A horizontal spread is an options trading strategy that profits from differences in time decay between short-term and long-term options. A horizontal spread is also known as a calendar spread because both options use the same strike but different expiry dates.

The history of horizontal spreads traces back to professional traders in the 1970s who began systematically exploiting time decay in options. With the rise of listed derivatives, traders realized that combining expiries gave predictable decay advantages.

What is a Horizontal Spread?

A horizontal spread is a strategy where a trader buys a longer-term option and sells a shorter-term option at the same strike. The profit comes from the faster decay of the short-term option compared to the long-term one.

It is called “horizontal” because the strike is the same but expiry dates differ along the time axis. This structure is designed to capture the effect of time decay (theta), while limiting exposure to large price moves.

Horizontal spreads are versatile. They can be structured with calls or puts, and are usually established as net debit trades, meaning the trader pays upfront.

How Does a Horizontal Spread Work?

A horizontal spread works by exploiting the difference in time decay between two options with the same strike but different expiries. The short option loses value faster, allowing the trader to benefit.

- Stock XYZ trades at ₹100.

- Buy 1 100 Call, 60-day expiry at ₹5.

- Sell 1 100 Call, 30-day expiry at ₹3.

- Net Debit = ₹2.

As 30 days pass, the short option decays faster than the long option. At the short option’s expiry, the trader ideally wants the stock near ₹100, where the short option expires worthless and the long option retains time value.

- Theta: The front-month call loses time value quickly.

- Vega: The back-month call benefits if implied volatility rises.

- Net Effect: The trader profits if the stock stays near the strike and volatility rises.

At expiry of the short call (30 days), the payoff curve looks like a tent shape centered at ₹100. Maximum profit occurs if the stock closes exactly at ₹100, because the short option expires worthless while the long option still has extrinsic value. Loss is limited to the initial debit paid.

Why Use a Horizontal Spread Strategy?

Traders use a horizontal spread to generate income from time decay while keeping risk defined. It is ideal for neutral to mildly directional views.

- Profits from Time Decay: The short option decays faster, producing income.

- Lower Cost: The premium collected from the short option reduces the cost of the long option.

- Neutral to Moderately Directional View: Works best when the stock consolidates near the strike.

- Flexibility: The spread can be adjusted into a diagonal spread by using different strikes, or rolled forward to manage exposure.

This strategy is particularly useful around earnings announcements where implied volatility is elevated in near-term options but lower in long-dated options, allowing traders to take advantage of both volatility differences and the effects of time decay.

When to Use a Horizontal Spread?

A horizontal spread is best used when a trader expects low movement in the underlying asset. It works in markets where volatility patterns create pricing inefficiencies.

- Low Price Movement Expected: The position makes the most money if the underlying price hovers near the strike.

- High Short-Term IV, Low Long-Term IV: Selling rich short-term volatility while buying cheaper long-term options increases edge.

- Earnings or Events: Ahead of results, short-term IV spikes. Traders sell short-term options and hedge with longer-term contracts.

In the Indian market, this is common in NIFTY and BANKNIFTY option trading before RBI policy announcements or large-cap stock earnings.

How Option Greeks Affect Horizontal Spread?

Option Greeks affect horizontal spreads by defining sensitivity to price, time, and volatility. The strategy benefits from theta and vega while keeping delta neutral.

- Theta: Positive, because the short-term option decays faster than the long-term option.

- Vega: Positive, since long-term options gain if implied volatility rises.

- Delta: Near-neutral at entry if options are at-the-money, but shifts as the stock moves.

- Gamma: Low, meaning limited sensitivity to small price moves.

This makes horizontal spreads appealing for traders who expect stability and want time decay to work in their favor.

How Implied Volatility Affects Horizontal Spread?

Implied volatility is critical for horizontal spreads because it influences both legs differently. Rising volatility generally benefits the strategy.

- Rising IV: Increases value of the long-dated option more than the short-dated one, improving profitability.

- Falling IV: Hurts the spread, since the long-dated option loses value.

- Best Case: IV rises in long-term options while short-term IV falls, such as after an earnings announcement.

- Volatility Skew: Traders analyze the IV surface to identify situations where calendar spreads are cheap.

