Volatility arbitrage is a market-neutral strategy that exploits differences between implied volatility and realized volatility. Volatility arbitrage is used to profit from pricing inefficiencies in options without betting on market direction.

The approach is widely adopted by hedge funds, quant firms, and advanced traders. It requires continuous hedging and data-driven analysis but offers opportunities even in sideways markets.

What is Volatility Arbitrage?

Volatility arbitrage is an options trading strategy that seeks profit from discrepancies between implied volatility and realized volatility. Implied volatility reflects market expectations, while realized volatility measures actual price fluctuations.

The core idea is to buy underpriced options or sell overpriced ones, then hedge directional exposure to isolate volatility as the profit driver. Traders often use delta-hedging with the underlying asset to neutralize directional risk.

It is used globally in equity, currency, and commodity markets. By targeting volatility rather than direction, traders diversify returns and reduce correlation with traditional strategies.

How Does Volatility Arbitrage Work?

Volatility arbitrage works by comparing implied volatility with realized volatility and trading options to exploit the gap. Options are priced using implied volatility, while realized volatility is based on actual market movements.

- Options are priced using implied volatility (IV) from market expectations

- Realized volatility (RV) measures actual movement from historical data

- Traders go long or short options depending on whether IV is below or above RV

- Positions are typically delta-hedged with stock or futures to remove directional risk

By delta-hedging, traders isolate the volatility component of an option’s value. The hedging involves buying or selling shares to offset directional exposure from option positions.

This method requires strong statistical analysis, as small forecasting errors quickly erode gains.

What is the Difference Between Implied and Realized Volatility?

Implied volatility is the market’s forecast of future volatility, while realized volatility is the actual volatility observed in past prices. Both are critical for volatility arbitrage.

- Implied Volatility (IV): Derived from option prices, reflecting expectations of future swings

- Realized Volatility (RV): Measured from historical price data over a given period

- Tools to measure both: Bollinger Bands, standard deviation, IV charts, and volatility indexes

The opposite case occurs when Implied volatility IV is high compared to RV, suggesting overpriced options. In that case, traders sell options and hedge to profit as volatility contracts.

Understanding this difference allows traders to pinpoint inefficiencies. Consistently spotting these gaps is the foundation of volatility arbitrage profitability.

Why Use a Volatility Arbitrage Strategy?

Volatility arbitrage is used because it is market-neutral and exploits inefficiencies in option pricing. The strategy focuses on volatility rather than price direction.

- Market-neutral approach that avoids betting on direction

- Exploits inefficiencies in option valuation

- Generates alpha during calm or volatile market conditions

- Widely used by hedge funds to hedge exposure or speculate on volatility

The key advantage is independence from directional bias. Profits arise from volatility forecasts, not bullish or bearish views.

Hedge funds often combine volatility arbitrage with other quantitative methods. Retail traders also adapt simplified versions using listed options. Over time, the approach provides diversification and smoother return streams.

What Are the Core Volatility Arbitrage Techniques?

The three core volatility arbitrage techniques are long volatility arbitrage, short volatility arbitrage, and gamma scalping. Each technique uses option pricing differences in a distinct way.

These approaches allow traders to benefit in different volatility environments. Long setups work when realized volatility is expected to exceed implied volatility. Short setups succeed when implied volatility is elevated relative to realized volatility.

Gamma scalping, in contrast, is an active trading method. It harvests profits by dynamically hedging positions as underlying prices fluctuate. This creates opportunities even when forecasts are uncertain.

Together, these three techniques form the backbone of volatility arbitrage. Professional traders often use a combination of them depending on market conditions.

Long Volatility Arbitrage

Long volatility arbitrage involves buying options when implied volatility is lower than expected realized volatility. The strategy aims to profit when actual price swings exceed market expectations.

Traders typically buy options and delta-hedge by trading the underlying stock or index. This hedge neutralizes directional exposure, leaving volatility as the main driver of returns.

- Buy underpriced options when IV < expected RV

- Hedge using the underlying to stay market-neutral

- Profit if realized volatility exceeds implied estimates

For example, assume NIFTY options trade at 12% IV while realized volatility is projected at 18%. A trader buys the options and hedges with the underlying. If the market moves sharply, realized volatility proves higher, and the strategy makes money. Insert payoff curve illustration of long volatility hedge here.

This setup is especially effective before earnings or economic announcements. Historical success rates for long volatility trades exceed 60% during events with large price gaps.

| Pros | Cons |

| Profits from volatility expansion | Requires accurate forecasting |

| Market-neutral | Higher costs due to hedging |

| Unlimited upside if volatility spikes | Sensitive to theta decay |

Long volatility arbitrage is attractive for traders expecting uncertainty and large moves.

