A box spread is a neutral, low-risk options strategy that involves a long call spread and a long put spread simultaneously on the same underlying asset. A box spread aims to take advantage of small mispricing discrepancies between different option strike prices.

To construct a long box spread, a trader buys a near-term in-the-money (ITM) call, sells a further out-of-the-money (OTM) call, buys a near-term OTM put, and sells a further OTM put. All options must have the same expiration dates. This combination creates a range between the long put and short call strikes, within which the position earns a profit regardless of price movement.

For example, ABC stock is at Rs. 100. A trader buys the Rs. 95 calls, sells the Rs. 105 calls, buys the Rs. 90 put, and sells the Rs. 110 put expiring in 3 months. The net profit arises from the intrinsic value difference between the calls and puts if ABC closes between Rs. 90 and Rs. 105. The maximum gain is limited but comes with very low risk due to the virtual elimination of directional exposure.

The main benefit of a box spread is its high profit likelihood due to intrinsic value convergence at expiration. It requires minimal capital to enter and maintains positive cash flow if held to maturity. However, transaction costs eat into profits for small mispricings. Tight closing of markets also poses risks if positions cannot be easily unwound.

What is the Box Spread (Long Box) strategy?

The box spread, also known as a long box, is an options trading strategy that consists of a bull call spread and a bear put spread on the same underlying asset with the same strike prices and expiration dates. The Box Spread (Long Box) strategy aims to profit from virtually risk-free arbitrage opportunities.

: Definition, How it Works, Trading Guide, and Example 7")

A box spread is constructed by buying a bull call spread and selling a bear put spread on the same security with the same strike prices and expiration dates. The bull call spread involves buying a call option with a lower strike price and selling a call option with a higher strike price, while the bear put spread involves selling a put option with a higher strike price and buying a put option with a lower strike price.

The long box strategy profits from differences in implied volatility between call and put options. It capitalizes on put-call parity, which defines the relationship between call and put prices based on the principle that synthetic positions using calls, puts, and the underlying security should have identical values. Any price discrepancies violate put-call parity and are exploited for riskless profits through the long box.

To initiate the long box strategy, the trader buys a call with a lower strike price, sells a call with a higher strike price, sells a put with a higher strike price, and buys a put with a lower strike price, all with the same expiration date. The distance between the strike prices is equal.

The long call and short put positions combine to mimic a long position in the underlying, while the short call and long put mimic a short position. This effectively creates a synthetic long and short position and locks in a risk-free arbitrage profit.

As expiration approaches, the options converge to their intrinsic values, yielding a profit to the long-box trader. This predetermined profit is equal to the difference between strike prices minus the net premium paid or plus the net credit received when initiating the trades.

For example, consider an underlying stock trading at Rs.50. A trader constructs a long box by buying the 40-strike call for Rs.10, selling the 60-strike call at Rs.1, selling the 60-strike put for Rs.1, and buying the 40-strike put for Rs.10. The cost to initiate the trade is zero (a net credit received of Rs.10 – Rs.1 – Rs.1 + Rs.10 = Rs.18).

At expiration, the 40-strike call expires in the money and is worth Rs.10. The 60-strike call expires worthless. The 60-strike put expires worthless. The 40 strike put expires in the money and is worth Rs.10. So the trader’s total profit is Rs.20 (the difference between strikes) minus the net Rs.0 premium paid, for a total profit of Rs.20.

The key advantages of a long box spread are virtually risk-free and guaranteed profit due to arbitrage, along with defined and limited risk. However, the upfront capital required is extensive to establish each component leg of the trade. Trading fees also eat into the potential profits.

How does Box Spread work?

The box spread involves simultaneously buying and selling calls and puts with the same expiration date but different strike prices to lock in a near risk-free profit when options are mispriced relative to the underlying security.

: Definition, How it Works, Trading Guide, and Example 8")

Specifically, the box spread is constructed by buying a bull call spread and selling a bear put spread on the same underlying asset with the same strikes and expiration. The bull call spread involves buying a call with a lower strike and selling a call with a higher strike. The bear put spread involves selling a put with a higher strike and buying a put with a lower strike.

The purchase of the call spread and sale of the put spread is executed for a net credit or debit. The goal is for the transactions to result in a net credit received. This nets out the need for any upfront capital required to initiate the trade.

The premia received from selling the call spread is used to finance the put spread purchase. The distance between the strike prices determines the predefined profit at expiration. This is calculated as the strike price differential minus any net debit paid upfront when initiating the trade.

As expiration approaches, the options converge toward their intrinsic values specified by the strike prices. This intrinsic value is what the trader pockets as the arbitrage profit.

For example, consider a stock trading at Rs.50. A trader initiates a box spread by buying the 40 strike call for Rs.10, selling the 60 strike call for Rs.1, selling the 60 strike put for Rs.1, and buying the 40 strike put for Rs.10.

The net result is a Rs.0 debit to enter the trade (credit of Rs.10 – Rs.1 – Rs.1 + cost of Rs.10). The distance between the strike prices is Rs.20. This represents the arbitrage profit the trader will realize at expiration, regardless of where the stock ends up trading.

