A Put Calendar Spread is an options strategy that leverages time decay and implied volatility for potential profit in neutral or slightly bearish markets. A Put Calendar Spread involves selling a short-term put and buying a longer-term put at the same strike price, typically when the trader expects minimal movement in the underlying asset.

This approach has evolved over decades, becoming popular among both retail and institutional traders, especially for earnings plays or when implied volatility is low but expected to rise. Traders favor it for its defined risk and the flexibility it offers compared to outright directional bets.

What is a Put Calendar Spread?

A Put Calendar Spread is an options strategy involving two put contracts at the same strike but with different expiration dates. The trader sells a short-term put and simultaneously buys a longer-term put, both typically at-the-money or slightly out-of-the-money.

This setup creates a position that profits from time decay and rising implied volatility. The short put, expiring sooner, loses value faster, while the long put retains more premium over time. As a result, the position benefits if the underlying asset remains near the strike price until the short put expires.

The net cost of the trade (net debit) is the difference in premiums, paid upfront by the trader. The risk is strictly limited to this net debit, while the reward potential is maximized if the stock price stays close to the strike at the short put’s expiry.

Because both legs share the same strike, the risk of significant loss from large moves in the underlying asset is reduced, compared to naked options selling. The strategy is particularly attractive in environments where volatility is expected to rise, or when the market is expected to remain neutral for a short period.

How Does a Put Calendar Spread Work?

A Put Calendar Spread works by selling a near-term put and buying a longer-term put at the same strike price, creating a position that profits from time decay and volatility shifts. The short-term put decays in value faster than the long-term put due to its impending expiration, providing a net benefit to the trader.

Typically, the trader chooses a strike price near the current trading level of the underlying asset, sells a put expiring soon (such as within a week or a month), and buys a put expiring further out (such as one or two months later). The difference in premiums represents the net debit paid.

As time passes, the value of the short put erodes more rapidly, especially if the underlying asset remains at or near the strike price. Meanwhile, the long put retains time value, particularly if implied volatility rises, making the overall position more valuable.

The trader close the position for a profit if the underlying stock stays close to the strike at the short expiry, roll the short leg forward, or manage further based on market conditions. If the stock moves sharply in either direction, the position’s value declines, but the loss is capped at the net debit initially paid.

Why Use a Put Calendar Spread Strategy?

A Put Calendar Spread strategy is used to profit from sideways market movement, take advantage of time decay, and benefit from rising implied volatility, making it ideal for range-bound or low-volatility setups. The unique structure of this strategy allows traders to capitalize on specific market conditions that are unfavorable for more directional trades.

One major advantage is the positive impact of time decay on the short put, which loses value more rapidly as expiration nears. This decay works in favor of the trader, especially when the underlying asset shows little price movement, allowing the position to be closed at a profit as the short-term option nears expiry.

Rising implied volatility also enhances the value of the longer-term put, providing an additional profit opportunity if market uncertainty increases. This makes the strategy particularly attractive around earnings releases or other events likely to boost volatility.

Traders often use put calendar spreads when they expect the underlying asset to remain within a tight range or when they anticipate a volatility increase after entering the trade. The strategy’s defined risk and flexible exit options make it a preferred choice for both novice and experienced options traders seeking profit in non-trending markets.

When to Use a Put Calendar Spread?

A Put Calendar Spread is best employed when expecting neutral to moderately bearish movement, especially around events like earnings or implied volatility expansion. This timing ensures the trader can take full advantage of the anticipated increase in volatility and the time decay of the short put.

The strategy excels when the underlying stock is range-bound, as it relies on minimal price movement to maximize profit. Entering the trade in a low implied volatility environment, where volatility is expected to rise, further boosts the potential for a favorable outcome.

Earnings announcements, major product launches, and other scheduled events often lead to volatility spikes, making these periods optimal for put calendar spreads. By positioning ahead of such events, traders prepare to benefit from the subsequent volatility increase and the rapid time decay of the short-term option.

Careful strike selection and timing are crucial. Traders should focus on assets known for stable price action or those with upcoming catalysts expected to drive volatility higher. Monitoring the position and managing the short leg before expiration is essential to avoid unnecessary risk and maximize returns.

How Do Option Greeks Affect a Put Calendar Spread?

Option Greeks have a significant impact on a Put Calendar Spread, with the most important being Theta (positive near expiry), Vega (positive), Delta (near-neutral), and Gamma (low). Each Greek measures a different risk and reward aspect of the spread, affecting how it behaves under various market conditions.

