Strangle Option Strategy involves simultaneously purchasing or selling an out-of-the-money (OTM) call option and an OTM put option with the same expiration date but different strike prices. Strangle Option Strategy provides traders with a powerful method to capitalize on significant price movements regardless of direction while limiting potential losses to the premium paid.

Introduced in the early 1980s alongside the growth of options trading in India, strangles gained popularity after the establishment of the National Stock Exchange (NSE) in 1994. The strategy became widespread following the introduction of options trading on the NSE in 2001. According to recent SEBI data, strangles account for approximately 18% of all option combination strategies traded on Indian exchanges, with volumes exceeding ₹8,500 crores daily on the Nifty options alone.

What is a Strangle?

Strangle Option Strategy represents an options trading strategy where an investor simultaneously purchases or sells an out-of-the-money call option and an out-of-the-money put option on the same underlying asset with identical expiration dates but different strike prices. Strangle enables traders to profit from significant price movements in either direction without necessarily predicting which way the market will move.

The strategy derives its name from the concept of “strangling” or capturing the underlying asset’s price between two option positions. Indian traders frequently employ strangles during volatile market periods or ahead of major events like budget announcements, RBI policy decisions, or corporate earnings releases.

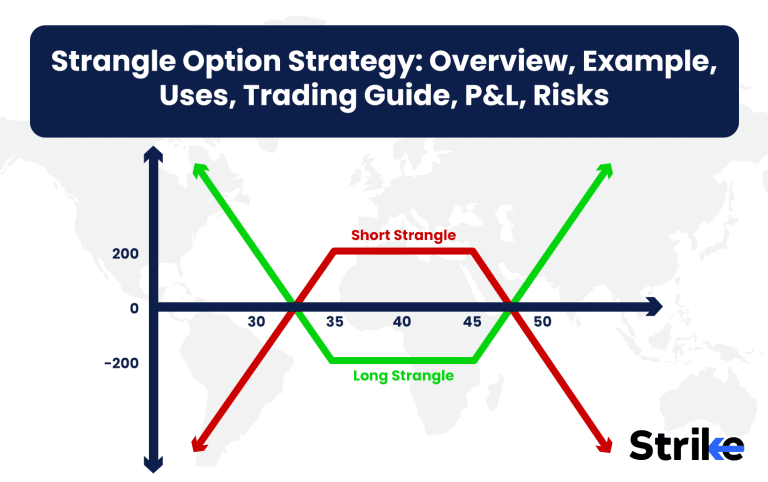

Strangles exist in two forms: long and short. A long strangle involves buying both options, benefiting from substantial price swings and offering unlimited profit potential with limited risk (premium paid). A short strangle involves selling both options, profiting when prices remain relatively stable and collecting the premium, but exposing the trader to potentially unlimited losses.

How Does a Strangle Work?

Strangle functions by positioning a trader to profit from significant price volatility regardless of market direction through the simultaneous purchase or sale of out-of-the-money put and call options. Strangle execution begins with selecting an underlying asset expected to experience substantial price movement, then identifying appropriate strike prices that sit above (for calls) and below (for puts) the current market price.

Consider an investor implementing a long strangle on Adani Ports trading at ₹950. They purchase a ₹1,000 call option for ₹20 and an ₹900 put option for ₹15, creating a total investment of ₹35 per share. The strategy becomes profitable if Adani Ports moves above ₹1,035 or below ₹865 before expiration.

The mechanics depend on whether the position is long or short. Profits increase, in a long strangle, as the underlying asset moves farther from the initial price, with potentially unlimited gains. The maximum loss equals the combined premium paid if the asset price remains between strike prices at expiration.

Short strangles work inversely – the seller collects premiums upfront and profits most when the asset price stays between strike prices, causing both options to expire worthless. However, short strangles expose the trader to unlimited risk if prices move dramatically.

Long Strangle

A long strangle involves buying an out-of-the-money call option and an out-of-the-money put option on the same underlying asset with identical expiration dates but different strike prices. This strategy positions traders to profit from significant price movements in either direction while limiting potential losses to the premium paid.

Traders implement long strangles when anticipating substantial volatility but remain uncertain about directional bias. For example, an investor expecting Bharat Forge to make a big move around earnings might purchase a ₹950 call for ₹12 and an ₹850 put for ₹10 while the stock trades at ₹900.

The maximum profit becomes theoretically unlimited as the underlying asset moves dramatically higher or lower. Breakeven points exist at the call strike plus premium paid (upside) and put strike minus premium paid (downside). The strategy suffers from time decay, working against the position as expiration approaches.

Long strangles perform best during periods of increasing volatility or before major market-moving events. Success depends on the underlying asset moving sufficiently to offset the cost of both options before expiration occurs.

Short Strangle

A short strangle involves selling an out-of-the-money call option and an out-of-the-money put option on the same underlying asset with identical expiration dates but different strike prices. This strategy generates immediate income through premium collection and profits most when the underlying asset remains between the strike prices until expiration.