On the expiration date, there are 3 possible scenarios, which are given below.

Provided that the stock price is below 40, then the 40 strike call and put expire worthless. The 60-strike call expires worthless. The 60-strike put expires in the money with Rs.20 of intrinsic value. The trader’s net profit is the Rs.20 intrinsic value of the put less the Rs.0 net debit paid, for a profit of Rs.20.

Suppose the stock is between 40 and 60. The 40 call expires in the money, while the other options expire in worthlessness. For example, at Rs.50, the 40 call has Rs.10 of intrinsic value. The profit again is Rs.20 – Rs.0 = Rs.20.

Or else when the stock is above 60, the 60 calls and 40 puts expire in the money. The 60 call has Rs.10 of intrinsic value, and the 40 put has Rs.20. Net profit remains Rs.20.

No matter where the stock ends up at expiration, the trader pockets the Rs.20 arbitrage profit locked in by the box spread structure. This predetermined payout is received regardless of which options finish in the money. The strategy has no upside beyond the arbitrage profit and no risk of loss beyond any net debit paid.

The key to making the box spread work is put-call parity. This defines the relationship between put and call prices based on the principle that synthetic positions using the calls, puts, and underlying security should have identical values. Any price discrepancies violate put-call parity, allowing for arbitrage profits.

The box spread exploits temporary put-call mispricing, providing traders virtually risk-free opportunities to lock in profits. However, trading fees and commissions eat into the arbitrage gains. Significant capital is required to fund each component leg. And the limited profit potential caps the reward scenarios.

What is the importance of the Box Spread in Options Trading?

The box spread is an important options trading strategy because it allows traders to lock in virtually risk-free arbitrage profits. Properly executing a box spread is one of the few ways traders are able to generate guaranteed profits regardless of market conditions.

The box spread profits from put-call parity arbitrage opportunities. Put-call parity defines the relationship between put and call premiums based on the principle that synthetic positions using the calls, puts, and underlying security should have identical values. It violates put-call parity, allowing for arbitrage profits when options are mispriced relative to the stock price.

The box spread is structured to capture these arbitrage opportunities and capitalize on mispriced options. By combining long and short positions in calls and puts, the box spread locks in a virtually risk-free profit when options are incorrectly priced. This guaranteed payout is rare in trading and makes the strategy invaluable.

The box spread has a defined maximum risk, which is limited to the net debit when establishing the position. The simultaneous long and short call and put positions offset, protecting against unlimited losses. Regardless of the extent of movement in the underlying stock, the maximum loss for most traders is limited to the upfront net premium paid.

This known and capped risk allows traders to precisely size positions without exposure to uncontrolled losses. The limited downside and locked-in upfront profit provide traders with rare clarity in an uncertain trading environment.

Rather than uncertain potential profits, the box spread offers a fixed return predefined at the outset before market changes occur. The built-in arbitrage opportunity locks in a specific profit amount the trader knows they will capture at expiration, barring any trading costs.

This definitive profit target helps traders confidently execute the strategy while reducing uncertainty. The locked-in payout is unaffected by which options finish in the money at expiration.

The box spread has relatively low margin requirements compared to other arbitrage strategies. The defined risk parameters allow brokers to offer reduced collateral requirements. This frees up trading capital for other opportunities.

Since the box spreads profits from arbitrage, it has an extremely high probability of success when constructed properly. The mispricing providing the profit opportunity will eventually be corrected, enabling the trader to capture the arbitrage.

This contrasts with speculative directional or volatility strategies that have uncertain outcomes. The box spread offers reliable, high-probability profits when the options are mispriced just right.

Box spreads generate profits in volatile markets and stagnant low-volatility environments. As long as options are mispriced, arbitrage profits are extracted. This makes the strategy valuable across diverse market conditions.

The market-neutral box spread provides diversification for portfolios concentrated in directional risk strategies. The arbitrage approach acts as a hedge, offsetting losses from other trades. This diversification improves risk-adjusted returns.

How to construct a Box Spread Strategy?

A box spread is also known as a long synthetic future. The box spread is constructed by buying a bull call spread and selling a bear put spread on the same underlying asset with the same expiration dates and equidistant strike prices to synthetically replicate buying or selling the underlying forward. The goal is to create a position that mimics buying or selling the underlying asset forward at a certain price. This strategy allows traders to profit from low volatility in the underlying asset.

To construct a box spread, first choose the underlying asset you want to trade, like a stock, index, or commodity. Then, determine your market outlook – whether you think the underlying will trade higher or lower by the options expiration date. Based on this, decide if you want to simulate a long position (buying the underlying forward) or a short position (selling it forward).

Next, pick the expiration date and strike prices to use. For optimal results, choose front-month options with at least 45 days to expiration to minimize time decay. The strikes should be equidistant from the current price of the underlying. For example, you could use a 45 strike for the put spread and a 55 strike for the call spread if the current price is Rs.50.

