A straddle is an options strategy that involves buying both a call and put option on the same underlying asset with the same strike price and expiration date. The Straddle strategy allows traders to profit from large price moves in either direction.

It works by giving the trader exposure to unlimited upside if the price rises via the long call option while also providing downside protection in case of a price drop via the long put. The maximum loss is limited to the premiums paid for both options.

The main advantage of a straddle is it allows profiting from volatility expansion without needing to predict a direction. It benefits from a sharp move up or down. The disadvantage is it requires a significant price move to turn profitable due to the high premium cost of both options.

A straddle is primarily used when expecting an explosive move before expiration but unsure of the prevailing direction. Earnings reports and other news events that could induce heavy volatility are prime straddle opportunities. Traders utilize them to isolate volatility while remaining directionally agnostic on the underlying asset.

What is a Straddle Strategy?

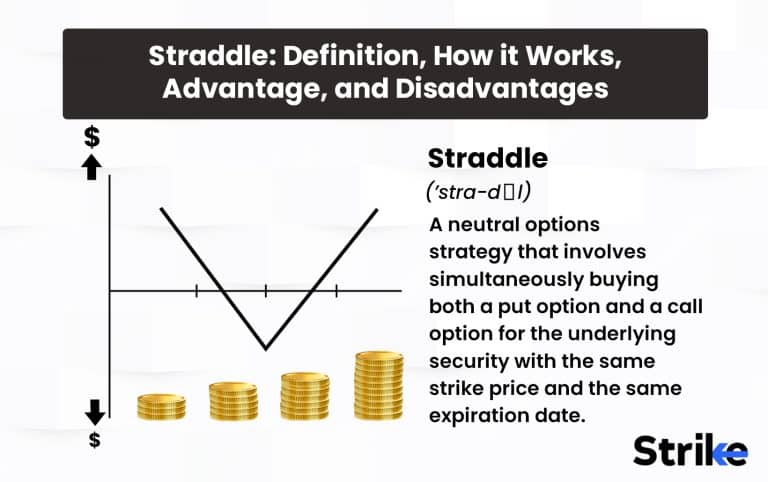

A straddle strategy is an options trading strategy involving the simultaneous buying of a put and a call option for the same underlying security with the same strike price and expiration date. The goal of a straddle is to profit from significant movement in the price of the underlying asset, regardless of the direction of the price change.

The straddle strategy aims to generate profits whether the underlying stock price increases or decreases substantially. By purchasing a put and a call option, the straddle strategy allows a trader to benefit from either a rise or fall in the stock price, above or below the strike price of the options. The potential for profit is unlimited on either side, while the maximum loss is limited to the premiums paid for the put and call options.

While implementing a straddle, the strike price of the options is typically set at or near the current market price of the underlying security. The put option gives the holder the right to sell the stock at the strike price if the stock falls below that level, while the call option gives the holder the right to buy the stock at the strike price if the stock rises above that level. Both options have the same expiration date.

The profit potential of a straddle relies on the underlying stock experiencing a very large price movement from the time the options are purchased to when they expire. The Straddle will likely lose money since the premiums paid for both the put and call will decline over time due to time decay if the stock price is stable and does not move much.

For a straddle to be profitable, the size of the price movement in either direction needs to be large enough to exceed the total premium paid for the put and call options. Any price movement less than the total premiums will result in a loss.

There are four advantages to using a straddle strategy. First, it generates profits whether the underlying stock price rises or falls substantially. The Straddle has unlimited profit potential in both upward and downward directions. Second, the maximum loss is limited and defined to the total premiums paid for the put and call options, providing some downside protection. Third, straddles are useful when expecting a large price swing in a stock but uncertain about the future direction. Finally, straddles are tailored to fit an investor’s specific market outlook or risk tolerance profile.

However, there are disadvantages to straddles to consider. The main drawback is that they require a large upfront capital outlay to purchase both the put and call options simultaneously. Additionally, profits require a very significant underlying price movement in order to exceed the total premium costs – if the stock price remains stagnant, the Straddle will result in losses. The expiration dates on the options also limit the window of time to realize gains. Time decay erodes the value of the options as expiration approaches as well. Moreover, the significant commissions paid on multiple option contracts take a bite out of potential gains.

What is the other term for Straddle Strategy?

The other common term used for a straddle strategy is a combination strategy. The terms Straddle and combination are often used interchangeably when referring to this options trading approach.

A combination strategy, like a straddle, involves simultaneously buying both a put and a call option on the same underlying asset with identical strikes and expiration dates. Since the trader is combining both a put and a call option in one strategy, it becomes known as a combination.

The goal of a combination strategy is to profit from a substantial move in the underlying asset’s price without caring about the direction of the move. By having exposure to both call and put options, the trader benefits when the price rises or falls dramatically.

Just like with a straddle, the combination strategy relies on the underlying stock experiencing a very large price movement for it to be profitable. The price needs to move enough to offset the premium costs of purchasing the put and call options.

