A long put, also known as a put option, is a derivative contract that gives the buyer the right, but not the obligation, to sell the underlying asset at a predetermined price on or before a specific expiration date. A long put is one of the most common option strategies used by traders to profit from a bearish market outlook.

A long put works by allowing traders to short-sell the underlying asset at the strike price. A trader who purchases a long put on ABC stock with a Rs.50 strike price has the option to sell ABC at Rs.50, regardless of the market price dropping below Rs.50.The maximum profit is capped at the strike price minus the premium paid and is realized if the stock falls to zero.

The long put helps limit the downside risk. The maximum loss is restricted to the premium paid to buy the put. This defined risk is an advantage over short selling, which has unlimited loss potential if the stock rises. Long puts are exited any time before expiration by selling them back to close the position.

Traders buy long puts when they expect the price of the underlying to decline. It provides leveraged exposure to profit from bearish moves without needing to sell short. Long puts also hedge long stock positions and provide insurance against potential down moves. Portfolio managers use put options to limit portfolio risk.

What is a Long Put?

A long put, also referred to as a put option, is a derivative contract that gives the purchaser the right, but not the obligation, to sell the underlying asset at a predetermined price on or before the expiration date. The long put gets its name because it represents a long position in a put option, just like going long stock. When a trader buys a put option, they are long a put, giving them a right to sell the underlying asset in the future. This is in contrast to shorting a put, where the trader sells a put option and collects a premium while taking on the obligation to buy the asset if assigned.

A long put option position is created when a trader pays an upfront premium to purchase a put contract from the options writer. This premium paid is the maximum possible loss on the trade. In return, the long put holder obtains the right to sell 100 shares of the underlying stock per contract at the specified strike price until the expiration date.

The maximum loss on a long put is limited to the premium paid to purchase the option. If XYZ remains above Rs.50, the long put option expires worthless, and the loss is the cost of the premium. The defined and limited risk of options is an advantage over short-selling the stock outright.

The flexibility and defined risk characteristics make long puts an essential tool for investors and traders looking to capitalize on declining asset prices. An effective long-put strategy requires choosing the right strike, managing time decay, and disciplined risk management. When used prudently, long puts offer substantial profit potential while limiting losses.

How does a Long Put work?

A long put works by giving the buyer the right, but not the obligation, to sell the underlying asset at the strike price, allowing them to profit if the asset price falls below the strike price. To create a long put position, the trader purchases a put option contract on the underlying asset they wish to trade. The purchase involves paying an upfront premium to the options seller. This premium is the maximum potential loss if the long put expires worthless.

The premium paid depends on factors like the strike price chosen, time to expiration and implied volatility. Out-of-the-money puts are cheaper as they have a lower chance of turning profitable before expiry.

In return for the premium, the long put holder receives the right to sell 100 shares of the underlying asset per contract at the preset strike price until expiration.

The potential outcomes of a long-term position are

Maximum Profit – Strike Price – Premium Paid

The profit is maximized if the underlying asset price falls to zero before expiry. The put holder sells the stock at a higher strike price. The maximum reward equals the strike price less the premium paid.

Maximum Loss – Premium Paid

Should the asset price stay above the strike at expiration, the long put option becomes worthless. The purchaser of the put limits their maximum loss to the premium amount they initially paid

Breakeven Point – Strike Price – Premium Paid

The asset price must fall below the strike price less the premium paid for the long put position to break even. This is the breakeven point. The long put holder only needs to hold expiration to realize a profit. If the asset price drops sufficiently below the strike price, the put option will gain intrinsic value. The trader chooses to exercise their right to sell at the strike price and immediately capture the in-the-money profit.

Alternatively, they sell the appreciated long put option back in the market to exit the position early and book the gains. Options have extrinsic time value on top of intrinsic value prior to expiry.

An important factor to consider is the time decay of options, also called theta. The value of the long put option erodes as expiry approaches due to declining time value. Traders look to manage the impact of time decay on long puts through timely entries, exits and rolling over positions to later expiries.

How does a Long Put differ from other types of Option Strategies?

A long put differs from other option strategies like covered calls, protective puts, credit spreads and iron condors in profit potential, tail risk, and objective. Compared to naked calls, long puts have defined risk. Understanding these contrasts allows traders to select the most suitable strategies for their market outlook and risk appetite.

A long call gives the buyer the right to buy the underlying asset at the strike price on or before expiry. It profits from bullish moves in the underlying. The maximum loss is limited to the call premium paid. Long puts and long calls are symmetrical option trading strategies. Calls make money when prices rise while putting profit from falling prices. Both have defined and limited risk.

A covered call is created by selling a call option against an existing long stock position. The trader collects the call premium to generate additional income from the long stock. The long stock acts as cover in case the call is assigned. The profit is capped at the strike price if the stock rises. Covered calls benefit from neutral to moderately bullish markets. Unlike covered calls, long puts do not need existing stock positions. Their profit potential is strongly leveraged to downward moves without the need for short-selling stocks.

