Vega is a measure of an option’s sensitivity to changes in volatility. Vega represents how much an option’s price will change, all else being equal, for a 1% change in the underlying asset’s volatility. Understanding vega is important because it impacts an option’s pricing and helps determine suitable trading strategies.

A higher vega indicates an option’s price will move more on volatility swings. Options with further expiration dates tend to have higher vegas since volatility plays a larger role in pricing the longer the contract. Volatility also tends to be priced higher for further dated options, making Vega more influential.

Vega is beneficial for traders to analyze. Strategies like long straddles and strangles profit when volatility increases due to their positive Vega. Short vega positions like covered calls are favorable in low-volatility environments. Around important news releases and earnings dates, volatility usually spikes, benefiting long Vega plays.

However, Vega also represents an exponential decay in an option’s price as time passes and expiration nears. This makes the impact of a 1% vega change diminish over the contract’s life. Vega changes also don’t factor in delta, which determines how an option moves with the underlying price changes. While Vega provides useful insights, it must be considered alongside other Greeks for a fuller picture.

What is Vega in Options Trading?

Vega is a measure of the sensitivity of an option’s price to changes in the underlying asset’s volatility. Specifically, Vega indicates how much an option’s price is expected to change given a 1% change in the implied volatility of the underlying asset.

Vega is one of the “Greeks” used in options pricing models like Black-Scholes. The Greeks refer to different sensitivities that affect an option’s price. While metrics like delta indicate sensitivity to the price of the underlying, and theta indicates sensitivity to time decay, Vega specifically measures sensitivity to volatility.

Volatility represents the degree of variation in trading prices of the underlying asset over time. Historical volatility looks back at actual past price changes, while implied volatility is what is suggested by the current pricing of options on the asset. Implied volatility changes with supply and demand for options, reflecting market expectations of future volatility.

Vega describes the extent to which an increase or decrease in the implied volatility of the underlying asset will impact the theoretical fair value of an option. For both calls and puts, Vega is positive – meaning higher implied volatility raises the value, while lower volatility decreases it. This is because higher volatility implies a greater range of potential outcomes for the underlying asset price, increasing the chances the option will expire in the money.

The Vega of an option indicates the amount its price is projected to change for a 1% change in implied volatility. For example, an option with a vega of 0.10 would be expected to increase in value by Rs. 0.10 if implied volatility rises by 1%. The Vega will always be expressed in dollar terms.

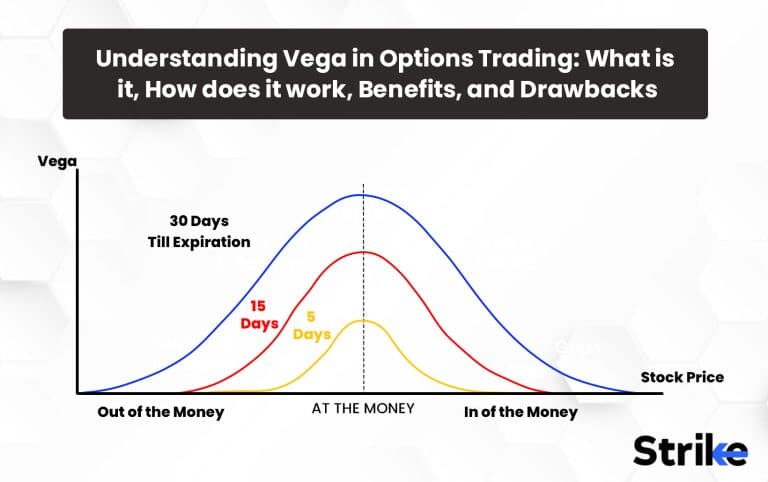

Typically, Vega decreases as an option heads toward expiration. This is because there is less time remaining for volatility to potentially impact the final settlement price. Longer-dated options, therefore, tend to have higher Vega than those expiring very soon.

At-the-money options also tend to have the highest Vega, as they stand the most to gain or lose from volatility changes. In-the-money and deep out-of-the-money options will have lower Vega since volatility changes matter less when intrinsic or extrinsic value dominates.

Vega helps options traders evaluate trades and manage risks. For buyers, higher Vega represents potential upside if volatility rises but also downside if it declines. Sellers see the opposite payoff profile. Monitoring vega exposure allows traders to size positions appropriately given their volatility outlook.

Vega also indicates how the time value is likely to decay for an option. As there is less time premium remaining, Vega decreases as volatility decreases. Traders use current vega values versus historical volatility levels to estimate time decay patterns.

While delta hedging focuses on offsetting price exposure, traders utilize Vega hedging to reduce directional volatility risks. Investors holding long stock positions often buy puts to protect against volatility spikes. The Vega of the put bet offsets the Vega exposure of the underlying shares.

Monitoring vega alongside other Greeks allows for constructing positions with a fuller understanding of the varying risks and potential outcomes.

Why is Vega important in Options Trading?

It is important for options traders to understand Vega because it measures how sensitive an option’s price is to changes in the underlying asset’s implied volatility. While other Greeks, like delta and theta, are undoubtedly important, Vega provides unique insights into how volatility exposure will impact option pricing and profits.

At its core, Vega indicates how an option’s price sometimes responds to changes in the volatility of the underlying asset. Monitoring vega is crucial precisely because volatility fluctuates dynamically, especially around major events or announcements that stir investor uncertainty. Options with higher Vega will see values rise if volatility increases, potentially boosting profits. But those values just as easily fall if volatility declines.