The terms Straddle and combination tend to be used interchangeably when referring to this strategy of buying a put and call together on the same stock. They both refer to the same core strategy and have the same desired payoff.

They both involve simultaneously buying a put and a call on the same stock with identical strikes and expiration. The profit/loss prospects are the same. Potential for unlimited gains if the stock moves substantially in either direction. Maximum loss is limited to the total premiums paid.

They carry the exact same risks, such as time decay and requiring a significant price move to break even. Implementing them requires the same initial outlay to purchase the put and call options together. They both aim to profit from volatility in the stock rather than a specific directional bet.

Combination and straddle strategies are opened and closed using identical methods. Traders use them under the same market conditions when expecting a large move but unsure of the direction.

While technically, there are subtle differences between straddles and combinations, in common usage among options traders and investors, the terms are used interchangeably. They both refer to the same strategy at the core.

In some cases, these combinations refer to a wider array of multi-leg option strategies beyond just a long straddle. But the simplest form, buying a put and a call on the same stock, is essentially identical to a basic straddle strategy.

The only real differentiation is that a combination seems to imply mixing different option types, while a straddle focuses more on the complementary nature of the put and call options. However, the actual strategy and expected payoff are identical between straddles and straightforward combination structures.

How does Straddle strategy work?

A straddle strategy aims to profit from significant price movement in the underlying security, regardless of direction, through the simultaneous purchase of a put and a call option. It works by giving the trader exposure to unlimited gains if the price moves up or down substantially while limiting the maximum loss to the premiums paid.

To implement a straddle, the trader first identifies an underlying stock they expect to experience a sizable price move leading up to the options expiration date. They then buy an at-the-money call option and an equal number of puts, generally with a strike price close to the current market price of the stock.

The put option gives the trader the right, but not the obligation, to sell the underlying stock at the strike price. It increases in value as the stock price drops below the strike. The call option conveys the right to buy the stock at the strike, becoming more valuable as the share price rises.

Both options expire worthless, and the trader loses the premiums paid if the stock price is between the strike prices of the put and call at expiration. This is the maximum loss scenario.

For the Straddle to be profitable, the stock must move sufficiently from the strike price to exceed the combined premiums of the put and call. This break-even point is the minimum price change required before gains are generated. Any additional upside or downside movement represents potential profit.

As an example, consider a stock currently trading at Rs.50 per share. A trader initiates a straddle by buying one 50-strike call for Rs.200 and one 50-strike put for Rs.200. The total spent on premiums is Rs.400.

The straddle profits if the stock finishes below Rs.49 or above Rs.51 at expiration. Any price between Rs.49 and Rs.51 results in a loss. Below Rs.49, the put option starts gaining value while the call expires worthless. Above Rs.51, the call option gains value while the put expires worthless.

The maximum loss is the Rs.400 paid for the options, but the potential profit is unlimited. Large gains are realized by exercising the profitable leg of the Straddle if the stock plummets to Rs.30 or skyrockets to Rs.70.

The further the price moves from the 50-strike price, the greater the gains. Volatility expansion also increases the options values. Time decay, meanwhile, works against the position, eroding premiums as expiration approaches if the price is stable.

A straddle benefits from selecting the optimum strike price and expiration date. Longer-dated options give more time for the price to move but cost more. The chosen strike price also impacts the total premiums and break-even points.

To close a profitable straddle position before expiration, the trader sells back the appreciating option while leaving the depreciating one to expire worthless. The initial premium paid is recouped on the profitable leg, with any additional option price representing profit.

The straddle strategy carries risks such as time decay on the premiums, selecting unsuitable strike prices or expiration dates, and the stock failure to move enough to exceed the total premium costs. However, it allows traders to profit from volatile price action in either direction. Straddles produce substantial gains when implemented under the right conditions.

What is the importance of Straddle in Options Trading?

Straddles play an important role in options trading by allowing traders to potentially profit from large moves in a stock’s price without having to predict the direction. Their ability to generate gains during periods of high volatility makes straddles a useful tool for certain trading approaches and situations.

Straddles are constructed to benefit from increased volatility and major price swings. This makes them useful when expecting volatile events like earnings reports or economic data releases. Since straddles involve puts and calls, they generate profits whether the stock rises or falls dramatically. This differs from directional trades like calls or puts alone.

The maximum loss on a straddle is the premiums paid for the options. This gives the trade a fixed, capped downside, unlike naked calls or puts, which have unlimited risk. Straddles allow profits from major price swings while outlying less capital than buying the stock outright. The leverage provides a greater percentage of returns on the initial investment.

Rather than buy volatility-based derivatives like VIX products, straddles allow traders to benefit from volatility in specific stocks they analyze. Constructing a straddle position is used to hedge or offset risks associated with holding the underlying stock long-term if volatility is expected.

Straddles give option traders expanded exposure to an asset’s price extremes over a defined period without additional capital outlay. Implementing straddles on certain stocks provides a diversifying options strategy compared to basic calls and puts within a portfolio mix.