This is often seen in BANKNIFTY, where short-term weekly options spike in Implied Volatility before events, while monthly options remain relatively cheaper.

How to Trade using Horizontal Spread?

Trading a horizontal spread involves buying a longer-dated option and selling a shorter-dated option at the same strike. The setup requires careful selection of strike and expiry.

Trading a horizontal spread involves buying a longer-dated option and selling a shorter-dated option at the same strike price. The success of this setup depends on careful strike selection, expiry choice, and volatility conditions.

- Choose Underlying

Select a stock or index that is expected to remain stable during the short option’s life. In India, liquid instruments like NIFTY, BANKNIFTY, Reliance, HDFC Bank, and Infosys are preferred because they have active option chains with narrow bid-ask spreads. - Select Strike

Pick an at-the-money (ATM) strike because the horizontal spread performs best when the underlying closes near the strike on the short expiry date. ATM strikes retain the highest extrinsic value, which maximizes the benefit of time decay. - Pick Expiries

Sell the near-term expiry (weekly or monthly) and buy the longer-term expiry (monthly or quarterly). This ensures the short option decays faster, while the long option still holds time value after the short leg expires. - Enter the Trade

Place the spread as a net debit order. The debit is the difference between the long option’s premium and the short option’s premium. Since debit defines the maximum risk, traders have clear downside exposure from the start. - Use Tools

Analyze the option chain to identify premiums across expiries. Tools like the probability cone help estimate the likelihood of the underlying finishing near the strike, which is key for profitability.

Suppose NIFTY is trading at 22,000.

- Buy NIFTY 22,000 CE (next month expiry) at ₹350

- Sell NIFTY 22,000 CE (this week expiry) at ₹200

- Net Debit = ₹150

In this trade,

- If NIFTY closes near 22,000 at the end of the week, the short option expires worthless. The long option still retains extrinsic value plus any intrinsic gain, creating maximum profit.

- If NIFTY moves far away (say 21,500 or 22,500), the spread loses effectiveness because the long option value does not cover the net debit.

- The maximum loss is ₹150, which is the upfront debit paid.

- The short weekly option loses value rapidly due to theta decay.

- The long monthly option retains value, especially if implied volatility rises.

The trade benefits from time decay mismatch and potential volatility skew between weekly and monthly contracts, which can be clearly observed through the option chain.

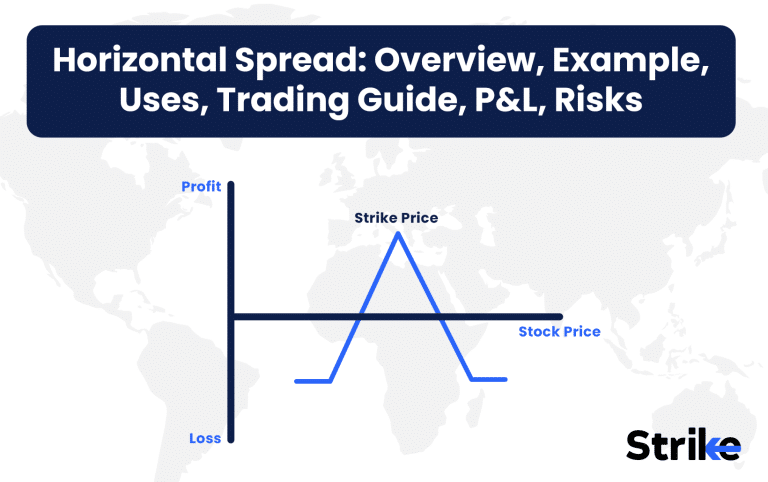

What are the Maximum Profit & Loss, Breakeven on a Horizontal Spread?

The maximum profit of a horizontal spread occurs when the underlying closes at the strike price of the options at short-term expiry, while the maximum loss equals the net debit paid. The payoff structure is unique and highly dependent on the timing of expiries.

- Maximum Profit

- Achieved when the stock finishes exactly at the strike on short option expiry.

- The short option expires worthless, while the long option retains time value.

- Formula = Value of long-dated option at front-month expiry – Net Debit.