The protective put strategy involves purchasing puts to hedge downside risk on an existing long stock position. The put acts as an insurance policy protecting against losses if the stock falls. While protective puts are bought to hedge long stocks, long puts are also used as standalone positions to speculate on bearish moves without needing to own the stock.

Covered puts involve short selling a put option against cash reserves kept aside to buy the stock potentially. The trader collects the put premium while the obligation to buy the stock at the strike price is assigned. Long puts are bought and don’t have the assignment obligation. Covered puts profit from neutral markets, while long puts need bearish moves to profit.

This strategy is constructed by buying a low strike call and simultaneously selling a higher strike call to offset part of the debit. The maximum profit is the difference between the call strikes and net debit. The bull call spread has limited profit potential due to the short call leg capping gains. Long puts have uncapped upside if the underlying falls sharply.

The iron condor combines a bull put spread and a bear call spread. The maximum profit is the net credit received. The risk is limited between the inner short strikes. It profits from range-bound markets. Long puts have greater leverage to large downside breakouts. Iron condors are tactical non-directional trades, unlike the directional long put.

What is the importance of a Long Put in Options Trading?

Long puts are important primarily because they open diverse opportunities in options trading like speculation, hedging, income generation, risk management and easy access to short selling. This makes long puts a foundational strategy for active traders and investors looking to incorporate bearish trades tactically within balanced portfolios.

A key use of long puts is speculating on bearish moves. Traders buy puts when they expect the underlying asset price to decline. Buying a put provides leveraged profit potential without the need to short-sell the asset. The maximum loss is restricted to the premium paid.

Long puts offer directional exposure to capitalize on falling markets. Traders use puts to speculate on various asset classes like stocks, commodities, currencies and indices. Puts provide a cost-effective way to profit from downtrends.

Investors holding long positions in an asset hedge downside risk by buying puts. It acts as portfolio insurance against adverse price moves. For example, long stockholders buy puts on the same stock to limit maximum loss.

The protective puts ensure the stock value remains protected at the strike price. It defines the exit price similar to a stop loss order. Hedging is important for mitigating portfolio risk.

Long puts allow traders to collect premium income through covered put writing. This involves buying long puts and simultaneously selling cheaper out of the money put against them. The long puts act as coverage in case the short puts are assigned. Income is generated from the short put premium. Long puts facilitate this neutral options strategy.

Long puts have limited downside risk, which is defined as the premium paid. This is unlike short selling, which faces potentially unlimited loss if the stock rallies. Portfolio managers use long puts to reduce portfolio risk in volatile markets. The defined and capped risk of long puts makes them useful hedging instruments and strategic portfolio insurance during market crashes.

Options provide an alternative way to benefit from falling asset prices without the need to short stocks. Shorting stocks has complications like high costs, limited availability of shares to borrow, and uncapped loss potential. Long puts allow similar bearish exposure with clearly defined risk parameters. Puts grant short sell-like payoff but without operational complexity and unlimited risk of shorting.

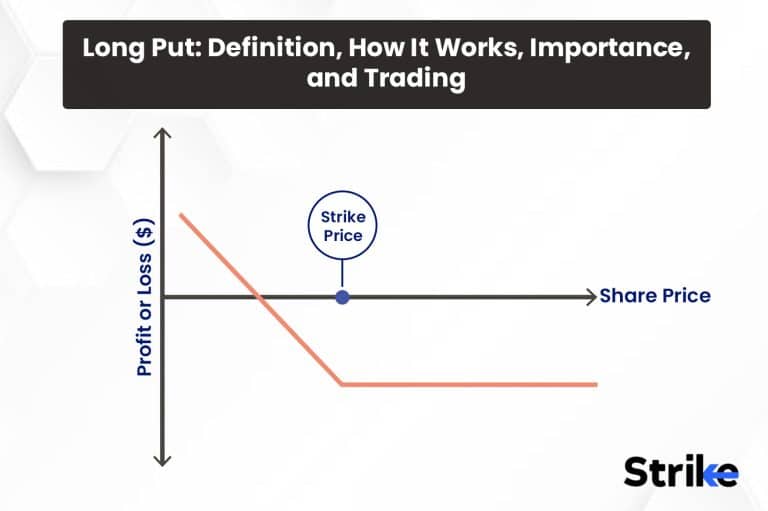

What does a Long Put diagram look like?

Below is what a long-out diagram will look like.

This diagram shows the payoff graph of a long put position. The maximum loss is limited to the premium paid to buy the put option contract. The profit increases as the underlying asset price drops below the strike price. The upside profit potential is uncapped if the price falls to zero. The breakeven point is equal to the strike price, less the premium paid.

How to Enter a Long Put?

Entering a long put position involves buying put option contracts to benefit from a bearish market outlook. The first step is identifying an asset or sector with a bearish bias where a price decline is expected. Research to determine the catalysts that could drive prices lower. This may include factors like weakening fundamentals, negative technical patterns, declining growth estimates, macroeconomic risks, or high valuations indicating overextension.

Select an appropriate expiry based on the anticipated price move timeline. Near-term expiries are suitable for short-term directional trades, while longer-dated puts allow time for the view to play out. Typically, 3-6 month expiries balance the duration of the put and minimize time decay.