Traders considering an options position must weigh the Vega against their own volatility forecast to judge attractiveness. For volatility-focused strategies like straddles or strangles, high Vega is desirable to maximize the upside if volatility rises. For other trades where directional bets matter more, lower Vega is preferable. In all cases, Vega indicates the degree of exposure to volatility swings in either direction.

Beyond assessing new positions, Vega plays a vital role in actively managing open options trades. Just as delta exposure is adjusted using hedging strategies, Vega likewise is balanced through trades specifically targeted at offsetting volatility exposure. For example, selling options with opposing Vega effectively locks in time value at current volatility levels. Monitoring vega helps fine-tune hedges to maintain risk tolerances.

Vega also sheds light on how time decay will impact an option as expiration approaches. As implied volatility decreases, so does Vega, indicating a reduction in the expectation that volatility will affect the closing price. Traders use vega trends to estimate time premium erosion over the option’s remaining life. In order to avoid significant time value losses, this helps determine when to exit positions.

In some options strategies like straddles, Vega is actually the primary metric rather than delta or theta theta. A long straddle profits when volatility rises, so traders need to assess whether Vega is sufficient relative to the position size. Large Vega indicates substantial upside from volatility expansion. The focus is more on Vega than the directional risk.

How does Vega in Options Trading work?

Vega works in Options Trading by measuring how an option’s theoretical value changes in response to changes in the underlying asset’s implied volatility. Vega indicates the estimated price change for a 1% change in volatility, quantifying the option’s sensitivity to volatility fluctuations.

Vega stems from options pricing models like Black-Scholes that estimate fair value based on various inputs. One of the core inputs is implied volatility – the level of volatility priced into options by supply and demand. Increased implied volatility increases the likelihood of more significant price swings, which increases the likelihood that an option will expire in the money.

As implied volatility rises, the pricing models adjust the fair value higher for both calls and puts to account for the greater price swing potential. Likewise, decreasing volatility lowers the projected price range and reduces option values. Vega quantifies the amount of change in the option price per 1% shift in implied volatility.

For example, say an option has a vega of 0.12. This means the model estimates the option’s value will increase by Rs. 0.12 if implied volatility rises by 1%. Conversely, the value would decrease by Rs. 0.12 if implied volatility dropped 1%. So, Vega captures the option’s theoretical sensitivity to volatility changes.

It is important to note Vega is always positive for both calls and puts because higher volatility universally increases the probability of larger underlying price moves in either direction. While calls and puts have differing delta exposure, they exhibit symmetrical vega exposure.

Typically, at-the-money options exhibit the highest Vega since they stand to benefit most from volatility-driven price swings in either direction. In-the-money and deep out-of-the-money options have lower Vega as intrinsic or extrinsic value dominates. Longer-dated options also tend to have higher Vega than those expiring very soon, as there is more time for volatility to materialize.

Vega is stated in dollar terms rather than percentage because it represents the tangible impact on option value from the percentage volatility change. Monitoring an option’s Vega informs traders on how sensitive the position is to shifting volatility expectations.

Active options traders utilize vega hedging strategies to offset vega risk by shorting or buying options with opposing exposures. For example, selling an option contract with a similar Vega effectively locks in volatility exposure. Traders isolate other Greek risks, such as delta or theta, by using hedging.

How do Vega Greek options compare to other types of Option Greeks?

Unlike delta and gamma, which measure an option’s sensitivity to changes in the underlying asset’s price, Vega specifically measures an option’s sensitivity to changes in the implied volatility of the underlying asset.

Delta indicates how much an option’s price changes given an Rs. 1 movement in the underlying asset price. Calls have a positive delta, and puts have a negative delta. It reflects directional exposure.

Vega does not provide directional insights but rather quantifies sensitivity to implied volatility. All else equal, Vega is positively correlated with the price for both calls and puts. An option’s exposure to price fluctuations relative to volatility fluctuations is seen by comparing delta and Vega.

Gamma measures how delta changes given price movements. Options with higher gamma see delta shift more rapidly as the underlying asset fluctuates up and down.

Vega quantifies how much an option’s price changes given a 1% volatility shift, not accounting for delta changes. Gamma provides insights on changing delta, whereas Vega isolates volatility sensitivity.

Theta indicates how much an option’s price is estimated to decay each day as it heads toward expiration due to time value erosion.

While thetatheta focuses strictly on time decay, Vega measures sensitivity to volatility which influences time value. As volatility drops, Vega decreases, reflecting a decreasing time premium.

Rho calculates expected price change given a 1% shift in the risk-free interest rate. Underlying moves impact carry costs associated with options trades.

Vega strictly focuses on volatility shifts, not interest rates. Comparing rho and Vega shows sensitivities to macro environment factors versus underlying asset assumptions specifically.

Vega provides additional, complementary insights isolating sensitivity to volatility changes. As volatility fluctuates constantly, sizing positions using Vega while hedging volatility exposure is crucial for options traders. Evaluating Vega alongside other Greeks results in a more comprehensive risk assessment.

How does Vega impact the Option prices?

Vega impacts option prices by determining how much the price will change based on changes in implied volatility – the higher the Vega, the more impact volatility changes will have on the option price.

Vega directly influences the theoretical fair value of an option as estimated by pricing models like Black-Scholes. Specifically, Vega indicates how much an option’s price is expected to move, given a 1% change in the implied volatility of the underlying asset.

