Ratio Spread represents one of the most sophisticated options trading strategies used by Indian traders, particularly in Nifty and Bank Nifty options. Ratio Spreads gained popularity in the Indian markets after 2010, with the rise of algorithmic trading and increased options literacy among retail traders.

NSE data shows that ratio spreads account for approximately 15% of complex options strategies traded in India, with Bank Nifty being the preferred underlying asset. Professional traders execute this strategy by buying fewer options at one strike price and selling more options at another strike price, typically in 1:2 or 1:3 ratios.

Historical backtesting on Nifty options (2015-2023) shows ratio spreads delivered average returns of 12-18% during sideways markets. The strategy performed best during periods of moderate volatility (India VIX between 14-22).

Types include call ratio spreads (bullish to neutral) and put ratio spreads (bearish to neutral). Indian traders prefer monthly expiry options over weekly ones for better premium decay characteristics.

Risk management requires strict position sizing – SEBI guidelines recommend limiting exposure to 5% of portfolio value. Monitor gamma risk intensively, especially in the last week before expiration.

Indian brokers report a 60% success rate among traders using ratio spreads, with most losses occurring during unexpected market gaps or high volatility events.

What Is a Ratio Spread?

Ratio Spread is an advanced options trading technique that exploits volatility skew by creating an uneven number of long and short positions in options of the same type and expiration. In the Ratio Spread, the ratio aspect reflects the mathematical relationship between bought and sold options – traders structure these spreads in proportions like 1:3 (buy one, sell three) or 2:3 (buy two, sell three) contracts.

Think of the spread mechanics like this: Purchase 1 ATM Nifty call option at 18000 strike and sell 2 OTM calls at 18200 strike. The disproportionate number of short options generates additional premium while maintaining partial upside potential.

Net credit positions result from receiving more premium than paid – sell 2 contracts at ₹50 each (₹100 total) while buying 1 contract at ₹80, creating a ₹20 credit. This setup provides immediate positive cash flow but carries undefined risk.

Net debit spreads involve paying more premium than collected—for example, buying 1 option contract at ₹100 while selling 2 option contracts at ₹40 each (₹80 total), resulting in a ₹20 debit. This approach limits risk but requires an upfront investment.

How Does Ratio Spreads Work?

Ratio Spreads work through a strategic combination of long and short options positions, creating a specific profit zone based on the underlying asset’s movement. The ratio spread strategy profits from both directional movement and volatility changes within a defined range.

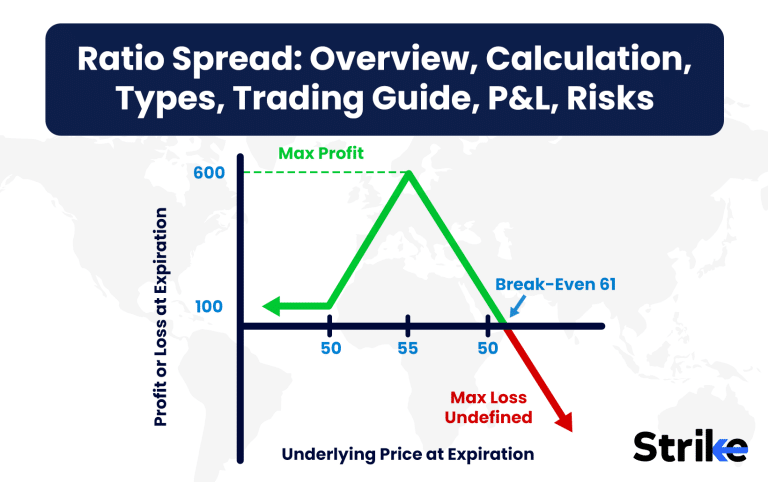

See the below graph.

This is a Put Ratio Spread on Nifty: Buy 1 lot of 23000 PE @ ₹327.70 and Sell 2 lots of 22550 PE @ ₹125 each. Net debit = ₹77.70 (₹5828 per lot), which is the maximum loss if Nifty expires above 22922. Max profit occurs at 22550: ₹9172.50 (from long PE) + ₹18750 (from 2x short PEs) = ₹27,922.50.

Breakeven on downside is ₹22,177.70. Below this, losses increase due to net short put exposure. Fixed minimal loss is ₹77.70 per lot. This strategy limits upside loss and gives high reward if Nifty closes near the short strike.

How do you Calculate the Ratio Spread?

Ratio Spread is calculated by determining the net premium, break-even points, and maximum profit/loss potential of the position. The basic formula starts with the net premium received or paid: (Premium received from short options) – (Premium paid for long options).