The strike price determines how far the asset must drop for the put to turn profitable. Lower strike out-of-the-money puts are cheaper but have a lower probability of gains. Higher in-the-money put strikes require less downside but have higher premium costs.

Evaluate the breakeven level, which is the strike price less premium paid. Check the potential risk-reward ratio based on the expected downside and size of the premium paid. Higher reward potential relative to the defined maximum risk indicates a favourable setup.

Place the long put trade by buying put option contracts on the chosen underlying asset at the desired strike and expiry. One contract grants the right to sell 100 shares. Adjust the number of contracts purchased to size the position properly.

To reduce premium outlay, use credit or debit spreads. This involves selling a higher strike put to fund purchasing the lower strike long put. The short put caps the upside but lowers the net cost.

Use stop-loss orders below the technical support level to limit maximum loss. The stop-loss order automatically exits the long put if the underlying price rises above a predefined level.

Actively track the underlying asset price movement and relevant news flow to determine if the bearish view is playing out as expected after putting on the long position.

Consider taking profits early or rolling the put to a lower strike or further expiry if the asset continues trending lower. Close out the puts if the thesis fails to avoid maximum loss.

The trader should map the bearish setup, smartly select the right strike and expiry, efficiently structure the spread, proactively manage risk, and diligently monitor the position to trade long puts effectively. Proper analysis, execution and discipline are key to maximizing gains.

How to Exit a Long Put?

Exiting a long put position involves strategically closing out the put options trade to capture profits, limit losses or manage the position. Traders place advance take profit orders to close out long puts at a predetermined profit target automatically. As the asset price falls and the puts become deeper in the money, the take profit orders get triggered to exit with profits.

The profit target is typically set at a technically significant support level or based on a favourable risk-reward ratio relative to the premium paid. Take profits and realize gains without needing to monitor the position constantly.

Stop loss orders are used to limit the maximum loss on the long puts. Stop loss orders automatically close out the losing long puts if the underlying asset price rises above a defined level. Appropriately setting stop loss levels below key resistance or technical reversal points allows exiting losing puts while restricting losses to a fixed amount.

The long puts significantly increase in value and become substantially in-the-money when the underlying falls considerably below the strike price. The trader chooses to exercise the right to sell the underlying at the higher strike price and immediately capture the intrinsic profit. Exercising monetizes large intrinsic gains instead of waiting until expiration. The shares are instantly sold at the strike price when exercising the long puts.

Instead of exercising, traders sell-to-close out long put options if they gain sufficient intrinsic value prior to expiry. Selling the puts closes the position and realizes gains from the appreciated put value without needing to hold until expiration. Early exits minimize time decay. The time value is highest when reselling the puts while still having remaining time to expiry.

Traders roll the long puts outward to a later expiration, assuming their bearish thesis maintains its relevance as expiry approaches. This involves simultaneously closing existing puts and opening new, longer-dated ones. Rolling defers time decay, allowing more time for the view to play out. The new puts are also opened at lower strike prices to increase leverage.

To offset time decay, long puts are sometimes combined with short-covered calls. The call premium income reduces the effective cost of holding long puts. The written calls provide downside protection with upside capped at the call strike. The long put hedges the short call exposure. This options collar strategy creates a range play while mitigating theta loss.

Considering initially implemented as a put debit or credit spread, traders leg out by closing the profitable long or short put side only. The other leg is retained longer to capture additional gains if the trend persists. Legging out decompresses the position, allowing greater exposure to favourably trending assets while booking partial profits.

What are the things to consider when using the Long Put strategy?

There are nine key factors to consider when using the long-put strategy. First, consider the potential position that could be created at the expiration. It’s also crucial to understand the effect of a change in volatility and the impact of time value on your strategy. Be clear about the maximum profit that is achieved and be aware of the maximum risk associated with this approach.

An appropriate market forecast is essential when deciding to use the long-put strategy, and you should also be mindful of the risk of early assignment. Calculating the breakeven stock price at expiration is another important step. Finally, before deciding to use this strategy, it’s advisable to engage in a thorough discussion to understand all aspects of the long-term strategy fully.

1.Potential Position Created at Expiration

Traders must analyze the potential position that could be created if the options are held till expiration because the outcome at expiration will determine the profit or loss realized on the long put trade.

Traders who need to be made aware of the impact of holding long puts till expiry sometimes incur unintended outcomes. The long put position transforms into a synthetic short stock position if assigned at expiration. Traders should factor this in while assessing the risk-reward scenario of letting the long puts expire in the money.

For example, consider a trader who buys a 3-month long put on a stock trading at Rs.50 with a strike price of Rs.45. If the stock drops to Rs.40 at expiration, the Rs.45 puts will expire in the money with Rs.5 of intrinsic value.

An unaware trader sometimes holds the puts, hoping for more profits. However, upon expiry, they would be assigned and obliged to sell the stock at Rs.45. Simultaneously, buying the stock from the market at Rs.40 to fulfill the assignment obligation results in a Rs.5 loss per share.