Traders employ short strangles when expecting minimal price movement or declining volatility. For instance, a trader anticipating Ashok Leyland to trade sideways after recent consolidation might sell a ₹180 call for ₹8 and a ₹150 put for ₹7 while the stock trades at ₹165, collecting ₹15 per share upfront.

The maximum profit equals the total premium received when both options expire worthless. Breakeven points occur at the call strike plus premium received (upside) and the put strike minus premium received (downside). Risk becomes theoretically unlimited if the asset moves dramatically in either direction, potentially triggering substantial losses exceeding the collected premium.

Short strangles benefit from time decay, as each passing day erodes option value when other factors remain constant. Successful implementation requires careful risk management, including setting appropriate strike prices and potentially using stop-loss orders to limit potential damage from adverse price movements.

Why Use a Strangle Strategy?

Traders employ strangle strategies to capitalize on expected volatility without committing to a directional bias in markets where significant movement appears likely but direction remains uncertain. This approach enables participation in potentially dramatic price swings while defining maximum risk in long positions.

Strangles offer economic efficiency compared to straddles, requiring less capital outlay since both options begin out-of-the-money with lower premiums. Traders frequently deployed strangles on Nifty options, during India’s general elections to profit from anticipated volatility without predicting political outcomes.

The strategy proves particularly valuable during earnings seasons when companies like Dixon Technologies or Zomato might experience substantial moves based on results versus expectations. Similarly, traders utilize strangles ahead of RBI monetary policy announcements or Union Budget presentations that historically trigger market volatility.

Short strangles generate income, for investors holding significant stock positions, through premium collection during sideways market phases. This enhances portfolio yield while defining potential entry and exit points if assigned.

Strangles adapt well to changing market conditions through adjustments like rolling positions, adding contracts in favorable directions, or closing losing sides. They accommodate various risk tolerances through strike price selection—wider spreads reduce cost but require larger movements for profitability.

Traders appreciate the strategy’s defined risk parameters in long positions and leverage advantages, allowing control of substantial notional value with relatively modest capital deployment. This creates opportunities for asymmetric returns during volatile market episodes.

When to Use a Strangle?

Traders deploy strangles most effectively during periods preceding anticipated high-impact events likely to generate significant market volatility without clear directional bias.

Quarterly results announcements present ideal opportunities, especially for companies with histories of substantial post-earnings price moves like PVR-Inox or Zydus Life Sciences.

Economic data releases significantly impacting markets create favorable conditions for strangle implementation. The Union Budget, IIP data, inflation reports, and RBI policy decisions historically trigger major market movements, making these periods strategically advantageous for strangle positioning.

Corporate actions including merger announcements, regulatory decisions, or major product launches generate the uncertainty and volatility conducive to successful strangle trading. Sectors experiencing disruption or regulatory shifts, such as recent developments in Indian telecom or pharmaceutical industries, offer fertile ground for this strategy.

Technical chart patterns indicating consolidation before breakouts create opportune entry points. Symmetrical triangles, wedges, and rectangle patterns frequently precede significant directional moves but don’t necessarily predict direction, aligning perfectly with strangle benefits.

How Option Greeks Affect Strangle?

Option Greeks directly influence strangle performance by quantifying how various factors impact option prices and overall position value throughout the trade lifecycle. Delta measures directional exposure, with long strangles starting delta-neutral but becoming increasingly positive or negative as the underlying moves, creating automatic adjustment as market conviction develops.

Theta represents the constant adversary for long strangle holders, continuously eroding option value as expiration approaches. A typical Nifty long strangle loses approximately 5-8% of its value weekly through time decay alone during normal volatility periods, accelerating in the final two weeks before expiration.

Vega emerges as the long strangle’s greatest ally, increasing position value during volatility expansions. Many Indian equity strangles gained 30-40%, during the 2022 Russia-Ukraine conflict, purely from volatility spikes before directional moves even materialized. Conversely, short strangles benefit from volatility contractions after major announcements.

Gamma accelerates delta changes as prices approach strike prices, magnifying profits in winning scenarios for long strangles. This creates a self-reinforcing momentum effect, particularly valuable during trending markets following breakouts from consolidation patterns.

Effective strangle management requires understanding these interrelationships. Professional traders actively monitor all Greeks rather than focusing exclusively on price movement. For example, position sizing based on vega exposure rather than simply contract quantity helps standardize volatility risk across different underlying assets.

What are the Maximum Profit & Loss, Breakeven on a Strangle?

Maximum profit for a long strangle reaches theoretically unlimited levels as the underlying asset moves dramatically higher or lower beyond breakeven points, while short strangles cap maximum profit at the total premium received when both options expire worthless. The profit potential increases proportionally with the magnitude of price movement in either direction for long positions.