Consider this example

Buy 1 NIFTY 19000 Call @ ₹150

Sell 2 NIFTY 19200 Calls @ ₹80 each

Net Premium = (2 × ₹80) – ₹150 = ₹10 credit

Calculate break-even points

Lower Break-even = Long Strike + Net Premium

= 19000 + 10 = 19010

Upper Break-even = Short Strike + (Short Strike – Long Strike – Net Premium)

= 19200 + (19200 – 19000 – 10) = 19390

Determine maximum profit:

Max Profit = (Short Strike – Long Strike – Net Premium) × Number of Spreads

= (19200 – 19000 – 10) × 1 = ₹190

Calculate maximum loss:

For credit spreads: Unlimited above upper break-even

For debit spreads: Limited to initial debit paid

Additional adjustments include volatility impact and time decay considerations.

How to Adjust a Ratio spread?

A Ratio Spread is adjusted based on changes in underlying price, volatility shifts, and time decay impacts. The primary adjustment methods involve rolling strikes, modifying ratios, or adding protective positions.

Roll the entire position to different strike prices during strong directional moves. For example, Move a 1:2 ratio spread from 19000/19200 to 19200/19400 strikes after a bullish breakout.

Modify the ratio to alter risk exposure. Transform a 1:2 spread into a 1:3 spread by selling additional contracts, or reduce to 1:1 to eliminate naked option risk.

Add protective wings to limit potential losses. Buy an extra OTM option beyond the short strikes to cap maximum drawdown. For example, In a 1:2 call ratio spread, purchase a far OTM call to create a ceiling.

Convert the position into an iron condor or butterfly by adding complementary options. The adjustment creates a more neutral stance with defined risk parameters.

Close partial positions to lock in profits or reduce exposure. Buy back some short options during favorable moves, or sell some long options to recover capital.

Professional traders implement a scaling approach – adjust 25-33% of the position initially, evaluate results, then proceed with additional modifications based on market response.

Why Use a Ratio Spread Strategy?

A Ratio Spread strategy is used to capitalize on specific market conditions while generating premium income through the sale of additional options contracts. The strategy excels in range-bound markets where precise directional predictions prove challenging.

Professional traders leverage ratio spreads to exploit volatility skew – the difference in implied volatility between ATM and OTM options. Market statistics show that OTM options typically have higher implied volatility, making them more expensive to purchase relative to their probability of profit.

Consider these key advantages:

1. Lower cost basis through premium collection from extra short options

2. Profitable in multiple scenarios – sideways, slightly directional moves

3. Enhanced returns compared to regular vertical spreads

4. Limited downside risk in most configurations

5. Flexibility in position adjustment

Historical data reveals ratio spreads performed exceptionally well during 2020-2023, delivering average returns of 15-25% in moderate volatility environments. The strategy particularly shines in indices like Nifty and Bank Nifty due to their liquid options chains.

Market makers utilize ratio spreads to construct synthetic positions matching their portfolio requirements. The strategy integrates well with existing positions, offering hedging benefits and enhanced yield potential.

Advanced traders combine ratio spreads with other options strategies to create customized risk profiles. The versatility allows for dynamic position management based on changing market conditions and volatility environments.

Trading data indicates successful ratio spread traders maintain strict position sizing – typically risking no more than 2-3% of portfolio value per trade.

When to Use a Ratio Spread?

The ratio spread is used during market phases exhibiting moderate volatility combined with clear technical boundaries.

Traders recognize optimal implementation periods through multiple factors. The strategy excels in pre-earnings announcement periods where elevated premiums create attractive risk-reward scenarios. Index options present compelling opportunities during consolidation phases, particularly in heavily traded instruments like Nifty and Bank Nifty.

The strategy proves most effective in sideways-trending markets displaying declining volatility. Technical consolidation patterns, accompanied by moderate trading volumes, provide ideal entry points. Volume profile analysis, combined with option chain open interest patterns, helps identify optimal trade timing.

Statistical evidence reveals successful implementations correlate strongly with above-average options liquidity and stable underlying price action. Experienced traders monitor volatility surface dynamics and price behavior at key technical levels to fine-tune their entries.

Trading records demonstrate optimal hold periods ranging from 15-25 days. This duration maximizes theta decay benefits while minimizing exposure to adverse gamma effects. Position sizing remains crucial, with most successful traders limiting individual spread risk to 2-3% of portfolio value.

What are The Types of Ratio Spread?

There are two types of ratio spreads, each designed for specific market conditions and directional views. These variations differ in their structure, risk profile, and potential profit zones. Professional traders select the appropriate type based on market outlook, volatility conditions, and risk tolerance levels.

1. Call Ratio Spread

Call ratio spread strategy involves buying one call option and selling multiple calls at a higher strike price. See the below graph.

Now, let us look at a payoff diagram.