The trader now holds a synthetic short stock position with the stock at Rs.40. At the same time, their effective purchase price is Rs.45. This could lead to further losses if the stock rebounds higher, contrary to the trader’s bearish bias, creating unintended risks.

Alternatively, the trader properly evaluates the expiration outcome, which means they would recognize that the Rs.45 long put striking in the money essentially creates a synthetic short stock position at Rs.45. Since the current market price is Rs.40, it makes sense to close out the position and book profits rather than face risks from an unfavourable short stock position.

Assessment of potential outcomes enables informed decisions on early exercise, closeouts or expiration strategies. Exercising long puts just prior to expiration is preferable if the bearish view remains intact. This captures the intrinsic profit without needing to short the stock.

Rolling the option forward or closing positions reduces unintended risks. Knowing the implications of holding in, at or out-of-the-money long puts till expiry is vital for maximizing gains and optimizing risk management.

2. Effect of Change in Volatility

Volatility is crucial for traders implementing a long-put strategy to incorporate the effect of volatility changes in their analysis and position management. This allows the creation of more accurate profit and risk scenarios.

A long put benefits from increasing implied volatility. Higher volatility results in greater time value being priced into the put option. This causes the value of previously purchased long puts to appreciate, enabling the trader to sell the puts back at a higher market price and lock in profits.

However, volatility declines substantially after initiating long puts, which means the time value erodes, leading to a loss in the put’s premium. The declining volatility works against the trader’s position.

For example, a trader establishes a long put when implied volatility is high due to an upcoming binary event; once the event passes, volatility quickly drops, causing rapid time value decay in the long put premium.

Not accounting for this volatility contraction will result in an unexpected loss in the position. The trader could have minimized the loss by proactively planning the exit before the anticipated plunge in volatility post-event.

On the contrary, volatility spikes sharply higher, which means the trader gains huge leverage by strategically increasing the size of the long put position to capitalize on the amplified time value.

The ability to quickly adjust position size and re-evaluate pricing allows for creating a favourable risk-reward scenario. Traders who fail to adapt their position to changing volatility give up this potential edge. Long-put traders should observe historical and implied volatility metrics, anticipate potential changes, model the impact on put valuations, and proactively modify positions and exits accordingly.

Monitoring volatility enables capitalizing on volatility expansion while hedging against time value decay from volatility contraction. Incorporating volatility dynamics is key for optimizing long-put trade outcomes, sizing positions efficiently, and executing strategically timed entries and exits.

3. Maximum Profit

Evaluating the maximum profit potential is a key component when analyzing potential long-put option trades. Traders should assess if the maximum profit represents an attractive risk-reward ratio relative to the maximum potential loss. This helps determine if the long-term trade presents a favourable opportunity.

The maximum loss on long puts is fixed at the premium paid to buy the options. However, profit potential is unlimited if the underlying asset price declines to zero. So traders aim to capture large gains in exchange for the defined capital at risk.

Analyzing maximum profit potential guides position sizing as well. Higher potential profit allows committing more capital to increase position size and maximize absolute gains.

Estimating maximum profit based on technical downside price targets helps assess the upside potential versus downside risk. Favourable risk-reward ratios where maximum profit exceeds the premium paid indicate positive expected value. Considering maximum profit potential and sizing accordingly is key to implementing an efficient long-put strategy.

5. Effect of Time Value

Time value, also known as extrinsic value, is a critical component of an option premium as it represents the amount by which the option price exceeds the intrinsic value. For long-put options, evaluating the impact of time value and its erosion over the life of the option is very important.

At initiation, a long put’s premium consists entirely of time value since the put is purchased at the money or out of the money. This time value represents the chance of the put gaining intrinsic value prior to expiration. But time value decays over time as expiry approaches.

The rate of time decay accelerates in the last month before expiry. If the underlying does not decline below the strike price, the long put loses its entire time value and expires worthless despite being initially in the money.

For example, a 6-month put may be priced at Rs.4 due to longer duration. But if held too close to expiry, its value may diminish to Rs.1, even if its intrinsic value is Rs.2, due to time decay. The loss of time value reduces potential profits.

An understanding of time value enables the creation of appropriate profit targets and exit points for long puts. Traders track time decay to avoid losing time value near expiry. Exiting prior to accelerated decay allows for preserving time value and maximizing profits.

Rolling the options forward is used to defer time value erosion. Traders may also choose lower time value options if holding till near expiry. Incorporating time decay analysis improves trade management.

Time value is a transient but important component of the long put premium. Analyzing time decay patterns, planning timely exits, rolling options forward, and selecting appropriate expiries based on investment horizon allows traders to minimize loss of time value. This results in greater long-term profitability.

6. Appropriate Market Forecast

Effectively deploying long put options requires an accurate bearish market outlook. Only after developing high-conviction views on market direction based on extensive analysis should traders consider initiating long put positions. Any inappropriate forecast could lead to losses.

Consider a scenario where a trader buys long puts on a stock, predicting negative earnings results. However, the actual earnings exceed estimates, causing a price rally, and the puts become worthless. This situation leads to the realization of the maximum loss due to an incorrect forecast.

