Synthetic put options are strategic combinations of options and stock positions designed to mimic the payoff of a long put contract, providing traders with flexible ways to manage risk and express bearish views. Synthetic put options traces its roots to the foundational principle of put-call parity, which links the prices of puts, calls, and the underlying asset.

This relationship was formalized in the 1970s as financial derivatives markets expanded, allowing for creative hedging and speculation techniques.

Synthetic puts emerged as a popular alternative in institutional trading desks and have since become a staple for sophisticated retail traders seeking efficient hedges or speculative downside exposure.

Why Use a Synthetic Put Options Strategy?

A synthetic put options strategy is used as a flexible and capital-efficient substitute for a direct long put, especially when puts are illiquid or expensive. A synthetic put options gives traders and investors a strategic edge in environments where traditional put options are hard to obtain or not cost-effective, while still providing robust downside protection.

One of the main appeals of the synthetic put is its ability to replicate long put exposure using two widely available instruments: short stock and long call options. This is particularly valuable when direct puts are either not trading in sufficient volume or the bid-ask spreads are too wide, making execution costly.

Capital efficiency is another key benefit. In margin-eligible accounts, the capital required to short stock and buy a call is often significantly less than the cash outlay for outright put purchases, especially in high-priced stocks.

This makes the synthetic put a preferred tool for institutions or active traders looking to hedge large portfolios or express bearish views without tying up excessive capital.

When to Use a Synthetic Put Options?

A synthetic put option is best used when you have a bearish bias on a stock and desire downside exposure with defined, limited upside risk. This strategy is particularly relevant when you expect the stock price to decline or volatility to increase, but face constraints that prevent direct put option purchases.

Traders often turn to synthetic puts when they want to profit from a drop in the underlying but also want to cap their potential losses if the market moves against them. The short stock component ensures that the position benefits from any substantial downward movement, while the long call limits the maximum loss, creating a safety net if the stock rallies.

An ideal scenario for deploying a synthetic put is during periods of low implied volatility, with the expectation that volatility will rise. Since the synthetic position includes a long call, it benefits directly from increased implied volatility, which raises the value of the call and thus provides a more favorable risk/reward ratio as the trade matures.

Regulatory and margin constraints often lead to the use of synthetic puts. Some accounts are restricted from buying puts directly due to regulatory or internal guidelines, but allow for the short stock and long call combination. This workaround enables portfolio managers and traders to maintain desired hedges or speculative positions without breaching compliance requirements.

Margin efficiency is another timing consideration. In margin-eligible accounts, the synthetic put often requires less upfront capital than purchasing a long put, especially in higher-priced stocks. When capital allocation is a concern, or when you want to use leverage responsibly, this strategy stands out.

How Option Greeks Affect Synthetic Put Options?

Option Greeks affect synthetic put options by determining their sensitivity to price, time, and volatility—primarily resulting in a net negative delta, low gamma, negative theta, and positive vega at entry.

Delta represents the position’s sensitivity to price changes in the underlying stock. For a synthetic put, the net delta is strongly negative, typically close to -1 at initiation, because the short stock position has a -1 delta and the long call has a positive delta (but less than 1). This means that for every Rs. 1 drop in the underlying, the synthetic put gains close to Rs. 1, very similar to a long put.

Gamma, which measures how delta changes as the underlying moves, is generally low for synthetic puts but increases as expiration approaches. This low gamma results from the offsetting nature of the stock and call legs, but as expiry nears, the position’s delta can shift more rapidly, especially if the underlying hovers near the strike price.

Theta, or time decay, is negative for synthetic puts due to the long call leg. As time passes, the value of the call option erodes, reducing the overall value of the synthetic put if all else remains constant. This means holding the position closer to expiry without a corresponding drop in the stock price will result in losses from time decay.

Vega measures sensitivity to changes in implied volatility. Synthetic puts benefit from rising volatility, as the long call’s value increases with higher implied volatility. This positive vega exposure is advantageous when entering the position in low-volatility environments with the expectation of a future volatility spike.

To visualize this, here’s a simple Greek profile for a synthetic put at inception

| Greek | Synthetic Put | Impact |

| Delta | -0.95 to -1 | Gains as price falls |

| Gamma | Low, rises near expiry | Delta changes faster near expiry |

| Theta | Negative | Loss from time decay |

| Vega | Positive | Gains as volatility rises |

As market conditions shift, the synthetic put’s risk profile evolves, requiring ongoing monitoring and potential adjustments to keep risk/reward in line with your objectives.

