At the money (ATM) refers to an options contract where the strike price is equal to the current market price of the underlying asset. At the money (ATM) option has no intrinsic value, only time value.

Its premium consists entirely of time value, which is the chance the option will become profitable by expiration due to movement in the underlying asset price. As expiration nears, the time value decays.

ATM options are popular trading vehicles because they offer greater leverage and usually have higher liquidity and trading volume compared to in-the-money or out-of-the-money options. Their probability of expiring worthless or in the money is around 50/50.

Traders use ATM options for several strategic reasons. They allow flexibility to capitalize on upside or downside moves. ATM straddles and strangles benefit from volatility expansion. ATM options are used to create synthetic positions replicating other instruments. Portfolio managers use them to hedge positions without significant cost.

The main advantage of ATMs is that they tend to have higher liquidity and tighter bid-ask spreads compared to out-of-the-money or in-the-money options. The higher volume makes it easier to get in and out of ATM options positions quickly. This allows Indian traders to capitalize on short-term opportunities.

What is At The Money (ATM)?

An ATM (at-the-money) option contract is an arrangement in which the strike price corresponds to the present market value of the underlying asset. The strike price aligns with the ongoing trading price of the stock when it comes to call options. The strike price is identical to how much the stock is valued in the market input options.

: Definition, How it Works, and How It Is Determined 21")

An at the money option has no intrinsic value, only time value composed of implied volatility and time to expiration. Time value decays as there are fewer days for the asset price to move favorably as the expiration date approaches. The time value drops to zero, and only intrinsic value remains if the option is in the money. Since ATM options have no intrinsic value, they expire worthless if the underlying price remains unchanged.

ATM options are popular trading vehicles because they typically have higher liquidity and trading volume compared to out-of-the-money or deep-in-the-money options. Their probability of expiring worthless or in the money is around 50/50 due to being closest to the current asset price.

Traders utilize at-the-money options for several strategic reasons. ATM options provide flexibility to capitalize on upside or downside moves in the underlying asset. Traders often use them when uncertain about further directional movement.

ATM straddles and strangles benefit from volatility expansion. Long straddles and strangles make money if the asset price moves significantly in either direction. ATM options maximize exposure to volatility while minimizing cost.

ATM options can create synthetic positions replicating other instruments. For example, an ATM long call combined with a short future replicates owning the underlying asset. An ATM short call combined with owning the asset creates a synthetic covered call.

Portfolio managers use ATM options to hedge positions without significant time value costs. The minimal premium paid for ATM options lowers the breakeven point versus using out-of-the-money options.

The money options offer traders defined risk exposure and leverage. Their intrinsic value is zero, but time value provides a payoff possibility from favorable underlying price movement. Investors must accurately determine if an option is currently ATM to properly utilize its advantages.

The at-the-money status of an option constantly changes. An ATM option today becomes out of the money tomorrow if the underlying asset price drops below the strike price. Or, the option could become in the money if the stock price rises above the strike.

Monitoring the difference between the strike price and underlying asset market price indicates whether an option is ATM, in the money, or out of the money. Calculating the option’s sensitivity to the underlying price using the delta and gamma values also helps gauge ATM status.

At-the-money (ATM) options work by having a strike price equal to the current market price of the underlying asset. Their intrinsic value is zero since there is no difference between the strike price and the market price. The entire premium or price of an ATM option consists of time value. The time value represents the chance the option will become profitable by expiration. Time value is composed of implied volatility and time to expiration. Implied volatility measures the expected future volatility of the underlying asset price. Higher implied volatility means a greater probability the asset price makes a large move and the option finishes in the money.

