Covered call writing is an options trading strategy used to generate income from stocks owned by the trader. With this strategy, the trader sells or “writes” call options against stocks in their portfolio and receives a premium upfront. A covered call means the trader agrees to sell the underlying stock at a specified price, known as the strike price, any time before the expiration date.

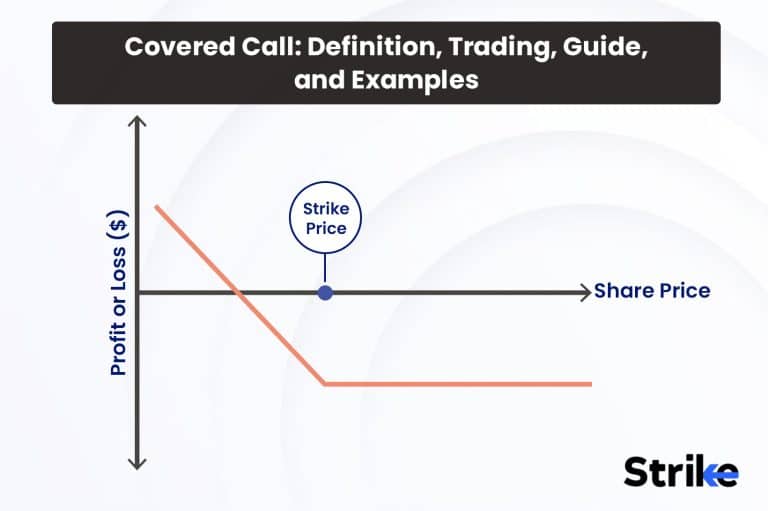

The goal of covered call writing is to generate a steady income through call premiums collected while holding the underlying stock. For this strategy to work, the trader “covers” their short call position by actually owning the number of shares that are sometimes called away if the calls are exercised. This limits the risk since the maximum loss is capped at the difference between the strike price and the current stock price. However, the trader has to forgo potential upside gains beyond the strike price.

Covered calls are best used in a relatively flat or mildly bullish market. By setting the strike price above the current stock price, call writers generate premium income as long as the stock stays below the strike on expiration. However, the shares will be called away, eliminating any further upside, if the stock price rises above the strike. Still, the premium provides downside protection and a defined risk level ideal for more conservative investors.

What is a Covered Call?

A covered call is an options strategy that income investors employ to generate income from the stocks they hold. A covered call allows an investor to buy a stock and write (sell) call options on that same stock in order to generate income from the premium received. The call options give the option buyer the right, but not the obligation, to buy the stock from the covered call writer at a predetermined price, known as the strike price, by a specific expiration date.

There are a few key characteristics of covered calls that define how they work. First, the investor must own the underlying stock before writing the call option against it. This is what makes the position “covered” – the investor delivers the shares if the option is exercised. The premium received from writing the call provides immediate income to the covered call writer. The investor agrees to sell their stock at the strike price in exchange for this premium if the call option is exercised.

However, the maximum profit potential is limited with a covered call because the stock will only be called away (exercised and sold) at the strike price or below. Any stock price appreciation above the strike is left on the table and not realized as profit. On the other hand, the covered call writer’s downside risk is reduced compared to just holding the stock since they receive the premium upfront. Another factor is that not all calls will necessarily be exercised. The calls expire worthless, and the shares are not called away if the stock price stays below the strike at expiration.

Investors employ covered calls primarily for their income-generation potential. The premiums received offer attractive yields, especially on high-dividend stocks that have call options traded on them actively. However, the strategy does cap upside profit potential. It is best suited for income investors who are happy to generate steady premium returns as long as the stock remains range-bound and not volatile. It allows participation in stock price appreciation, just not at levels higher than the strike.

All options, including covered calls, have an expiration date. This introduces time decay as a factor that favors the covered call writer. It becomes increasingly less likely to be exercised as the option nears expiration if it is out of the money (stock below strike). This causes the option premium to erode or decay over time. The covered call writer benefits from this by collecting the premium upfront but facing less risk of assignment (the option being exercised) the closer it gets to expiration.