How Implied Volatility Affects Synthetic Put Options?

Implied volatility (IV) affects synthetic put options by increasing their value when IV rises, since the long call leg benefits from this change. This makes the synthetic put especially attractive when entered in low-IV environments with the expectation of future volatility spikes.

The synthetic put’s positive vega exposure means that it gains value as implied volatility increases. Since the long call becomes more expensive when volatility rises, the overall synthetic position appreciates, mirroring the behavior of a long put in similar conditions.

This relationship makes the strategy highly sensitive to volatility forecasts and market sentiment.

Ideally, you want to initiate a synthetic put when implied volatility is low, as the cost of the call is minimized and there is room for IV expansion. If volatility rises after the position is established, the call’s value increases, which helps offset any adverse movement in the underlying or further enhances gains if the stock drops.

However, the synthetic put is not suitable during periods of “IV crush,” such as immediately following major news events or earnings announcements. In these scenarios, implied volatility often collapses rapidly, causing the value of both puts and calls to drop sharply.

Since the call is a primary component of the synthetic, this decline can erode the value of the position, even if the underlying moves in your favor.

Compared to a real (direct) put, the synthetic put’s sensitivity to IV is nearly identical, provided the put-call parity relationship holds. Both structures gain from rising volatility and suffer when volatility falls, but the synthetic offers additional flexibility in rolling or adjusting legs if market conditions change.

How to Trade using Synthetic Put Options?

To trade using a synthetic long put strategy, follow this step-by-step approach to replicate the payoff of a long put without directly purchasing one.

- Identify a Bearish Candidate

Begin by selecting a stock that is showing signs of weakness or potential correction. In this case, Eicher Motors is chosen based on the weekly chart structure. The stock has seen a consistent uptrend but now appears to be stalling, suggesting possible profit booking or short-term correction. This makes it a strong candidate for a bearish trade setup.

- Short the Stock (via Futures)

Since short selling equity stocks is not allowed for positional trades on NSE, the trader chooses to short futures instead. A futures short position allows directional bearish exposure and is paired with a long call to limit risk. This futures short acts as the core bearish position in the synthetic put.

- Buy a Call Option (Same Strike & Expiry)

To limit the risk on the upside, the trader buys an ATM call option of the same expiry as the futures contract. This hedge transforms the futures short into a synthetic long put. The call acts as insurance if the price unexpectedly rises.

- Ensure Margin Requirements are Met

One major advantage of synthetic puts is the reduced margin requirement. While a naked futures position might require about ₹1,65,000, the synthetic put position (futures short + long call) only needs around ₹38,000, making it highly capital-efficient.

Below is the position structure.

- Short 1 Futures Contract @ ₹5,405

- Buy 1 ATM Call Option (Strike = ₹5,400) @ ₹147.6

- Lot Size = 175

This setup replicates a long put payoff, profiting when the underlying stock falls, while capping losses if the price rises sharply due to the long call hedge.

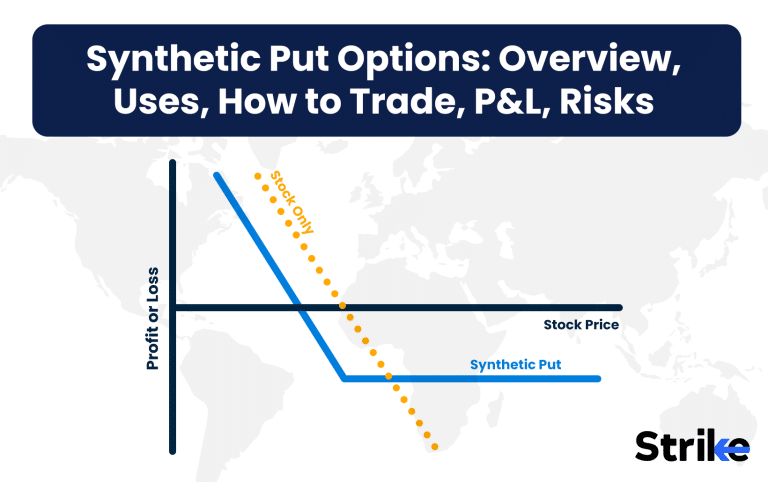

What are the Maximum Profit & Loss, Breakeven on a Synthetic Put Options?

The maximum profit on a synthetic put options strategy occurs if the underlying falls to zero, while the maximum loss is limited to the difference between the stock price and call strike plus the call premium; the breakeven is stock price minus net premium paid. Understanding these points is crucial for risk assessment and trade planning.