Maximum loss for long strangles equals the combined premium paid for both options, occurring when the underlying price remains between strike prices at expiration. Short strangles face theoretically unlimited losses if prices move significantly beyond breakeven points, potentially far exceeding the premium collected.

Breakeven points calculation involves two separate price levels. The upside breakeven equals the call strike price plus the total premium paid (for long) or received (for short). The downside breakeven equals the put strike price minus the total premium paid (for long) or received (for short).

Consider a Wipro long strangle with shares at ₹450: buying a ₹480 call for ₹8 and a ₹420 put for ₹7 creates a total cost of ₹15. The upside breakeven becomes ₹495 (480 + 15), while the downside breakeven equals ₹405 (420 – 15). The strategy generates profits if Wipro moves above ₹495 or below ₹405 before expiration.

What are the Risks of Strangle?

The primary risk of a long strangle involves losing the entire premium paid when the underlying asset fails to move significantly before expiration, resulting in both options expiring worthless. This scenario occurs frequently during periods of unexpected market consolidation or when anticipated catalysts produce muted reactions.

Time decay aggressively erodes long strangle value, accelerating as expiration approaches. A typical Nifty long strangle loses approximately 5-7% weekly through theta decay alone, creating a constant headwind against profitability that intensifies dramatically in the final two weeks of the option’s life.

Implied volatility collapse devastates long strangle positions regardless of price movement direction. Implied volatility frequently decreases 30-40% overnight, following events like earnings announcements, causing substantial value erosion even when the underlying moves favorably but insufficiently to overcome this effect.

Short strangles expose traders to potentially catastrophic losses exceeding account value during black swan events or gap movements. The 2020 pandemic market crash saw many short strangle positions on Indian indices facing losses exceeding 500% of the initial premium received.

Execution risk emerges from wide bid-ask spreads in less liquid Indian options, particularly on individual stocks outside the top 50 by market capitalization. These spreads reduce potential profitability through unfavorable entry and exit prices, sometimes exceeding 10-15% of the option value

Is Strangle Strategy Profitable?

Yes, strangle strategies generate consistent profits for traders who accurately identify high-volatility periods and properly manage position sizing and exit timing.

Profitability depends heavily on entry timing relative to volatility cycles and catalyst events. Long strangles implemented during low implied volatility periods preceding significant announcements historically outperform those placed during already elevated volatility environments. Short strangles perform best following volatility spikes when mean reversion typically occurs.

Is Strangle Bullish or Bearish?

A strangle strategy takes a market-neutral stance rather than expressing bullish or bearish directional bias. The strategy positions traders to profit from significant price movement regardless of direction, focusing instead on the magnitude of the move rather than predicting market direction.

Traders implement strangles precisely when uncertain about future price direction but confident about increased volatility. This market-neutral characteristic distinguishes strangles from directionally biased strategies like vertical spreads or naked options. Strike price selection remains symmetrical around the current price in pure strangles, though traders sometimes adjust strike distances to reflect slight directional preferences while maintaining the strategy’s fundamental non-directional nature.

What are Alternatives to Strangle Strategy?

Alternative strategies to strangles mainly include straddles, which involve buying or selling at-the-money call and put options with identical strike prices and expiration dates. Straddles require smaller price movements to become profitable but cost more to establish, making them suitable when expecting significant volatility with greater certainty.

Iron condors create another alternative by combining a short strangle with further OTM long options, limiting maximum loss potential while reducing potential profit. This strategy benefits from time decay while defining maximum risk, particularly valuable for Indian retail traders with limited capital facing SEBI’s strict margin requirements.

Butterfly spreads offer neutral positioning with defined risk-reward characteristics by using three strike prices and four total options. These complex structures profit from minimal price movement but provide significantly reduced capital requirements compared to short strangles.

Calendar spreads present another alternative where traders sell near-term options while buying longer-dated options at identical strikes. This approach capitalizes on accelerated time decay of near-term options while maintaining exposure to potential later movements, effective during temporary volatility spikes.

Ratio spreads create alternative asymmetric exposures by purchasing options at one strike while selling multiple contracts at further OTM strikes, generating income while maintaining directional exposure. These provide more cost-effective volatility exposure than pure long strangles but introduce directional risk.

Which is better, straddle or strangle?

Neither strategy universally outperforms the other as each serves different market scenarios and trader objectives. Straddles provide greater sensitivity to smaller price movements since both options start at-the-money, making them superior when expecting moderate volatility or when probability of movement exceeds directional certainty.

Strangles offer economic efficiency through lower initial cost, requiring approximately 30-40% less capital outlay than comparable straddles on Indian indices. This capital efficiency creates superior percentage returns when substantial moves occur. The structure provides wider breakeven points, reducing the impact of minor price fluctuations while maintaining unlimited profit potential during extreme moves typically seen around major economic announcements or unexpected corporate developments.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 20")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 21")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 22")

: Overview, 10 Types of Indicators, Settings for Different Markets 24")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 26")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 30")

No Comments Yet.