Synthetic options are powerful tools in modern trading, allowing investors to replicate the payoffs of other financial instruments using combinations of standard options contracts. Synthetic options have become an essential part of the options landscape, offering flexibility, capital efficiency, and innovative ways to express market views or manage risk.

The concept of synthetics dates back to the development of options pricing theory in the 1970s, when traders and academics realized that specific combinations of calls, puts, and the underlying asset could create positions with identical risk and reward profiles.

This insight laid the groundwork for advanced hedging, arbitrage, and speculative strategies that remain popular today.

What is a Synthetic Options?

A synthetic option is a combination of two or more standard options positions that replicates the payoff of another financial instrument, usually a stock or another option. A synthetic option is achieved by carefully selecting options with specific strikes and expiries to mirror the price movement and risk profile of the desired underlying asset.

By constructing synthetics, traders mimic long or short stock positions, or even other option strategies, without actually owning the underlying security.

The idea is rooted in the principle of financial equivalence, where different combinations of options and underlying positions deliver the same risk and reward outcomes.

Synthetics are central to options pricing theory and are widely used by professional traders for hedging, arbitrage, and capital efficiency.

For instance, a “synthetic long stock” consists of buying a call and selling a put at the same strike price and expiration, which behaves just like owning the stock itself.

The popularity of synthetic options stems from their flexibility and the ability to gain exposure or hedge positions without transacting in the underlying asset.

This approach is especially attractive in markets where direct short selling faces restrictions or borrowing costs, making synthetics a powerful tool in both retail and institutional portfolios.

What are The Types of Synthetic Options?

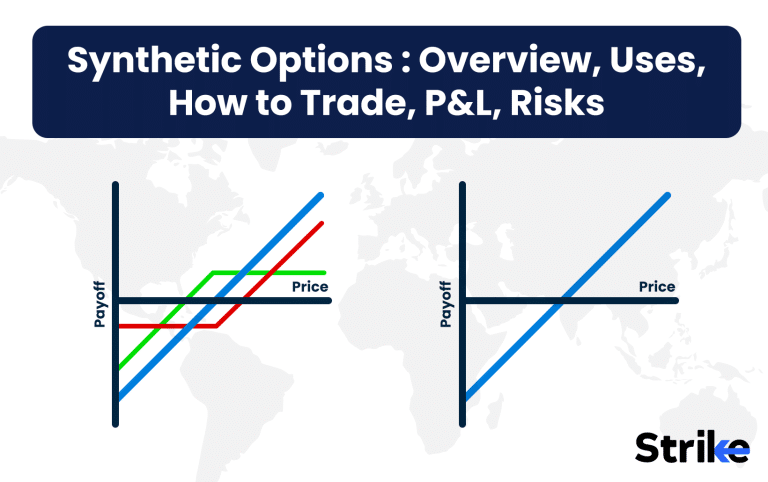

The types of synthetic options are synthetic long stock, synthetic short stock, synthetic long call, synthetic short call, synthetic long put, and synthetic short put.

1. Synthetic Long Stock

A Synthetic Long Stock position is created by combining a Long Call option and a Short Put option with the same strike price and expiry. This combination replicates the payoff of owning shares, providing gains if the stock rises and losses if it falls, just like holding equity.

However, the margin required for this options setup is much less than what is needed to buy the actual stock, making it a capital-efficient alternative.

For instance, in Apollo Hospital (lot size: 125 shares), initiating a Synthetic Long Stock costs ₹160,225, while buying 125 shares in the cash market would require ₹8,83,000. This substantial difference allows traders to gain exposure to the stock’s upside at a fraction of the capital outlay.

The position behaves almost exactly like an equity holding for the duration of the options contract, with profit and loss profiles closely mimicking actual share ownership.

The attached payoff chart would show a straight diagonal line, identical to the equity curve, confirming that this setup is effective for those looking to replicate stock holding without tying up large amounts of capital.

This strategy is particularly useful for traders seeking stock-like exposure over a short period or for those who want to save capital for other opportunities.

2. Synthetic Short Stock

Synthetic Short Stock is constructed by pairing a Long Put option with a Short Call option at the same strike and expiry, thereby replicating the payoff of a short position. In Indian markets, carrying forward a short stock position is generally not allowed beyond intraday, so traders often use futures for positional shorts.

The Synthetic Short Stock setup provides a capital-efficient and flexible alternative, as the margin required is typically less than that for a short futures position.

For Apollo Hospital (lot size: 125 shares), the Synthetic Short Stock costs ₹140,266, compared to ₹1,54,000 for a short futures contract. This means traders save on margin requirements while achieving the same profit and loss exposure as shorting the stock via futures.

The resulting payoff is a mirror image of a long stock position, where profits accrue if the stock falls and losses occur if it rises.

A payoff chart for this position would mirror the short futures payoff, sloping downward as the stock price increases. This strategy is valuable for traders seeking to benefit from a decline in stock price without the higher margin or restrictions of futures contracts.

3. Synthetic Long Call

A Synthetic Long Call is achieved by combining a long futures contract (or an equity holding) with a Long Put option of the same expiry and lot size. Since representing equity on payoff graphs is less straightforward, traders prefer using futures to create this structure.