To simulate a long position, you would buy a bull call spread by purchasing a call option with the higher strike (55) and selling a call with the lower strike (45). You fund this vertically by selling a bear put spread, selling a put with the lower strike (45), and buying a put with the higher strike (55). The premium collected from the put spread will offset the debit for the call spread.

For a short position, it is the reverse – you sell a bear call spread (short 55 calls, long 45 calls) and buy a bull put spread (long 55 put, short 45 put). Again, the put spread premium will cover the call spread debit.

The key is matching the distance between the call and put strikes so the net debit/credit is zero. This creates a synthetic long or short position similar to owning the underlying futures contract outright.

You want the call and put spreads to expire at the same time with equal spreads so you are not exposed to directional risk from the underlying asset. The max profit is locked in upfront from the net credit or debit when initiating the box. Profit is realized if the underlying finishes between the call and put strikes at expiration.

Managing the position involves closing the box spread as one trade before expiration. You take profits early or roll the position further out in time if needed. Box spreads have defined risk, so losses are capped at the difference between the call and put strikes minus any net credit received.

When is the best time to use a Box Spread?

The optimal time to employ a box spread strategy is when you expect implied volatility in the underlying asset to decline or remain relatively low through expiration. Since box spreads profit from stable low volatility prices, entering when IV is high almost guarantees the options will lose value, capping your potential profit. Ideally, you want to initiate the box when implied volatility is at or near the lower end of its historic range.

Several signals indicate good box spread entry points from an implied volatility perspective, first, by observing the IV rank or percentile versus recent history. IV rank under 25% often signals optimal conditions, meaning current implied volatility is in the bottom quartile of the past 12 months readings. Likewise, an IV percentile under 30 indicates relatively low volatility expectations priced into the options.

You also gauge entry timing using metrics like a stock’s HV20 or the VIX volatility index. HV20 under 30 suggests lower volatility anticipated in the near term, while a VIX reading under 12 indicates overall options market volatility is depressed. Even better is when the VIX is testing 52-week or all-time lows, signaling extremely muted volatility expectations.

From a technical analysis lens, lower volatility periods often coincide with tight trading ranges and directionless price action. So, entering box spreads when the underlying is consolidating near key support/resistance levels or moving sideways in a narrow range is advantageous. You want to avoid initiating strong trends when prices are exhibiting wide daily swings.

In terms of fundamental catalysts, times of low earnings, economic data releases, central bank announcements, and other scheduled events tend to foster subdued volatility as uncertainty recedes. The summer months, when trading volume dries up or year-end holidays, are also conducive to stabilization and low IV.

In essence, you want to deploy box spreads when volatility appears “too low” based on the converging signals above. This maximizes the edge of profiting as IV means reverting higher or remaining muted through option expiration.

The consequences of implementing box spreads when volatility is too high are detrimental. It will boost option premiums across the board if implied volatility rises significantly after entry. This prevents the short- and long-term option spreads from converging by expiration, capping the possible gain.

Worse, if volatility spikes sharply, it could completely blow up the trade. The short options could expand rapidly while the long options offsetting them lag behind, creating substantial losses. Box spreads rely on non-directional volatility compression to be profitable. Surging IV skews the risk versus reward against you.

Likewise, entering box spreads too late when volatility has already started to rise will cut into potential profits. Ideally, you want to log into the call and put spreads with IV at the lower end of its range rather than on the upswing. Chasing after volatility already looks to be rising is not optimal.

How to exit the Long Box Spread strategy?

The optimal time to exit a long box spread prior to expiration is when a predetermined profit target is reached, the underlying price breaches either side of the call/put strike range, implied volatility rises materially, liquidity dries up, losses mount, an expiration rollover is needed, or major fundamental news/events necessitate sidestepping potential volatility expansion.

One exit timing indicator is when the box spread has reached your predetermined profit target. For example, you have the option to buy back the position at a profit of Rs.0.80, locking in the majority of the maximum gain if you structured the box to collect a net Rs.1 credit per share/contract. Some traders will close out half the position at a 50% profit level as part of scaling out.

Monitoring the underlying asset price between the call and put strikes. It signals the box spread is at greater risk of finishing out of the money if the price breaches either side of this range. For instance, if you established a long box between the Rs.45 and Rs.55 strikes, you would look to exit if the underlying asset price closed below Rs.45 or above Rs.55.

Relatedly, look to close the box if implied volatility in the options begins to expand rapidly. Rising IV boosts extrinsic value and impacts the convergence between the call and put spreads, especially if an earnings event or major announcement is approaching. It’s better to lock in a profit early before volatility crushes it.

Whenever the box spread falls substantially into a loss, that also signals it is time to cut bait and close the position. For example, the loss worsens by holding into expiration if you collect a Rs.1 credit initially, but the trade then moves to a Rs.0.30 debit. Sometimes, it is best to realize the loss and free up capital rather than face a greater downside.

Closing the box spreads well before expiration if liquidity in the options starts drying up. Thinly traded options become tough to leg out of at reasonable prices, so a lack of open interest or volume is a warning sign. Give yourself enough time to unwind the call and put spreads if liquidity disappears.

