The Iron Butterfly is an advanced options trading strategy designed to profit from a neutral outlook on the underlying asset. The Iron Butterfly involves selling an at-the-money (ATM) straddle and buying two out-of-the-money (OTM) wings—a call and a put—at equal distances from the ATM strike, forming a position with defined risk and reward.

Historically, traders have leveraged the Iron Butterfly for its efficient use of capital and favorable risk-to-reward ratio. The strategy emerged as a popular alternative to naked straddles, as it offers protection against large, unexpected market moves by capping both potential losses and gains.

What is an Iron Butterfly?

An Iron Butterfly is an options strategy that combines selling an at-the-money straddle and buying protective out-of-the-money options to create a position with limited risk and reward. An Iron Butterfly uses both calls and puts to form a spread, with all options sharing the same expiration date.

This approach involves four options contracts: selling one call and one put at the same strike, while simultaneously buying a lower-strike put and a higher-strike call. The short strike is typically at the current market price, making the position centered on the underlying asset’s value at entry.

The primary goal of the Iron Butterfly is to collect a net premium, which is the maximum profit if the underlying finishes at the short strike at expiration. The protective wings—the purchased OTM options—limit both upside and downside risks, creating a payout profile that resembles a butterfly’s shape on a risk graph.

How Does an Iron Butterfly Work?

An Iron Butterfly works by simultaneously selling an at-the-money call and put, and buying out-of-the-money call and put options at equidistant strikes, generating a net credit and a defined risk/reward profile. The structure ensures that the position’s maximum profit and loss are both predetermined at entry.

The formula for constructing an Iron Butterfly involves selecting a central strike at or near the asset’s current price (the “body”), selling both a call and a put at that strike, and then buying a call above and a put below this strike (the “wings”).

The distance between the body and wings determines the width of the spread and the risk.

Mathematically, the net premium received (credit) is calculated as

Net Premium = (Premium received from sold options) – (Premium paid for purchased options).

This credit represents the maximum possible profit. The maximum loss is the width between the strikes minus the net premium collected.

Incase where the underlying asset closes at the short strike at expiration, all options except the sold straddle expire worthless, allowing the trader to retain the entire net credit. If the price moves beyond either wing, the loss is capped, as the bought options offset further adverse moves.

The Iron Butterfly’s structure creates a defined, limited-risk position that benefits from the underlying asset staying near the chosen strike price.

As expiration approaches, time decay (theta) works in the trader’s favor, eroding the value of the sold options faster than the bought wings.

Why Use an Iron Butterfly Strategy?

Traders use the Iron Butterfly strategy for its ability to profit from a neutral outlook, high theta decay benefits, and clearly defined risk and reward. The strategy is ideal for scenarios where the trader expects minimal movement in the underlying asset.

A key advantage of the Iron Butterfly is its positive theta, meaning time decay works in the trader’s favor. As expiration approaches, the sold options lose value faster than the bought wings, allowing the trader to keep the bulk of the premium if the price stays near the central strike.

The well-defined risk and reward profile appeals to traders who want to avoid unlimited risk. Losses are capped by the wings, while the maximum profit is known upfront, providing confidence and clarity in trade management.

Because the Iron Butterfly is market neutral, it’s suitable when traders expect the asset to remain in a tight range. The strategy is especially attractive in high implied volatility environments, as premiums are elevated and the likelihood of contraction post-event (such as earnings) is high.

When to Use an Iron Butterfly?

The Iron Butterfly strategy is best used in low volatility environments, during earnings when implied volatility is high, or when anticipating the price will stay in a range. Its strengths align with periods of expected consolidation or limited price fluctuation.

Low volatility periods are ideal, as the probability of the underlying asset closing near the short strike increases, maximizing the chance of full premium collection. In these conditions, the Iron Butterfly outperforms more directional strategies, as it thrives when price stagnation prevails.

Earnings seasons or other volatility events present unique opportunities. Implied volatility surges ahead of such events, inflating option premiums. By selling an Iron Butterfly, traders exploit the likelihood of volatility collapsing after the event, which benefits the short options.

The strategy shines when technical or fundamental analysis suggests a range-bound move, or when the trader has no directional bias. Tight strike selection and correct timing are crucial to maximize profitability and minimize risk.

How Option Greeks Affect Iron Butterfly?

Option Greeks play a crucial role in the Iron Butterfly, with the position showing positive theta, near-zero delta, negative vega, and limited gamma exposure. Each Greek influences the trade’s performance in unique ways.