Straddles allow participation in the move without picking a side beforehand when uncertain whether a stock will rise or fall. Overall, straddle strategies are useful for traders who want exposure to potential breakouts and volatility spikes, expect a large price swing but are unsure of direction, want to express a view on volatility expansions, or aim to benefit from a coming price extreme.

Straddles are not ideal for range-bound stocks, low-volatility environments, earnings play with uncertain results, or periods of time decay. But when properly deployed, their ability to generate gains from volatility and large price swings makes them an important aspect of an options trader’s toolkit.

Providing defined, capped risks and unlimited upside potential straddles gives traders an excellent mechanism to target profits from major volatility-fueled price movements. Their flexibility and leverage make them a strategically important component of options trading.

What are the different types of Straddle?

There are several variations of the core straddle strategy, which involves simultaneously buying a put and call on the same underlying asset. The different types of straddles are distinguished by their option strike prices, expiration dates, and construction methods.

The 10 main types of straddles are given below.

1. Long Straddle

The basic, traditional Straddle involves buying an at-the-money put and calls with the same strike price and expiration date. It is the most common Straddle, offering unlimited profit potential and capped loss at the cost of the premiums.

2. Short Straddle

This involves writing or selling both a put and call option on the same stock at the same strike and expiration. The trader collects the premiums upfront but has uncapped downside risk if the stock moves substantially in either direction.

3. Zero-Cost Collar Straddle

Also known as a synthetic straddle, this uses a protective put funded through selling a covered call. There is no net debit taken, creating a zero-cost trade. Gains are limited to the upside beyond the call strike.

4. Calendar Straddle

Rather than buying options expiring on the same date, this uses options expiring in different contract months. For example, buying a nearer-term put and longer-dated call, or vice versa. Provides more timing flexibility.

5. Diagonal Straddle

A diagonal straddle combines a long call and a short put or a long put and a short call. The options have different strikes and expiration months. Provides some premium collection.

6. Straddle Spread

Involves buying a straddle while also selling a call and put with farther out-of-the-money strikes. This helps offset the cost of the Straddle through the short strikes but caps upside potential.

7. Strangle

Buys out-of-the-money call and put options with the same expiration. It is cheaper than a straddle due to the OTM strikes but requires a larger price move to profit.

8. Long Strangle Spread

Buys an OTM strangle while shorting a call and puts at even farther OTM strikes. The short strikes serve to reduce the cost of implementing the strangle.

9. Iron Butterfly Straddle

Combines a long straddle with a short strangle, consisting of both an OTM call and an OTM put sold against the straddle strikes. Offsets long straddle costs.

10. Long Condor Straddle

It involves buying a straddle, then selling a call spread and put spread, yielding four total options. The short spreads reduce net costs but also limit the profit potential.

1.Long Straddle

A long straddle is when a trader buys a call and puts it with the same strike price and expiration.

The long straddle profits from substantial price movement in either direction. The call benefits from upside moves above the strike. The pit benefits from downside moves below the strike. Maximum loss is limited to the premiums paid if the stock finishes between the strikes at expiration.

Straddles allow profits from large upside or downside price swings. They have uncapped profit potential from outsized moves. The maximum loss is limited to the premiums paid for the options. Straddles provide leveraged exposure with defined risk.

Straddles require significant price movement to break even. Time decay hurts the position as expiration nears. Straddles have higher complexity than simply buying options or stock. The multiple legs mean high commission costs.

A trader buys 1 XYZ 50 call for Rs.200 premium and 1 XYZ 50 put for Rs.200. The total outlay is Rs.400.The call profits, if XYZ rises above Rs.50.The put profits, if XYZ falls below Rs.50. But if XYZ is between Rs.49 and Rs.51 at expiration, the maximum Rs.400 loss is incurred.

2. Short Straddle

A short straddle is an options strategy where the trader sells a put and call with the same strike price and expiration date.

The trader collects premiums upfront by shorting the put and call options. Maximum profit is capped at the premiums received if the stock price stays between the strikes at expiration. However, potential losses are unlimited if the stock moves significantly above or below the short strikes.

Short straddles generate income from the premiums collected. They do not require a market-directional view. The maximum profit is defined as the premiums received.

Short straddles have substantial downside risks with no upside limit. They require a margin to maintain the short options. Time decay accelerates losses closer to expiration. Early assignment forces stock purchase/sale.

A trader sells 1 XYZ 50 put for Rs.200 premium and 1 XYZ 50 call for Rs.200 premium. Maximum gain is Rs.400 if XYZ is below Rs.50 and above Rs.50 at expiration. However, if XYZ declines to Rs.30 or rises to Rs.70, uncapped losses accumulate from being short the put or call. The short Straddle has a defined maximum gain but unlimited maximum loss.

How does the Straddle strategy perform in the volatility of options?

Straddle strategies are specifically constructed to profit from volatility expansion in the options market. As volatility increases, straddles benefit from the rising value of both the put and call legs. The key is for volatility to drive a substantial price move rather than stagnation.