Rolling the box spread further out in expiration is another alternative to closing if implied volatility looks ready to spike higher in the short term. Maintaining the structure but pushing out the expiration to give volatility time to mean revert lower again. This avoids realizing a loss but delays the profit potential.

Finally, fundamental news or events related to the underlying asset spur early box spread exits. It warrants closing the box spread to sidestep potential volatility expansion if a major surprise announcement like an earnings shock or regulatory decision seems imminent.

The biggest risk in holding a box spread too long is increased volatility, disrupting the convergence between the call and put spreads. Letting options get too close to expiration also reduces flexibility to adjust or roll the position. Exiting at the first signs of volatility expansion or liquidity shortfalls preserves profits captured from the long box spread.

Should I let a Box Spread expire?

Yes, you should usually allow box spreads to expire in order to realize the maximum profit. The key benefit of these strategies is locking in a fixed return by buying and selling options to create a net credit or debit at the onset. As long as the underlying asset finishes between the call and put strike prices, the box spread is profitable at expiration.

There are some specific scenarios where closing a box spread out prior to expiration is optimal. For example, it skews the balanced risk profile by inflating short option premiums faster than longs if implied volatility rises substantially after initiating the trade. In this case, it is prudent to lock in profits before a predefined IV expansion threshold is breached.

Likewise, if the underlying asset trends are strongly outside the call/put strike range well before expiry, it signals a greater probability of finishing out of the money. Suppose you have strikes at Rs.45 and Rs.55, but the price trades above Rs.60; closing early is wise. This gives you the flexibility to avoid max loss.

Liquidity risk also necessitates early box spread closure at times. You get squeezed out at unfavorable prices near expiration if bid-ask spreads widen considerably or volume dries up as expiration nears. Exiting before illiquidity hits retains flexibility and allows you to exit at reasonable levels.

Cutting at a partial loss makes sense versus giving back all initial credit received if holding to expiry means realizing large losses. Salvaging some premium is preferable to max loss.

Finally, upcoming binary events that boost implied volatility rapidly warrant early box spread closure to avoid vega exposure. Time decay acceleration in the last weeks before expiration will also non-linearly erode the remaining time value quickly, hurting longer-dated options. Monitoring theta decay speeds is prudent.

Overall, though, the advantage of the box spread is fully capitalizing on time decay and stable low implied volatility through expiration. Letting the options converge within the profit zone is the most efficient way to realize the maximum gain.

Unless faced with the risks above, it is generally prudent to hold the box spread to the final settlement. Doing so allows the short options to expire worthless while the offsetting longs retain value.

Trying to time exits adds market timing risk and transaction costs from bid-ask spreads. The best risk-adjusted play typically sticks it out into expiration if IV ranks stay low and the stock holds within its expected range.

What is the potential maximum loss for the Box Spread strategy?

The maximum potential loss on a box spread is defined as the difference in strike prices between the long and short call/put spreads minus any net credit received when initiating the position. This defined risk is one of the main advantages of box spreads versus other multi-leg option strategies.

The potential loss is equal to the difference between the strike prices of the long and short call spreads minus any initial net credit received when putting on the trade.

For example, the maximum loss would be 5 points (50 strike long call – 45 strike short call) minus any net credit from the put debit spread if you construct a long box by buying a call spread at 50 and selling a call spread at 45.

The total margin required and max loss is just 3 points, calculated as the spread width of 5 minus the 2 points collected if the box was established for a net credit of 2 points.

This limited risk occurs because the long and short call spreads move conversely, offsetting losses on each side. Even if the stock drops below the range of strikes at expiration, the short 45 call spread loses value to offset the declining long 50 call spread.

The only scenario where max loss is realized is if the underlying asset closes exactly at the short call strike at expiration. In that case, the short call spread expires worthless, while the long call spread loses the full 5-point width.

But any finish below the lower short call strike results in the same max loss, as both call spreads to expire worthless, and the put spread is in the money by the width. The loss cannot exceed the defined amount at trade inception.

For a short box spread, the max loss maths works the same but in reverse. For example, shorting the 50 call and going long the 45 call, then the max loss is 5 points minus any net debit paid when entering the trade.

Here, max loss occurs if the stock closes precisely at the higher long call strike at expiration. The long call spread finishes in the money by the full 5 points while the short call spread above expires worthless.

In essence, the max loss equals the difference in call/put strikes, offset by any net credit or debit. It represents the risk of the underlying stock finishing outside the call/put spreads at expiration.

However, the loss cannot exceed this defined amount because the dispersed strikes act as a hedge, limiting risk. The most the long and short call spreads lose is the distance between them.

For optimal loss mitigation, many traders will close box spreads at 50% of max loss. So, in the example above, with 5 points of risk, they exit at a 2.5-point loss. This caps loss at the half while still giving the trade room to profit on volatility compression.

How important is implied volatility in the Box Spread strategy?

Implied volatility is extremely important when trading box spreads as the strategy relies on relatively low and stable IV, or compression through expiration, to profit from the convergence between the long and short call and put spreads. Taking advantage of relatively low and stable IV is key to profiting from these volatility-defined trades.