Taxes must also be considered with covered calls. The premiums received are treated as short-term capital gains by the IRS since options expire annually when writing call options. This means the option income is taxed at the holder’s ordinary income tax rate, which is higher than long-term capital gains rates on investments held over one year. However, any long-term capital gains from stock price appreciation in excess of cost basis are still taxed at the preferable long-term capital gains rate if the stock is held for over a year before being called away.

Covered calls restrict upside profit potential if the stock rises sharply above the strike price in terms of drawbacks. They are also not well suited for volatile stocks that undergo large, unpredictable swings. High volatility increases the risk of the calls being exercised, leaving less profit potential unrealized. Investors tend to use covered calls on stocks they would not mind selling at the strike price anyway as part of their investment thesis. The premiums also tend to be lower than other options strategies involving higher risk.

What is the importance of a Covered Call?

Covered calls hold importance for many active traders and income investors due to the balanced risk-return profile they provide. Covered calls allow participation in the upside of an underlying stock while collecting premiums to offset potential downside losses by writing call options against stock positions.

This strategy offers an advantage over simply taking naked positions in options or stocks alone for traders. The premiums received from call writing offer a buffer that reduces the cost basis in the covered stock. This provides downside protection and an income stream that traders could use to enter other trades or average down if needed. Covered calls mitigate downside exposure through premium collection rather than risking the whole investment amount in an uncovered stock or naked option position.

The steady premium income generation aspect is also appealing to many traders. Covered call writing allows an options overlay on existing stock holdings to boost returns consistently through the options premiums alone. Collecting call premiums every month or quarter from covered calls fits their goals well for income investors focusing on generating cash flow from their portfolios. It offers a way to enhance dividend yields or capitalize on non-dividend-paying stocks through this income strategy.

Covered calls provide a disciplined way to benefit from stocks trapped in a range or consolidation phase. Traders collect premiums until the calls are either exercised or expire worthless by writing near or at-the-money calls with 30-45 DTE (days to expiration). They participate in further stock price appreciation up to the strike and have time on their side for the option to decay in value through theta. This “theta decay” improves their odds of keeping the shares if the calls are not exercised. Another advantage for more bullish traders is that assigning calls (having them exercised) allows realizing gains at prices potentially higher than what could be obtained by simply selling the shares in the open market at that time. Writing covered calls lock in higher sale prices than spot market rates if a short-term spike drives the stock price up to or through the strike.

How does Covered Call Work?

A covered call works by owning the underlying stock and selling call options on that stock to collect the option premium as additional income. The call writer takes a short call position by selling an option contract to open. This obligates them to sell their covered shares to the caller at the predetermined strike price if the option is exercised. The trader must first buy and hold shares of the underlying stock to set up a covered call. This long stock position “covers” the call options they subsequently write against that stock. For example, a trader would hold a long position valued at Rs 5,000 if they bought 100 shares of XYZ trading at Rs 50.

Call options are written, and another stock is purchased. Call options represent the right, but not the obligation, for the option holder (buyer) to purchase shares from the option writer (seller) at the chosen strike price by expiration. The option seller receives an upfront premium from the buyer in exchange for taking on this short obligation. The trader could write (sell) 1 call contract representing 100 shares with a Rs 55 strike price expiring in 30 days for XYZ trading at Rs 50.

The trader is now short 1 call against their long 100 share position since each option contract covers 100 shares. They would receive the premium, let’s say Rs 150, immediately as payment for taking on this obligation. The first scenario is that at expiration, XYZ closes below Rs 55. The call option expires worthless in this scenario since the strike price was not reached. As a result, the trader gets to keep both their originally purchased shares and the premium they received from writing the call. They have successfully generated income from the trade without any of their shares being called away.

The second possible result is that at expiration, XYZ closes at or above Rs 55. The call buyer, in this case, has the right to exercise their option and purchase the shares from the trader at the agreed-upon strike price of Rs 55 per share. This results in the trader’s shares being “called away” as they are obligated to sell them to the call buyer.