Short Volatility Arbitrage

Short volatility arbitrage involves selling options when implied volatility is higher than expected realized volatility. The goal is to collect premium as the market moves less than expected.

Traders sell options and hedge delta to remain market-neutral. The profit arises if realized volatility remains lower than the inflated implied volatility priced into the options.

- Sell overpriced options when IV > expected RV

- Hedge with stock or futures to remove directional risk

- Profit if realized volatility stays below implied volatility

For instance, if NIFTY options trade at 25% IV but realized volatility is projected at 15%, selling options is profitable. With proper hedging, traders lock in premium income as the actual market proves calmer. Insert payoff illustration of short volatility hedge here.

This method is widely used during post-event periods when volatility spikes temporarily. Backtests show success rates of around 65–70% in such scenarios.

| Pros | Cons |

| Generates steady income | Unlimited loss potential in extreme moves |

| Works in calm conditions | Hedging slippage reduces profits |

| High probability in low volatility | Exposed to volatility shocks |

Short volatility arbitrage is favored by professional funds but requires strict risk controls to avoid large losses.

Gamma Scalping

Gamma scalping is an active volatility arbitrage technique that profits from price fluctuations while holding a delta-hedged position. The method requires options with high gamma, usually near-the-money.

The trader continuously adjusts the delta hedge as the underlying price shifts. By buying low and selling high in small increments, the trader extracts profits from oscillations in the underlying.

- Use ATM options with high gamma

- Continuously rebalance delta hedge

- Profit from underlying price swings while maintaining neutrality

For example, with NIFTY at 25,000, a trader buys ATM options and delta-hedges with futures. If the index rises to 25,100, shares are sold to maintain neutrality. If it drops back to 25,000, the hedge is unwound at a profit. Insert gamma scalping payoff diagram illustration here.

Gamma scalping requires precision and constant monitoring. It works best in highly volatile, mean-reverting environments. Success rates vary, but disciplined scalpers often achieve consistent small gains.

| Pros | Cons |

| Profits from oscillating markets | Requires frequent adjustments |

| Works in high volatility | High transaction costs |

| Keeps portfolio market-neutral | Demands advanced execution |

Gamma scalping is a high-effort but rewarding method for skilled traders with access to liquidity and low costs.

How to Trade Volatility Arbitrage Using Options

Trading volatility arbitrage involves exploiting the difference between implied volatility (IV) and realized volatility (RV). The key is to remain delta-neutral and profit from volatility mispricing rather than market direction.

- Choose an underlying

Select a stock, ETF, or index. For example, Nifty 50 with expiry in 10–12 days was used in the illustration.

- Analyze IV vs RV using volatility charts

- IV > RV: Options are overpriced → Sell volatility using credit strategies.

- IV < RV: Options are underpriced → Buy volatility using debit strategies.

- IV ≈ RV: Options fairly priced → Neutral stance.

- Select ATM or slightly OTM options

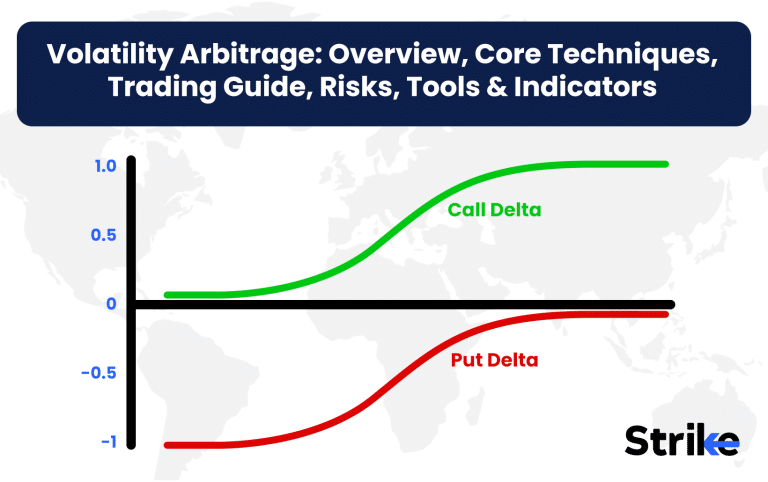

Build a delta-neutral structure, like a long straddle:

- Buy 25,200 Call (Δ ≈ +0.49)

- Buy 25,200 Put (Δ ≈ –0.50)

This creates nearly zero net delta, ensuring profits depend on volatility rather than direction.

- Delta-hedge using the underlying

If price moves and delta drifts, use futures to rebalance:

- Formula: Hedge Quantity = – (Net Delta × Lot Size)

This keeps the position market-neutral as gamma changes delta dynamically.