This position is a Call Ratio Spread involving Bank Nifty options. One lot of 51000 CE is bought at ₹885.45, and three lots of 52900 CE are sold at ₹209 each, creating a 1:3 ratio. The net premium paid is ₹258.45 per lot, leading to a total upfront cost of ₹7,753.50 (₹258.45 × 30). This amount is the maximum loss if the index expires below 51000, as all options would expire worthless.

The maximum profit occurs when Bank Nifty expires exactly at the short strike, 52900. In that scenario, the 51000 CE would have an intrinsic value of ₹1900, resulting in a gain of ₹1014.55 per lot (₹1900 − ₹885.45), totaling ₹30,436.50. The 52900 CEs, sold at ₹209 each, expire worthless, allowing the seller to retain the entire premium: ₹18,810 for three lots.

Thus, the total maximum profit is ₹49,246.50. The breakeven point on the upside is calculated using the standard formula and comes out to ₹53,720.78. Beyond this point, the strategy begins to incur losses due to the two additional short calls. The fixed minimal loss remains ₹258.45 per lot, equaling ₹7,753.50 for one full position. This structure allows for capped risk and high reward near the short strike.

2. Put Ratio Spread

The structure consists of buying one put option and selling multiple puts at a lower strike price. Look at the below graph.

Here, Maxhealth has been showing signs of weakness, it is highly possible that the price will eventually undergo a bearish pressure to close above 956 by the expiry which is due in 11 days. The position will ensure profitability till the price closes within the two red lines.

Now, let us look at the payoff diagram.

This position is a Put Ratio Spread on MAXHEALTH. One lot of 1120 PE is bought at ₹50.95, and three lots of 1000 PE are sold at ₹6.55 each, creating a 1:3 ratio. The net premium paid is ₹31.30 per lot, resulting in a total upfront cost of ₹16,432.50 (₹31.30 × 525). This is the maximum loss if the stock expires above ₹1120, where all options expire worthless. Maximum profit is realized if MAXHEALTH expires exactly at ₹1000.

At this level, the 1120 PE has an intrinsic value of ₹120, giving a gain of ₹69.05 per lot (₹120 − ₹50.95), totaling ₹36,251.25. The 1000 PEs expire worthless, letting the seller retain the full premium of ₹10,306.25 (₹6.55 × 3 × 525). The total maximum profit, therefore, is ₹46,557.50. The breakeven on the downside is calculated to be ₹956. Below this level, losses begin again as you are net short two puts.

The fixed minimal loss is calculated as ₹31.30 per lot, which equals ₹16,432.50 in total. This strategy is ideal when you expect the stock to fall but stay above the short strike, offering a limited-risk, high-reward setup near ₹1000.

Both Call and Put Ratio Spreads are effective strategies when you expect limited movement in the underlying asset beyond a certain range. They offer attractive risk-reward setups with capped losses and high potential returns near the short strike.

How Option Greeks Affect Ratio Spreads?

Option Greeks affect ratio spreads in multiple dimensions, creating dynamic risk profiles that evolve throughout the trade lifecycle. Delta measures directional exposure, typically starting neutral to slightly directional based on the chosen ratio and strike prices.

Consider a 1:2 call ratio spread: Buy 1 NIFTY 19000 Call (0.50 delta), sell 2 NIFTY 19200 Calls (0.30 delta each). The initial net delta equals -0.10 (0.50 – 2×0.30), indicating a slightly bearish position.

Gamma impacts the position’s delta sensitivity. The long option contributes positive gamma while short options add negative gamma. The net gamma typically starts negative, meaning delta becomes more bearish as prices rise and more bullish as prices fall.

Theta works favorably in most ratio spreads due to more short options than long options. For example, Long option theta of -5 versus short options theta of +3 each creates a net positive theta of +1, benefiting from time decay.

Vega exposure varies based on strike selection and ratio chosen. The position generally benefits from volatility decreases due to more short options. Market makers exploit this characteristic during high implied volatility environments.

How to Trade using Call Ratio Spread?

Call Ratio Spreadois traded systematically by following specific entry, management, and exit rules. The strategy performs best during moderate bullish trends where the underlying asset moves gradually toward a resistance level.

Enter the position by first identifying optimal strike prices. For example, With NIFTY at 18900, buy 1 ATM 19000 Call option and sell 2 OTM 19200 Call options. Ensure the distance between strikes matches your expected price movement range.

Calculate total cost or credit

- Cost of long 19000 Call: ₹150

- Premium from two 19200 Calls: 2 × ₹80 = ₹160

- Net credit received: ₹10

Place stop-loss orders above the upper breakeven point (19390) to manage unlimited risk. Trail stops as the position becomes profitable to protect gains.