Higher implied volatility indicates that options are pricing in larger expected moves in the stock before expiration. This expands the value of options, including the puts and calls that make up a straddle.

As actual volatility strikes and the underlying stock makes a sizable price swing, the straddle profits through the appreciating value of whichever option leg aligns with the directional move.

For example, if rising volatility drives the stock higher, the call option becomes profitable while the put expires worthless. In a volatility-fueled decline, the put profits while the call dies off.

The key is for realized volatility to push the stock price beyond the break-even points of the Straddle. Just an expansion in implied volatility alone is not enough – it must be accompanied by a pronounced price move.

Straddles benefit most from directional volatility expansion. The Straddle loses value from time decay if volatility rises, but the stock oscillates in a range. The ideal scenario is a spike in actual volatility coupled with a strong upward or downward swing in the stock.

During earnings releases or economic data reports that cause drastic stock movements, straddle traders aim to capture expanding volatility through sizable price action. Event-driven volatility provides ideal conditions.

The tradeoff is that in low, stable volatility environments, straddles tend to underperform. With the stock pinned to a tight range, both the put and call decay steadily.

So, straddles clearly perform optimally when volatility drives large directional price swings. The unlimited upside potential from runaway moves allows properly structured straddles to generate substantial profits.

However, the trader needs volatility to manifest through significant stock movement rather than stagnation. Avoiding stable but high IV environments and targeting volatile price reactions are key to maximizing results.

How to create a Straddle?

A straddle involves buying both a call option and a put option on the same underlying stock to profit from substantial price movement in either direction. Here are the 8 key steps for constructing a basic straddle.

Select Underlying Stock

Identify a stock you expect to make a sizable price move. Look for potential catalysts like upcoming earnings, events, product releases, etc., that could spark increased volatility. The larger the expected move, the better.

Choose Expiration Date

Determine appropriate options for the expiration date. Give enough time for the anticipated move to potentially occur, but limit excessive time decay. 1-2 months out is common.

Pick Strike Price

Decide on a suitable strike price. Typically, this is at-the-money or close to the current stock price. Higher probability of profitability with minimal directional bias.

Buy Put and Call Options

Buy an equal number of put and call options on the stock at your chosen strike and expiration. Use only as many contracts as you are comfortable with the associated risks.

Monitor Price Action

Monitor the stock closely as expiration approaches, watching for the upward or downward swing needed for the Straddle to become profitable.

Manage Profitable Scenarios

Be prepared to sell the call option to take profits while letting the put expire worthless if the stock moves above the call strike. Sell the put to capture gains while allowing the call to expire worthless if the stock drops below the put strike.

Mitigate Losses

Close the full straddle position to avoid maximum loss of premiums paid if nearing expiration with the stock between strikes. Don’t hold to expiration if the stock fails to move enough for gains; otherwise, the maximum loss will be incurred.

Follow Sound Trading Principles

Avoid overtrading – be selective with stocks, wait for optimum conditions, and give the trade time to play out before adjusting or exiting. Utilise stop-losses on the total position to contain full losses to a predetermined threshold if movement expectations fail. Conduct extensive research before initiating to select suitable stock, strike, expiration, and maximize odds of profitable volatility. Use proper position sizing – don’t risk excessive capital on any single trade. Straddles require sizable moves to profit. Have a plan for managing both profitable and losing scenarios as they develop. React quickly if goals aren’t being met.

How to trade a Straddle?

Trading a straddle requires simultaneously buying a call and putting on the same stock, then actively managing the position as the stock price moves before expiration. Follow these 8 steps to trade using the straddle strategy.

Conduct Research

Conduct research to identify a stock likely to make a sizable price move with an impending catalyst. Look at technicals, fundamentals, upcoming events, earnings, etc.

Initiate Straddle

Choose appropriate strike prices and expiration dates aligned with your outlook. ATM strikes allow price movement in either direction. Expire when expecting the move to occur. Buy equal number of calls and puts at chosen strikes and expirations to establish the Straddle. Use limit orders at suitable entry points.

Monitor Price Action

Closely monitor the stock price movement and any changes in volatility expectations after initiating the Straddle.

Manage Profitable Leg

The call option becomes profitable, while the put loses value if the stock trends up strongly. Prepare to sell the call at a profit. The put option appreciates while the call depreciates if the stock declines considerably. Get ready to sell the put to realize gains.

Mitigate Losses

Use stop-losses on individual legs to protect any profits achieved as expiration approaches. Manage the losing position before expiration to avoid max loss if the stock is flat or oscillating.

Optimal Exits

Buy back the profitable leg gains while letting the loss-making leg expire worthless for optimal exit. Scale-out in portions to take partial profits rather than exiting the entire position all at once.

Avoid Premature Action

Avoid overtrading or prematurely exiting – give the stock time to make its anticipated move. Be willing to roll the position if the move is delayed, but the outlook remains favorable.

Adjust Strategy

Hedge against further losses using spreads if the underlying starts moving contrary to expectations. Record and track the results of each trade to refine the approach and improve future odds of success. Adjust strategy based on changing market conditions and volatility expectations as the trade progresses.