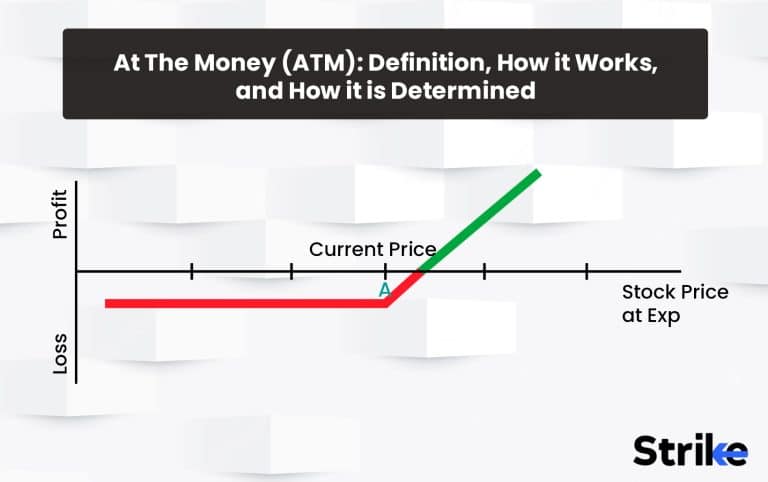

Time to expiration is the remaining time until the option expires. The more time remaining, the higher the chance the asset price moves enough to put the option in the money. As expiration approaches, time value decays because there are fewer days for a favorable price move to occur. The buyer pays the time value premium for contract terms, giving them the right to buy the underlying asset at the strike price when an ATM call option is purchased. Profit potential comes from the asset price rising above the strike before expiration. Consider an ATM call option on Stock XYZ with a Rs.50 strike price when XYZ trades at Rs.50.

The call premium may be Rs.2, which the buyer pays for this right. Consider XYZ rises to Rs.55 before expiration, then the call option can be exercised to buy XYZ at Rs.50 and immediately sell it at Rs.55 for a Rs.5 profit per share minus the Rs.2 premium cost. Put options work similarly but in reverse. Buying an ATM put option creates the right to sell the underlying at the strike price. Profit occurs if the asset price falls below the strike. For an Rs.50 XYZ put, gains accrue if XYZ drops below Rs.50. The put is exercised to sell XYZ at Rs.50 even as the market price declines.

Traders utilize various strategies to profit from ATM options. A long straddle involves buying an ATM call and put with the same expiration. Gains occur if the asset price moves significantly up or down. The trade loses only the premium paid if the price stays flat. A long strangle is buying an out-of-the-money call and an out-of-the-money put. This is similar to a straddle but requires a larger price move to break even due to the OTM options being cheaper. However, loss is limited to the lower premiums paid.

Selling covered calls involves writing ATM calls against a long position in the underlying asset. As the asset is held, premium income is generated from the short calls. Profits accrue from both rising share prices and call premiums.

What are the characteristics of the At The Money Option?

ATM options have a unique risk-return profile and set of trading characteristics that make them a popular choice among options traders. Understanding when an option is considered ATM and how ATM options behave can help investors utilize them effectively for strategies around directional bets, volatility trading, and portfolio hedging.

Strike Price Equals Underlying Price

The main characteristic of an ATM option is a strike price identical to the current market price of the underlying asset. Whether a call or put option, the strike price equalling the trading price of the stock defines its ATM status.

No Intrinsic Value

ATM options have zero intrinsic value because there is no difference between the strike price and the underlying price. Intrinsic value only exists if an option is in the money when the strike is advantageous relative to the market price.

All-Time Value Premium

Since ATM options have no intrinsic value, their entire premium consists of time value. Time value represents the possibility the option becomes profitable by expiration if the underlying price moves favorably. It is determined by implied volatility and time remaining until expiry.

Higher Vega

Vega measures an option’s sensitivity to changes in implied volatility. ATM options have higher vega relative to in or out-of-the-money options. This makes their value more responsive to volatility fluctuations.

Approximately 50 Delta

An ATM option has a delta of close to 0.50. Delta measures the option’s price movement compared to the underlying asset. A 0.50 delta means the option price changes by about 50% of the underlying price change.

Uncertain Expiration Profitability

ATM options retain their time value all the way to expiration. Whether they expire profitably depends on the underlying asset price at expiry. There is roughly a 50% chance of finishing in the money.

High Liquidity and Volume

ATM options tend to have the most liquidity and daily trading volume. Their volume exceeds out-of-the-money and deep-in-the-money options, as more traders prefer ATM contract specifications.

Used for Directional Trading

ATM options are often used when traders are uncertain about further upside/downside direction. ATM provides exposure for bullish or bearish bets with limited risk to the option premium paid.

utilized for Volatility Strategies

ATM options maximize exposure to volatility fluctuations. Straddles and strangles using ATM options benefit from time value gains if implied volatility rises significantly before expiry.

Flexibility in Constructing Spreads

ATM options are frequently used as a leg in spreads. Their lower cost than ITM options provide flexibility to create credit or debit spreads at various risk/reward levels.