Box spreads involve simultaneously buying and selling calls and puts at different strikes but equal spreads. To be profitable, the options must expire worthless or retain value in a very narrow range. This happens when the IV decreases or remains compressed through expiration.

Higher implied volatility boosts extrinsic option premiums across all strikes. This prevents the call and put spreads from converging optimally. The short options widen more than the long options, skewing the risk-reward profile.

For example, the short call spread expands significantly while the long call lags behind if a long box spread is initiated when IV is 25% and it rises to 45% into expiration. This disparity curtails the potential profit.

Worse, a sharp volatility spike could upend the entire strategy. The rapid premium increase in the short options could lead to runaway losses faster than the longer options offsets. Box spreads on stable, muted volatility.

Traders want to deploy box spreads when IV appears relatively low or at least has limited upside. Metrics like IV rank/percentile, HV20, and VIX levels provide clarity on current expectations.

Ideally, the IV rank is below 25%, HV20 is under 20, and the VIX is testing 52-week lows. Historical volatility should also be declining over the past 30 to 90 days. Entering when volatility looks rich virtually guarantees option values decay.

Rolling the box spreads further out in time helps if a volatility swell is expected in the near term. This maintains the structure while avoiding realizing losses, allowing IV to stabilize again later.

It is also essential to avoid earnings, major announcements, and other binary events that rapidly increase implied volatility ahead of expiration. The vega risk associated with post-event IV spikes crushes profits.

What is the impact of the time decay in the Box Spread strategy?

Time decay, or theta, has a significant impact on box spread positions and must be carefully managed. Since box spreads involve both long and short options, the nonlinear erosion of extrinsic premium near expiry helps or hurts, depending on direction. It generally benefits long box spreads through steady erosion of short option premium but hurts if acceleration near expiry is greater in the long options, while short boxes need amplified theta drain and vega compression into expiration to maximize profits.

For long box spreads, the gradual time decay is beneficial as expiration approaches. The steady drain of extrinsic value in the short call and put options boosts the overall profit potential.

As the short options bleed theta, they are more likely to expire worthless, while the longer call and put retain more intrinsic value. This convergence within the profit zone is the goal. However, the acceleration of time decay during the last month before expiry also works against long box spreads. The final weeks see a nonlinear acceleration in theta drain.

It closes the gap in profitability if this occurs substantially faster in the long term. Faster erosion of extrinsic premium in the long call/put negates the gains from short option decay. So, while time decay generally aids long box spread positions, the trader still has to be mindful of the closing time frame. Managing early to lock in profits if convergence stagnates avoids leaving money on the table.

For short box spreads, time erosion is detrimental overall, leading up to expiry. Since these strategies profit from the short strikes expiring worthless, any retention of extrinsic value hurts.

Gradual theta decay minimizes profit if the short options still hold a non-zero premium into expiration. This prevents them from finishing out of the money as intended.

The ideal scenario for short boxes is a sudden crash in implied volatility into expiry. This amplifies downward vega pressure and extrinsic drain just before settlement.

Of course, the trader cannot predict if such a favorable volatility term structure will develop. It requires proactive management, like rolling the short box further out if theta decay remains muted with weeks left.

Thoughtful timing of entries and management of rolls is key. Since box spreads have defined risk, early action to defend profits in light of unfavorable time decay is prudent. Mastering theta directionality and impact is critical for trading these volatility-based option strategies.

Is hedging a Long Box Spread strategy recommended?

No, hedging is generally not necessary for long box spread positions. One of the main benefits of these strategies is defined as capped risk. Additional hedges usually only reduce potential profit while adding complexity and costs.

Long box spreads are structured to maximize gains from non-directional low volatility. The dispersed long and short strikes hedge each other, limiting potential losses. The maximum risk is known upfront at the trade’s inception.

As long as the underlying asset finishes between the call and put strikes at expiration, the box spreads profits. Even large upside or downside moves outside this range only forfeit the calculated maximum loss.

Given the built-in loss definition, adding further hedges like ratio spreads or VIX calls is typically redundant. These defenses just erode profits while the long box spread already controls drawdowns alone.

However, hedges are utilized if implied volatility spikes sharply after trade entry. Surging IV skews the max loss equation by disproportionately inflating short option premiums. This swings the risk profile negatively.

In cases of extreme volatility expansion, pairing the long box with a put ratio spread or negative delta call fly cushions against vega sensitivity. The hedge offsets rising IV’s damage to the short call and put spreads.

But for most stable, range-bound conditions, hedging only dampens the upside. The exceptions are black swan events risking large volatility term structure shifts late in the trade. Here, selective hedging is prudent to defend profits.

Hedging long boxes is generally unnecessary and only advisable as a form of tail risk management in periods of extreme vega dislocations. Otherwise, the deliberate construction of box spreads already provides its own loss protection.

Is it possible to adjust a Box Spread strategy?

Yes, it is possible to make adjustments to box spreads, but adjustments are not always necessary or advisable.

