A synthetic covered call is an options trading strategy designed to replicate the payoff of a traditional covered call without requiring ownership of 100 shares. A synthetic covered call uses a deep in-the-money call to mimic share ownership and an out-of-the-money call to generate income. This makes it highly capital-efficient for traders who want exposure to premium income without tying up large capital.

Statistics show the growing adoption of synthetic covered calls in retail markets. According to the Options Clearing Corporation, retail option volume in single-leg LEAPS (long-term calls) grew more than 40% between 2018 and 2023, highlighting increasing use of synthetic substitutes. Market-neutral and income-generating strategies, including synthetic covered calls, are widely used by hedge funds to enhance yield in sideways or moderately bullish markets.

What is a Synthetic Covered Call?

A synthetic covered call is an options strategy where a trader buys a deep in-the-money call and sells a near-term out-of-the-money or at-the-money call. This setup replicates owning stock and simultaneously writing a call option against it.

The long deep ITM call provides nearly identical price movement to stock ownership because of its high delta. The short call generates income by collecting premium, just like in a traditional covered call. Together, they create a position with limited upside potential and downside risk tied to the cost of the long call.

This structure is often referred to as the “Poor Man’s Covered Call” or a more flexible form of covered calls, but technically it is a pure synthetic equivalent. Unlike holding shares, the trader holds option contracts that simulate share behavior and option-writing income.

How Does a Synthetic Covered Call Work?

A synthetic covered call works by combining a deep in-the-money long call with a short call to create stock-like exposure plus premium income. The goal is to replicate the risk and reward of a covered call while committing less capital.

It is constructed as follows

- Long Call: Deep ITM call option, often a LEAPS, which has high delta and mimics stock ownership.

- Short Call: Near-term OTM or ATM call that collects option premium and generates income.

- Net Exposure: Similar to long stock plus short call, but without needing to buy 100 shares.

- Margin Requirements: Typically lower than buying stock, making it attractive to retail traders.

Payoff Comparison

| Strategy | Components | Upside Profit | Downside Risk | Capital Needed | Time Decay Impact |

| Traditional Covered Call | Long 100 shares + Short Call | Limited above strike | Loss below stock cost | High (stock cost) | Short call positive |

| Synthetic Covered Call | Long ITM Call + Short Call | Limited above strike | Loss below call debit | Much lower (option debit) | Long call negative, short call positive |

A payoff diagram of the synthetic covered call using Leaps mirrors the traditional version. The position profits in moderately bullish or sideways markets but loses if the stock drops significantly below the ITM strike price.

Why Use a Synthetic Covered Call Strategy?

A synthetic covered call is used to achieve capital efficiency and income generation without owning stock. Traders prefer it because it offers flexibility and accessibility.

- Capital Efficiency: Buying stock requires significant cash, while a deep ITM call costs much less.

- Lower Entry Barrier: Retail traders can access strategies on high-priced stocks without needing thousands of dollars.

- Flexibility: Adjustments are easier since rolling calls requires less cash movement than selling stock.

- Paper Trading & Hedging: Useful in simulations or hedging without physical share transactions.

For example, a stock trading at Rs.3,500 would require Rs.350,000 to own 100 shares. A synthetic covered call option strategy using a LEAPS deep ITM call might cost only Rs60,000 to replicate a similar payoff while still allowing the trader to sell short calls against it.

When to Use a Synthetic Covered Call?

A synthetic covered call is best used in bullish or neutral markets where traders seek income and exposure without buying shares. It is especially effective for high-priced stocks.

- Bullish to Neutral Outlook: The strategy profits if the stock rises modestly or stays flat, as the short call premium cushions mild downside.

- Avoiding Stock Ownership: Traders unwilling or unable to purchase shares directly find this setup cost-effective.

- Expensive Stocks: High-value stocks like AMZN, TSLA, or GOOG are popular for synthetics because owning 100 shares is costly.

- Income Seeking: Premium from the short call adds consistent income opportunities.

A common use case occurs around earnings, where traders expect stability but not a breakout move. Entering a synthetic options covered call allows them to earn income from call selling while holding stock-like exposure via the long call.

How Option Greeks Affect Synthetic Covered Call?

Option Greeks affect synthetic covered calls by defining risk and reward sensitivity to price, time, and volatility. The position behaves similarly to a covered call but with some differences.

- Delta: The long deep ITM call has high delta (0.80–0.95), mimicking stock movement. The short call reduces net delta slightly, just like in a covered call.

- Theta: Time decay hurts the long call but helps the short call. Net theta is slightly positive, making the strategy income-friendly.

- Vega: The long call benefits from rising implied volatility, while the short call loses value. Net effect is balanced but not neutral.

- Gamma: Exposure remains low to moderate, ensuring stability in small price movements.

