Barrier options are path-dependent derivatives whose value or validity is determined by the underlying asset breaching a predetermined barrier during the contract’s life. Barrier options activate or nullify based on this trigger, offering tailored risk management and typically lower premiums.

Common types include knock-in, knock-out, and rebate options. These contracts are mainly traded over-the-counter by institutions and corporates due to their complexity and need for customization. While barrier options provide cost-efficient, customizable solutions for hedging or speculation, they also involve greater pricing challenges, liquidity risks, and require advanced quantitative modeling.

What Are Barrier Options?

Barrier options are derivatives whose validity or payoff depends on the underlying asset crossing a specified barrier level during the option’s life. Barrier options contract either activates or nullifies if the underlying asset reaches a predetermined price.

Unlike standard (“vanilla”) options that depend solely on the price at expiry, barrier options introduce an extra condition—the barrier—which determines whether the option is live or dead.

The primary purpose of this structure is to provide more customizable risk management or speculative opportunities for the buyer or seller. For example, a bank might issue a barrier option to a client who wants protection only if rates spike or drop dramatically—otherwise, the client prefers a lower premium.

Barrier options are a type of “path-dependent” product; the entire journey of the underlying asset matters, not just the ending.

How Do Barrier Options Work?

Barrier options work by activating or nullifying based on the underlying asset crossing a predetermined price barrier, in addition to the usual strike price feature. The barrier level is a key trigger: if the underlying price hits this point during the contract’s life, the option’s status changes.

Barriers is sometimes monitored either continuously (at every moment) or only at expiry, depending on how the contract is written. This monitoring frequency affects both the risk profile and the premium.

For example, a continuously monitored barrier will be easier to breach and thus will typically result in a cheaper option compared to one only checked at expiry.

Key components of a barrier option include the below.

- Strike price: The agreed price at which the right to buy or sell is exercised.

- Barrier level: The specific price that triggers activation (knock-in) or nullification (knock-out).

- Knock-in or knock-out feature: Determines if the option becomes valid (“knock-in”) or invalid (“knock-out”) when the barrier is breached.

- Call or put type: Specifies whether the right is to buy (call) or sell (put).

For example, consider a knock-out call option with a strike at Rs. 100 and a barrier at Rs. 120. If the underlying asset price ever touches Rs. 120, the option ceases to exist—even if the price later drops. This structure allows advanced risk management, enabling users to reduce cost by accepting conditional protection or participation.

What Are the Types of Barrier Options?

Barrier options are divided into three types based on how the barrier alters the contract’s activation or cancellation. The three main families are knock-in options, knock-out options, and rebate options, each serving a distinct purpose.

1. Knock-In Options

Knock-in options are barrier options that only become active if the underlying asset breaches a specified barrier level during the option’s life. This means the option holder gains the rights of the contract only if a significant market event occurs—otherwise, the option expires worthless and the premium paid is lost.

Knock-in options are particularly useful for investors who want to participate in the market only if a notable price movement takes place. There are two main types:

- Up-and-in: The option activates if the asset price rises above the barrier (e.g., a stock climbs from Rs. 500 to breach a barrier at Rs. 550).

- Down-and-in: The option activates if the asset price falls below the barrier (e.g., a currency pair drops below Rs. 82 in a USD/INR contract).

This structure allows buyers to reduce upfront costs, as knock-in options are generally less expensive than standard (vanilla) options. The lower premium reflects the fact that protection or participation only starts after the barrier event, which may never occur.

For example, a company hedging oil prices might use a down-and-in put to only insure against drastic declines, thus saving on hedging costs if mild fluctuations are not a concern.

2. Knock-Out Options

Knock-out options are barrier options that become void if the underlying asset breaches a specified barrier level at any time before expiry.

In other words, if the asset price touches or crosses the barrier—even once—the option is immediately cancelled and the holder loses their rights, although a rebate might be received in some structures.

Knock-out options are attractive to investors and hedgers seeking lower-cost exposure compared to vanilla options. The knock-out feature essentially places a cap on the possible payout, allowing buyers to pay a reduced premium. There are two principal types.

- Up-and-out: The option is cancelled if the price rises above a certain barrier (e.g., a stock’s price hits Rs. 1,200, knocking out a call option).

- Down-and-out: The option is cancelled if the price falls below a certain barrier (e.g., a currency falls below Rs. 80, knocking out a put option).

These structures are valuable when the investor believes the underlying will stay within a certain range.

For example, an exporter might use a down-and-out put option to protect against moderate declines in currency value but avoid paying for protection if the currency collapses below a critical threshold.