What is the best strategy for Straddle?

The most common and generally the most effective strategy for trading straddles is to use at-the-money strikes for both the call and put legs. ATM straddles balance risk, cost, and probability in an optimal way.

At-the-money means choosing strikes close to the current market price of the underlying stock. This could be strikes slightly above or below the current price but still near that midpoint area.

Using at-the-money (ATM) straddles provides exposure to price movement in either direction. Since the strikes are close to the current value, substantial upside and downside both lead to gains. ATM straddles balance premium outlay relative to probability. ATM options have higher premiums than out-of-the-money options but also have a greater chance of finishing in-the-money at expiration.

ATM straddles set defined maximum risk. Losses are capped at the total premium paid if held to expiration. ATM provides a predictable, fixed-cost basis. ATM straddles require less dramatic price movement. Lower strike distances mean smaller requisite moves for profitability. Easier to exceed break-even points.

ATM options have deltas near 50, giving good price exposure per dollar spent. ATM straddles limit directional bias. With the strikes equidistant from market price, no inherent bullish or bearish tilt exists initially. ATM options benefit from time decay later. ATM decay accelerates closer to expiration if no price change occurs.

The drawbacks of ATM straddles include higher premium outlays and lower leverage compared to out-of-the-money variants. But overall, the balance of risk-reward, cost efficiency, defined risk, and probability of gains makes at-the-money straddles a superior choice in most cases.

Proper stock selection, timing, and active position management ultimately determine success more than strike selection alone. But beginning with ATM strike prices provides a strategically advantageous starting point when deploying straddles to maximize their unique upside potential while minimizing key downside risks.

When is the best time to use the Straddle?

The optimal times to deploy straddle strategies are in periods leading up to expected volatility spikes or significant price movements but with uncertainty in direction. Major events, earnings, releases, and announcements that could cause increased volatility are ideal scenarios.

Leading up to high-profile earnings releases from momentum stocks where the reports could cause drastic price swings, but the direction is unclear based on mixed expectations. A straddle allows playing the volatility in either direction.

Ahead of major events like product launches, FDA decisions, court rulings, regulatory votes, etc., that could have a binary market reaction pushing the stock either much higher or lower depending on the outcome. The unknown outcome makes straddles attractive.

Volatility sharply contracts right before known catalysts, indicating an impending volatility expansion once the news hits, which a straddle captures. The Straddle benefits from the volatility increase.

Around economic data announcements like employment, inflation, or GDP numbers could spark massive uncertainty and equity volatility depending on the results. Straddles profit from the volatility irrespective of direction.

The implied volatility rankings or technical oscillators when they signal a low volatility period for a stock is ending and impending volatility expansion is likely. The anticipated volatility swell favors straddles.

During index or sector-wide volatility, contractions signal calm before potential storms. The Straddle gains from volatility picking up across the index/sector.

The key is anticipating which stocks or situations could cause substantial price movements and volatility clusters. But critically, the direction must be uncertain. Without unpredictability, a simple directional call or put would be superior to a straddle.

In low-volatility environments or sideways trading ranges, straddles tend not to perform as well since they rely on dynamic price movements. Traders deploy them most successfully during periods of expected volatility spikes.

What is the success rate of Straddle?

Due to the complex nature of options trading and volatility, there is no universally accepted success rate statistic for straddle strategies. Their profitability depends on many factors outside the trader’s control. However, estimates generally suggest straddles have an approximate success rate of around 25-35% when properly utilized.

Straddles require substantial price movement in either direction to overcome the premium costs. According to historical data, the underlying stock reaches the breakeven points needed for gains only around one-quarter to one-third of the time on average.

The breakeven points consist of the strike price plus the total premiums paid for the put and call. The Straddle loses money if the stock finishes between these points at expiration. Only a sizable up or down move yields profits.

This dynamic makes straddles risky in stagnant markets and better suited for anticipating volatility. Traders utilize them when expecting a large swing, but the direction is unknown. The low probability of such a perfect combination materializing makes consistent success challenging.

However, skilled traders improve results by applying savvy stock selection, discipline around entries/exits, and prudent position sizing. Those who time straddle well around catalysts and manage risk see higher, though still modest, success rates.

For instance, deploying straddles exclusively ahead of heavily anticipated events known for volatility, like Federal Reserve announcements, push success chances closer to 40-50% for some traders. But mediocre results remain typical.

Loss-cutting rules, like exiting straddles if the stock fails to move 1 ATR within the first half of the duration, also help curtail needless losses from false signals. Adjusting strategy for evolving market conditions further enhances results.

For the majority of active traders, win rates on straddles likely land in the 25-35% area, according to research and observed results. This makes them far from a surefire strategy. Substantial research, timing, and risk management help improve those odds modestly.

Straddles require embracing the reality of occasional large losses as the cost for attaining periodic huge gains when volatility aligns properly. Managing position sizes and maintaining wide stop-losses assists with enduring the inevitability of low win percentages.