However, the trader still profits from keeping the premium they initially received for writing the covered call. XYZ closes between Rs 50 and Rs 55 at expiration, which is the ultimate result. The trader’s breakeven price on the shares, in this scenario, is reduced from their initial Rs 50 cost basis due to the Rs 0.15 premium received. Their new breakeven is Rs 50 – Rs 0.15 = Rs 49.85. The trader still ends up making a profit on the trade overall from the reduced cost basis, even if the share price only rises modestly between the entry point and expiration.

The trader generates premium income by writing calls while remaining able to profit from stock price appreciation up to the strike price. This lowers their cost basis and reduces risk compared to owning the shares naked. However, gains over the strike are capped due to early stock delivery if exercised. The skill in covered call writing lies in choosing an appropriate strike price and expiration date based on the outlook for the underlying stock and volatility expectations.

Active traders roll options or adjust their positions in response to market moves as well. But in essence, the covered call combines income generation and reduced risk from short options writing with participation in stock upside to a defined limit based on the strike price. This balanced risk-return is why covered calls remain an important strategy for many investors.

What are the reasons why Covered Call is a go-to strategy by traders?

Covered calls are a go-to trading strategy because they generate income from option premiums while allowing investors to profit from upside stock moves up to the strike price of the sold call options.

A covered call strategy provides an attractive risk-return profile that appeals to many traders. The upside is capped at the strike price, but the downside risk is reduced through premium collection by writing calls against an existing stock position. This balanced outcome makes covered calls suitable for a variety of market conditions.

Generating income from premiums is a core advantage. Covered calls provide a regular stream of cash flow simply from selling options each month or quarter. This achieves one of the primary goals of active trading – producing returns. The premiums boost a portfolio’s yield and payout rate without relying solely on dividends.

Controlling downside risk through premiums collected is valued by prudent traders. Covered calls limit maximum potential loss to the difference between the stock’s cost basis and the premiums retained over time. This floor reduces volatility relative to uncovered equity positions. The downside is further mitigated the closer the strike is to current prices.

Capitalizing on range-bound stocks is another utility of covered calls. Regular premiums are still harvested through writing calls just above the market if volatility is low with a stable share price. Ranges provide an ideal environment for covered call strategies to generate income.

Factors like time decay favor the option seller in covered call trades. The probability increases that they will expire worthless as expiration nears and options lose value predictably. This dynamic augment covered call returns through what’s known as the “theta decay tailwind.”

The ability to flexibly adjust positions also appeals to savvy traders. Calls are rolled, closed early, or have their strikes and expirations modified to changing market conditions. This offers greater discretion than buy-and-hold strategies.

What are the disadvantages of a Covered Call strategy?

The main disadvantage of a covered call strategy is it caps the upside profit potential on the underlying stock at the strike price of the sold call options. While covered calls have some benefits, such as generating income from the option premiums, there are also several potential drawbacks to be aware of with this strategy.

1.Capped upside potential: Writing calls limits the ability to profit from significant moves beyond the strike price since shares would be called away. Major breakthroughs in the underlying that push it well above the strike sacrifice some gains.

2. Early assignment risk: There is a chance calls could be exercised prior to expiration if the stock makes a rapid advance and edges into the money. This realizes profits prematurely without being able to participate in the further potential upside.

3. Higher break even: The net stock cost per share after writing a call is higher than simply buying the stock since premium income is collected upfront. The share price needs to overcome this higher initial basis before profits are earned on the covered position.

4. Volatility risk: Highly volatile stocks that experience sharp swings present challenges to covered call writing. The switches raise the likelihood that shares will be called away at unfavorable times or levels and make direction prediction more difficult.

5. Time decay complexity: the optimal timing to write new covered calls depends on this dynamic, while theta decay benefits sellers as expiration nears. It introduces an element of option Greek analysis and timing that negatively impacts trades if mishandled.

6. Tax implications: Premiums are taxed as short-term capital gains regardless of the holding period due to the options’ one-year duration. This results in higher taxes than long-term gains if shares have been held over a year.

7. Limitations on bullish views: Extremely bullish long-term stock theories will not mix well with covered call strategies’ limited upside and income focus. It generally suits neutral to moderately bearish shorter-term views.