Higher implied volatility indicates greater expected price variation of the underlying asset over the option’s life. For both calls and puts, higher volatility raises the probabilities of larger price swings that could cause the option to finish in the money at expiration.

Given higher implied volatility, pricing models adjust their fair value estimate upward to account for the increased probability of positive payoff. The models incorporate volatility levels into their pricing formulas, so projected price range expansion translates to higher theoretical value.

On the other hand, as the underlying is anticipated to fluctuate less, the projected price ranges contract if implied volatility decreases. This lowers the probability of outsized price swings that would bring substantial profits. With lower volatility, pricing models reduce their fair value estimates.

The degree of price change in response to a 1% volatility movement is quantified by the option’s Vega. Higher Vega means the option value is projected to increase more for a given volatility uptick. Lower Vega means the price is less responsive to volatility shifts in either direction.

Longer-dated options have higher Vega since volatility has more time to impact the ending price potentially. At-the-money options also tend to have the highest Vega. Time value is most significantly impacted by volatility the closer the strike is to the current price.

Monitoring current implied volatility versus historical levels provides context on expected pricing impacts. The volatility index (Vega) shows how much more premium could be priced into the option if the volatility means returns to a higher level if implied volatility trades significantly below historical norms.

What are the factors that influence Vega?

The main factors that influence Vega are the time to expiration, implied volatility, strike price relative to underlying price, and option type (calls vs puts).

1.Time to Expiration

The time remaining until an option expires is a major determinant of Vega. Options with a longer time to maturity will have higher Vega. This is because there is more time for volatility to potentially rise or fall before the option expires, which would impact the option’s value. Vega decreases as an option approaches expiration. At expiration, an option’s Vega drops to zero because changes in volatility no longer affect the price of an expiring option. Therefore, longer-dated options tend to have higher Vega than shorter-dated options.

2. Strike Price

An option’s strike price relative to the current price of the underlying asset also affects Vega. For at-the-money options, where the strike price equals the current market price, Vega reaches its maximum level. As options move further out-of-the-money or into-the-money, their Vega decreases. This is because deep-in-the-money and deep out-of-the-money options behave more like the underlying asset, becoming less sensitive to volatility. But at-the-money options with strike prices near the current trading price of the underlying asset have the most exposure to volatility.

3. Implied Volatility Level

Vega tends to be higher when implied volatility is low and lower when implied volatility is high. This asymmetry exists because volatility cannot fall below zero but potentially rises without limit. There is less upside potential for implied volatility to rise when it is already high. However, implied volatility has greater room to rise when it is depressed. Therefore, Vega diminishes at very high levels of implied volatility.

4. Option Type

Calls typically have higher Vega than puts. This is because calls become more valuable as volatility rises, whereas puts become less valuable. Increased volatility implies greater upside movement potential, which benefits call options. Put options fare better with reduced volatility, implying limited upside for the underlying asset. Additionally, the asymmetric nature of returns for calls versus puts makes call options more responsive to changes in volatility.

5. Interactions with Other Greeks

While Vega specifically measures an option’s sensitivity to volatility, it does not exist in isolation. Vega interacts with other option Greeks and shifts as other variables change.

Vega and delta often move in opposite directions. As an option becomes deeper in the money, its delta rises while its Vega falls. Conversely, a falling delta typically corresponds with increasing Vega for out-of-the-money options.

Time decay measured by theta theta reduces an option’s time value premium. As expiration approaches, theta theta accelerates while Vega declines. Longer-dated options have higher Vega but lower theta. The influence of time decay increases as options near expiration.

Higher interest rates tend to increase call option prices and decrease put prices. Since calls have higher Vega than puts, an increase in interest rates should correspond to an increase in an option’s overall Vega.

Accelerating delta changes near the strike price result in higher gamma. But higher gamma also indicates lower Vega because gamma peaks for at-the-money options while Vega is maximized slightly out-of-the-money.

Vega interacts with other Greeks, often moving inversely to delta, theta, and gamma while positively correlating with rho. An option trader should be aware of the variables influencing Vega in order to understand and manage an option position’s exposure to volatility.

What is a positive Vega?

Vega is positive when an increase in the implied volatility of the underlying asset increases the price of the option. A positive Vega means the option price is expected to move higher if implied volatility rises. Vega indicates the rate of change in an option’s value relative to a 1% change in volatility. The potential for upside from volatility expansion leads to a positive Vega.

Longer-dated options generally have higher Vega than short-term options. There is greater uncertainty over a longer time horizon, so an increase in volatility has a bigger impact on options with more time until expiry. The most sensitive options are those with 3-9 months until expiration. Short-dated options have minimal time value remaining, so changes in volatility do not impact the price much. Longer expiries allow rising volatility to have a greater positive effect.

At-the-money options, with strike prices closest to the current trading price of the underlying asset, have the highest Vega values. As options move further in-the-money or out-of-the-money, their Vega starts declining. Maximum Vega occurs when the delta is around 50. This pins the strike price very close to the market price, maximizing sensitivity to volatility. Deeply out-of-the-money and deep-in-the-money options have limited volatility exposure. But strike prices positioned close to current levels allow Vega to become positive.

Vega is higher when implied volatility levels are lower. Volatility cannot drop below zero, but the upside potential has no limit. There is less space for volatility to rise when it is already high. However, any increase significantly benefits longer-dated at-the-money options when volatility is low. The Vega for these options will be positive, reflecting potential gains if volatility reverts higher from oversold lows.