Rolling the expiration date further out is an adjustment to consider for box spreads if implied volatility is rising into the near-term expiration. This allows more time for volatility to revert back lower again. It also retains the original structure while capping risk through the new expiration date.

Widening the call and put spreads is prudent if the underlying price seems poised to break out above or below the original call/put strike range. This widening provides more room for the asset to fluctuate without hitting max loss prematurely before expiry.

The box spreads are adjusted into a conversion or reversal position to align with the emerging trend if the underlying trend starts trending directionally. This requires careful legging to shift from calls to puts or vice versa while maintaining the box integrity.

The box spreads are partially unwound early, like closing out half the position to lock in some profits and reduce outstanding risk exposure. This partial unwind enhances the overall risk-adjusted return profile.

Finally, new offsetting box spreads are layered on to counterbalance delta exposure if the price moves outside the initial strike range. While complex, this effectively hedges the downside through new boxes.

However, adjustments like the above incur additional transaction costs from bid-ask spreads and commissions. They also require precision timing and execution to properly leg in/out of adjusted positions.

For many stable, low-volatility conditions, it is prudent to leave box spreads alone rather than complicating them with adjustments. The key advantage of these trades is defined as manageable risk.

Unless faced with extreme circumstances like the underlying price crashes or implied volatility spikes, adjustments are generally unnecessary. It is preferable to accept the known max loss in most cases.

Adjustments can be set in fine-tuned box spreads but also introduce added risks and costs. Static box spreads with no adjustments tend to yield the cleanest risk-reward profile if implemented properly at the outset. Only make adjustments to defend the downside.

How do traders profit from a Box Spread?

Traders are able to profit from box spreads by taking advantage of the convergence or divergence between the long and short call/put spreads as expiration approaches. The goal is for the dispersed options to expire worthless or retain value in a very narrow range.

For long box spreads, the structure profits as the short call and puts options decaying in value into expiry during the long call and retaining intrinsic value. This convergence within the profit zone between the strike prices allows the trader to close or expire the spread at the maximum credit received.

Short box spreads profit from the opposite effect – the expiration of the long call/put spreads out of the money while the short strikes decay and expire worthless. Again, the trader pockets the initial debit taken to establish the trade.

Both long and short boxes benefit from stable muted volatility that compresses option premium differentials. As IV declines or remains low, short options lose extrinsic value faster than long options. This expands profit potential.

So, box spreads do not rely on the directional movement of the underlying asset to generate profit. The dispersion of the call and put strikes hedges delta exposure. Gains stem from non-directional volatility compression over time.

For this reason, box spreads tend to be highly profitable and consistent income-generating strategies for options traders. They have defined risk, a high probability of success if structured properly, and benefit from theta decay and vega premium erosion.

The key is deploying box spreads when implied volatility appears relatively low or at least poised to decline further into expiration. This magnifies the edge in profiting from time and volatility decay. Avoiding earnings events and other catalysts is also crucial.

Careful construction, timing, and management are still essential to avoid risks like directional breakouts, IV spikes, and liquidity constraints near expiry. Within controlled conditions, box spreads reliably produce consistent income from vega and theta decay, offering an attractive risk/reward profile.

What is the success rate of the Box Spread?

Executed properly under optimal conditions, box spreads are able to achieve a success rate of over 85-90%. This high probability of profit depends on 7 key factors such as implied volatility, time decay, technical range, etc. They are given below.

Initiating box spreads when IV rank/percentile is low, in the bottom quartile of its range, maximizes the edge for volatility compression into expiry. High IV distorts the risk profile.

Managing box spreads to avoid sharp acceleration of time decay in the final weeks and days guards against the erosion of extrinsic premium.

Avoiding earnings announcements, economic data releases, and other catalysts that spur IV spikes limits vega exposure risk.

Underlying price consolidation between support and resistance improves the odds of finishing between strike prices. Trends breaking out skew risk.

Sufficient open interest and volume enable easy legging in/out. Thin liquidity makes closing spreads challenging.

The box spread structure itself hedges through offsetting call and put strikes. Caps and quantifies max loss at the outset.

Proactively monitoring price action, volatility signals, time decay, liquidity, and closing trades early when necessary to both maximize profits and minimize losses.

In essence, the high win rate depends on an ideal confluence of volatility technical, fundamental, and behavioral factors. Traders must implement and manage box spreads at optimal times across the right underlying and expirations.

Even then, the condensed risk profile still has vulnerabilities – namely unforeseen volatility spikes, premature time decay, and illiquid options. So, the ~90% historical win rate is not a guarantee.

Poor structuring, sloppy execution, and inattentive management easily turn profitable box spread conditions into losers. The success rate quickly declines without rigorous analysis and discipline.

In controlled environments where volatility appears pegged at relative lows, box spreads offer a reliably profitable options strategy. But this high win rate relies on ideal criteria and proactive optimization. It is far from an “easy win” strategy if not implemented prudently across the box spread’s lifecycle. The devil is in the details with these spreads.

What are the advantages of the Box Spread strategy?

The box spread offers traders 6 key advantages as an options strategy. They are given below.