Prior to putting on long put trades, traders should utilize various analytical tools to build a bearish thesis. Studying price charts, indicators, support/resistance levels, market fundamentals, valuation models, macroeconomic trends, and geopolitical risks produces evidence for downtrend probability.

Backtesting determines if seasonality, cycles or historical trends support the potential for declines. Sentiment indicators may also confirm excessive optimism preceding market reversals. Building a firmly grounded bearish outlook is vital.

Traders should also evaluate alternate scenarios and consider hedges in case the forecast does not materialize. Long-put sizing should be moderated based on conviction level in the bearish view. Appropriate forecasting and measured positioning are crucial for long-term success.

7. Maximum Risk

The long put strategy involves purchasing put options on a stock to profit from a potential decline in the stock’s price. While long puts present an opportunity to gain from a bearish outlook on a stock, it is crucial to consider the maximum risk associated with this options strategy carefully.

Long puts offer limited profit potential but carry an unlimited risk if the stock’s price escalates. The maximum gain is the strike price minus the premium paid if the stock plunges to zero. Yet, a significant rise in the stock price results in the put options expiring worthless, causing the trader to lose the entire premium paid. Due to this asymmetric risk-reward ratio, traders must calculate the maximum loss based on the premium paid to judge whether the potential upside justifies the downside risk.

The clear parameters for position sizing and risk management come from defining maximum risk. Traders should risk only a minimal proportion of their account on any one trade. By ascertaining the maximum loss per contract and the overall position, traders can size the trade appropriately to confine the downside risk to acceptable levels. They base this on their account size, risk tolerance, and diversification strategy. It’s crucial to set loss limits for risk management, as these determine when a trader will exit a position that moves against them.

Traders estimate the likelihood of maximum loss by evaluating the fundamental and technical factors that might cause the put options to expire worthless. Analyzing the stock’s momentum, support levels, earnings outlook, and market sentiment helps determine if the stock is likely to undergo a downward shift, leading to profitable puts. Traders should support their bearish outlook with a thesis to justify taking on the maximum risk.

Reviewing implied volatility levels assists in assessing whether put option premiums are overpriced, thereby increasing maximum risk. Greater demand for puts, indicated by higher implied volatility, results in heightened premiums. This situation amplifies the potential loss if the puts expire worthless. A look at historical volatility levels helps decide whether heightened implied volatility will persist or revert to the mean.

It’s crucial to consider the impact of time decay on long puts when assessing maximum risk. Time value erosion accelerates as options approach expiration. Given everything else remains equal, a put with 30 days till expiry will have a higher premium than a 60-day put. The shorter the option’s term, the greater the time decay risk the trader assumes.

8. Risk of Early Assignment

The long put strategy involves purchasing put options to benefit from a potential decline in the underlying stock’s price. While long puts offer leveraged bearish exposure, traders must be mindful of the risk of early assignment, especially on short-dated, in-the-money puts. Assessing the chances of early assignment is critical when implementing long puts for several key reasons:

Firstly, early assignment leads to unanticipated losses. If a put holder is assigned early, they are forced to purchase the stock at the higher strike price versus the current market price. This subjects the trader to an immediate loss as they must buy high and sell low. If the trader lacks sufficient margin to take delivery of the stock, their brokerage will liquidate the position at a loss. Even if there is a margin available, the forced stock purchase locks in a loss.

Secondly, evaluating the likelihood of early exercise allows traders to incorporate the risk into position sizing and profit targets. Deep in-the-money puts far from expiry have a greater chance of early assignment. Traders adjust their size accordingly to limit exposure or aim for larger gains to justify the risk. Assessing this risk helps set realistic targets.

Thirdly, monitoring circumstances that increase chances of early exercise, like dividends, earnings, or corporate actions, allows traders to take proactive measures. For example, puts may be assigned before an ex-dividend date, so the short put holder misses out on the dividend. Traders exit positions early to capture remaining time value if early exercise is probable.

Fourthly, understanding the motivations behind early assignment helps traders evaluate probability. Counterparties may exercise options early to capture dividends, interest rate differentials or simply because it suits their investment strategy. Analyzing these motivations provides colour on how likely contra-parties are to exercise contracts prematurely.

Fifthly, reviewing trading volumes, open interest levels, and bid-ask spreads helps gauge the liquidity of the specific put options. Illiquid options have a higher risk of early exercise because the counterparty may have difficulty exiting their position otherwise. Conversely, highly liquid puts likely have lower early exercise risk.

Finally, studying historical early assignment trends in specific options provides clues into future probability. Puts on certain stocks with high dividends or in sectors like banking see higher rates of early exercise. Traders incorporate historical tendencies into their analysis.

9. Breakeven Stock Price at Expiration

The breakeven stock price at expiration is a key metric to consider when employing a long-put strategy. It helps the investor determine the stock price at which the strategy would start to become profitable. By calculating the breakeven point, the investor evaluates whether the expected stock price movement is likely to exceed this threshold and make the long put trade worthwhile. There are several reasons why carefully analyzing the breakeven stock price is an important part of executing a long-put strategy effectively.