Call options typically display higher Vega values than puts. Upside volatility benefits call options, whereas downside volatility benefits put options. The asymmetric return profile causes calls to be more responsive to volatility changes. Deep out-of-the-money calls still have positive Vega due to unlimited upside if volatility spikes. The positive Vega signals such calls will rise in value if volatility increases.

Options traders deliberately structure positions with positive Vega by selecting longer-dated at-the-money calls when implied volatility is expected to rise. For example, purchasing call options on the S&P 500 index with 6 months until expiration and strike prices close to the current index level will create positive Vega exposure. As volatility rises, the value of these calls would be expected to increase, generating profits for the options trader.

Holding long option positions also hedge a portfolio against volatility risk. For example, an equity portfolio could buy put options on the index to help buffer against market declines. The put options will have positive Vega, adding value for the hedge as volatility increases during a falling market. Managing overall portfolio Vega helps smooth returns and mitigate volatility risk.

The convexity of options makes Vega asymmetric so that it is always positive. Time and strike price are the primary factors creating positive Vega. Long-dated at-the-money call options usually exhibit the highest positive Vega sensitivity to volatility. Traders utilize positive Vega to benefit from potential increases in volatility or to hedge portfolios by offsetting short Vega positions in other assets.

How common for Vega to be negative?

No, it is very uncommon for Vega to be negative for most standard options contracts. Vega represents the change in an option’s price due to a 1% change in implied volatility. Since higher volatility typically increases the value of an option, Vega is almost always positive. The convex nature of options payoffs means higher volatility boosts the value of both calls and puts. It is rare to see negative Vega in normal market conditions.

However, there are four exotic option structures where negative Vega occurs more regularly.

Iron Condors options strategy involves selling an out-of-the-money put and call while also buying further out-of-the-money puts and calls to create a range-bound position. The short options have positive Vega, while the long options have minimal Vega. Vega for the structure is negative if the short options outweigh the long ones.

Ratio Spreads involve selling more options contracts than are purchased. For example, selling 2 calls and buying 1 call. The excess short options result in negative Vega overall. This position benefits if volatility declines.

Instruments that track volatility indices like the VIX will display inverted Vega. Lower VIX levels increase the value of VIX calls and decrease VIX puts. So VIX options have negative Vega, indicating they gain value as volatility drops.

Options on futures like commodity and currency contracts more regularly have negative Vega. This is because futures options derive value primarily from interest rate differentials rather than volatility.

What is considered a high Vega option?

A high Vega option is one that has a Vega of 0.10 or higher. The key factors driving higher Vega include longer time to expiration, at-the-money strike prices, and lower levels of implied volatility.

Longer-dated options have higher Vega since there is more time for volatility to potentially change before expiration. Options expiring within 1-2 months will have a relatively low Vega around 0.02. But options expiring in over 6 months have Vega above 0.15. The upside from a volatility spike has a greater impact the longer the option lifetime. So longer expiries carry higher Vega.

At-the-money options with strike prices closest to the current trading level of the underlying asset have the highest Vega. Maximum Vega occurs when the delta is around 50, meaning the strike price is near the market price. Out-of-the-money and deep-in-the-money options have lower Vega below 0.05 as they behave more like the underlying with less volatility exposure. But strike prices positioned close to the money have greater upside from volatility, boosting Vega.

Vega tends to peak when implied volatility is low. Elevated volatility dampens upside potential, lowering Vega. However, options are more susceptible to future increases when volatility is low. Therefore, options maintain higher Vega when implied volatility starts under 20% compared to Vega declining sharply above 40% volatility.

Calls tend to exhibit higher Vega than puts. Upside volatility benefits call more, while puts benefit from downside volatility. The asymmetry means calls have greater sensitivity and higher Vega values.

High Vega is advantageous for trades that benefit from rising volatility. For example, a long call option position has positive theta theta, so higher volatility would increase the option’s value. High Vega also provides volatility insulation for hedged portfolios.

But high Vega also comes with risks. There can occasionally be a significant drop in value for high-volatility options. Traders sometimes need to defend against volatility spikes and skew by managing Vega. Sudden drops in implied volatility hurt long options with elevated Vega.

How does Vega behave under different market scenarios?

Under different market scenarios, Vega increases when implied volatility is high and decreases when implied volatility is low.

Periods of elevated market volatility cause a rise in the implied volatility of options. This benefits options with positive Vega, as higher implied volatility increases the value of these options. Long calls and puts positions with high positive Vega will appreciate during spikes in actual and implied volatility. Their value gets a boost from the heightened volatility. However, high Vega also comes with the risk of loss if volatility reverts lower in the future. Traders should consider locking in profits on large Vega gains by closing out positions when volatility peaks. Or they sometimes look to neutralize the high Vega by trading lower Vega options.

Options typically show higher Vega values when implied volatility is low across the entire options market. Because there is more potential for gain, Vega is most advantageous when volatility is near the lower end of its historical range. In low volatility environments, long option positions are constructed to take advantage of mean reversion higher. Buying medium-term at-the-money options provides positive convexity to benefit from an increase in volatility. However, traders need to actively manage the positions if the low volatility persists, as the long options will steadily decay in value over time.

Shifts in investor sentiment impact volatility patterns. For example, a decline in bullish sentiment increases downside volatility. In this case, the Vega for put options is likely to rise while the call option Vega decreases. Put options become more responsive to volatility changes. Traders adopt by trading higher Vega puts to benefit from downside volatility expansion while reducing long call exposure. Call option Vega is anticipated to rise as upside volatility resumes when sentiment improves. Rotation between calls and puts allows traders to remain nimble.