Carefully evaluating the drawbacks and implementing covered calls selectively help mitigate risks and utilize them effectively. The limitations require consideration, but covered calls are still utilized successfully within the context of an investor’s broader investment plan and risk tolerance.

How to perform Covered Call Strategy?

To perform a covered call strategy, you buy shares of the underlying stock and sell call options on the same amount of shares to collect the premium income.

1. Select the Underlying Stock: Choose a stock you would be comfortable owning long-term. It should have adequate liquidity in its options market. Preferably select stocks with relatively low volatility and a stable price history.

2. Establish the Long Stock Position: Buy shares of the chosen stock. The number purchased will determine your ability to write covered calls; each option contract covers 100 shares.

3. Pick a Strike Price: Select a strike closely matching or slightly above the current stock price for an at/in the money call. Further out of the money calls lower premiums collected.

4. Choose an Expiration Date: Monthly or quarterly targets expire approximately 30 to 45 days before they are due. Further dates lower premiums but give more time for options to expire worthless.

5. Write the Covered Call: Sell call options equal to your shareholdings at the chosen strike and date, receiving premium payments upfront into your account.

6. Monitor the Position: Watch the underlying stock and option prices as expiration approaches. Consider closing early for profit or rolling to avoid assignment.

7. Decide on Expiration: Your calls expire worthless, and you keep shares and premiums if the strike is above the stock price. Shares are called away at or above the strike price.

8. Repeat the Process: Analyze the market and repeat steps 3-7 by writing new covered calls once current options expire or are closed. Receive ongoing income through multiple cycles.

9. Adjust Strategically – Be willing to adapt based on changing market conditions. Opt to roll, let exercise, or close calls depending on perceived risks versus rewards at any point.

Careful stock and option selection balanced with flexible adjustments are keys to successful long-term covered call management. Following these guidelines helps generate consistent premium income from low-risk covered write strategies.

Covered calls are also used in the second phase of the covered call wheel strategy, after a trader gets assigned shares through a sold cash-secured put.

What market structure to look for when performing Covered Call strategy?

To optimize premium income and reduce the risk of the underlying stock being called away, look for an upward-trending or neutral market structure when executing a covered call strategy.

Liquidity in the underlying stock and options markets is important. There needs to be sufficient trading volume and interest from other market participants to provide tight bid/ask spreads. This allows entering and exiting positions smoothly with minimal market impact costs.

Stocks of large, well-known companies usually offer the best liquidity. Implied volatility levels should also be assessed. Covered calls tend to perform best when underlying volatility is elevated, as this drives option premiums higher. Periods of low volatility result in lower premiums collected per trade. Option selling strategies like covered calls benefit most from “volatility harvesting” environments.

Trending vs. ranging markets matter. Quietly ranging stocks within a defined price band provide opportunities to collect premiums reliably month after month by writing calls just above the range. Strong trending periods introduce a greater risk of early assignment if the trend continues unexpectedly.

Range-bound stocks suit covered calls. Strike price selection depends on technical support/resistance zones. Picking strikes slightly above recent highs or just penetrating resistance helps modulate downside risk. Pursuing premiums too close to current prices raises the risk-return tradeoff unattractively for the covered call writer.

While choosing an options expiration cycle, take future catalysts such as earnings reports into consideration. Steering clear of potentially volatile announcement dates by a few weeks allows positions time to recover should unexpected volatility arise temporarily on the news. Carefully analyzing these structural aspects enables covered call traders to stack the statistical odds in their favor via optimal stock, strike, and timing selection. Doing so enhances the strategy’s probability of success over repeated implementation.

Is Covered Call better to use in a bearish market?

Yes, covered call strategies are more suitable for bearish market environments compared to bullish periods in some ways. This is because covered calls are designed to mitigate downside risk through premium collection while still allowing participation in a modest upside.

Volatility tends to increase as uncertainty rises when the overall market is declining. Higher implied volatility boosts option premiums, improving the income-generating potential of covered call trades. The premiums collected offset some of the downward price pressure on the underlying stocks.

Is Covered Call better to use in a bullish market?