How do traders break even for a Straddle?

For a straddle trade to break even at expiration, the underlying stock price needs to move far enough from the strike price to cover the total premium costs of the put and call options. This distance represents the breakeven points.

Specifically, the upper breakeven point is the strike price plus the premium paid for the call and put together. The lower breakeven is the strike price minus the total premiums.

The Straddle returns a profit if the stock finishes outside of this range. The maximum loss of the premium spent occurs if the stock remains between the breakevens.

For example, consider a stock trading at Rs.50. A trader buys a 50-strike call for Rs.2 and a 50-strike put for Rs.2, spending Rs.4 total in premiums.

The upper breakeven point would be Rs.50 + Rs.4 = Rs.54.The call side becomes profitable, offsetting the Rs.4 paid if the stock rises above Rs.54 at expiration.

The lower breakeven point would be Rs.50 – Rs.4 = Rs.46. Below Rs.46, the put option gains value to cover the premium costs.

Between Rs.46 and Rs.54, both options expire worthless, and the Straddle loses the full Rs.4 premium investment. This range must be exceeded to break even.

Four factors impacting the breakeven points are given below.

- Actual stock price – Drastically affects the starting point of the range.

- Strike prices are chosen – ITMs require less movement but cost more. OTMs need bigger moves.

- Time to expiration – More time allows more chance to reach breakevens.

- Implied volatility – Higher IV raises option prices, increasing premium outlay.

To optimize break-even odds, traders balance strike selection with expiration date and premium costs. Longer-dated ATM straddles offer a balance of probability and breakeven positioning.

Actively managing a straddle by rolling, adjusting strikes, or hedging also helps modify the breakevens if it appears they will not be reached initially. Defined exit rules on unprofitable straddles to limit losses from false signals.

Is Straddle profitable?

Yes, straddles are profitable when the trader correctly anticipates an impending period of high volatility, selects suitable options strikes and expirations in advance, and then actively manages the position as the stock makes a substantial move up or down. The unlimited profit potential when volatility aligns with price movement makes straddles capable of generating sizable returns.

However, straddles incur losses more frequently than profits over multiple trades. Because they require significant price movement exceeding the premium paid, they have an inherently low probability of success on any given trade, usually 25-35% historically. Between untimely volatility forecasts and suboptimal expiry/strike selection, straddles face continuous headwinds.

Further, straddles rely heavily on the trader’s discipline to cut losses quickly during adverse moves, while letting winners run when the price action aligns. Poor execution of entries and exits drastically cuts into potential profitability. Even with ideal volatility conditions, the wrong management will turn profits into losses.

Straddles are profitable options strategies when utilized properly, but they rely heavily on timing, volatility forecasting, and active position management. Simply buying a straddle does not guarantee profits.

What is an example of a Straddle strategy?

A straddle involves simultaneously buying a call and putting an option on the same underlying stock to profit from a sizable move in either direction. Here is an example of a straddle trade on a hypothetical stock.

Current stock price: Rs.50

Upcoming binary event: FDA drug approval decision on July 30th

Expected move: High volatility once decision is announced

Trade plan: Leg into Straddle ahead of the event

On July 1st, the trader initiates a straddle by buying 1 call and 1 put on the stock, both with July 30th expiration as given below.

Buy 1 Rs.50 call

Premium paid: Rs.2

Buy 1 Rs.50 put

Premium paid: Rs.2

Total straddle cost: Rs.4 (Rs.2 call premium + Rs.2 put premium)

The Straddle is established at the money to benefit whether the stock rises or falls based on the event volatility.

On July 20th, the stock is still trading at around Rs.50 as the event approaches. The Straddle has not shown signs of profitability yet, as the stock has largely trended sideways.

On July 30th, after the market closed, the FDA approval decision was announced as a rejection of the awaited drug. The stock plunges 35% the next day to Rs.32.50 as the news is absorbed.

At this point, the Rs.50 put option has increased in value with the stock drop and is now deep in the money with substantial intrinsic value. The call has decayed towards zero.

Rather than exercising the profitable put, the trader sells it back into the market at its trading price for a sizable gain, allowing the call to expire worthless.

For example, the put could be closed out at Rs.20, resulting in a Rs.18 profit after initially costing Rs.2. The Rs.2 call premium was lost. This creates a net gain on the Straddle of Rs.16.

The trader successfully benefited from the binary event, causing a volatile downside price swing. By logging into the Straddle early before uncertainty arose, sizable gains were achievable from the explosive bearish reaction.

This example illustrates how a straddle allows capitalizing on major volatility-fueled price moves in either direction. Straddles produce substantial profits from volatile conditions when timed and managed prudently.

What are the advantages of Straddle?

The 10 advantages of Straddle are as follows.

1. Profits from Volatility Expansion

Straddles allow traders to specifically target increased volatility and benefit from the uncertainty it creates. The dual call/put structure profits whether prices rise or fall sharply.