Traders evolve options strategies by managing Vega exposure relative to changing volatility conditions. Trade longer-dated at-the-money options to increase Vega when volatility looks low with upside potential. Close high Vega options to lower Vega if volatility appears to be elevated with a risk of downside. Rotate strike prices closer to or further from the money to adjust Vega when volatility is rising or falling. Favor put options when downside volatility dominates and rotate to calls when upside volatility prevails. Manage time decay by closing or rolling options approaching expiration to maintain the desired Vega profile since longer-dated options have higher Vega.

What is the most effective way to use Vega options?

The most effective way to utilize Vega is to increase long exposure when volatility is expected to rise and decrease or hedge Vega when volatility is expected to fall.

Vega provides a precise measure of how much an option will gain or lose based on movement in implied volatility. Traders explicitly utilize Vega to implement volatility directional and arbitrage strategies. Going long options with positive Vega profits from an increase in volatility, while short options or spreads benefit from declining volatility. Traders are in positions to capitalize on mispricings between actual and implied volatility.

Options directly on the VIX volatility index itself provide another instrument for trading volatility. By actively managing Vega, traders implement pure volatility views and arbitrage strategies beyond just directional bets on the underlying asset. The size of the Vega exposure indicates the degree of leverage to volatility changes. Constructing trades with appropriate Vega levels is crucial for volatility strategies.

Options are incorporated in an investment portfolio to hedge against volatility risk. Holding long options positions cushions against volatility spikes. For example, buying put options on equity indexes provides downside protection in case of a market selloff. The long puts have positive Vega, gaining value from rising volatility. Portfolio managers balance Vega exposure across assets to insulate against volatility shocks.

Changes in implied volatility impact option prices independently of movements in the underlying asset. Traders neutralize other Greeks and isolate pure volatility exposure using option spreads. A long/short strangle benefits from volatility expansion in either direction while minimizing delta exposure. Legging into a delta-neutral straddle maximizes Vega while removing directional risk. Calendar spreads focus on time decay versus volatility effects. By isolating the Vega component through spreads, traders implement strategies to capitalize solely on expected changes in volatility, separate from views on the underlying asset direction.

Periods leading up to major events like earnings announcements are particularly prone to volatility spikes. Buying short-term out-of-the-money options with elevated Vega before events produces outsized returns from the rapid rise in implied volatility. Additionally, selling expensive options right before events allows benefiting from the mean reversion lower in implied volatility after the news.

Vega contributes to an option’s overall risk-reward profile. Higher Vega options have greater volatility risk but also offer enhanced leverage. Fine-tuning the position Vega based on volatility expectations and risk tolerance optimizes the trade structure.

What is the expected return on a Vega option?

The expected return on a Vega option position is directly proportional to the magnitude and direction of volatility changes, independent of the underlying price movement.

There is no predefined return simply from an option having non-zero Vega. Projected returns require making an assumption on future volatility changes.

For example, an at-the-money S&P 500 call option with a Vega of 0.10 implies the option value will increase by approximately Rs.10, given a 1% rise in the index’s implied volatility, all else equal. The actual return depends on how much-implied volatility changes over the holding period.

The magnitude and direction of volatility changes are primary drivers of Vega-based strategy returns. Larger increases in implied volatility result in greater profits for long Vega positions, while significant declines reduce returns. Traders must estimate potential volatility ranges to forecast Vega option profits. Upside and downside volatility shifts have asymmetric impacts for calls versus puts. Rising volatility boosts long call returns while declining volatility reduces profits. For long puts, increasing downside volatility raises returns.

Time decay from theta theta reduces Vega’s return potential over the option’s life. Declining time value somewhat offsets Vega’s gains even in the event of an increase in implied volatility. Longer-dated options see bigger time premium erosion effects. The interaction of delta and Vega sometimes augments or dampens net returns, depending on whether they change in alignment. Traders should model the Greeks’ combined influences to project overall profitability.

Other factors like gamma, carry costs, and rebalancing transactions also impact net results. Gamma and theta changes affect total returns along with Vega. Carry costs are relevant for future options. Maintaining consistent Vega exposure requires ongoing rebalancing and rollovers, incurring transaction fees. Incorporating all these dynamics is key to accurately estimating expected returns from Vega-based strategies.

What strategies can be employed when trading Vega options?

Traders utilize strategies like volatility spreads, delta-hedged straddles, ratio spreads, and VIX options to capitalize on opportunities from changing volatility when trading Vega options.

1.Long Calls or Puts

Buying call or put options provides positive Vega exposure to benefit from an increase in volatility. Long calls profit if upside volatility rises, while long puts benefit if downside volatility increases. The advantage is unlimited profit potential if volatility spikes. However, long options have a time decay risk if volatility declines or remains muted.

2. Short Calls or Puts

Selling calls or putting short creates negative Vega exposure. This generates income from the options premium received and profits as volatility contracts over time. The risk is uncapped losses if volatility rises sharply. Short options have negative theta decay as well, reducing value into expiration.

3. Spreads and Combinations

Using vertical or horizontal options spreads limits risks from outright long or short positions. For example, call spreads cap upside and downside risk. Diagonal call spreads allow for managing time decay. Put spreads limit downside exposure. Spread strategies isolate Vega exposure in line with volatility expectations.