Theta, representing time decay, is positive for the spread as the short put loses value rapidly near expiry, benefiting the position. Vega, which measures sensitivity to changes in implied volatility, is also positive; an increase in IV raises the value of the longer-term put more than the short-term put, enhancing the spread’s profit potential.

Delta for a put calendar spread is typically close to neutral, though it can shift slightly bearish or bullish depending on how the strikes are set relative to the underlying price. This delta neutrality helps minimize directional risk, making the strategy suitable for traders who do not want to bet on a large price move.

Gamma, measuring sensitivity to changes in delta, remains low for calendar spreads, as the position is not highly responsive to sharp price swings. Below is a typical Greek sensitivity table.

| Greek | Sensitivity | Impact on Spread |

| Theta | Positive | Profits from decay |

| Vega | Positive | Profits from IV rise |

| Delta | Near-zero | Minimal direction |

| Gamma | Low | Not responsive |

Understanding these Greeks helps traders better manage their positions and anticipate how the spread will respond to market changes.

How Does Implied Volatility Affect a Put Calendar Spread?

Implied Volatility (IV) affects a Put Calendar Spread by increasing its value when IV rises, as the longer-term put benefits more than the short-term put. This relationship makes the strategy especially effective when entered at low IV, expecting it to increase over time.

A rising IV environment means both the short and long puts gain in value, but the longer-term put, having more extrinsic value, reacts more strongly. As a result, the spread widens, allowing the trader to exit at a profit or roll the short put for additional premium.

Conversely, falling IV can hurt the spread, as the value of both options drops, but the longer-term put loses more, shrinking the spread and potentially leading to a loss. The strategy works best when IV is low at entry and is forecasted to rise, such as before earnings or major news events.

The primary risk is an IV crush, which often occurs after a significant event like earnings. If volatility drops sharply, the spread’s value collapses, and the trader risks losing the net debit paid. Thus, timing is critical, and traders must monitor implied volatility closely to maximize the strategy’s effectiveness.

How to Trade a Put Calendar Spread

To trade with a put calendar spread, start with selecting an underlying asset that is showing low implied volatility and is likely to stay within a tight range. The idea is to benefit from time decay on the short leg while retaining exposure through the longer-term option.

For instance, consider a trade setup where you sell one ATM put option at the 25100 strike for the current weekly expiry at ₹153.65, and simultaneously buy one put at the same strike with a monthly expiry at ₹282.

This results in a net debit of ₹128.35 per share, or ₹9,626.25 for a lot size of 75. The maximum profit from this strategy—around ₹9,484—is theoretically achieved if the underlying closes exactly at 25100 at the weekly expiry.

At that point, the short leg expires worthless while the long leg still retains time value. The maximum possible loss is limited to the net debit paid, which is ₹11,928, if the price moves significantly away from the strike before the long option gains value.

Breakeven for the trade is estimated between ₹24,812 and ₹25,430. Managing this trade involves monitoring time decay and IV, and ideally exiting or rolling before the short put expires.

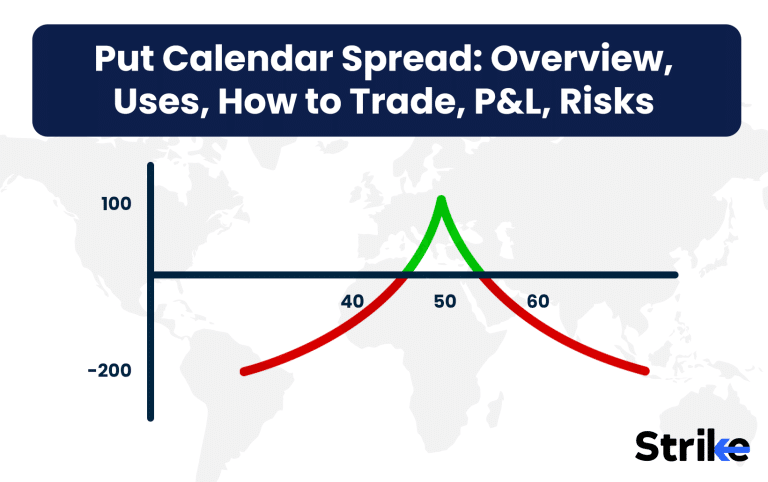

What is the Payoff, Max Profit & Loss in a Put Calendar Spread?

The Payoff of a Put Calendar Spread is maximized when the underlying asset closes near the strike price at short expiry, with the maximum loss limited to the net debit paid. The strategy’s profit and loss profile is defined and predictable, making it attractive for risk-conscious traders.

Maximum profit occurs if the underlying price finishes at or very close to the strike price when the short put expires. At this point, the short put has decayed to almost zero, while the long put still holds significant time value, which can be sold or managed further. The exact profit amount depends on the remaining premium in the long put.

