Variance Swap is an over-the-counter derivative that lets traders speculate on or hedge against the future variance (volatility squared) of an asset’s price. Variance Swap pays out based on the difference between realized variance and a pre-agreed strike, providing pure volatility exposure without any directional risk.

The contract is settled in cash, making it attractive for institutional traders, volatility arbitrageurs, and hedgers. Pricing uses a strip of options weighted by the inverse square of strike. Main risks include jump risk, model error, and counterparty risk. Compared to volatility swaps, variance swaps are more sensitive to extreme price moves and are widely used for volatility trading.

What Is a Variance Swap?

A variance swap is an over-the-counter derivative contract that allows traders to speculate on or hedge against the future variance (i.e., volatility squared) of an underlying asset’s price. The variance swap contract settles in cash based on the difference between realized variance and a pre-agreed variance strike, both measured over a set period.

Variance swaps are unique because they deliver pure exposure to volatility, not direction. Unlike options, they pay out based only on the magnitude of price moves, regardless of whether the market goes up or down. The reference asset might be a stock, index, interest rate, or even an exchange rate.

The main appeal is the ability to isolate and trade volatility risk directly, with no need for delta hedging. This makes them highly attractive for institutional traders and hedge funds. The payout depends on realized volatility over the contract life, making them valuable for volatility arbitrage and managing risk in complex portfolios.

How Does a Variance Swap Work?

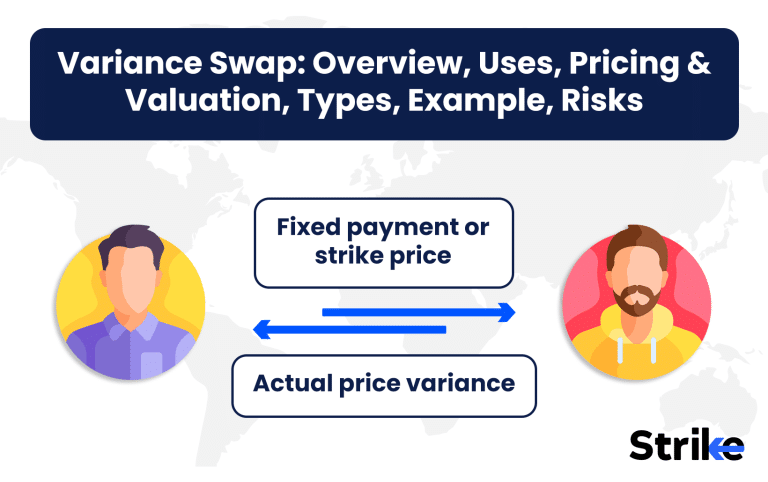

A variance swap works by exchanging cash flows between two parties: one pays the realized variance of the underlying asset, and the other pays a fixed strike set at inception. At maturity, the net payoff equals the notional amount multiplied by the difference between realized variance and the variance strike.

One leg pays an amount based on the actual variance observed (using daily log returns, annualized), while the other leg pays a fixed amount agreed at the start.

The payoff formula is , Payoff = Variance Notional × (Realized Variance – Variance Strike).

Where Variance Notional is usually quoted in Rs. per variance point, Realized Variance is calculated from observed returns, and Variance Strike is set at inception.

No directional exposure: The payoff is unaffected by the direction of the underlying’s movement. Only the size of movement matters.

For example, if the realized variance is higher than the strike, the buyer of the variance swap profits. If it’s lower, the seller profits. This structure provides pure volatility exposure, without the complications of options’ delta or gamma.

Who Uses Variance Swap and Why?

Variance swaps are used by volatility traders, hedgers, and institutional desks to gain or offset exposure to volatility without taking on directional risk. The main user groups include three.

- Volatility traders: These market participants seek to express directional views on volatility, betting that realized volatility will differ from market expectations.

- Hedgers: Fund managers or dealers with exposure to structured products, convertible bonds, or large options books use variance swaps to neutralize volatility risk.

- Institutional speculators: Banks, hedge funds, and proprietary trading desks use variance swaps for arbitrage, portfolio insurance, or to structure complex products for clients.

By providing a direct bet on realized volatility, variance swaps are far more efficient than trying to replicate volatility exposures using options, which require constant rebalancing and often come with slippage or tracking error. They are frequently used in volatility strategies, and their OTC nature allows large, customized exposures that suit institutional needs.

What Is the Variance Risk Premium?

The variance risk premium refers to the typical difference between implied variance (set at inception in the swap) and the variance that actually gets realized; historically, implied variance exceeds realized variance. This difference is central to volatility arbitrage strategies.

- Implied vs. realized: Market prices for variance swaps generally anticipate higher volatility than what is realized, creating a premium for those willing to sell variance.

- Volatility arbitrage: Hedge funds and prop desks exploit this by selling variance swaps, collecting the premium if realized moves are lower than implied.