The Synthetic Long Call mimics the classic Long Call option payoff: unlimited upside with limited downside.

In practice, a trader might buy a 2-month Apollo Hospital futures contract (expiry: 26 June) and simultaneously purchase an ATM Put option with the same expiry.

For example, buying 1 contract at ₹8,764.5 and a Put at the same strike for ₹350, with a lot size of 75. The maximum loss is capped at the premium paid for the Put, calculated as ₹314.5 × 75 = ₹23,587.5 (rounded to ₹23,588). The breakeven point is the futures buy price plus the put premium (₹8,764.5 + ₹350 = ₹9,114.5).

This structure simulates the payoff of a Long Call, providing the trader with unlimited profit potential above the breakeven and strictly limited loss, making it an effective hedge or speculative tool.

4. Synthetic Short Call

Synthetic Short Call is constructed by combining a short futures position with a Short Put option of the same strike and expiry. Since Indian markets restrict holding short equity positions overnight, traders use futures for carrying short exposure.

Adding a Short Put to the short futures creates a position that replicates the payoff of a plain Short Call.

The payoff profile for this strategy, as shown in the attached chart, mimics that of a Short Call: it profits if the underlying stays at or below the strike but suffers unlimited losses if the stock price rises sharply. The position is exposed to significant risk on a major rally, as there is no long option for protection.

This setup is useful for traders who want to receive premium income and are willing to take the risk of a rally in the underlying, with all the benefits of margin efficiency that synthetic positions offer.

5. Synthetic Long Put

Synthetic Long Put is created by pairing a short futures position (since equity shorting is only allowed intraday in India) with a Long Call option of the same strike and expiry. This construction mimics the payoff of a standard Long Put, which benefits from a falling market and has limited downside.

The payoff profile resembles a classic Long Put: capped loss (limited to the premium paid for the long call) and significant profit potential if the underlying falls. This setup allows traders to simulate being long a Put using futures and options, offering capital efficiency and the ability to maintain a bearish position beyond a single trading day.

This method provides a practical way to gain downside exposure with a safety net, especially when actual Put options are illiquid or expensive.

6. Synthetic Short Put

Synthetic Short Put is achieved by combining a long equity position with a Short Call option at the same strike and expiry, effectively replicating the payoff of a Short Put. This structure allows the trader to collect premium income while being exposed to the risk of the stock falling below the strike price.

The position profits if the stock stays at or above the strike, just like a traditional Short Put, but losses accrue if the price drops significantly. This strategy is commonly used by those willing to acquire shares at a lower price or who already own the stock and seek additional income via option premium.

This synthetic approach is popular for its margin efficiency, as the combination faithfully mimics the payoff and risk profile of a naked short put but with the added flexibility of using existing equity holdings.

These strategies use combinations of options, futures, and equity to replicate the payoff profiles of standard option positions.

Why Use a Synthetic Options Strategy?

Synthetic options strategies are used to achieve similar financial outcomes as direct positions in a more capital-efficient or flexible manner. One major advantage is the reduction in capital requirements, since synthetics often require less margin than buying or shorting the actual stock.

Traders also use synthetics to replicate positions that are otherwise difficult or costly to access, such as shorting illiquid stocks or gaining exposure in markets with high regulatory barriers.

These strategies allow participants to avoid the complications of physical stock delivery or the need to borrow shares, which can be cumbersome or expensive.

Hedging is another key motivation, as synthetics permit precise management of risk against underlying price movements without altering the core holdings in a portfolio. Synthetics also empower traders to express volatility or directional views with leverage, amplifying both the potential returns and the associated risks.

Advanced investors frequently deploy synthetic strategies to exploit pricing inefficiencies between the options and the underlying, especially in volatile or fast-moving markets. This flexibility, combined with the potential for tailored risk exposures, makes synthetic options a staple in sophisticated trading arsenals.

When to Use a Synthetic Options?

Synthetic options strategies are best employed when you want directional exposure but seek capital efficiency or face trading constraints. For example, a bullish or bearish bias in a security, combined with the desire to avoid tying up large amounts of capital, makes synthetics ideal.

Traders often turn to synthetics in high volatility environments or illiquid equity markets, where direct trading in the underlying stock is either impractical or excessively costly. Synthetics also become especially useful when shorting the actual stock isn’t possible, whether due to regulatory rules, scarcity of borrow, or other limitations.

Strategic portfolio hedging is another situation where synthetics shine, as they offer flexibility in adjusting exposures without altering existing positions. Investors in derivatives-rich markets utilize synthetics for both tactical and strategic adjustments, tailoring their risk profiles to changing market conditions.

How Option Greeks Affect Synthetic Options?

Option Greeks directly influence the risk and reward profile of synthetic positions, mirroring the characteristics of the replicated position.

Delta, for instance, tracks the sensitivity to the underlying’s price changes; a synthetic long stock will have a delta close to +1, just like the actual stock.

Gamma, which measures how delta changes with the underlying price, is determined by the time left until expiration and the specific options used. Synthetics built from options with the same expiry usually exhibit lower gamma than at-the-money single options but still react dynamically as the underlying price moves.