3. Rebate Options

Rebate options provide the holder with a predetermined cash payment if the barrier is breached and the main option is rendered inactive. This feature is designed to soften the financial blow of a knock-out event, offering partial compensation when the primary protection or payoff disappears.

In standard barrier options, being knocked out results in the total loss of the premium and any potential payoff. Rebate options, however, return a fixed sum—often set at a fraction of the initial premium or a negotiated amount—if the barrier is hit. This structure is especially appealing in volatile or unpredictable markets, where sudden price moves might nullify protection at the worst possible moment.

Rebate options add a layer of complexity to both pricing and risk management. The value of the rebate must be included in the option premium calculation, and the likelihood of a barrier breach must be carefully modeled. These contracts are most often used in over-the-counter (OTC) markets, allowing for customization based on the client’s risk tolerance and financial goals.

Choosing the appropriate type helps users create highly targeted risk profiles for various market conditions and needs.

What are Examples of Barrier Options in Action?

Real-world examples show how barrier options deliver tailored outcomes in different market situations. These instruments are commonly used by corporates, institutional investors, and traders for both hedging and speculation.

- Up-and-out Call Example: Suppose an investor buys a call option on a stock at a strike price of Rs. 1,000, with an up-and-out barrier at Rs. 1,200. If, at any time before expiry, the stock touches or exceeds Rs. 1,200, the option becomes void—even if the price later falls below Rs. 1,200. If the barrier is not breached and the stock ends above Rs. 1,000, the payoff is like a standard call. This is popular for investors who want upside, but only if the market doesn’t surge past a certain point.

- Down-and-in Put Example: A company worried about a sharp drop in commodity prices buys a down-and-in put with a strike at Rs. 80 and a barrier at Rs. 70. The put becomes active only if prices fall to Rs. 70, providing protection against severe drops but at a lower premium.

- Rebate Option Example: An exporter buys a knock-out option with a rebate of Rs. 10,000. If the barrier is breached and the contract is nullified, the exporter receives the rebate as partial compensation.

Visualizing these scenarios on payoff diagrams shows how the option’s value “jumps” or “drops” at the barrier, making the risk/reward profile much different from vanilla options.

Why Use Barrier Options in Trading?

Barrier options are favored in trading for their ability to deliver tailored risk management, cost advantages, and innovative hedging strategies. The structure of these options allows market participants to align financial protection or speculation with specific market conditions.

- Tailored Risk Control: Barrier options help investors precisely define the conditions under which they receive a payoff or lose coverage. This is particularly useful when certain price levels represent significant business or investment risk.

- Lower Premiums: Because the payout is conditional, barrier options are often much cheaper than equivalent vanilla options. For example, a knock-in option will only pay out if a large move occurs, allowing buyers to reduce upfront costs.

- Custom Hedging: Corporates and financial institutions use barriers to hedge exposures with custom triggers, such as protecting cash flows only if currency rates breach critical levels. This is especially useful for exporters, importers, and companies with large foreign currency transactions.

- Structured Products: Investment banks frequently include barrier options in structured products, combining them with vanilla options to create unique payoff profiles for clients.

Barrier options also allow traders to express views on volatility, correlation, and market direction in more nuanced ways than vanilla options.

How Are Barrier Options Priced?

Barrier options require more advanced pricing methods than vanilla options due to their path dependency and conditional triggers. Standard models like Black-Scholes are insufficient because barrier options depend on whether the underlying asset hits certain levels during the contract’s life, not just the ending price.

- Monte Carlo Simulations: Simulate thousands of potential price paths to estimate the likelihood of barrier breaches and final payoffs.

- Binomial Lattice Models: Build a tree of possible price movements, checking at each node whether the barrier has been crossed.

- Modified Black-Scholes Models: Adjust traditional models to factor in the probability of hitting the barrier, often using partial differential equations.

Key factors affect pricing.

- Volatility: Higher volatility increases the chance of crossing the barrier, reducing the value of knock-out options but increasing knock-in value.

- Barrier Proximity: The closer the barrier is to the current price, the more likely it is to be breached, affecting premium.

- Time to Maturity: Longer durations give more time for the barrier to be hit.

- Interest Rates: Influence the present value of expected payoffs, as with all options.

Accurate pricing demands robust quantitative tools and calibration to current market data. Inaccurate modeling introduces substantial risk for both buyers and issuers.