The main unique characteristics of ATM options are a strike price equal to the asset price, no intrinsic value, high time value, uncertain expiration payoffs, and versatility for directional and volatility trading strategies. Recognizing these ATM features allows informed trading decisions.

What is the ATM option time value?

At the money (ATM), options have no intrinsic value, only time value. An option’s premium consists of intrinsic value + time value. Since the strike price equals the underlying asset price for ATM options, there is no difference between the two that would create intrinsic value.

Time value represents the chance an ATM option becomes profitable by expiration if the underlying asset price moves favorably. Time value is composed of two components – implied volatility and time to expiration. Higher implied volatility indicates greater expected volatility that would increase the probability the option finishes in the money. More time until expiration provides a greater opportunity for the underlying price to move past the strike price.

As an ATM option approaches its expiration date, time value decays exponentially because there are fewer days remaining for the option to become in the money. On the actual expiration date, all time value disappears from the premium, leaving only intrinsic value if it expired in the money. Since ATM options have zero intrinsic value, they expire worthless if unchanged on expiration day.

How is At The Money (ATM) determined?

The at-the-money (ATM) status of an option is determined by comparing the option’s strike price to the current market price of the underlying asset. The strike price equals the market price of the stock means the option is considered at the money. For call options, the strike price must match the trading price of the underlying stock for the call to be ATM. The strike price is lower than the market price means the call option has intrinsic value and is considered in the money. The strike price is higher than the share price means the call option has no intrinsic value and is out of the money.

Put options follow the same principle. The put option is ATM when its strike price equals the current market value of the underlying security. A put option is in the money when its strike price exceeds the market price of the stock. The strike price is lower than the market value means the put is out of the money.

An easy way to determine if an option is ATM is to simply compare the strike price to the stock’s price when considering entering a position. However, the ATM point can change constantly as the underlying stock price fluctuates up and down. An ATM option one day could be out of the money the next day if the stock price declines below the strike.

Active traders monitor the difference between the strike price and underlying asset market value to determine when an option transitions between in-the-money, out-of-the-money, and at-the-money status. An ATM option can quickly move into one of the other categories with any movement in the stock.

The intrinsic value of an option must also be calculated to determine if it is ATM. Intrinsic value is the difference between the strike price and the underlying price. No difference means no intrinsic value, indicating an ATM option. Calculating intrinsic value provides mathematical confirmation of ATM status.

Using the Greeks – specifically delta and gamma – provides sensitivity measures that can identify an ATM option. Delta measures the option’s price movement compared to the underlying asset. ATM options have a delta of around 0.50, meaning a 50% price change relative to the stock.

Gamma gauges how fast the delta changes when the stock price moves. ATM options have higher gamma than in or out-of-the-money options. Their delta moves closer to 1.00 or 0.00 at an accelerating rate with a larger gamma. A high gamma signals an option is at the money.

How does an At The Money (ATM) Option’s strike price relate to the underlying asset’s price?

The key characteristic of an at-the-money (ATM) option is that its strike price equals the current market price of the underlying asset. Whether a call or put option, for it to be considered ATM, the strike price must be the same as the trading price of the stock or other security. This match between the fixed strike price and the variable market price is what defines an option as being at the money. The strike price represents the fixed price at which the option holder will be able to buy or sell the underlying if exercised. The market price is the current value at which the stock or asset is trading.

For call options, the strike price must be identical to the market price of the stock for the calls to be ATM. The strike price is lower than the market value means the calls are in the money since they give the holder the right to buy at a cheaper price. The call option is out of the money If the strike exceeds the market price. Put options work the same way. The put is ATM when its strike price equals the market price of the stock. The put strike is higher than the market value means it is in the money because the holder sells at an advantageous price. A lower strike makes the put out of the money.

As the underlying asset price fluctuates, the ATM level changes as well. What was an ATM option one day may become out of the money the next if the stock price declines below the existing strike. An in-the-money option can transition to an ATM if the market value rises or falls to equal the strike. The intrinsic value of an option also depends on the difference between strike and market price. Only ATM options have zero intrinsic value. When a strike differs from market value, intrinsic value exists equal to the amount of that difference. This intrinsic value contributes to the premium for in-the-money options.