Theta, representing time decay, varies with the structure—synthetic stock positions might be neutral or slightly negative, depending on the net premium paid or received.

Vega, which measures sensitivity to volatility, is generally lower for synthetics compared to outright long or short options, making them less reactive to volatility spikes.

How Implied Volatility Affects Synthetic Options?

Implied volatility (IV) plays a critical role in synthetic options because their payoff assumes options are fairly priced relative to the underlying. Entering a synthetic position when IV is high or low affects both the cost of establishing the position and the risk-reward profile.

The timing of entry becomes crucial, as misaligned IV levels can lead to mispricing, making it either more expensive or less profitable to use a synthetic instead of the actual asset. Implied volatility (IV) skew—where different strikes have varying implied volatilities—may further distort the equivalence between the synthetic and the real position.

Sophisticated traders exploit these discrepancies for arbitrage or volatility trading, profiting when the synthetic is mispriced relative to its theoretical value. However, success relies on accurate pricing models and swift execution, as market forces quickly eliminate obvious arbitrage opportunities.

How to Trade using Synthetic Options?

To trade with synthetic options, first define your directional view.

Ultracemco has been selected as the underlying stock to deploy a synthetic long put strategy due to a bearish outlook. Since positional shorting is not allowed in the equity segment on NSE, the short leg is established using a futures contract. The payoff diagram focuses only on futures and options, excluding the equity segment.

Next, select matching strike prices and expiry dates to align with your view. In this setup, the current month’s futures contract is shorted at ₹11,421, and an ATM call option with a strike of ₹11,400 is bought for ₹130. This creates a synthetic long put—functionally similar to a standard long put strategy.

The synthetic put mimics a bearish position where gains occur as the stock price falls. The strategy is defined-risk on the upside with theoretically unlimited profit potential on the downside. The breakeven point is calculated as: Futures Price − Call Premium = ₹11,421 − ₹130 = ₹11,291.

Maximum loss is capped and equals the time value in the call option. The intrinsic value of the ₹11,400 call is ₹21 (i.e., ₹11,421 − ₹11,400). So the time value is ₹130 − ₹21 = ₹109. With a lot size of 50, the total max loss equals ₹109 × 50 = ₹5,450.

As long as the price expires below ₹11,291, the strategy begins to generate profit. Below this breakeven point, the profit potential increases sharply with further declines in the stock price.

What are the Maximum Profit & Loss, Breakeven on a Synthetic Options?

Maximum profit and loss for synthetic options depend entirely on the specific structure employed, mimicking the payoff of the position being replicated. For example, a synthetic long stock (long call, short put at same strike) has unlimited upside and theoretically unlimited downside, precisely like owning the stock.

Breakeven for this position occurs at the strike price plus or minus any net premium paid or received when setting up the synthetic. Payoff diagrams visually represent these outcomes, showing how profit and loss evolve with changes in the underlying’s price.

What are the Risks of Synthetic Options?

The primary risks of synthetic options include assignment risk, execution complexity, margin requirements, and potential mispricing or slippage. Assignment risk is particularly prominent for short options, which may be exercised at any time, potentially forcing you into unexpected positions.

Execution complexity arises because synthetics require multiple legs, so partial fills or execution delays can alter your intended exposure. Margin requirements are often higher than for single-leg options, reflecting the increased risk and potential for rapid losses if the market moves against you.

Mispricing between the synthetic and the actual position can erode profits or even create unintentional losses, especially in less liquid or volatile markets. Finally, if the underlying moves sharply against your bias, synthetic options will incur losses just as quickly as the real position they replicate.

Is Synthetic Options Strategy Profitable?

Yes, a synthetic options strategy is profitable when the market moves in the direction anticipated, just like its underlying equivalent. The strategy’s profitability depends on correct forecasting, efficient execution, and appropriate management of transaction costs and slippage.

Synthetics yield additional profits if pricing inefficiencies exist. However, competition and market efficiency usually limit these opportunities, making most profits contingent on directional accuracy and tight execution.

Is Synthetic Options Bullish or Bearish?

Synthetic options strategies can be either bullish or bearish depending on their construction. For instance, a synthetic long stock is bullish, while a synthetic short stock position is bearish.

The flexibility of synthetics allows traders to express any market view by adjusting the combination of calls and puts. This adaptability is one of the primary reasons why synthetic strategies are so widely used in options trading.

What are Alternatives to Synthetic Options Strategy?

Alternatives to synthetic options strategies include outright purchases of stocks or options, vertical spreads, covered calls, protective puts, and using derivatives like options on futures or ETFs. Each alternative offers different risk-reward profiles, capital requirements, and flexibility.

Vertical spreads, for example, limit both potential profit and loss, making them suitable for defined-risk trading. Covered calls and protective puts combine stock and options for enhanced income or downside protection, while derivatives on futures or ETFs open up additional markets and instruments for more advanced strategies.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 48")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 49")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 50")

: Overview, 10 Types of Indicators, Settings for Different Markets 52")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 54")

No Comments Yet.