Firstly, the breakeven stock price helps establish reasonable profit expectations. A long put profits when the underlying stock falls below the strike price by an amount greater than the premium paid for the put. The breakeven point is the strike price minus the premium. So, for any stock price below this level, the long put position will be in the money and start generating profits. By understanding the breakeven point, the investor gets a clearer sense of the minimum price move needed in the anticipated downward direction to reach the breakeven level and then profits beyond it. Setting achievable profit expectations is key to evaluating the attractiveness of the long-put trade.

Secondly, the breakeven stock price forms a useful comparison point against price targets and technical analysis. Experienced options traders will complement the break-even analysis with price targets based on technical indicators, support levels, and trend lines. By overlaying the breakeven point on the chart, the trader visualizes how far the projected price target is relative to the breakeven level. This provides better context for judging the feasibility of the price target and whether the expected downward move is large enough relative to the breakeven point to warrant placing the long put trade.

Thirdly, the breakeven analysis guides appropriate strike price selection. Choosing the optimal strike price is crucial for a long-put strategy. A strike too close to the current stock price requires a larger downward move to reach profitability. A strike too far from the current levels makes the options premium too expensive and the breakeven point harder to reach. By modelling breakeven points at various strike prices, the trader identifies the ideal strike that balances the affordability of premium with a realistically achievable breakeven stock price.

Fourthly, the breakeven point helps assess the risk-reward payoff of the long-put trade. The spread between the break-even level and the strike price represents the maximum payout possible if the stock expires at zero. This spread minus the premium paid equals the potential reward of the trade. The trader compares this potential payoff versus the risk of loss if the stock fails to breach the breakeven point by expiration. Evaluating this risk-reward ratio is essential for prudent position sizing and money management.

Finally, tracking the underlying stock price versus the breakeven point guides early exit decisions. As expiration approaches, the trader may consider exiting the long put position early if the stock remains stubbornly above the breakeven level. The breakeven analysis provides an objective reference point for assessing whether to stick with the position or cut losses based on the expected probability of still reaching profitability.

10. Discussion of Strategy

Employing options strategies requires careful planning and analysis. For a long put strategy, the investor should thoughtfully consider the approach before deploying the trade in their portfolio. Evaluating and discussing the strategy beforehand allows the trader to weigh all elements of the position and ensure it aligns with their goals and risk tolerance. There are several aspects of the long-term strategy that warrant deliberation.

The investor should clearly define their thesis and motivation for the trade. Are they bearish on the stock for fundamental reasons, or do they expect a short-term pullback based on technical factors? Do they want downside protection for an existing long stock position? By outlining the rationale and objectives, the trader determines if a long put properly aligns with their viewpoint and aims for the trade.

Consideration should be given to appropriate expiration selection. Longer-dated puts allow more time for the stock to decline but have higher premium costs. Short-term puts are cheaper but require a quicker stock move to profit. Expiration selection depends on the investor’s time horizon, conviction level, and risk tolerance. Discussing preferences here will guide suitable expiration picks.

The trader should contemplate their appetite for leverage and risk versus potential reward. Long puts when buying single contracts provide leveraged exposure with capped risk. However, losing the full premium paid is possible if the stock remains flat or rises. The investor should ensure the defined risk-reward payoff aligns with their capital limitations and loss willingness.

Realistic risk management rules should be predefined through self-discussion and reflection. Stop loss triggers, position sizing limits, and early unwind conditions should be strategized before entry. Conservative risk guardrails will help avoid emotional decisions and oversized bets.

The long-put strategy merits consideration of optimal strike price selection. Too aggressive of a strike risks the loss of full premium if unreached. Too conservative of a strike reduces potential profits. Strike selection should balance the probability of reaching the profitable zone with affordable premium payments.

Factors like implied volatility and timing of earnings announcements should be contemplated to maximize the position’s outlook. Higher implied volatility raises premium values, benefiting long-put holders. Avoiding trades into upcoming binary events like earnings reduces the likelihood of unexpected adverse moves.

The investor should consider how to incorporate long puts within the context of their broader portfolio. Puts hedge long stock positions or provides a means to gain short exposure in an otherwise long-only account. Planning proper portfolio integration is key.

Tax implications may warrant discussion for long puts executed in taxable accounts. Contract gains held over one year get preferential long-term capital gains tax treatment versus short-term treatment for shares held under a year.

The exit plan merits deliberation before entry. Defined unwinds at target profit thresholds or stop loss levels avoid emotional exits. Rollover conditions to continue the position should also be predetermined.

When should you sell a Long Put?

It is ideal to sell the underlying stock price rises above the breakeven point. Since the long put profits when the stock falls below the strike price, if the stock rises above the put’s breakeven (strike minus premium), the option is unlikely to be profitable. The put has lost most or all of its value, so selling to close the position and salvaging any remaining premium would be prudent.

Third, significant time value premium erodes as expiration approaches. If the long put is not in the money as expiration nears, its value will decay rapidly due to time value erosion. Selling the put while the premium remains recoups some of the investment rather than letting the option expire worthless.

Fourth, implied volatility declines substantially. Higher implied volatility inflates put premiums. So, a sharp drop in IV hurt long-put valuations. Selling to close the position when you still get a reasonable premium price is often the best move when an IV collapses.