No, covered Call strategies are likely less advantageous compared to bearish environments while they still play a role in bull markets. The primary limitation is their capped upside potential, which works against capturing the full rewards of a strong uptrend. Bull markets, by definition, involve rising share prices and growing optimism.

But covered calls restrict profit-taking at the strike level, leaving gains above that price unrealized if the options are executed. This ceilings their performance potential relative to outright long positions. Aggressive bull runs also increase the odds of early assignment as stocks surge past strikes into profitable territory for call holders. This denies further participation just as prices start accelerating. Well-timed naked calls might generate greater returns.

Is Covered Call better to use in a neutral market?

Yes, a neutral market environment, where volatility is subdued, and the directional bias is unclear, presents the most suitable conditions for employing a covered call strategy effectively. Individual stocks often trade within defined sideways ranges during periods where the overall market trend is neither strongly bullish nor bearish.

This type of price consolidation lends itself well to the income objectives of covered call writing. Premiums are collected predictably each month as options expire worthless, allowing the shares to be retained by selling calls just above the current trading range. Neutral markets with steady but narrow daily price fluctuations optimize this outcome.

When to enter the market using a Covered Call strategy?

The ideal time to enter a covered call trade is when implied volatility is high, as that allows you to collect larger premiums when selling the calls. You want to buy the stock when it is at support or oversold technically, so there is less risk of the stock falling further.

Finally, only use the covered call strategy when you have a moderately bullish bias on the stock and expect it to rise or trade sideways in the near term. This allows you to potentially profit from both the stock price appreciation and the call premium decay.

When to exit the market using a Covered Call strategy?

With a covered call position, you would want to close the trade if the stock price falls significantly below your purchase price, especially if the stock breaks technical support levels. This allows you to avoid further losses on the declining stock. You may also want to buy back the call option you sold if it declines in value due to a drop in implied volatility.

This allows you to collect profits on the short call. Alternatively, you can choose to exit the covered call position by waiting for the call option to expire worthless or get assigned on the short call if the stock rises above the strike price. This allows you to maximize your premium income from the covered call trade.

What is the maximum profit of a Covered Call strategy?

The maximum profit of a covered call strategy is limited to the premium received for selling the call option plus any dividends received while holding the underlying stock. The investor has a long stock position and a short call option written against those shares when establishing a covered call position.

Let’s consider an example where an investor establishes a covered call by purchasing 100 shares of stock ABC at Rs 50 per share for a total cost of Rs 5,000. They then write 1 call contract with a strike price of Rs 55 expiring in 1 month. The premium received for writing this call is Rs 0.50 per share or Rs 50 total.

The maximum profit scenario in this position would be if the stock price of ABC remains below Rs 55 at expiration. The call option, in this case, expires worthless, and the investor keeps both their stock (now valued up to Rs 5,000) and the premium received of Rs 50 for a total profit of Rs 5,050.

This caps the maximum possible profit at the difference between the stock purchase price and the premium. Any stock appreciation beyond this point is left on the table, as the shares would be called away if above the strike. There are a few additional factors that could slightly increase maximum profit in some cases. One is allowing the option to be repurchased for credit before expiration if implied volatility rises significantly. Transaction fees must also be considered.

Ultimately, though, the upside is finite with covered calls due to capping participation at the strike price. The tradeoff is collecting premiums while waiting for options to expire out of the money. Effective strategies roll positions to continue harvesting income. Covered calls are best suited to neutral or range-bound markets versus periods of strong price momentum for investors wanting both income and the ability to profit fully from bull markets. The method limits downside risk rather than unrestrictedly maximizing upside potential.

What is the maximum loss of a Covered Call strategy?

The maximum possible loss from a covered call trade is limited due to the reduction in cost basis afforded by the premiums received from writing call options. The investor has a long stock holding and has received an upfront credit from selling a call against those shares when establishing a covered call position.

Let’s consider the example we used before, where an investor purchases 100 shares of stock ABC at Rs 50 per share for a total cost of Rs 5,000. They write 1 contract with a strike of Rs 55 expiring in 1 month, collecting a Rs 0.50 per share or Rs 50 premium.