Greek Profile Comparison

| Greek | Traditional Covered Call | Synthetic Covered Call |

| Delta | ~0.60–0.70 | ~0.60–0.70 |

| Theta | Slightly Positive | Slightly Positive |

| Vega | Neutral | Mixed, depends on option structure |

| Gamma | Low | Low |

This makes the strategy appealing for traders who want steady returns with controlled risk exposure.

How Implied Volatility Affects Synthetic Covered Call?

Implied volatility directly impacts synthetic covered calls by changing option premiums and overall profitability. Both legs react differently to IV changes.

- Higher IV: Increases the cost of the long ITM call but also raises premium received from the short call.

- IV Crush: After earnings or big events, the long call may lose value rapidly, while the short call premium declines too.

- Best Entry: Traders often initiate synthetic covered calls when implied volatility is elevated, ensuring maximum short call premium.

- Risk Management: Monitoring IV is essential because swings influence both income and net exposure.

For instance, entering the strategy before earnings with high IV can lead to attractive premium income. However, an IV crush post-earnings reduces the value of both legs, limiting profits.

How to Trade using Synthetic Covered Call?

Trading a synthetic covered call involves buying a deep ITM call and selling a near-term call, step by step. The execution requires careful strike selection and breakeven analysis.

Trading a synthetic covered call involves buying a deep ITM call and selling a near-term call in the same stock. The goal is to replicate covered call payoffs with less capital while generating regular income.

- Choose Asset & Outlook

Select a stock or index with a bullish to neutral outlook. For Indian markets, traders often use NIFTY, BANKNIFTY, or liquid stocks like Reliance, HDFC Bank, or Infosys. These have active options chains with tight spreads and good liquidity. - Buy Long Call (Synthetic Stock)

Pick a LEAPS or a deep ITM call with delta around 0.80–0.95. In India, LEAPS (long-term options) go up to 1 year expiry. For example, suppose Reliance trades at ₹2,500. A trader could buy a Reliance 2000 CE (1-year expiry). This option behaves almost like owning stock, but costs a fraction compared to buying 100 shares (₹2.5 lakh). - Sell Short Call (Income Leg)

Write a near-term ATM or slightly OTM call to collect premium. Continuing the Reliance example, the trader could sell a Reliance 2500 CE (1-month expiry) for, say, ₹40. This generates premium income immediately. - Check Costs & Margin

Assume the long ITM 2000 CE costs ₹600 and the short 2500 CE brings in ₹40. Net debit = ₹560 × 505 (lot size) = ₹2,83,000 approx. This is far cheaper than owning 100 shares worth ₹2,50,000 × 1 = ₹2,50,000 (for 1 lot, NSE lot sizes vary). - Monitor & Adjust

As expiry approaches, the short call decays in value. Traders can roll it to the next month for additional premium. If Reliance rallies sharply, rolling strikes higher locks further gains.

Outcome

- Stock price at trade entry: ₹2,500

- Buy Reliance 2000 CE (1-year) = ₹600

- Sell Reliance 2500 CE (1-month) = ₹40

- Net debit = ₹560

Breakeven = 2000 + 560 = ₹2,560

Maximum Profit = (2500 – 2000 – 560) × lot size = -₹60 loss beyond breakeven (since capped upside)

Risk = Entire debit of ₹560 per share (₹2,83,000 total).

This mirrors the covered call payoff but avoids buying costly shares directly.

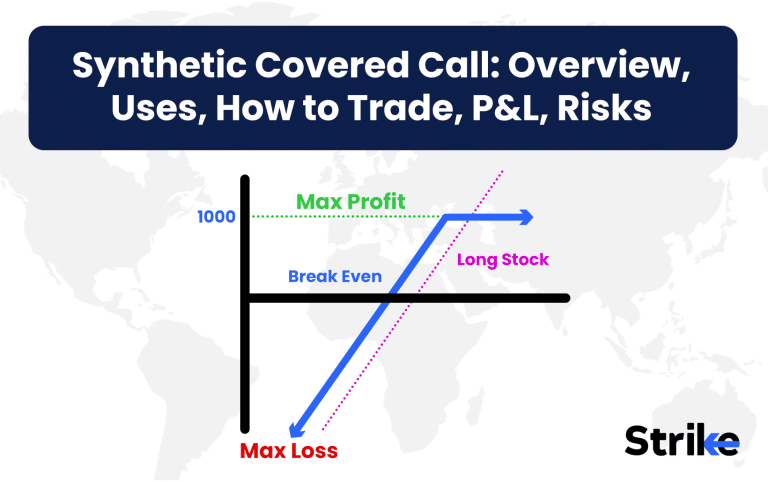

What are the Maximum Profit & Loss, Breakeven on a Synthetic Covered Call?