Traders closely monitor the activity between strike and market prices over the life of an option to determine when transitions between ATM, in the money, and out of the money occur. This informs strategy adjustments and decisions to exercise options before expiration if optimal intrinsic value exists.

What is the relevance of At The Money and Near The Money?

At the money (ATM) is an option where the strike price equals the current market price of the underlying asset. Near the money (NTM) describes options with strike prices close to, but not exactly equal to, the market price. Traders sometimes use ATM and NTM interchangeably as general terms for options close to being at the money. However, they have important differences since ATM options have zero intrinsic value while NTM options have some degree of intrinsic value.

An ATM option with a strike equal to market price has no intrinsic value because there is no benefit to exercising it based on the strike versus market differential. All of its premium consists of time value based on volatility and time to expiration. NTM options have strike prices slightly higher or lower than the market price. This minor difference creates a small amount of intrinsic value and reduces time value compared to ATM options. The smaller the difference, the less intrinsic value exists.

For example, consider a call option with a strike of Rs.49 when the stock trades at Rs.50. This NTM call has Rs.1 of intrinsic value since the strike is Rs.1 “in the money” or below market price. An ATM call with a Rs.50 strike would have no intrinsic value when the stock is Rs.50.

Traders use NTM and ATM interchangeably when discussing general trading strategies around the current market price. For example, a trader planning to trade NTM calls sometimes also considers similar ATM calls. In this case, ATM and NTM both reflect closeness to the market price. However, for strategies where intrinsic value is a key consideration, traders must distinguish between ATM and NTM options. For example, selling covered calls to collect time value premium favors ATM over NTM since ATM has a higher time value.

The mix of intrinsic value and time value is critical. NTM options make better long call spread legs than ATM since they have higher delta and intrinsic value. Higher theta makes ATM better for short-call spread legs.

How to use At The Money in Trading?

The key is recognizing their unique risk-return profile versus in-the-money (ITM) or out-of-the-money (OTM) options. ATM options have strike prices equal to the current market price of the underlying asset. With no intrinsic value, their premium consists entirely of time value based on volatility and time remaining until expiration. ATM options are often incorporated directionally for bullish or bearish bets since they are poised right at the current market price. For example, buying ATM calls provides leveraged upside exposure if the stock rallies above the strike price. ATM similarly benefits from a decline in the underlying. Define your market outlook and use ATM options to capitalize if that view proves correct.

Another application of ATM options is constructing volatility spreads. ATM options maximize exposure to changes in volatility. An ATM straddle profits from a significant move either up or down. Build an ATM strangle to benefit from a large move outside the breakeven points. Manage these positions actively around earnings or events.

You will also be able to use ATM options as part of multi-leg strategies like butterflies, condors, or iron condors that incorporate options at different strike prices. For example, a call butterfly combines an ATM call, an OTM call, and an ITM call. The mix of option “Greeks” from the ATM, ITM and OTM legs allows fine-tuning the risk-reward profile.

Hedging a portfolio or directional positions in the underlying ATM options provides efficiency from mostly time value premiums. Their cost is lower than comparable ITM options. Collar strategies combining a long stock position with a protective ATM put and covered call are popular for hedging.

Finally, recognizing ATM options provides liquidity advantages in some cases. Their volume is generally higher than deeply ITM or OTM options. This becomes important when constructing multi-leg strategies involving potentially illiquid options. Factor this volume benefit of ATM options into your trade planning.

The keys to utilizing ATM options are understanding their unique risk-return dynamics, capitalizing on volatility exposure, incorporating them into multi-leg strategies, leveraging for efficient hedging, and recognizing potential liquidity advantages – while always actively managing your positions.

What trading strategy works best with the ATM Option?

Long Straddle is a trading strategy that works with ATMs.

: Definition, How it Works, and How It Is Determined 22")

The long straddle involves buying an ATM call and an ATM put on the same underlying asset with the same expiration date. It benefits from a significant move up or down in the underlying price. Maximum loss is limited to the premiums paid if the price stays flat. ATM options maximize volatility exposure while minimizing cost. Below are some other strategies.

Like the long straddle, the long strangle profits from a large price movement in either direction. However, out-of-the-money options are purchased instead of ATM options. This further reduces cost but requires an even greater move for profitability. ATM options will cost more but provide greater gamma and probability of success.

Writing covered calls generates income by selling call options against a long position in the underlying stock. ATM calls maximize time value premium income compared to in/out of the money calls. The goal is earning premiums as the stock is held, not assigned. ATM call values decay rapidly, which benefits the seller.