2. Directionally Agnostic

You don’t need to predict which way the price is headed. As long as it moves substantially, the Straddle generates gains from the volatility.

3. Leverage

Straddles provide leveraged exposure to upside and downside price swings. The gains significantly outpace the premium spent to open the trade.

4. Defined and Limited Risk

The maximum loss on a long straddle is simply the total premium paid if held to expiration. This caps and defines the downside.

5. Large Profit Potential

The profitable leg keeps gaining value, leading to a large return on the initial investment if the price move is strong enough.

6. Benefits From Time Decay and Volatility Skew

As expiration approaches, time decay accelerates, and volatility skew develops, improving breakeven points.

7. Balances Bullish and Bearish Exposure

The dual call-and-put structure provides equal exposure to upside and downside price trends.

8. Access to Price Extremes of Underlying

Straddles allow benefiting from the wide price range and extremes a stock reaches during volatile periods.

9. Diversification

Adding straddles to a portfolio of directional trades improves diversification and lowers overall risk exposure.

10. Hedging Application

Straddles are tailored to hedge risks associated with holding the underlying stock long-term.

The advantages of straddles significantly boost a portfolio’s performance and risk-adjusted returns when deployed judiciously at opportune times. The benefits center around embracing volatility and uncertainty.

What are the disadvantages of Straddle?

The potential 10 disadvantages of straddle option strategies that traders should be aware of are given below.

1. Requires Substantial Price Movement

Straddles become profitable only if the underlying stock price moves sufficiently from the strike price to exceed break-even points. Small fluctuations won’t suffice.

2. High Probability of Maximum Loss

Statistically, straddles face a high chance of losing the full amount of premium spent if held until expiration, around 65-75% based on studies.

3. Expiration Time Decay

As time until expiry diminishes, the values of both the call and put decay, working against an unprofitable straddle position.

4. High Commissions on Multiple Legs

The commissions from putting on a straddle with call and put legs are significantly higher than buying options alone.

5. Opportunity Cost of Tying Up Capital

Capital deployed in a stagnant straddle cannot be utilized elsewhere for potentially more profitable positions during that period.

6. Early Assignment Risks

The short options legs of a straddle could be assigned early, forcing the trader into unwanted stock positions.

7. Complex Structure

Straddles involve more moving parts than simple call or put buying, increasing the difficulty of management.

8. Difficult Balance of Timing Entry and Exit

Perfect timing, both entering and exiting straddles, is paramount but challenging to execute consistently well.

9. Requires Close Monitoring

Straddles demand full-time focus and active position management to avoid missed opportunities or losses.

10. Interest Rate Risk

Rising interest rates could increase costs associated with maintaining margin requirements on short straddle options.

While straddles certainly have potential benefits, the nature of their complex structure and probabilities means they also come with substantial risks and downsides. Traders should fully understand these disadvantages before attempting to trade straddles.

How risky is a straddle option?

Straddles involve substantial risks due to their reliance on significant underlying price movement and time decay effects. However, straddles are generally less risky than short iron butterfly spreads when implemented cautiously.

High chance of maximum loss if held to expiration – around 65-75% historically. Requires substantial volatility just to break even. The likelihood of the stock finishing between the strikes results in the total premium spent being lost.

Time decay erodes the position every day, working against the trader. The extrinsic value of the options declines steadily, which creates a headwind.

The opportunity cost of capital being tied up in a potentially stagnant trade. The funds could be deployed elsewhere if the stock fails to move sufficiently.

Adjustment and early exit risks if volatility expectations are wrong. The trader will need to close at a loss instead of waiting for expiration if the price action indicates the initial forecast was incorrect.

In comparison, short iron butterflies involve selling an out-of-the-money call spread and putting spread with the short strikes at the same price. The defined risk comes from the difference between the wing strikes sold and the body strikes purchased.

The capped profit potential is limited to the credit received from opening the trade. Unlike long positions, the maximum gain is fixed upon entry regardless of how favorable the price action becomes.

Uncapped losses beyond the credit amount if the stock price moves outside the wing strikes. While defined risk within the wings, extreme moves above or below create unlimited risk.

Time decay works against the position as expiration nears. As options move closer to expiring, time value erosion hurts short option positions.

Assignment risk on the short option contracts. Early assignment before expiration forces early closure of the trade at suboptimal prices.

Margin requirements to maintain the short positions. The broker will require posting margin to hold the naked short options, tying up buying power.

While short iron butterflies have defined maximum profits, their loss potential is unlimited, making them generally riskier than long straddles, which have defined maximum losses.

However, iron butterflies are less risky in low volatility scenarios, while straddles become extremely dangerous without sufficient volatility expansion. Traders tailor the variants to their outlooks.

Is Straddle a good strategy?

Yes, straddles are good strategies when a trader has high conviction in an impending period of volatility expansion. The dual call/put structure allows profiting from sharp price movements in either direction. The defined and limited risk provides leverage and sizable gains from major swings.