Defined Risk Profile: The construction of box spreads using both long and short call/put spreads limits and quantifies maximum losses. The dispersed strikes act as a hedge, capping risk at the spread width. This differs from short naked options, which have unlimited risk. Knowing the full risk parameters ahead of time allows for prudent position sizing.

Higher Probability of Profit: Box spreads to profit from stable low implied volatility into options expiration, which is a frequent market condition. Their non-directional nature means they do not rely on predicting underlying price moves. This results in consistently high win rates, around 85%, when deployed in optimal low-volatility environments.

Benefits from Theta Decay: Box spreads aim to capture profits as time decay erodes the extrinsic premium, especially in the short call-and-put options. This convergence, catalyzed by theta, boosts the overall profit potential into expiration. The gradual erosion of time value aids box spread returns.

Benefits from Vega Decay: Because box spreads thrive on muted volatility, declines or stability in implied volatility also increase profit probability. Lower IV results in a greater loss of extrinsic value in the short options. Vega decay amplifies gains uniquely available to box spread strategies.

Consistent Income Generation: The positive expectancy from a high probability of success combines with defined risk parameters to make box spreads reliable income generators. They sustainably produce monthly yields above buy-and-hold returns in calm, stable markets.

Decreased Role of Market Timing: Since box spreads do not rely on market direction predictions, traders avoid risks associated with perfect entry and exit timing. They simply need volatility to remain contained over the trade period. This simplifies trading decisions.

Box spreads provide defined risk profiles, high probabilities of profit, leveraged theta and vega decay benefits, consistent income generation, and decreased reliance on market timing when optimally implemented in low-volatility environments.

What are the disadvantages of the Box Spread strategy?

While box spreads offer advantages like defined risk and high probability, they also come with some inherent disadvantages and vulnerabilities. 7 key disadvantages are given below.

Vulnerable to Volatility Spikes: Box spreads rely on stable, low implied volatility to thrive. Significant volatility spikes outside expectations create substantial losses, skewing the balanced risk profile. Surging IV has an outsized impact on short-option spreads.

Liquidity Risk: The need to simultaneously leg into four options across call and put spreads requires sufficient liquidity. Thin markets increase slippage costs and widen bid-ask spreads. Lack of volume makes closing spreads challenging near expiry.

Strict Selection Criteria: Proper underlying strikes and expirations fitting the stable volatility criteria significantly narrow the pool of actionable setups. This limits opportunities relative to directional trades with more flexibility.

Precise execution Needed: Entering and exiting box spreads requires precision timing and legging to accurately adjust positions. Even slight missteps throw off the balanced convergence and negatively alter payoff odds.

Increased Commission Costs: The minimum of four spread legs involved with box spreads increases broker commissions relative to straightforward directional trades. More contracts and precision legging amplify transaction costs.

Acceleration of Time Decay: While theta decay generally aids box spreads, its nonlinear acceleration near expiry works against positions. The complexity of balancing time erosion across four options must be monitored.

Tax Treatment Complications: Box spreads involve both long and short positions across multiple options for an extended duration. This blended tax treatment requires thorough accounting and potentially multiple filings.

Box spread’s advantages do not emerge without proper structuring, timing, execution, and risk management. Volatility spikes, illiquid options, and accelerated time decay represent the main threats traders must actively mitigate to harvest box spread profits successfully. The strategy also requires precision trading, which is not suitable for all retail options investors.

What is an example of a Box Spread strategy?

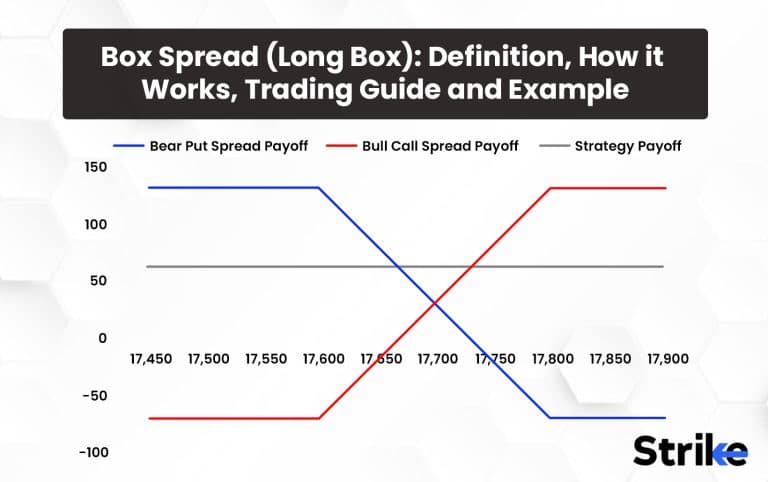

A long box spread is one of the most common and basic box spread structures. It involves buying a bull call spread while selling a bear put spread on the same underlying with the same expiration dates and equidistant strike intervals.