The maximum theoretical loss in this scenario would be if ABC’s share price fell to Rs 0 overnight. The loss would be Rs 5,000 (cost) – Rs 50 (premium received) = Rs 4,950 if the shares were sold at this point. This factors in that premium collection lowers net cost based on purchase price alone. The maximum drawdown is effectively limited to the difference between the entry price and proceeds.

Some additional factors could slightly decrease this maximum. First, the call writing creates a covered obligation, so the shares are not sold until option expiration or repurchase. Second, fees apply to closing any resulting option positions at a loss. Share prices do not usually gap down to Rs 0 in reality, and covered call income compounds to further diminish risk over time. However, conceptually, the strategy caps potential monetary loss through premium risk reduction.

Containing downside is just as important as uncapped returns for conservative investors. Covered calls succeed on this count by marrying short option premiums to long stock ownership to reduce risk. Positions are adjusted or exited if a threat to the maximum develops.

How often is the Covered Call used by traders?

A covered call is a very common options strategy used routinely by traders, with over 50% of options volume attributed to covered call writing. Covered call writing has become one of the most popular options strategies employed by both retail and professional traders. Covered calls are utilized across a wide spectrum of market participants due to their ability to generate consistent income streams with limited risk.

More conservative, income-focused individual investors will commonly employ covered calls on a monthly or semi-monthly cycle, taking advantage of the steady premium generation. This provides a supplementary income stream to potentially boost portfolio yields.

Active retail traders also make significant use of covered calls, often on a weekly or bi-weekly schedule. They seek optimized risk-adjusted returns versus buy-and-hold strategies by more frequently establishing and adjusting strike prices. The flexibility to roll positions appeals to this cohort.

Even larger institutional traders regularly employ six-figure covered call programs. The ability to reliably harvest premiums makes it well-suited for hedging purposes within their portfolios. Even small incremental returns add up substantially with extensive holdings.

Covered call writing forms the basis of various product offerings within trading firms and wealth management shops. These are focused income solutions or provide new vehicles for accessing well-known stocks and ETFs with reduced volatility.

The rise of online brokers has also spurred covered call adoption by simplifying the implementation process for self-directed traders and lowering entry barriers. Easy-to-use interfaces expose more investors to the benefits.

Is Covered Call a good strategy for the short term?

Yes, covered call strategies are effective for short-term time horizons, but they also carry some drawbacks versus longer durations. On the plus side, the income focus of covered calls makes them a sensible tactic for opportunistically harvesting premiums within condensed windows.

Covered calls leverage the strong influence of theta decay near expiry, with short-dated options expiring within weeks or months. This enhances the probability contracts will expire worthless, allowing the retention of shares and premiums. Trading expenses are also minimized for such a quick turnover.

For traders, asset managers, or products aiming for steady, non-directional income, medium-long holding periods capitalize covered calls’ full benefits. However, skilled tacticians extract profits within limited horizons, accepting constraints. Applications exist for both spectra.

Is Covered Call a good strategy for the long term?

Yes, covered call strategies are well-suited for long-term investment horizons, as their benefits are optimized over extended periods. Covered calls generate income in a low-maintenance, buy-and-hold fashion by establishing covered positions and continuously rolling contracts forward month after month.

Over the years, the consistent premium collection compounds have boosted total returns significantly. Even relatively small monthly paydays accumulate substantially when reinvested continually. This compounding effect is maximized through uninterrupted serial writing over the long run.

Extended durations also allow adapting positions smoothly to changing market conditions without disrupting income. Volatility spikes or trend shifts are navigated by widening strikes or adjusting expiration dates instead of panicking and exiting. Covered calls reduce portfolio volatility naturally through their limiting downside. Over bull-bear market cycles and multiple years, this risk-managed quality preserves more capital for compounding gains steadily versus plain equities experiencing volatile drawdowns.

In addition, tax treatment favors covered call strategies employed long-term. Premiums are taxed as capital gains instead of ordinary income after holding over a year. This enhances the value proposition of covered call holdings, realizing multi-year gains.

Finally, evolving covered positions intelligently attuned to the business cycle optimizes income potential versus naive set-and-forget approaches. Active management remains important, but years provide flexibility to optimize based on macro and company-specific backdrops unfolding gradually.