Finally, the stock stabilizes or reverses higher against the trade thesis. If the stock stops falling as expected or starts rallying higher, the premise for holding the long put dissipates. Taking the loss and selling the put avoids further losses if the stock keeps moving the wrong way.

The optimal times to sell a long put are when it hits your profit target, if the stock blows through upside breakeven, if time decay accelerates near expiration if IV drops markedly, or if the stock price action negates the bearish rationale for the trade. Cutting losses or securing gains promptly is key to long-term success.

Is a Long Put strategy profitable?

Yes, a long put strategy is profitable if used properly and under the right market conditions, however, the potential profit is limited to the strike price minus premium paid which is realized if the stock falls below the strike at expiration, and key factors that determine profitability are how much the stock price declines as the more the underlying drops below strike the greater the intrinsic value, declining implied volatility since higher IV inflates put premiums, time decay as the put loses value as expiration approaches, and strike price selection since strikes too far OTM require bigger stock declines to profit while strikes too close ITM have expensive premiums.

In summary, long puts are profitable if the trader selects an optimal strike price, times entry and exit well based on volatility and time decay factors, and the underlying stock drops below the strike price by more than the premium paid before expiration but if not executed properly or the stock fails to decline as expected, the puts may expire worthless and lose the full premium amount.

How to calculate Long Put payoff?

The long-put payoff at expiration is

Max(Strike price – Asset price at expiration + Premium, -Premium)

Where the maximum payoff is capped at the strike price less the premium paid. Here is an instructional guide to calculating the payoff for a long-put option position.

Identify the strike price of the long put option. This is the price at which the putholder has the right to sell the underlying asset. Let’s denote the strike price as Rs—50 for this example.

Note the premium paid to purchase the long put. For example, if the put premium is Rs. 5, this is the maximum amount that is lost on the trade.

Calculate the breakeven point. This is the strike price minus the premium paid. In this case, breakeven point = Rs. 50 – Rs. 5 = Rs. 45.

The payoff depends on where the asset price ends up at expiration. The long put expires worthless when the asset price exceeds the strike price at expiration, resulting in a payoff of -Rs. 5, the premium paid.

What are the advantages of Long Put?

There are six main advantages of long put. Below is a detailed description.

1. Provides leveraged profit potential with limited risk

Buying long puts allows traders to benefit from a bearish move in the underlying asset with a smaller capital outlay compared to shorting the stock. Maximum loss is limited to the premium paid for the option, while the profit potential is unlimited up to the strike price if the stock falls to zero. The built-in leverage allows for outsized percentage returns compared to the initial investment.

2. Flexible risk management through strike price selection

Traders customize the breakeven level and margin of safety by choosing an appropriate strike price relative to the current stock price. Lower strike prices have higher premium costs but provide a wider buffer from current levels. Higher strikes have lower premiums but require a larger adverse move in the stock. Strike selection allows managing profit potential versus loss risk.

3. Hedges downside risk in a portfolio

Long puts help hedge against potential declines in long stock positions or an overall portfolio. Puts effectively cap the maximum loss if the underlying stock falls. Hedging helps mitigate unsystematic risk events impacting single positions.

4. Allows expressing a bearish view with defined risk

A long put provides an avenue to speculate on or hedge against a bearish outlook without shorting stocks. The maximum loss is known upfront, enabling appropriate capital allocation and risk planning. Puts allow benefiting from declining prices with lower complexity than short positions.

5. Potential to profit from high implied volatility

An increase in implied volatility raises extrinsic value and the price of put options. Traders benefit from volatility spikes if they are holding long puts. IV expansion provides an additional tailwind alongside the underlying bearish move.

6. Gains from timing volatility cycles

Implied volatility tends to expand, leading to earnings announcements and other catalyst events. Well-timed long puts before volatility spikes capture increased premium valuation. Traders aim to monetize rich premiums by selling puts as IV means reverts lower post-events.

The leveraged payoff profile, flexibility in managing risk, hedging capabilities, tax benefits, margin efficiencies, and speculation potential make Long Puts an attractive instrument under the right circumstances and aligned with appropriate strategies.

What are the disadvantages of Long Put?

The main disadvantages of a long put strategy include the limitations on profit potential, time decay, capital requirements, and difficulty in timing entry and exit points are the main drawbacks to a long put strategy.

Limited Profit Potential

The profit potential on long puts is limited to the difference between the strike price and zero if the stock price falls to zero. Unlike a short position that has unlimited profit potential as the stock falls, long puts have a defined maximum profit. Traders cannot fully capitalize on a sharp decline in the stock price with long puts.

Time Decay

Time decay, or theta, works against the value of long puts over time. As the approach expires, the time premium built into the option price declines. Time decay accelerates in the last 30-60 days until expiration. Traders need the stock to make a significant move lower to offset time decay. Sitting idle with long puts as expiration approaches usually results in losses.