Collars combine a long stock position with a protective ATM, put purchase below the current stock price, and covered call sold above the price. The ATM put hedge protects against the downside without significant premium cost, while the short call generates income to offset the put purchase cost.

Iron condors involve simultaneously selling an OTM put and call while buying further OTM put and call to create a range position. Adding an ATM put and call creates an iron butterfly with a higher probability of profit but lower credit received. ATM options increase the likelihood of expiration success.

Synthetic positions replicate other instruments using options combined with stocks or futures. ATM call options allow the efficient construction of synthetic long stock positions when paired with short futures on the same asset. Managing synthetic positions is easier with ATM options.

Any spread benefiting from increasing implied volatility favors ATM over in/out of the money options. Time value comprises most of the ATM premium, so volatility growth directly increases ATM values. ATM back spreads, straddles, and strangles maximize volatility exposure.

ATM options are well-suited for strategies focused on volatility and time decay effects. Their exposure to implied volatility fluctuations and time value decay enhances profit potential.

When to trade ATM Option?

Trading ATM options is advantageous when you have a neutral outlook on market direction and want to maximize leverage while minimizing cost. Uncertainty about further upside or downside makes ATM options positioned at the current market price allow benefiting from either direction. ATM options are also ideal when constructing volatility trading strategies around events like earnings announcements. Their premium consists largely of time value derived from implied volatility. So ATM options maximize exposure to volatility expansion leading into binary events. Strategies like straddles and strangles benefit most from using ATM options.

Periods of historically low volatility present another opportunity to use ATM options. Their higher time value allows benefiting from an increase in volatility. Implied volatility rises mean the value of ATM options will increase more than comparable out-of-the-money options. Some traders specifically utilize ATM options during low-volatility environments to position for expansion. The higher vega makes ATM options more reactive to volatility, enabling leveraged participation if volatility picks up.

ATM options also provide relatively higher liquidity when trading less popular underlying assets or constructing complex multi-leg option spreads. The volume of ATM options tends to be greater than deep in-the-money or deep out-of-the-money options.

ATM options offer efficiency from mostly time value premiums when hedging portfolio exposure or existing positions in the underlying asset; their lower cost than comparable in-the-money options reduce the hedging cost while still providing downside protection.

Leading into binary events like earnings, product releases, FDA decisions, etc, ATM options provide maximum exposure to the announcement. Straddles or strangles allow benefiting from upside or downside price swings from the news. Periods of historically low volatility present an opportunity to trade ATM options to maximize exposure to potential volatility expansion. ATM options are more sensitive to volatility changes due to higher vega.

Why buy the ATM Option?

ATM options tend to have the highest daily trading volumes and liquidity compared to out-of-the-money or in-the-money options. This makes it easier to get into and out of positions. ATM options provide maximum leverage since they are poised right at the current value. A small move in the underlying translates to a significant return. ATM options offer a balance of risk and reward. They have about a 50% chance of expiring worthless or in the money. Their limited risk is known upfront to the premium paid. An ATM option’s entire premium consists of time value driven by implied volatility.

Their value benefits the most from increases in volatility. They provide flexibility for neutral strategies, directional trades, volatility plays, or hedging. Since they are at the current market price, they can capitalize on the upside and downside. Hedging with ATM options is efficient since most of the premium is time value rather than higher intrinsic value. Their cost is lower than comparable in the money options. Time value decays rapidly for ATM options as expiration approaches. Short option sellers benefit from steadily declining premiums if the underlying price stays flat.

Is the ATM Option profitable?

Yes, at-the-money (ATM) options are certainly profitable trading instruments when used properly as part of an options trading strategy. However, ATM options do not have inherent profitability simply due to their status of having strike prices equal to the underlying asset’s market price. ATM options have the potential to be profitable. However, profitability depends significantly on how the options are traded, which strategy is used, and whether the trader’s market outlook proves correct before expiration.

Should you sell the ATM Option?

Selling at the money (ATM) option is an effective strategy for experienced options traders in the right situations, but it does come with defined risks to manage. The advantages of selling ATM options include collecting higher premiums due to maximum time value, benefiting from rapid time decay as expiration approaches, roughly 50% probability of expiring worthless, and limited risk defined by the strike price. However, traders must be cautious of downsides like increased gamma risk, uncertain directional outlook, and potential margin requirements for uncovered shorts. With proper position sizing, risk management, and an understanding of ATM dynamics, selling ATM options offer opportunities to profit from time value decay.