- Maximum Loss

- Defined by the net debit paid for entering the position.

- If the stock moves far from the strike, both options lose value relative to the debit.

- Breakeven Points

- Breakeven is not a fixed number, as it shifts with volatility.

- Approximated by calculating ranges where long option value offsets initial debit.

For example,

- NIFTY at 22,000.

- Buy 22,000 CE (monthly) = ₹350.

- Sell 22,000 CE (weekly) = ₹200.

- Net Debit = ₹150.

If NIFTY closes near 22,000 at weekly expiry, profit is highest. If NIFTY drifts away, loss is capped at ₹150.

The payoff diagram looks like a tent curve, peaking at the strike and declining on either side.

What are the Risks of Horizontal Spread?

The primary risks of a horizontal spread are sharp price movement, volatility collapse, and assignment on the short option. Traders must manage these carefully.

- Sudden Price Move: If the stock rallies or falls sharply, both options lose relative value, and the debit becomes a loss.

- Implied Volatility Drop: If IV falls after trade entry, the long-dated option loses value faster, reducing profitability.

- Time Decay Mismatch: If the market stays too calm or moves too much, the spread produces smaller profits than expected.

- Assignment Risk: If the short option goes in-the-money before expiry, the trader risks early exercise. This is rare in Indian cash-settled index options but relevant in U.S. equity options.

- Liquidity: Longer-term options sometimes have wider bid-ask spreads, which increases slippage.

Risk management involves entering only in liquid underlyings, monitoring volatility conditions, and rolling short legs proactively.

Is Horizontal Spread Strategy Profitable?

Yes, a horizontal spread is profitable if the stock stays near the strike while implied volatility rises in longer-term options. It is designed to monetize theta and vega exposure.

Profitability improves in conditions where-

- Stock remains range-bound.

- Short-term implied volatility is higher than long-term volatility.

- Long-dated options retain significant time value.

According to CBOE data, calendar spreads deliver consistent returns in low-volatility regimes. Historical backtests show success rates of nearly 60–65% when used around earnings with carefully chosen strikes.

Traders often find profitability in NIFTY or BANKNIFTY horizontal spreads during policy weeks, where weekly options inflate but monthly options trade cheaper.

The strategy is not profitable in trending or highly volatile markets, as price moves erode the advantage of time decay.

Is Horizontal Spread Bullish or Bearish?

A horizontal spread is a neutral-to-slightly bullish strategy. The payoff is structured for stability rather than strong direction.

- Neutral: Works best if the stock closes at or near the strike.

- Bullish Tilt: A calendar using calls has mild bullish exposure if the stock rallies slowly.

- Bearish Tilt: A calendar using puts has mild bearish exposure if the stock declines moderately.

Traders often adapt the strategy depending on whether they use calls or puts. But in general, it is a range-bound strategy rather than directional.

What are Alternatives to Horizontal Spread Strategy?

Alternatives to a horizontal spread include vertical spreads, diagonal spreads, iron condors, and butterfly spreads. Each alternative offers a different mix of risk, reward, and complexity.

| Strategy | Structure | Market Outlook | Risk | Profit Zone | Best Use Case |

| Horizontal Spread | Buy long-term option, sell short-term option (same strike) | Neutral, low movement | Net debit | Peak at strike | Volatility skew, range-bound stocks |

| Vertical Spread | Buy and sell options of different strikes, same expiry | Bullish or bearish | Defined | Directional | Trending markets |

| Diagonal Spread | Buy long-term option, sell short-term option (different strikes) | Mild directional with volatility edge | Defined | Broader than horizontal | Trend + volatility play |

| Iron Condor | Sell OTM call spread + sell OTM put spread | Neutral, very low movement | Capped | Wide, low return | Range-bound index markets |

| Butterfly Spread | Buy 1 ITM, sell 2 ATM, buy 1 OTM | Neutral | Defined | Narrow peak at strike | Pinning around expiry |

Horizontal spreads remain attractive for traders who expect time decay to dominate price movement.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 16")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 17")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 18")

: Overview, 10 Types of Indicators, Settings for Different Markets 20")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 22")

No Comments Yet.