How does Covered Call differ from other income strategies?

Covered call differs from other income strategies in that it generates income by selling call options on stocks already owned rather than purchasing assets solely for income. Covered call writing is one of many approaches investors take to generate income from their portfolios. Covered calls, while they share similarities to other strategies, also have unique characteristics that set them apart.

Companies that pay dividends provide regular cash flows to shareholders. However, dividends are never guaranteed and are reduced or suspended at any time by management. Covered calls generate income through option premiums, not corporate payouts, avoiding this risk. They also allow retaining stocks without dividends being paid out.

Real estate investment trusts focus on income through property rents. REIT share prices tend to be more volatile than broad markets, even while competitive yields are offered. Covered call writing seeks steadier returns through minimized downside risk. It also maintains liquidity versus direct real estate investments.

Bonds deliver interest payments dependably. However, their income potential is capped, and prices are exposed to interest rate swings. Covered calls provide equity participation with income resembling bond-like yields but less rate sensitivity through diversification.

High-yield savings accounts and money market funds rely on rates set by central banks. These rates change gradually, limiting income-earning potential over the long run. Covered calls produce competitive rates taxed at capital gains instead of ordinary income like fixed deposits.

Some generate income from foreign exchange markets. However, directional exposure subjects profitability to unpredictable currency fluctuations. Covered calls mitigate downside vulnerability through premium collection and limited risk parameters.

Selling naked puts/calls carries unlimited risk, requiring more margin. Covered calls reduce obligation through the paired stock and limit danger versus premium selling alone. Rolling positions also maintain steady income versus one-off trades.

Covered calls carve a versatile niche fit for diverse investors and markets, generating income durably from high-quality companies by marrying equity upside to short premium credits. No strategy perfectly extracts all benefits, requiring selecting techniques that best match risk appetite and holding periods. Covered calls present an option for penetrating income spheres not entirely correlated to alternatives.

Is Covered Call a better strategy than Naked Put?

A covered call is generally considered less risky than a naked put since the call writer already owns the underlying stock, limiting potential losses if the stock price declines. A covered call strategy involves being long the underlying stock in addition to writing call options against those shares. This provides downside protection from holding the stock. In contrast, a naked put strategy simply involves writing put options without owning the underlying stock.

One key difference is the risk profile. The maximum risk is capped at the difference between the stock purchase price and premiums received as a covered call writer. Downside is defined. But a naked put writer faces unlimited risk if the stock falls substantially below the strike price, as they are assigned shares far higher than the current market value.

Premium collection potential also differs. Covered calls generate premium income on a regular recurring basis by writing calls month after month, allowing shares to be retained through expiration. Naked puts are one-time trades, requiring closing the position to realize maximum profits rather than rinse-repeating. Income is less stable.

Flexibility is enhanced with covered calls. Positions are rolled over to maintain coverage if needed by repurchasing existing puts/calls and writing new ones. This keeps positions hedged. Naked puts must be exited entirely to close prevailing risks and start anew. Adaptability is reduced.

Taxes are handled more optimally with covered calls as well. Premiums incur long-term capital gains rates instead of ordinary short-term rates for naked puts by holding the stock over a year. This improves after-tax returns meaningfully, assuming extended holding periods.

Covered calls better hit the trifecta of risk management, income generation, and tax efficiency most investors seek from options strategies. Covered calls present a more holistic value proposition for the average options trader, even though both have places.

Is Covered Call a better strategy than Long Iron Butterfly?

Yes, the covered call has lower risk and simpler management than Long Iron Butterfly, which involves multiple option legs and needs significant price movement to profit. A long iron butterfly is a neutral options strategy that involves being long a call and put at one strike price while simultaneously being short a call and put at a higher and lower strike, respectively.

Is Covered Call a better strategy than Bear Call Spread?

Yes, a covered call is a more bullish strategy than a bear call spread, with the ability to profit from limited stock price gains rather than needing the underlying price to fall for the spread to be profitable. A bear call spread is a bearish options strategy that involves selling a call option while simultaneously buying a further out-of-the-money call to cap risk.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.