: Definition, How it Works, Trading Guide, and Example 9")

With the stock at Rs.50, buy a Rs.55 call for Rs.2, sell a Rs.45 call for Rs.4, sell a Rs.45 put for Rs.2, and buy a Rs.55 put for Rs.4. This creates a bull call spread funded by a bear put spread at the same strikes. The Rs.4 put credit offsets the Rs.4 call debit, so the total entry cost is zero.

This creates a bull call spread by going long for the higher strike call and short for the lower strike call. This is funded by selling a bear put spread, short the lower strike put and long the higher strike put.

The total debit to enter the trade is zero, as the Rs.4 credit received from the put spread offsets the Rs.4 debit paid for the call spread. This locks in the maximum profit upfront.

The goal is for the stock to finish between Rs.45 and Rs.55 at expiration. In this case, the short 45 calls and puts expire worthless while the long 55 calls and puts retain their intrinsic value of Rs.5, the width of the spreads.

The maximum loss is defined as Rs.5 (the spread width) if the stock finishes below Rs.45 or above Rs.55. This risk is mitigated by the dispersion of the long and short strikes, which hedge each other.

The profit potential is maximized when implied volatility declines or remains low going into expiry. This increases the likelihood of the short options expiring worthless while the long options retain value.

Is the Box Spread strategy bullish?

No, box spreads are neither inherently bullish nor bearish strategies. They utilize a market-neutral framework to isolate profits from volatility compression and time decay. The direction of the underlying asset price is mostly irrelevant.

Box spreads take positions across both calls and puts simultaneously, dispersing risk through a range of strikes. This limits directional exposure and relies on the options expiring worthless or retaining value in a very narrow zone.

Since the box spread trader profits from vega and theta decay regardless of market direction, there is no outright bullish or bearish bias embedded in the structure. The only “bias” is for volatility to decline or remain muted into expiry.

Both long and short box spreads are established across the exact same strikes and expirations to capitalize purely on time and volatility erosion. The directional effect is negligible as long as the underlying remains range-bound.

The trader focuses solely on volatility and expiration dynamics, not predicting up or down moves. There is no need to forecast direction, only stability. This market-neutral framework differentiates box spreads from most other option strategies.

However, adjustments like rolling untested short strikes lower or Call/Put conversions introduce directional tilts to box spreads. But in their basic form, box spreads have negligible delta exposure.

So while adjustments are possible to make box spreads directionally biased, their core structure and profit mechanics rely on non-directional volatility and time decay. This market-neutral advantage offers unique opportunities for volatility-focused traders across any market environment.

Is Box Spread profitable?

Yes, box spreads are highly profitable options trading strategies when implemented correctly under optimal market conditions. Their unique structure provides several inherent advantages.

The combined long and short call and put spreads in box spread hedge each other, limiting potential losses to the width between the strike prices. This caps and quantifies maximum risk at the outset.

Box spreads are structured to thrive in low-volatility environments, which occur frequently in most markets. Their non-directional nature means that accurately predicting the underlying price movement is not required.

Time erosion of extrinsic premium accelerates into expiry, boosting profits as the short call and put options in the box decay faster. Stable or declining implied volatility aids this via vega compression.

The above-average probability of success combines with defined risk parameters to make box spreads reliable monthly income generators uncorrelated to markets.

However, the profitability relies heavily on proper structure, timing, execution, and active management of risks. Neglecting any of these key tenets turns potential profits into losses. Volatility spikes, illiquid options, and outsized directional price trends represent the main threats.

Within the right low-volatility conditions and expertly implemented, box spreads offer high-probability profitable setups for options traders. However, their non-directional nature requires specialized expertise and monitoring. Done well, box spreads generate consistent income – done sloppily, they underperform.

What is the difference between a Box Spread and a Bull Call Spread?

The main difference between box spreads and bull call spreads is that box spreads are non-directional strategies that benefit from time/volatility decay, while bull call spreads are directionally bullish strategies betting on upside price movement.

Box spreads involve simultaneously buying a call spread and selling a put spread, disclosed into four total options positions. This market-neutral framework profits from vega/theta decay as options expire worthless or retain value in a narrow range.

Bull call spreads purchase call options at a higher strike while shorting calls at a lower strike to fund the trade. The maximum gain occurs if the underlying rallies above the higher strike at expiration. A directional view is required.

Box spreads have defined and capped risk quantified at the outset. The dispersed strikes hedge each other to limit losses. Bull call spreads face uncapped risk if the stock crashes below the lower short strike.

While bull call spreads rely on rallying prices for profit, box spreads simply need the underlying to hold stable within the call/put strike ranges into expiry. No directional forecasting is involved.

Bull call spreads face timing challenges regarding entry and exit points to maximize gains. Box spreads are entered when volatility appears relatively low, with minimal timing requirements beyond that.

Bull call spreads benefit from rising volatility, boosting call premiums across the curve. Box spreads, conversely, need to be muted, with stable volatility for the short options to decay.

Finally, bull call spreads involve basic two-leg directional structures easily accessible to most option traders. Box spreads require advanced knowledge to structure properly and actively manage into expiration.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 16")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 17")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 18")

: Overview, 10 Types of Indicators, Settings for Different Markets 19")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 22")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 25")

No Comments Yet.