Theta, or time decay, is positive for the Iron Butterfly. This means the position profits as time passes, provided the underlying remains within th e expected range. The strategy’s main edge comes from collecting premium as the sold options decay faster than the protective wings.

Delta, the measure of directional exposure, is close to zero. The position is structured to have minimal sensitivity to small price movements, which aligns with its neutral bias. Large moves, however, result in increased delta risk near the wings.

Vega, which measures sensitivity to implied volatility, is negative. The Iron Butterfly profits when implied volatility drops, as this reduces the value of the options sold, boosting the position’s overall profitability. Sudden volatility spikes can hurt the trade, making timing critical.

Gamma exposure is limited due to the spread nature of the trade. While large price movements still pose risk, the bought wings cap exposure and reduce the impact of gamma compared to naked straddles or strangles.

How to Trade using Iron Butterfly?

Trading an Iron Butterfly involves selecting the underlying asset, identifying suitable strike prices, entering all four legs simultaneously, managing margin requirements, and knowing adjustment strategies. The process starts with analysis and careful setup.

First, choose an underlying asset with liquid options and tight bid-ask spreads to minimize slippage. Next, identify the central strike (at-the-money) and determine the width for the wings, typically equidistant out-of-the-money strikes for both calls and puts.

Here, a trader has sold one at-the-money (ATM) call and one ATM put at the 24600 strike, collecting premiums of ₹79.2 and ₹72.1 respectively. To limit potential losses, a 24950 out-of-the-money (OTM) call is bought for ₹12.4 and a 24350 OTM put is bought for ₹11.2. The lot size is 75.

To calculate the net premium received, we subtract the cost of the protective options from the premiums received from the short options. That is: ₹79.2 + ₹72.1 − ₹12.4 − ₹11.2 = ₹151.3 − ₹23.6 = ₹127.7. This makes the strategy a net credit one, meaning the trader collects ₹127.7 per lot upfront.

The maximum profit occurs when the underlying asset closes exactly at 24600, which is the strike of both short options. In this case, all options expire worthless, and the entire collected premium is retained. The maximum profit is ₹127.7 × 75 = ₹9,577.5, which rounds off to ₹9,578.

The maximum loss happens if the underlying closes beyond the protective wings—below 24350 or above 24950. In such cases, losses from the sold options increase, but they are capped by the long options. The formula for max loss is the difference between the short and long strike minus the net premium, multiplied by the lot size: (24600 − 24350 − 127.7) × 75 = (250 − 127.7) × 75 = ₹122.3 × 75 = ₹9,172.5.

There are two breakeven points in this strategy. The lower breakeven is the put strike minus the net premium received: 24600 − 127.7 = ₹24472.3, rounded to ₹24473. The upper breakeven is the call strike plus the net premium received: 24600 + 127.7 = ₹24727.7, rounded to ₹24727.

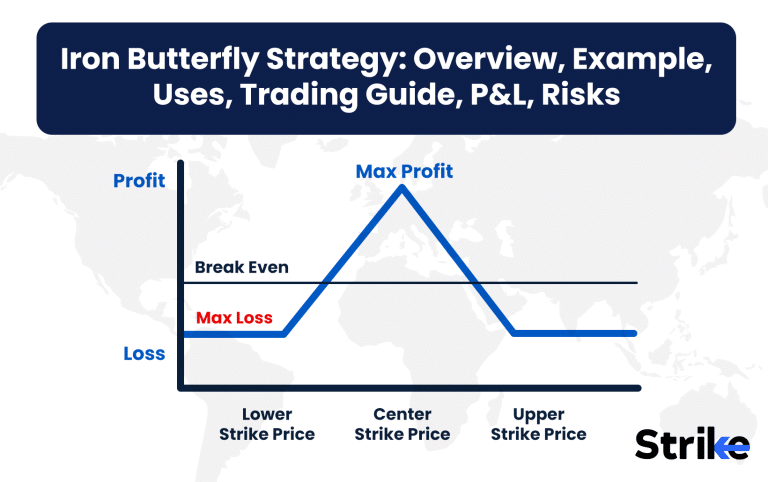

What are the Maximum Profit & Loss, Breakeven on an Iron Butterfly?

Maximum profit on an Iron Butterfly equals the net premium received, maximum loss is the difference between wing and body strikes minus net premium, and breakeven points are the body strike plus or minus net credit. This clarity makes risk management straightforward.