- Historical context: Before the 2008 financial crisis, many hedge funds systematically sold variance swaps, earning steady returns. After 2008, the risk of large, sudden volatility spikes became more apparent, and the premium adjusted higher.

This premium reflects the market’s compensation for bearing volatility tail risk. It remains a key element in the risk-return profile of variance swaps.

What’s the Pricing Mechanism and Valuation Methods of Variance Swap?

Variance swaps are priced using a portfolio of European call and put options weighted inversely by the square of the strike price, allowing for accurate replication of variance exposure. The Wikipedia reference explains that the fair value of a variance swap can be derived from the prices of vanilla options across all strikes.

- Static replication: The theoretical price uses a strip of out-of-the-money puts and calls, plus a bond and a futures contract. The payoff is mathematically equivalent to the weighted sum of all options’ prices.

- Formula:

- Discrete sampling: In practice, realized variance is calculated from observed daily log returns, annualized using a standard factor (often 252 for trading days).

- No arbitrage: The fair strike is set so the contract has zero value at inception, ensuring no arbitrage.

Market models like Heston are often used for analytical pricing in option trading. Market practice also includes Monte Carlo simulations for more complex underlyings or payoff structures.

What are the Types of Variance Swap?

There are three main types of variance swaps, each providing different exposures to volatility depending on their structure.

- Vanilla variance swap: The standard product, providing exposure to the full realized variance over the life of the contract.

- Conditional variance swap: Pays only on variance realized when the underlying trades within a specified price corridor, making the exposure more targeted.

- Exotic variations:

- Corridor variance swap: Only considers variance when the underlying is within a set range.

- Forward-start variance swap: Exposure starts at a future date, useful for anticipated events.

- Gamma swaps: Pay based on the realized variance weighted by the underlying’s price level.

These variants help traders fine-tune their exposure, hedge specific risks, or construct more complex volatility-linked products for bespoke needs. Each offers different risk and reward profiles.

What is an Example of Variance Swap?

A typical variance swap example involves two parties agreeing to exchange realized variance for a fixed strike over a set period, with payoff determined at expiry. Suppose an investor and a dealer enter a variance swap on NIFTY with the following terms.

- Notional: Rs. 10,00,000 per variance point.

- Variance strike: 0.04 (implies 20% annualized volatility).

- Measurement period: 1 year.

At expiry, realized variance is measured from daily log returns and annualized. Assume the realized variance is 0.0625 (25% annualized volatility). The payoff to the buyer is:

- Payoff = Notional × (Realized Variance – Strike)

- = Rs. 10,00,000 × (0.0625 – 0.04) = Rs. 2,25,000

If realized variance is less than the strike, the seller profits instead. This payoff is independent of the direction of NIFTY’s movement—only the size of its swings over the year matters.

What are the Risks and Limitations of Variance Swap?

Variance swaps carry risks, including jump risk, model risk, counterparty risk, and negative convexity fVariance swaps carry risks, including jump risk, model risk, counterparty risk, and negative convexity for those selling the product. Each risk affects the payout and suitability for certain market participants.

- Jump risk: Large, unexpected price moves (jumps) significantly increase realized variance, leading to outsized losses for sellers.

- Model dependence: Pricing uses option-implied volatilities across strikes; misestimation or calibration errors impact the fair value.

- Counterparty and liquidity risk: Variance swaps are OTC instruments, so participants are exposed to default risk and may face illiquidity, especially in stressed markets.

- Negative convexity: Sellers of variance swaps face increasing losses as volatility rises; this is known as negative convexity.

These risks require careful management, margining, and often limit access to sophisticated institutions. Past crises like 2008 have highlighted these vulnerabilities, with some sellers experiencing significant losses.

What’s the Difference Between Variance Swap vs Volatility Swap?

The main difference between a variance swap and a volatility swap is that a variance swap’s payoff depends on the squared volatility (variance) of the underlying asset, while a volatility swap’s payoff depends on the actual volatility (standard deviation), making the variance swap more sensitive to large price moves.

| Feature | Variance Swap | Volatility Swap |

| Payoff | Based on squared volatility (variance) | Based on volatility (standard deviation) |

| Formula | Notional × (Realized Var – Strike Var) | Notional × (Realized Vol – Strike Vol) |

| Sensitivity | More sensitive to large moves (jumps) | Less sensitive (linear in volatility) |

| Replication | Strip of options (weighted by 1/K²) | Similar but more complex, non-linear |

| Market Use | More liquid and widely used | Used, but less common |

| Negative Convexity | Higher for variance sellers | Lower compared to variance swaps |

| Hedging Complexity | Easier to statically replicate | Harder due to non-linearity |

Variance swaps provide pure exposure to variance, while volatility swaps target volatility directly. The choice depends on the desired payoff profile, risk tolerance, and available hedging instruments.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 30")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 31")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 32")

: Overview, 10 Types of Indicators, Settings for Different Markets 34")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 36")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 39")

No Comments Yet.