Maximum profit is realized if the underlying stock goes to zero. For example, if you short ABC at Rs. 100 and buy a Rs. 100 call for Rs. 5, your maximum gain is Rs. 100 (from the short sale) minus the Rs. 5 call premium, totaling Rs. 95 per share or Rs. 9,500 per contract.

Maximum loss is capped because the long call limits your risk above the strike. Continuing the example above, if ABC rises sharply, the call offsets losses above Rs. 100. Your loss is the difference between the short sale price and the strike (if any), plus the call premium.

For a short at Rs. 100, bought a Rs. 100 call for Rs. 5, and the stock ends at Rs. 120, the call covers the Rs. 20 move above Rs. 100, so your loss is Rs. 5 per share, or Rs. 500 per contract.

The breakeven point is reached when the underlying price equals the initial short sale price minus the call premium paid. Using the same numbers: Rs. 100 (short sale) – Rs. 5 (call premium) = Rs. 95. If the stock ends at Rs. 95, you break even.

In this graph, the payoff turns positive as the stock drops below Rs. 95 (assuming Rs. 5 call premium), is flat between Rs. 95 and Rs. 100, and losses are capped above Rs. 100.

What are the Risks of Synthetic Put Options?

Synthetic put options carry risks including unlimited loss potential if the call leg is not managed, margin requirements on short stock, assignment risk, slippage, and operational complexity compared to a simple long put. Each of these elements must be understood and managed to avoid unexpected outcomes.

The primary risk comes from the short stock position. If the underlying stock rises significantly, losses accumulate rapidly. Although the long call caps this loss, if the call is not held through expiry or is inadvertently closed, the position becomes a naked short with unlimited risk. Constant monitoring is needed to ensure the hedge remains intact.

Margin requirements for shorting stock are another concern. Brokers require significant collateral, and if the stock price moves against you, margin calls can force liquidation at unfavorable prices. This risk is compounded in volatile markets, where price spikes can trigger forced closures.

Assignment risk arises if the call option is exercised early, particularly in American-style options. If the call is deep in-the-money before expiry and is exercised, you could be assigned, resulting in the need to buy back the stock at the higher market price. This operational detail adds complexity not present in a single long put.

Slippage and liquidity issues also affect the strategy. If the underlying stock or call options are illiquid, entering or exiting the synthetic put at the desired price may prove difficult, resulting in worse-than-expected execution and higher transaction costs.

Is Synthetic Put Options Strategy Profitable?

Yes, a synthetic put options strategy is profitable when the underlying stock declines significantly or volatility rises after the position is established. The structure’s profit comes from the short stock position, with the long call capping losses and providing additional value if implied volatility increases.

Profitability depends on accurate market timing and volatility forecasts. If the trader correctly anticipates a price drop or a spike in volatility, the synthetic put can generate substantial returns for relatively low upfront capital. The main benefit is leveraged downside exposure, with risk defined by the call premium and capped by the call’s protection.

Is Synthetic Put Options Bullish or Bearish?

A synthetic put options strategy is inherently bearish, as it profits from a decline in the underlying stock’s price. The core component—a short stock position—means the position gains value as the underlying moves lower, while the long call limits potential losses if the stock rallies.

This bearish orientation makes the synthetic put ideal for traders with a negative outlook on a security, or for those seeking protection against downside risk in a portfolio. It is not suitable for neutral or bullish market views, as profits rely on the underlying declining in value.

What are Alternatives to Synthetic Put Options Strategy?

Alternatives to the synthetic put options strategy include direct long puts, bear put spreads, short calls, and inverse ETFs for equity exposure, each offering distinct risk/reward profiles. Choosing the right alternative depends on your goals, risk tolerance, and market conditions. Here’s a comparison of these alternatives

| Strategy | Cost | Risk | Reward | Use Case |

| Long Put | High | Limited | Unlimited | Simple downside hedge or speculation |

| Bear Put Spread | Lower | Limited | Limited | Cost-effective, defined-risk bearish |

| Short Call | Low | Unlimited | Limited | Income-focused, bearish-neutral |

| Inverse ETF | Varies | Limited | Limited | Equity-only accounts, hedging broad indexes |

A direct long put is the simplest way to bet on a decline, offering unlimited profit potential with limited risk (the premium paid). However, it can be expensive, especially in volatile markets.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 20")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 21")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 22")

: Overview, 10 Types of Indicators, Settings for Different Markets 24")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 26")

No Comments Yet.