4. Straddles and Strangles

Straddles combine a long call and put at the same strike price. This strategy benefits from volatility expanding in either direction. Strangles utilize an out-of-the-money call and put the leg to lower costs at the expense of capped upside. Straddle-strangle strategies offer leveraged Vega exposure.

5. Volatility Skew Trading

Volatility skews measure the difference between implied volatility for out-of-the-money puts versus calls. Traders exploit skew changes by being long options with rising skew and short options with falling skew. Imbalances in volatility skews create Vega trading opportunities.

6. VIX Options

The VIX index tracks short-term expected volatility for the S&P 500 options market. Traders take positions directly in VIX options to capitalize on changes in broad market volatility. VIX options offer precise Vega exposure to implied volatility shifts.

7. Delta Hedging

Applying delta hedging rebalances positions to maintain delta neutrality as the underlying asset price fluctuates. This isolates Vega exposure by minimizing directional risks. Delta hedging targets profiting purely from volatility changes.

8. Asset Hedging

Long options positions in negatively correlated assets provide diversification and volatility hedging. For example, long S&P 500 put options hedge a long stock portfolio from market declines. The protective puts have positive Vega to appreciate as volatility rises in a falling market.

9. Volatility Arbitrage

This involves logging into long and short options to take advantage of mispricings between current implied volatility and longer-term realized volatility forecasts. Traders aim to capture profits as implied volatility reverts toward realized trends.

Traders utilize a variety of strategic approaches ranging from simple long/short positions to sophisticated arbitrage and advanced combinations to maximize profits from implied volatility movements.

What are the benefits of trading Vega options?

Trading Vega options allow traders to potentially benefit from changes in the implied volatility of the underlying asset while also providing leverage and requiring less capital than buying the asset outright.

1.Leveraged Returns

Options offer leveraged profits from Vega relative to the required capital outlay. A small move in implied volatility generates outsized percentage returns on the initial investment. Vega indicates the asymmetric return potential, with uncapped upside, if volatility rises sharply.

2. Defined Risk

Unlike trading volatility directly, options strategies allow for defining and limiting risk parameters. Loss exposure is managed through spread positions and strike price selection. The maximum loss is fixed at the net premium paid for long option trades.

3. Volatility Isolation

Certain options strategies isolate the impact of volatility changes separate from the underlying price action. This provides pure exposure to implied volatility movements.

4. Hedging Flexibility

Options allow crafting positions to hedge risks across diverse market environments. Portfolios are protected from spikes in volatility via long options exposure. Options make volatility a tailorable hedge instrument.

5. Access to Volatility Trading

Vega provides an efficient means to trade volatility without needing to access specialized VIX products directly. Standard options incorporate an expectation of future volatility via their implied volatility levels.

6. Volatility Arbitrage

Mispricings between actual and implied volatility are captured by legging into positions to exploit mean reversion tendencies. Vega trading facilitates volatility arbitrage strategies.

7. Event Trading

Major events like earnings releases offer lucrative short-term volatility trading opportunities. Buying or selling options with elevated Vega heading into events provides a leveraged way to benefit from volatility spikes and retreats around the news.

8. Portfolio Diversification

Incorporating options with distinct return drivers related to Vega diversifies the Greeks’ risks underlying a portfolio. Vega helps balance correlation exposures.

9. Capital efficiency

Options offer capital-efficient access to implied volatility trading due to their inherent leverage. The percentage returns relative to capital allocated are potent for Vega-based strategies.

The sensitivity gauge of Vega allows direct targeting of opportunities arising from volatility shifts and mispricings in the derivatives markets. Harnessing Vega’s advantages provide alpha generation potential.

What are the drawbacks of trading Vega options?

Trading Vega options carry the risk of losing money if implied volatility decreases when you have a long vega position or if implied volatility increases when you have a short vega position, as the value of the options decreases rapidly with vega exposure.

1.Time Decay

Options have expirations and lose value over time due to time decay. Even options positions with positive Vega experience erosion due to theta theta. This time, premium decay offsets potential profits from Vega, especially if volatility remains flat.

2. Uncapped Losses

Selling options create negative Vega exposure and the obligation to buy or sell the underlying at unfavorable prices if the market moves sharply. Short options face unlimited loss if volatility surges.

3. Volatility Guesswork

Predicting short-term volatility direction is challenging. Implied volatility sometimes does not converge to longer-term realized trends. Being incorrect about volatility expectations leads to losses on Vega trades.

4. Other Greek Risks

While Vega measures sensitivity to volatility, options also have exposure to delta, gamma, theta theta, and other Greeks. Cross-effects from conflicting Greeks undermine purely Vega-driven trades.

5. Early Assignment

Holding short option positions runs the risk of early assignment if the options go deep in the money. This forces early closeouts to avoid unwanted stock positions.

6. Correlation Variability

Underlying assets shift in terms of volatility correlations. For example, gold sometimes begins tracking equity volatility. Changing correlations alter the effectiveness of volatility hedging.

7. Volatility Skews

Divergences between implied volatility for puts versus calls require managing volatility skew. Skew changes create unexpected losses on certain strike prices.

8. Liquidity Constraints

Illiquid options sometimes have very wide bid-ask spreads. This increases slippage on entering and exiting trades. Lack of volume also makes trades more difficult to execute at favorable prices.

9. Volatility Cycles

Implied volatility tends to move in long-term cycles between periods of expansion and contraction. Accounting for these cyclical swings requires actively timing entries and exits.