Maximum loss is capped at the net debit paid to establish the spread—essentially, the difference between the long and short put premiums. This loss happens if the underlying moves sharply away from the strike, causing both options to lose value, or if implied volatility collapses sharply.

Breakeven points are slightly above and below the strike price, varying with implied volatility at entry and expiry. The following table summarizes the key P&L points:

| Underlying at Expiry | Result |

| Near strike | Max profit (remaining value of long put) |

| Far from strike | Loss, up to net debit paid |

Below is a typical payoff diagram.

This visualizes how the spread profits most when the underlying finishes near the strike.

What Are the Risks of a Put Calendar Spread?

Risks of a Put Calendar Spread include the potential loss of the full premium, volatility crush after major events, mismanagement of expiration, and rare short option assignment. These risks are generally manageable, but they must be understood before placing a trade.

In case the underlying asset moves significantly away from the strike price, both the short and long puts lose value, resulting in a loss up to the net debit paid. This is the most common risk, especially if a sharp move occurs unexpectedly.

A volatility crush, particularly after events like earnings, can rapidly erode the value of both options, leaving the trader with little or no recoverable premium. Entering the trade when implied volatility is already elevated increases this risk.

Mismanaging the short put’s expiration, such as failing to roll or close it before expiry, introduces additional dangers. For example, if the short put finishes in-the-money, the trader faces assignment risk, which, while rare, can complicate the position and require urgent action.

Is a Put Calendar Spread Strategy Profitable?

Yes, a Put Calendar Spread strategy is profitable when the underlying asset remains near the strike price at short expiry and implied volatility rises or stays steady. Profitability hinges on proper timing, effective strike selection, and managing the position in response to market movements.

The strategy thrives in range-bound markets, where neither bulls nor bears dominate price action. In such environments, the short put decays rapidly, while the long put retains value, allowing the trader to close the spread at a profit. If implied volatility increases during the life of the trade, the long put’s value rises, further boosting returns.

However, profitability is limited by the maximum gain, which occurs only in a narrow price range, and the risk of loss if the underlying moves sharply or volatility drops. Consistently profitable use of this strategy requires disciplined entry and exit points and ongoing market monitoring.

Is a Put Calendar Spread Bullish or Bearish?

A Put Calendar Spread is generally a neutral to slightly bearish strategy, but its bias depends on the strike selection and market setup. When constructed at-the-money, it benefits most from little movement in the underlying, making it market-neutral.

If the spread is established slightly out-of-the-money, it takes on a mildly bearish stance, profiting if the underlying declines modestly or remains flat. However, the position does not reward large price drops, since both the short and long puts lose value if the stock falls too far.

The strategy’s flexibility allows traders to adjust their exposure based on market outlook. By shifting the strike price above or below the current level, the calendar spread’s delta (directional sensitivity) can be tweaked to suit a more bullish or bearish bias.

The put calendar spread is best utilized when little price movement is expected, with the potential for a slight bearish tilt depending on structure.

What Are Alternatives to a Put Calendar Spread?

Alternatives to a Put Calendar Spread include the Call Calendar Spread, Diagonal Spread, Vertical Put Spread, and Iron Condor, each with different risk/reward profiles and market biases. These strategies offer similar mechanics or objectives but suit different market views and risk tolerances.

A Call Calendar Spread functions like the put version but uses call options, making it suitable for neutral to slightly bullish outlooks. It profits in a similar manner when the underlying remains near the strike price at short expiry.

The Diagonal Spread uses options at different strikes and expiries, providing more flexibility in directional bias and payoff structure. This approach fits traders who wish to combine the benefits of calendar and vertical spreads.

A Vertical Put Spread involves buying and selling puts at different strikes but the same expiry, offering a defined-profit, defined-risk bearish position. This spread is better for traders expecting a more pronounced move in the underlying.

The Iron Condor combines both put and call spreads, creating a neutral, income-generating strategy with limited risk and reward. Iron condors thrive in very stable markets but offer less profit potential than calendar spreads in volatile conditions.

| Strategy | Bias | Risk/Reward |

| Put Calendar Spread | Neutral/Bearish | Limited/Limited |

| Call Calendar Spread | Neutral/Bullish | Limited/Limited |

| Diagonal Spread | Bullish/Bearish | Flexible/Limited |

| Vertical Put Spread | Bearish | Limited/Limited |

| Iron Condor | Neutral | Limited/Limited |

Choosing the right alternative depends on market outlook, risk appetite, and desired payoff structure. Each offers a unique way to express a view on the underlying asset.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 32")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.