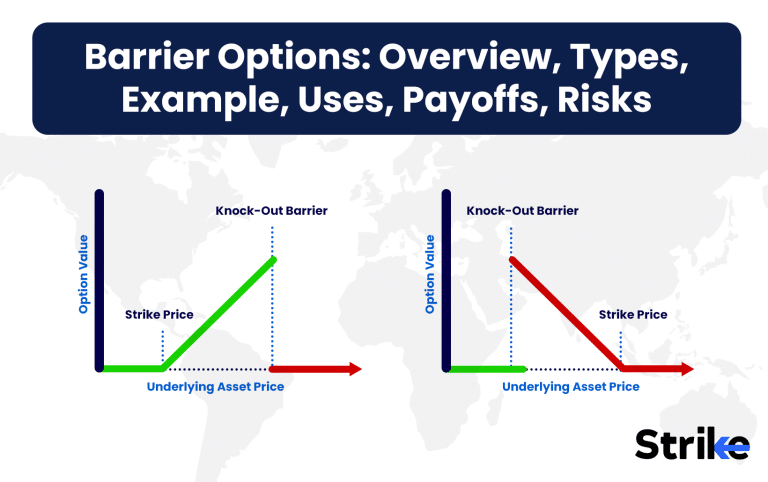

What Are the Payoffs of Barrier Options?

The payoff from a barrier option depends on whether the underlying asset breaches the barrier during the option’s life, resulting in a structure different from vanilla options. Path dependency is key: the journey, not just the destination, matters for payout.

- Up-and-In Call: No value unless the price rises above the barrier; if breached, behaves like a standard call. Payoff = max(Spot – Strike, 0) if barrier is breached; otherwise, zero.

- Down-and-Out Put: Standard put payoff unless the price falls below the barrier, in which case the option is extinguished. Payoff = max(Strike – Spot, 0) only if barrier is not breached.

- Rebate Option: If the option is knocked out, the holder receives a pre-agreed fixed rebate, regardless of where the underlying finishes.

- For an up-and-in call, the payoff graph is zero until the barrier is breached, after which it mirrors a vanilla call.

- For a down-and-out put, the payoff follows a vanilla put until the barrier, where it drops abruptly to zero.

- For a rebate, the graph shows a sudden payout at the barrier breach, rather than at expiry.

These structures allow users to match option payoffs to particular risk scenarios, often at a lower cost or with more targeted coverage than vanilla contracts.

What Are the Risks of Barrier Options?

Barrier options come with significant risks, including complexity, liquidity issues, pricing challenges, and exposure to market manipulation. Their path-dependent nature makes them less transparent and harder to hedge than standard options.

- Complexity: Understanding the payoff structure requires advanced financial knowledge, making them unsuitable for most retail investors. The exact risk profile can be unintuitive, with sudden changes in value near the barrier.

- Limited Liquidity: Most barrier options are OTC products, and the secondary market is thin. This makes it difficult to exit or adjust positions quickly.

- Barrier Manipulation: In illiquid markets, the underlying can be pushed toward the barrier by large traders, deliberately or inadvertently, triggering or nullifying the option.

- Valuation Difficulty: Sudden volatility spikes or market jumps increase the difficulty of pricing and risk management, as standard models may not capture real-world price jumps.

- Knock-Out Timing: Being knocked out just before expiry can mean losing all potential value, even if the underlying moves favorably afterward.

These risks require robust controls, counterparty credit assessments, and frequent revaluation. Institutional users often demand detailed scenario analysis before entering such contracts.

What’s the Difference between Barrier Options vs Vanilla Options?

Barrier options differ from vanilla options in structure, risk profile, liquidity, and pricing, as summarized below.

| Feature | Vanilla Options | Barrier Options |

| Structure | Simple call/put | Activation or nullification on barrier |

| Payoff Profile | Only expiry price matters | Path-dependent; barrier is key |

| Pricing | Black-Scholes model | Advanced (Monte Carlo, binomial, etc.) |

| Liquidity | High, exchange traded | Lower, mainly OTC |

| Transparency | High | Moderate to low |

| Premium | Higher | Often lower due to conditional payout |

| User Base | All investors | Mainly institutions, corporates |

| Risk | Well-known | Complex, subject to sudden value change |

| Accessibility | Widely available | Custom, negotiated OTC |

Barrier options provide more customization but at the cost of complexity and potential risk.

Is Barrier Options an Exotic Options?

Yes, barrier options are classified as exotic options because their structure, payoffs, and risk characteristics significantly differ from standard vanilla options. Exotic options are defined by their non-standard features, such as dependency on the price path, additional triggers, or multi-asset linkages.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 33")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.