10. Risk Management Challenges

The asymmetric return profile makes options risky to short-sell without defined exit plans. Letting losses accumulate is damaging to long-term performance.

The leveraged nature of Vega cuts both ways depending on the direction of volatility. Controlling the downside risks associated with options is key to successfully harnessing the upsides of Vega trading.

How can traders handle the drawbacks of Vega options?

Traders manage the risks of trading Vega options by using appropriate position sizing, hedging Vega exposure, and closely monitoring changes in implied volatility.

Vega erodes quickly for shorter-dated options, so traders sometimes choose longer expiries to maintain exposure. Rolling to farther-dated contracts before excessive time decay occurs helps preserve Vega. Spread positions also define risk from time erosion.

Strategies like straddles and strangles combine call-and-put options to hedge against directional price action in the underlying. This provides purer exposure to implied volatility changes measured by Vega. Directional bets are isolated separately.

Modeling a position’s full Greek profile reveals how the Greeks offset or augment each other. Traders neutralize unwanted Greeks by legging into offsetting options contracts. Delta hedging also strips out directional exposure.

Selling options have an unlimited downside if volatility rises, so planning early exit points is key. Defined risk-reward parameters should guide closing out short options before losses accumulate.

Risks on short Vega trades are reduced by purchasing protective long options to cap the downside. Put spreads to limit losses on short-call positions. Call spreads limit risk on short-put trades. The long options cover the unlimited risk of naked shorts.

Concentrate trading on highly liquid underlying like broad indexes to avoid wide bid-ask spreads and execution difficulty. Liquid options enable efficient entering and exiting Vega-driven strategies.

Observe shifting correlations between asset volatilities and adjust hedges accordingly. Changes in historical correlations are quantified to determine optimal portfolio volatility exposures.

Compare put and call implied volatility skews to identify distortion opportunities. Changes in skew gradients over time signal mispricings to exploit.

Leverage from Vega trading requires keeping the overall position size modest relative to portfolio assets. Right-sizing prevents overexposure that could lead to excessive drawdowns.

Use hard stops, profit targets, maximum loss limits, and defined exit strategies to minimize errors and emotions. Automated risk controls are preferable for enforcing objective volatility trade management.

What are the risks associated with trading Vega options?

Trading Vega options carry risks such as potentially losing money quickly if implied volatility moves against your vega position, requiring constant monitoring of volatility changes, and the need for proper position sizing and hedging to manage vega exposure appropriately.

1. Volatility Guesswork

The largest risk is making inaccurate predictions about the direction of future volatility. Implied volatility sometimes does not converge to forecasted realized volatility. Incorrect volatility expectations lead to losses as Vega exposure works against the trader.

2. Uncapped Losses

Selling options exposes traders to uncapped losses if implied volatility rises. For example, naked short calls face unlimited risk if the underlying rallies sharply. Short options have negative Vega, so volatility spikes result in outsized mark-to-market losses.

3. Time Decay

All options lose value over time due to declining time premium. Time decay from theta theta works against the positive Vega in long options. Time erosion reduces ROI even in cases where volatility increases by offsetting potential Vega gains.

4. Directional Exposure

Changes in the price of the underlying affect options through delta sensitivity. Directional moves counter to the trader’s view on volatility introduce P&L uncertainty. The asset price impact needs to be isolated from Vega.

5. Early Assignment

Holding short option positions leaves traders vulnerable to the early assignment if options move deep in the money. This sometimes forces the unwanted receipt/delivery of shares, requiring costly liquidation.

6. Greek Imbalances

Options have multiple Greeks beyond simply Vega. Cross-effects from gamma, theta theta, and other Greeks undermine purely volatility-driven strategies. Conflicting risks need to be neutralized.

7. Volatility Skew Changes

Shifts in the implied volatility skew between puts and calls affect the pricing along different strike prices. Skew changes challenge volatility assumptions for specific contracts.

8. Correlation Variability

Underlying price correlations are unstable. For example, falling equity-volatility correlations reduce the effectiveness of hedges. Changing correlations alter the reliability of Vega trading.

9. Liquidity Constraints

Thinly-traded options have very wide bid-ask spreads and reduced pricing transparency. Illiquid options are more difficult to leg into complex strategies and exit positions efficiently.

10. Event Risks

Major events like earnings announcements or economic data spark directional volatility spikes. Event-driven moves to introduce binary risks separate from sustainable volatility trends.

11. Portfolio Overexposure

The leveraged nature of options requires modest position sizing. Excessive Vega exposure relative to portfolio assets risks oversized drawdowns from volatility swings.

From volatility forecasting challenges to managing Greece’s balance to position sizing guidelines, traders must implement robust risk management practices tailored to the intricacies of volatility-driven options strategies.

How can traders manage Vega risks?

Traders manage Vega risks by using hedging strategies, diversifying their Vega exposure across multiple options, closely monitoring implied volatility and adjusting their positions to account for changes in volatility.

Fluctuations in the underlying asset price affect option values through delta sensitivity. Strategies like straddles and strangles combine call-and-put options to isolate pure volatility exposure uncorrelated with directional price action.

Options have multiple Greeks beyond simply Vega that interact in complicated ways. Traders neutralize unwanted Greeks by legging into offsetting options contracts. Delta hedging also strips out directional risks from delta and gamma.

Selling options exposes traders to uncapped losses if implied volatility rises. Purchasing protective long options caps this downside risk. For example, buying a farther out-of-the-money call hedges a short-call position. The long call protects if volatility spikes.