Is it better to buy ATMs instead of ITMs?

There is no definitive answer on whether ATM or ITM options are inherently “better” for all traders in all situations. Each has advantages and disadvantages that come down to an individual trader’s strategy, risk preferences, and market outlook. There are merits to buying both ATM and ITM options depending on the trading strategy and market outlook. ITM options provide greater leverage through a higher delta and probability of finishing in the money but have higher premium costs and lose upside potential.

ATM options offer maximum leverage due to lower premiums, enabling more contracts, retaining upside/downside exposure at the current market price, and providing flexibility for directional or neutral strategies. Experienced traders utilize both ATM and ITM options, choosing one over the other based on individual trade goals, risk tolerance, and maximizing opportunities under current market conditions.

What is an example of an ATM?

Let’s assume trader A wants to trade options on Reliance Industries (RELIANCE). The current market price of RELIANCE shares is ₹2,500.

Trader A decides to buy 1 RELIANCE call option contract with a strike price of ₹2,500, expiring in 45 days. Since the strike price of ₹2,500 equals the current RELIANCE market price of ₹2,500, this call option is considered at the money (ATM). The ATM RELIANCE ₹2,500 call option has a premium cost of ₹150 per share. With each options contract covering 75 shares, the total premium paid by trader A is ₹150 x 75 = ₹11,250 for the long ATM call position.

At expiry in 45 days, if RELIANCE shares are trading above ₹2,500, the ₹2,500 calls will expire in the money and have intrinsic value. For every ₹1 increase above ₹2,500, the calls gain ₹75 in intrinsic value since they control 100 shares.

For example, image RELIANCE is at ₹2,600 at expiry, the ₹2,500 calls will have an intrinsic value of (₹2,600 – ₹2,500) x 75 = ₹1,500. In this scenario, trader A’s profits on the long ATM call position would be ₹1,500 – ₹11,250 premium paid = ₹750.

However, if image RELIANCE stays below ₹2,500 at expiration, the ATM ₹2,500 calls will expire worthless with no intrinsic value. In this case, Trader A’s loss is limited to the ₹11,250 initial premium paid for the calls.

By purchasing the ATM calls, Trader A sees leverage from RELIANCE moving above ₹2,500. But downside risk is defined if the stock stays flat or declines. This balance of risk-reward made ATM calls optimal for trader A’s bullish outlook.

What are the benefits of At The Money (ATM)?

Trading at the money option has eight main advantages for traders, including high liquidity. Below listed are them.

Higher Liquidity

ATM options tend to have higher liquidity and tighter bid-ask spreads compared to out-of-the-money or in-the-money options. The higher volume makes it easier to get in and out of ATM options positions quickly. This allows Indian traders to capitalize on short-term opportunities.

Lower Premium Cost

The premium cost for ATM options is lower than deep out-of-the-money options, which have a lower probability of expiring in the money. ATM options offer a better risk-reward ratio compared to OTM options. Traders pay comparatively lower premiums with reasonable odds of making profits.

Flexibility in Trading Strategies

ATM options are used to construct various trading strategies like iron condors, straddles, strangles, butterflies, etc. These strategies allow traders to profit from range-bound, neutral, or volatile markets. ATM options provide flexibility to adapt trading strategies for bullish, bearish, or neutral outlooks.

Lower Delta

ATM options have a delta value close to 0.5, which makes them less sensitive to changes in the price of the underlying asset. This lower delta reduces the risk compared to deep ITM or OTM options, which have deltas close to 1 or 0. A lower delta also means lower margin requirements for traders.

Better Hedging Tools

The balance of time value and intrinsic value make ATM options efficient hedging tools, especially for short-term neutral strategies like straddles and strangles. Hedging is easier with ATM options due to availability across multiple expiries and strike prices.

Risk Management for Long-Term Traders

ATM options are preferred for risk management by buy-and-hold investors holding large equity positions. ATM call options protect against the downside while allowing participation in the upside. Purchasing ATM options provides insurance against market crashes.

