single narrow zone.

When traders expect the market to stay in a broader range with wider fluctuation, a normal iron condor’s range might not be sufficient. The trader then combines the two iron condors, one upper-range iron condor and the other lower-range iron condor. This gives traders a wide range for profit and increases premium collection.

The payoff graph may look like a wide plateau or slightly multi-peaked structure.

Let’s understand how we have merged two iron condors. The table below mentions the strikes of each iron condor.

Iron Condor 1

| Side | Action | Strike | Type |

| Put Side | Buy | 23250 | PE |

| Put Side | Sell | 23450 | PE |

| Call Side | Sell | 23850 | CE |

| Call Side | Buy | 24100 | CE |

Iron Condor 2

| Side | Action | Strike | Type |

| Put Side | Buy | 23850 | PE |

| Put Side | Sell | 24100 | PE |

| Call Side | Sell | 24500 | CE |

| Call Side | Buy | 24700 | CE |

Here, we have created a double iron condor using 8 legs (positions), where the profit zone is between 23450 and 24500. which is much wider than a normal condor. However, the risk in a double iron condor is comparatively more than the reward.

What are The Margin Requirements for Iron Condors?

A margin requirement for an iron condor is capital blocked by the broker to cover the maximum possible loss. This capital requirement is usually calculated based on the width of the spreads and net premium to be received.

The margin can be calculated by using the formula given below.

- Margin Required = Spread Width – Net Premium Received × Lot Size

Where,

Spread Width = Difference between strikes on one side (call or put spread)

Net Premium = Total premium collected from selling both spreads

Let’s calculate the margin required for an iron condor by creating a real-time iron condor.

Net Premium Received = (76.85 + 124.8) − (40 + 62.55) = 201.65 − 102.55 = ₹99.1

Total premium = 99.1 × 65 (Lot size) = ₹6,441.5 ≈ ₹6,442

Spread Width

Put Spread = 23800 − 23600 = 200

Call Spread = 24400 − 24200 = 200

So, max width = 200

Margin Required = Spread Width – Net Premium Received × Lot Size

Margin Required = 200 − 99.1 × 65 = ₹6,559 approx

As you can see, the formula-based margin is ₹6,559, which is a true economic risk; however, the brokers’ margin is showing ₹68,039. as it includes SPAN and exposure margins to cover extreme market moves.

What Are the Risks of Iron Condors?

The only risk of an iron condor strategy is a trending move. As an iron condor is a range-bound market strategy, a strong move beyond the chosen strike price gives a loss. There are four major risks associated with the trending move in an iron condor.

- Trend Risk: When price moves suddenly beyond your short strike due to a breakout, increased IV, or any event, it accelerates your loss. If your hedges are far OTM, you will incur even more loss.

- Risk-Reward Imbalance: In an iron condor, the profits are usually small compared to losses. One loss can wipe out multiple small gains.

- Adjustment Risk: Many traders try to cover their losses by doing adjustments. These adjustments increase complexity, and wrong adjustments increase losses instead of reducing them.

- Psychological Risk: As wins are frequent in an iron condor, traders become overconfident, especially beginners. They increase position size due to overconfidence and take significant damage in one loss-making trade.

An iron condor does not fail often, but when it fails, one trending move erases a series of disciplined gains.

What are Alternatives to Iron Condor Strategy?

The alternatives to the iron condor strategy are the iron butterfly, vertical spread, short strangle, and calendar spread.

| Strategy | Market View | Risk Level | Reward Potential | Key Difference from Iron Condor |

| Iron Butterfly | Neutral (very tight range) | Limited Risk | Moderate | Narrower range, higher premium, more sensitive to movement |

| Vertical Spread | Directional (bullish or bearish) | Limited Risk | Limited | Focuses on one direction instead of range-bound trading |

| Short Strangle | Neutral (wide range) | Unlimited Risk | High | No protection wings, higher risk but higher premium |

| Calendar Spread | Neutral to slightly directional | Limited Risk | Moderate | Uses different expiries to benefit from time decay differences |

Iron Condor is about balance, but the real edge comes from switching strategies like an Iron Butterfly or a Vertical Spread based on volatility and conviction. While a Short Strangle is excellent for aggressive premium collection, a Calendar Spread offers a distinct advantage in low-volatility markets. Professionals don’t stick to one setup; they adapt to what the market is offering, whether that means shifting from an Iron Butterfly to a Vertical Spread, or choosing between a Short Strangle and a Calendar Spread as conditions change.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 32")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.