Concentrate trading on highly liquid underlying like major indexes and large-cap stocks. The improved spreads and pricing transparency of liquid options enhance the effective execution of Vega strategies.

Analyse put and call implied volatility skews to detect trading opportunities from skew divergences over various expiries and strike prices. Changes in skew slopes signal potential mispricings.

Monitor changes in correlations between asset volatilities. Falling correlations, for instance, between equities and gold volatility, alter the effectiveness of hedging strategies.

Implied volatility tends to cycle between periods of expansion and contraction. Develop models or indicators to identify volatility regimes and optimize the entry/exit timing of Vega trades.

The leveraged nature of options requires modest overall position sizing relative to portfolio assets. Excessive Vega leads to oversized losses from adverse volatility swings.

Use stop losses, profit targets, maximum loss limits, and exit triggers to enforce trading discipline. Define and stick to risk/reward objectives for all Vega option positions.

What are some common misconceptions about Vega?

Common misconceptions about Vega are that it only matters for options expiring soon, it is the same as volatility, and that Vega cannot be hedged.

1. Vega Always Increases Option Values

Vega measures the change in an option’s price based on a 1% change in implied volatility. It does not necessarily mean higher volatility always increases option values. For example, VIX options or downside options sometimes decline if broad market volatility rises. Higher volatility hurts certain option positions depending on their structure. Vega indicates sensitivity, not a definitive direction.

2. Vega Is the Same for Calls and Puts

Calls generally exhibit higher Vega than puts on the same underlying. This is because calls benefit from upside volatility, whereas puts benefit more from downside volatility. The asymmetric return profile makes calls more responsive to volatility changes, resulting in higher Vega values for calls.

3. Vega Is Higher for In-the-Money Options

In-the-money options behave more like the underlying and have less volatility exposure. Maximum Vega is achieved for at-the-money options where the strike price equals the current market price. As options move deeper in or out of the money, their Vega declines.

4. Vega is sometimes Negative

Vega is almost always positive outside of some exotic option structures. The convexity of options payoffs means volatility is positive for both calls and puts. It is extremely rare to see negative Vega in traditional options since higher volatility increases their value.

5. Vega Is Constant Over Time

An option’s Vega deteriorates rapidly as maturity approaches, falling to zero at expiration. Longer-dated options have higher Vega. The time value erosion from theta decay reduces Vega significantly near expiry.

6. High Vega Means Bigger Gains

Higher Vega options do not necessarily produce greater profits. Gains depend on the magnitude of implied volatility changes. A 10% Vega option could produce lower returns than a 5% Vega option if volatility increases more modestly. The projected volatility move determines returns.

7. Vega Trading Is Less Risky

Vega trading carries significant risks, including volatility forecasting errors, uncapped losses on shorts, early assignment, and loss amplification from leverage. Appropriate position sizing, hedge correlation analysis, greeks balancing, and risk management protocols are required to trade Vega prudently.

8. Vega Is All That Matters

While Vega measures volatility sensitivity, options prices are also affected by delta, gamma, theta theta, and rho. Focusing solely on Vega ignores risks from underlying price actions and time decay. A comprehensive Greek-based perspective is required to trade options effectively.

9. Vega is sometimes Arbitraged

Arbitrage opportunities from Vega are limited since implied volatility levels reflect market consensus. Volatility arbitrage involves complex strategies like assessing skew patterns, volatility cycles, and relative value between correlated assets – not simply long/short Vega trading.

Assessing options based on a holistic Greek approach rather than viewing Vega in isolation avoids misconceptions that could lead to flawed volatility strategies.

What is the difference between Vega and Theta?

Vega measures an option’s sensitivity to changes in implied volatility, while theta measures the rate of decline in an option’s value due to the passage of time. While both are important Greeks, Vega and Theta differ in significant ways.

Vega is determined by changes in implied volatility, which represents an estimate of future volatility. Theta, on the other hand, simply measures the time decay as the option approaches its expiration date. Vega reacts to changing volatility expectations, while theta theta is purely a function of time.

Vega produces returns in an option position if implied volatility increases or decreases depending on the trader’s exposure. Theta, however, always results in negative returns as options lose value over time. Traders cannot profit from theta theta – they only seek to minimize losses.

As expiration approaches, theta theta accelerates rapidly, draining an option’s remaining time premium. But Vega steadily declines near expiry as volatility becomes less relevant with little time left. Theta spikes, leading into expiration, while Vega falls to zero.

Vega is maximized for at-the-money options with medium time remaining. Far out-of-the-money options have lower Vega but also diminished theta theta. Deep-in-the-money options exhibit lower Vega and theta theta. Different positioning impacts Vega versus theta exposures.

Long options positions generate negative theta theta but positive Vega. These are incorporated as portfolio hedges to offset theta losses against volatility protection. Theta and Vega offer different, sometimes contrary, hedging attributes.

Theta always generates negative slippage that must be mitigated or overcome. But, Vega poses bidirectional risks depending on the direction of volatility. Traders potentially profit from appropriately positioned Vega exposure.

While theta theta and Vega are distinct Greeks, they do interact inversely. As theta acceleration nears expiration, it erodes the time premium that contributes to Vega. So, theta decay has a dampening effect on Vega.

Theta Burn provides short trading options around earnings events. Meanwhile, Vega trading involves volatility cycles, skew analysis, and spreads for volatility isolation. Theta and Vega offer different tactical approaches.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 32")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.