What are the Maximum Profit & Loss, Breakeven on an Iron Butterfly?

Maximum profit on an Iron Butterfly is the net premium received in rupees, maximum loss is the difference between the wing and body strikes minus the net premium, and breakeven points are the body strike plus or minus the net credit, all calculated in ₹. For example, suppose you set up an Iron Butterfly on NIFTY with these legs.

- Sell 1 ATM Call at ₹22,000 (receive ₹220 premium)

- Sell 1 ATM Put at ₹22,000 (receive ₹210 premium)

- Buy 1 OTM Call at ₹22,300 (pay ₹70 premium)

- Buy 1 OTM Put at ₹21,700 (pay ₹65 premium)

Net Premium Received = (₹220 + ₹210) – (₹70 + ₹65) = ₹295

Maximum Profit – This is the total net premium received, so ₹295 per lot if NIFTY expires at ₹22,000.

Maximum Loss – This is the difference between the body and wing strikes minus the net premium. Here,

Spread width = ₹22,300 − ₹22,000 = ₹300

Maximum loss = Spread width − Net premium = ₹300 − ₹295 = ₹5 per lot

There will be two breakeven points.

- Upper Breakeven: Body Strike + Net Premium = ₹22,000 + ₹295 = ₹22,295

- Lower Breakeven: Body Strike − Net Premium = ₹22,000 − ₹295 = ₹21,705

| Outcome | Formula | Value (₹) |

| Max Profit | Net Premium Received | ₹295 |

| Max Loss | Spread Width – Net Premium | ₹5 |

| Upper Breakeven | Body Strike + Net Premium | ₹22,295 |

| Lower Breakeven | Body Strike – Net Premium | ₹21,705 |

This structure makes the Iron Butterfly easy to manage and understand since risk and reward are defined upfront and all key numbers are in rupees.

What are the Risks of Iron Butterfly?

Iron Butterfly risks include limited profit potential, assignment risk, sensitivity to volatility spikes, the need for precise strike selection, and exposure to regulatory or margin changes. Understanding these risks is critical for effective trade management.

Profit is capped by the net premium received, which means large underlying moves result in missed opportunities compared to more aggressive strategies.

Assignment risk arises if the short options are exercised early, particularly in American-style options or near ex-dividend dates.

Volatility spikes pose a challenge. Because the strategy has negative vega, sudden increases in implied volatility lead to losses, especially if the underlying moves rapidly outside the profit zone. This sensitivity requires close monitoring and timely adjustments.

Precision in strike selection is crucial. Poorly chosen strikes increase the likelihood of losses or reduce the premium collected, undermining the strategy’s effectiveness. Furthermore, regulatory or broker-driven changes in margin requirements can impact the feasibility and returns of the trade.

Risk management and scenario analysis are essential when deploying Iron Butterflies, as the strategy’s success relies on both market behavior and disciplined execution.

Is Iron Butterfly Strategy Profitable?

Yes, The Iron Butterfly strategy is profitable in range-bound, low-volatility markets where the underlying stays near the sold strike. Profits are typically modest but consistent, thanks to premium collection and defined risk.

Success depends on accurate market outlook and timing, as large moves or volatility spikes erode gains. Traders who excel at strike selection and risk management often find the Iron Butterfly a reliable income generator in the right conditions.

Is Iron Butterfly Bullish or Bearish?

Iron Butterfly is a market-neutral strategy, neither bullish nor bearish. It profits when the underlying asset remains at or near the strike price of the sold options.

Traders use it when they expect minimal price movement, making it ideal for periods of consolidation or after sharp moves when volatility is expected to decrease.

What are Alternatives to Iron Butterfly Strategy?

Alternatives to the Iron Butterfly include the Iron Condor, Straddle, and Strangle strategies, each with distinct risk and reward profiles. The Iron Condor features wider wings for a larger profit zone but lower premium, making it less sensitive to small moves.

A Straddle involves selling both a call and put at the same strike, offering higher premium but unlimited risk. Strangles, on the other hand, sell OTM call and put options, providing more room for movement but increased exposure to volatility and larger potential losses.

Each alternative suits different market conditions and trader objectives, providing a spectrum of choices for managing risk and reward in options trading.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 20")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 21")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 22")

: Overview, 10 Types of Indicators, Settings for Different Markets 23")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 26")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 29")

No Comments Yet.