Upfront Capital Required

Buying options requires an upfront capital outlay. The trader has to pay the premium to purchase the puts. This ties up capital that could be used for other opportunities. The amount paid for the puts also represents the maximum loss if the trade does not work out. Unlike a short position with defined risk, long puts require guessing how much to pay for downside protection. Paying too much for puts creates unnecessary losses.

Lack of Leverage

There is no leverage or borrowing with a straight, long-put purchase. The trader can only control up shares as they have capital. With a short put or call option, leverage arises from the ability to control 100 shares per contract without the capital to purchase those shares. Long puts only provide leverage if paired with other strategies like a long stock position in a married put.

Assignment Risk

For long puts that end up in the money, the trader retains the puts through expiration. The put seller, upon exercising, takes on the obligation to buy the stock from the trader at the strike price. The absence of assignment risk is a notable advantage over short options strategies. However, it also means traders forego potential extra income from early assignment on short puts. Traders must hold long puts until expiration to capture their full value.

Implied Volatility Changes

A decline in implied volatility negatively impacts long puts. Implied volatility represents the demand premium priced into options. Lower demand leads to lower prices for long puts. Falling implied volatility devalues long puts, even when the trader correctly predicts the market direction. Predicting and modelling changes in implied volatility presents a greater challenge than doing so for changes in stock prices.

Opportunity Cost

The premium spent on long-put options could be used elsewhere. Buying options have a high opportunity cost compared to taking no action or using the capital for other strategies. Traders have to account for the time value lost while waiting for the puts to become profitable. The opportunity cost is especially apparent if the trader was wrong on market direction and the puts expire worthless.

Difficulty Timing the Market Peak

To maximize profits on a long put, traders want to purchase the puts as close to the peak in the underlying stock price as possible. However, no one predicts the exact peak. Buying puts too early means more time decay working against the position. Buying puts too late reduces the potential profit if the stock continues moving higher after the purchase. Timing the market peak when buying long puts is challenging.

Lack of Dividends

Traders have to compensate the lender of the shares for any dividends paid while short. With long puts, the trader misses out on earning dividends while waiting for the stock to decline. For dividend-paying stocks, some income is forfeited by using long puts compared to other bearish strategies. The lost dividends are an indirect cost of long puts.

Weighing the disadvantages against the benefits of downside protection and increased leverage helps traders decide when long-term puts fit their goals and risk tolerance. As with most trading strategies, long puts come with certain tradeoffs compared to alternatives like short puts, spreads, or being outright long or short the stock.

What is an example of a Long Put?

Let us look at an example of a long put. Ramesh believes prices of Tata Motors shares are due for a fall in the coming weeks. Tata Motors stock is trading at ₹430. To profit from the expected decline, Ramesh buys 10 put option contracts on Tata Motors with a strike price of ₹400 expiring in 45 days.

Ramesh pays a premium of ₹12 per share for the puts, so for 10 contracts of 100 shares each, the total outlay is ₹12,000 (₹12 x 100 x 10). The put options give Ramesh the right to sell Tata Motors shares at ₹400 on expiration day.

Over the next month, Tata Motors’ stock fell to ₹380 due to weaker-than-expected car sales. As the share price declines, the value of Ramesh’s puts increases. With 15 days left until expiration, the ₹400 puts are now trading at a premium of ₹22.

Ramesh decides to close out his long-put position by selling his 10 contracts to lock in his profits. He sells the puts for ₹22, receiving ₹22,000 total (₹22 x 100 x 10). After factoring in the initial cost of ₹12,000, Ramesh nets a profit of ₹10,000 on the long put trade.

This example highlights the advantages and disadvantages of a long put strategy. Ramesh had limited risk, as his maximum loss was the premium paid upfront for the options. However, his profit was also capped at the difference between the strike price and zero.

Ramesh avoided time decay by closing out the position with 15 days remaining rather than holding to expiration. He successfully benefited from the decline in Tata Motors’ share price using long puts. However, timing the entry and exit was crucial to maximizing his profits on the trade.

Is Long Put the same as Short (Naked) Call?

No, a Long Put and a Short Naked Call are not the same. A Long Put involves buying puts to profit from a decline in the stock price, while a Short Naked Call involves selling uncovered calls to profit from neutral or downward movement in the stock with unlimited downside risk.

What is the difference between Long Put and Long Call?

The main difference between a long put and a long call is the market expectation and the rights conferred to the holder. A long put option grants the holder the right to sell an asset at a specific price within a specified period, and investors typically utilize this when they predict a decrease in the asset’s value.

Conversely, a long call option confers the right to buy an asset at a specific price within a set timeframe, used by investors when they anticipate an increase in the asset’s value.

What is the difference between Long Put and Short Put?

The main difference between a long put and a short put lies in the position the investor takes and the market expectation. A long put option grants the investor the right to sell an asset at a specific price within a certain timeframe, typically used when expecting the asset’s value to decline.

In contrast, a short put option involves the investor selling or “writing” the put option, which obligates them to buy the asset at the strike price if the option is exercised. Investors use short puts when they believe the asset’s price will remain stable or increase, as they profit from the premium received without needing to purchase the asset.

Previous Article

Previous Article

37")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 40")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 41")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 42")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 46")

No Comments Yet.