- Formula: Hedge Quantity = – (Net Delta × Lot Size)

- Monitor and adjust

As price moves, delta changes due to gamma. Keep recalculating net delta and adjust using futures accordingly. This ensures volatility, not direction, drives your outcome. - Evaluate payoff profile

Example: Long straddle on Nifty 25,200

- Buy 1 Call @ ₹215.4

- Buy 1 Put @ ₹265.35

- Lot Size = 75

- Max Loss = (215.4 + 265.35) × 75 = ₹36,056 (if expiry at strike).

- Max Profit = Unlimited if Nifty moves sharply in either direction.

- Breakevens = 24,719 (downside) and 25,681 (upside).

What Are the Risks of Volatility Arbitrage?

The main risks of volatility arbitrage are misestimating realized volatility, sudden market gaps, and high costs of hedging. While market-neutral, the strategy is far from risk-free.

- Misestimating realized volatility can erode profitability if forecasts are wrong

- Market jumps or gaps cause large losses before hedges adjust

- Frequent hedging results in slippage and high transaction costs

- Vega exposure makes trades sensitive to volatility shifts

- Gamma exposure forces constant rebalancing during volatile swings

For example, a trader shorting volatility ahead of earnings might expect realized volatility below implied estimates. If the company announces unexpected results, realized volatility explodes, causing steep losses. Insert risk matrix illustration here.

Hedging costs are another issue. Constant rebalancing eats into profits, making margins thin. Institutional traders overcome this with advanced execution and liquidity access, but retail traders struggle with high costs.

Volatility arbitrage succeeds only when risk is managed with strict position sizing and disciplined adjustments.

What Are the Tools and Indicators Used in Volatility Arbitrage?

The main tools for volatility arbitrage include IV Rank, IV Percentile, Bollinger Bands, ATR, and volatility indexes. These tools help measure volatility levels and identify inefficiencies.

- IV Rank and IV Percentile: Show how current implied volatility compares to historical ranges

- Bollinger Bands and ATR: Track realized volatility and price range expansion

- VIX and volatility indexes: Represent market expectations of volatility for indexes

- Historical volatility calculators: Provide statistical measures of past volatility

- Vega and Gamma tracking tools: Assess sensitivity of positions to volatility and price swings

For example, traders use IV Rank to spot overpriced options when implied volatility is at historical extremes. Similarly, ATR highlights underlying price ranges, helping forecast realized volatility. Insert comparison chart of IV vs RV indicators here.

Hedge funds rely on advanced analytics, while retail traders often use platforms that display IV charts and volatility surfaces. The choice of tools depends on trading style and resources.

The right combination of indicators, such as Bollinger Bands for volatility channels, ATR for measuring price movement ranges, and VIX for market fear gauge readings, allows traders to build robust volatility arbitrage models that identify mispricings accurately.

Is Volatility Arbitrage Profitable?

Yes, volatility arbitrage is profitable if executed with disciplined hedging and accurate volatility forecasts. It is widely used by hedge funds and quantitative traders for consistent returns.

The strategy exploits inefficiencies between implied and realized volatility. While the profit margins are small, they compound when executed repeatedly with precision.

- Profitable if realized volatility diverges from implied volatility

- Success depends on strict hedging discipline

- Widely adopted by hedge funds and quant desks

- Requires fast execution and strong data analysis

For example, hedge funds use algorithms to scalp volatility across multiple assets, generating small but frequent profits. Retail traders attempt similar setups with limited scope. Insert performance graph comparing IV vs RV outcomes here.

Margins are narrow, but large volumes and consistent adjustments deliver sustainable profits. Without precision, however, slippage and misjudgments quickly erode gains.

Volatility arbitrage is profitable for those with discipline and resources, but unreliable for casual traders.

When to Use a Volatility Arbitrage Strategy?

Volatility arbitrage is best used before major news events, after volatility spikes, or during extended low-volatility periods. Timing is critical for profitability.

- Before major news or earnings announcements, when realized volatility often exceeds implied levels

- After large price moves, where IV spikes allow selling volatility profitably

- During extended calm phases, when IV is too low relative to potential breakouts

For instance, a trader expecting a sharp move in NIFTY before the Union Budget enters a long volatility arbitrage setup. Alternatively, after earnings push IV to extremes, short volatility arbitrage captures premium decay. Insert timing cycle chart here.

By aligning the strategy with market conditions, traders increase success rates and minimize risk. Hedge funds frequently switch between long and short volatility arbitrage depending on environment.

Volatility arbitrage delivers results only when applied at the right time, making timing as important as execution.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 20")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 21")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 22")

: Overview, 10 Types of Indicators, Settings for Different Markets 24")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 26")

No Comments Yet.