However, for most retail traders, straddles likely pose more risks and difficulties than potential rewards over the long run. The historically low probability of gains for straddles, around only 25-35% per trade, makes consistent success challenging. Between premium decay, untimely volatility, and strike/expiry challenges, profitable straddles remain elusive.

Further, straddles require constant monitoring and adjustment to avoid missing opportunities or letting losses accumulate. This hands-on management and decisive risk control are difficult to maintain over many trades. The complexity also leads to higher commissions and margin needs.

While straddles certainly generate sizable returns and provide defined risk, only well-researched and timed implementation by disciplined traders makes them generally good strategies. Their inherent low win percentages and management needs likely make them inappropriate for casual options traders. As with all strategies, aligning the trade with timing, goals, and risk tolerance is key.

So for the right person under the right circumstances, straddles offer advantages. But for most traders, simpler directional strategies with higher probabilities and fewer variables sometimes prove superior over time. Evaluating individual skills and risk appetite determines if straddles are a “good” personal choice. Their uniqueness presents both positives and negatives depending on the Application.

Is Straddle strategy better than Strip strategy?

Yes, straddles are often superior to strips. They generally provide more flexibility and profit potential compared to strip strategies, making them more favorable in most market conditions. However, strips do maintain some advantages in specific situations.

Straddles allow volatility profits in either direction, while strips rely on directional movement. This makes straddles more robust. Straddles provide unlimited profit potential if the price move is large enough. Strip gains are limited. Straddles allow customization of strike prices and expirations. Strips utilize preset strips defined by the exchange. Straddles are held through expiration. Strips must be closed out prior to the expiration day. Straddles are tailored to a trader’s individual outlook. Strips only allow buying or selling pre-packaged strips.

However, strip strategies do have benefits in some cases. Strips provide clearly defined maximum risk and profit parameters based on the strip details. Strips have favorable commission structures defined by the exchanges that created them. Strips do not require a margin to purchase, unlike short straddles, which need a margin. Strips are simpler with pre-packaged strikes and expirations.

Straddles provide more flexibility for volatility strategies, especially around earnings or events. But strips are easier to implement directionally in trending markets with limited downside and commissions. Depending on the situation, each strategy has advantages that make it preferential.

Is the Straddle strategy bullish?

No, straddle strategies themselves are market-neutral overall and neither explicitly bullish nor bearish. The combined long call and long put structure provides exposure to price movement in either direction without a directional bias.

Straddles do not rely on the market moving higher or lower, just on it moving substantially from the strike price chosen. A long straddle has exposure to whether the stock rallies strongly or sells off sharply.

The dual calls and puts make straddles more contingent on volatility expansion rather than bullish or bearish trends specifically. Their flexible nature allows profits in up markets and down markets if volatility spikes occur.

Five key aspects that keep straddles directionally neutral are given below.

- Buying equivalent calls and puts balances the bullish and bearish exposures.

- Typically initiated at or near the current market price, there is minimal inherent upside/downside tilt.

- Gains are achievable from both rising and falling prices, not just one.

- There is no need to predict market direction; only anticipate if volatility will expand or contract.

- Maximum loss is reached from a sideways, trendless market condition.

The trader’s view on upcoming volatility is more important than their bullish/bearish outlook when deploying straddles. Their flexibility provides utilization in both up and down markets.

A trader creates a directionally biased straddle by using unequal calls and puts, skewing strikes, or combining with other spreads. But in their basic form, straddles themselves contain no structural bullish or bearish lean. They aim to capture volatility, not direction.

What is the difference between Straddle and Strangle strategy?

The main difference between straddles and strangles is the strike prices chosen relative to the current market price of the underlying stock.

Straddles involve simultaneously buying or selling a call and putting on the same stock with the same strike price. The strikes are chosen at or very near the current market price, making them at-the-money options.

For example, if a stock is trading at Rs.50, a straddle would consist of buying a Rs.50 call and a Rs.50 put with the same expiration date.

Strangles also consist of a long call and a long put. However, the strikes are selected equidistant from the market price, making them out-of-the-money options.

Using the same example, if a stock is trading at Rs.50, a strangle might buy a Rs.55 call and a Rs.45 put. Here, the strikes are positioned 5 points above and below the current price.

Straddles use at-the-money strikes, while strangles use out-of-the-money strikes. The closer strikes in straddles increase probability but reduce breakeven requirements. Strangles rely on larger price moves to reach the upside/downside strikes.

Straddles have higher probabilities of profit but also cost more in premiums due to the at-the-money strikes. The higher cost needs bigger returns to break even. Strangles are cheaper but require larger moves.

Strangles require larger price moves to become profitable due to the upside/downside strike distance. The out-of-the-money strikes are farther from the current price. Straddles are balanced between calls and puts, while strangles are skewed directionally depending on the trader’s bias.

Both straddles and strangles benefit from significant price movement but use different strike selection strategies. Straddles focus on at-the-money options while strangles utilise greater out-of-the-money distances between strikes.

Previous Article

Previous Article

49")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 52")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 53")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 54")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 58")

No Comments Yet.