ATM Options for Short-Term Traders

Active traders can use ATM options to capitalize on upcoming events and data releases. The advantage is multi-fold – limited premium outlay, Defined and managed risk, Descent reward if the expected move plays out. ATM options offer favorable risk rewards for short-term directional bets.

Collar Strategies Using ATM Puts and Calls

Equity investors can hedge portfolios by buying ATM puts and selling ATM calls to create collar strategies. The put protects against the downside, while the call premium reduces the cost of protection. Collars using ATM options are easy to construct for average investors.

ATM options offer Indian traders several advantages like better liquidity, lower premiums, flexibility in trading strategies, and efficient hedging. Both short-term traders and long-term investors benefit from using ATM options in Indian markets.

What are the risks of At Money (ATM)?

ATM options offer several benefits, but traders need to be aware of the associated risks, including lower reward potential

Lower Reward Potential

The breakeven point for ATM options is close to the market price of the underlying. Thus, profits are limited even if the view on market direction is correct. Traders are better off buying out-of-the-money options if expecting a significant move in the underlying. ATM options have lower profit potential compared to OTM options.

Time Decay Risks

ATM options consist of both intrinsic and time values. As expiration approaches, the time value decays rapidly. Traders need to correctly time the entry and exit to benefit from time value. Time decay can lead to losses even if the underlying moves favorably if held too close to expiry.

Vulnerable to Volatility Changes

Volatility changes can negatively impact ATM options. An increase in implied volatility raises ATM premiums quickly, while a sharp fall in volatility causes premiums to decline rapidly. Traders can get whipsawed if volatility reversals are not anticipated correctly.

Requires Accurate Market Direction Forecast

To profit from ATM options, traders need to accurately forecast the market direction, magnitude, and timing of the expected move. Even a small error in the forecast can result in losses due to the lower reward potential. Getting market direction wrong can lead to large losses.

Risk of Early Exercise

For ATM options on dividend-paying stocks, there is a risk of early exercise around dividend dates. Short ATM call options are assigned early means traders may lose time value and miss out on subsequent profits. Early exercise can happen even if the in-the-money amount is insignificant.

Wide Bid-Ask Spreads in Illiquid Markets

In illiquid markets, ATM options can have wide bid-ask spreads, which increases trading costs. Wider spreads make profitable exits difficult at times, forcing early closures at unfavorable prices. This risk is higher for stock or index options with limited liquidity.

Risk of Overpaying for ATM Options

Beginner traders often overestimate the probability of large moves and overpay for ATM options. The premium paid can become a loss if the forecast move does not materialize within the expiry. Paying too much premium is a common mistake.

Assignment Risk on Short ATM Options

Short ATM options have higher odds of getting assigned on expiry compared to OTM options. Traders sometimes face unintended assignments and are forced to buy or sell the underlying at unfavorable prices.

Traders should take the time to fully understand these risks before using ATM options in trading strategies. Proper position sizing, disciplined trade management, and risk mitigation techniques are essential when trading ATM options.

What is the difference between ATM and other types of Option Moneyness?

At-the-money (ATM) options have a strike price equal to the current market price of the underlying asset. This differs from in-the-money (ITM) and out-of-the-money (OTM) options in key ways,

Premium Composition

ATM options consist entirely of time value in the premium with no intrinsic value. ITM options have significant intrinsic value, making up part of the premium. OTM has solely time value premiums like ATM, but lower time value since there is less chance of becoming profitable.

Delta

The delta of an ATM option is close to 0.50, meaning it has about a 50% probability of expiring in the money. ITM options have a higher delta approaching 1.0. OTM options have a lower delta, around 0.20-0.30.

Gamma

ATM options exhibit the highest gamma, which means their delta changes more rapidly with movements in the underlying asset price. Gamma is lower for both ITM and OTM options.

Theta

Time decay for ATM options accelerates as expiration nears. They have higher theta than OTM but lower than ITM options. Maximum time value results in greater theta decay.

Vega

Vega measures sensitivity to volatility. ATMs tend to have the highest vega. ITM and OTM vega are constrained by higher intrinsic value and lower time value, respectively.

ATM options, characterized by their Option Moneyness, offer a balanced risk-reward profile with about even odds of profit or loss. ITM options, with a different Option Moneyness status, have a higher probability of finishing in the money but cost more. OTM options are cheaper but, due to their Option Moneyness, have a lower chance of success.

Previous Article

Previous Article

26")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.