The maximum profit of a synthetic covered call is limited to the short call strike minus the cost of the long call, while the maximum loss equals the net debit paid for the position. This mirrors the structure of a traditional covered call.

- Maximum Profit

- Occurs when the stock closes at or above the short call strike at expiry.

- Formula = (Short Call Strike – Long Call Strike) – Net Debit.

- Profit is capped because the short call offsets gains beyond its strike.

- Maximum Loss

- Defined by the premium paid for the long ITM call minus premium received from the short call.

- The entire long call premium could be lost if the stock falls significantly.

- Breakeven Point

- Breakeven = Long Call Strike + Net Debit – Short Call Premium.

- This ensures that gains above this level offset costs.

Assume TATA is at Rs.900.

- Buy deep ITM LEAPS call (strike Rs.700, cost Rs.220).

- Sell short-term ATM call (strike Rs.900, premium received Rs.25).

- Net debit = Rs.195.

- Breakeven = Rs.700 + Rs.195 = Rs.895.

- Max profit = (Rs.900 – Rs.700) – Rs.195 = Rs.5 per share (Rs.500 total for 1 contract).

- Max loss = Rs.195 per share (Rs.19,500 total).

This shows how the strategy limits upside while defining loss based on initial outlay.

What are the Risks of Synthetic Covered Call?

The primary risks of a synthetic covered call include losing the long call premium, assignment on the short call, and time decay eroding the long call’s value. Traders must also account for mispricing and liquidity issues.

- Long Call Expiry: The deep ITM call could expire worthless if the stock crashes, resulting in large losses.

- Assignment Risk: The short call could be exercised early, especially near dividends, forcing adjustments.

- Time Decay: The long call loses value as expiry nears, reducing synthetic stock-like behavior.

- Liquidity Issues: Wide bid-ask spreads on LEAPS can reduce efficiency and increase slippage.

- Broker Approval: Not all traders have access to Level 3 options approval required for spreads.

Risk management requires choosing liquid underlyings with tight spreads, rolling short calls regularly to control assignment and entering positions with well-defined capital allocation.

What’s the Difference Between Synthetic Covered Call vs Synthetic Covered Put?

A synthetic covered call is a bullish income strategy using long calls and short calls, while a synthetic covered put is a bearish strategy using short stock and long puts. Both provide controlled risk but differ in outlook.

| Strategy | Components | Market Outlook | Profit Profile | Risk Profile | Use Case |

| Synthetic Covered Call | Long ITM Call + Short Call | Bullish to Neutral | Income + capped upside | Long call premium at risk | Used for premium income without stock ownership |

| Synthetic Covered Put | Short Stock + Long Put | Bearish | Limited profit, capped downside | Risk if stock rallies hard | Used for bearish bets while hedging upside risk |

The synthetic covered call suits traders expecting modest gains or sideways moves. The synthetic covered put suits traders expecting declines but wanting downside hedging.

Is Synthetic Covered Call Strategy Profitable?

Yes, a synthetic covered call is profitable when the stock rises moderately or trades sideways, allowing the trader to keep short call premium. Profitability depends on strike selection, volatility, and timing.

The strategy earns income regularly from short calls. Over time, these premiums accumulate and offset the long call’s cost. Success rates increase in stable markets where large price swings are less frequent.

Is Synthetic Covered Call Bullish or Bearish?

A synthetic covered call is a bullish-to-neutral strategy. The trader expects moderate gains or stability, not large rallies or sharp drops.

- Bullish Element: The long ITM call acts like stock ownership, profiting from upward moves.

- Neutral Element: The short call premium cushions flat markets and mild declines.

- Not Bearish: The structure loses value in steep declines, making it unsuitable for bearish conditions.

In essence, the trader sacrifices unlimited upside for steady premium income, aligning with moderately bullish or neutral outlooks.

What are Alternatives to Synthetic Covered Call Strategy?

Alternatives to a synthetic covered call include traditional covered calls, poor man’s covered calls, diagonal spreads, and cash-secured puts. Each offers different trade-offs in capital, risk, and payoff.

| Alternative | Structure | Pros | Cons |

| Traditional Covered Call | Buy 100 shares + sell call | Straightforward, dividend income | High capital requirement |

| Poor Man’s Covered Call | LEAPS + short call | Cheaper, long-term flexibility | LEAPS lose time value |

| Diagonal Call Spread | Buy long-term call + sell shorter-dated call | Rolling flexibility, lower cost | Complex management |

| Cash-Secured Put | Sell put against cash | Income, potential stock entry at discount | Risk if stock falls sharply |

Each alternative fits a slightly different trader profile. For capital efficiency, synthetic or poor man’s covered calls are best. For conservative investors, covered calls and cash-secured puts work better.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 8")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 9")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 10")

: Overview, 10 Types of Indicators, Settings for Different Markets 11")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 14")

No Comments Yet.