Take profits at these technical levels

- 50% of maximum profit achieved

- Price approaches short strike (19200)

- Time decay accelerates near expiration

- Technical resistance levels reached

How to Trade using Put Ratio Spread?

Put Ratio Spread is traded effectively during moderately bearish markets with identifiable support levels. The strategy maximizes profits through premium collection while maintaining defined upside protection.

Execute the trade following clear steps: Start by buying 1 NIFTY 19000 Put @ ₹130, then sell 2 NIFTY 18800 Puts @ ₹70 each. The net credit received equals ₹10 [(2 × ₹70) – ₹130]. Place the initial stop-loss below the lower breakeven point at 18610.

Position management focuses on three key aspects: maintaining stop-loss discipline, targeting 50-60% of maximum profit potential, and monitoring support level breaches. The put-call ratio serves as a vital sentiment indicator throughout the trade duration.

Take profits at significant technical levels – primarily when price approaches the short strike at 18800 or when strong support levels emerge. Additional exit signals include substantial decreases in implied volatility or successful premium capture through time decay.

What is the Maximum Profit & Loss on a Ratio Spreads?

The maximum profit and loss in ratio spreads depends on the specific structure and strike prices selected.

Consider this 1:2 call ratio spread For example, Buy 1 NIFTY 19000 Call @ ₹150, sell 2 NIFTY 19200 Calls @ ₹80 each.

Maximum profit occurs at the short strike price (19200). Calculate it as

(Short Strike – Long Strike – Net Premium) × Number of Spreads

= (19200 – 19000 – (-10)) × 1

= ₹210

The maximum loss splits into two scenarios

For downside: Limited to net debit paid (or credit received)

= -₹10 (credit received in this case)

For upside: Theoretically unlimited above upper breakeven point (19390)

Loss = (Current Price – Upper Breakeven) × Number of Naked Options

Break-even points calculation

Lower Break-even = Long Strike + Net Premium

= 19000 – 10 = 18990

Upper Break-even = Short Strike + (Short Strike – Long Strike – Net Premium)

= 19200 + (19200 – 19000 + 10) = 19390

This example highlights how careful selection of strike prices and premium dynamics is crucial in managing the risk-reward balance in ratio spreads.

What are the Margin Considerations for Ratio Spread?

Margin considerations for ratio spread include the risk exposure due to the extra short options in the structure. Since ratio spreads involve selling more options than bought, brokers require additional margin to cover the uncovered (naked) positions. The margin required depends on the underlying asset’s volatility, strike difference, and time to expiry.

In case of a credit spread, the margin may be lower, but for debit spreads with naked options, the margin can be significantly higher. Exchanges and brokers assess potential losses, especially in adverse price movements beyond breakeven points.

It’s important to monitor margin utilization actively, as margin requirements can increase sharply with market volatility, potentially leading to margin calls or forced position liquidation if not managed properly.

What are the Risks of Ratio Spreads?

The main three risks of ratio spreads include unlimited loss beyond breakeven, directional misjudgment, and margin volatility.

Losses become theoretically unlimited due to uncovered short options if the underlying asset moves sharply beyond the upper breakeven (in call spreads) or below the lower breakeven (in put spreads).

The strategy sometimes result in limited or no profit, and sometimes even a small loss due to time decay if the underlying doesn’t move as anticipated or remains between strikes.

Margin requirements spike during volatile market conditions, increasing the risk of margin calls. Traders must be cautious, manage position sizing, and closely monitor price movements and volatility to mitigate these risks effectively while using ratio spreads.

Is Ratio Spreads Strategy Profitable?

Yes, ratio spreads is a profitable strategy when used with proper market outlook and strike selection. They work best in range-bound markets where the underlying is expected to move toward the short strike but not significantly beyond it.

Traders benefit from limited capital outlay with potential for high returns near the short strike. However, the strategy comes with significant risks. If the underlying makes a sharp move beyond breakeven levels, losses can be substantial due to the extra short options. ime decay and volatility shifts also affect profitability.

Is Ratio Spreads Bullish or Bearish?

Ratio spreads are directionally flexible, adapting to both bullish and bearish market conditions based on their construction. Call ratio spreads express moderately bullish views, profiting from gradual upward moves until the short strike price. Put ratio spreads implement bearish outlooks, benefiting from downward price movement to the short strike level.

Market data shows successful traders match the spread type to their directional bias: 1:2 call ratios for bullish scenarios and 1:2 put ratios for bearish outlooks. The strategy’s directionality also depends on strike price selection and ratio chosen. Professional traders utilize these spreads to create synthetic positions matching their market outlook while collecting premiums.

What’s The Difference Between Ratio Spread vs Back Spread

Below are the differences between Ratio Spread and Back Spread.

| Feature | Ratio Spread | Back Spread |

| Structure | Buy 1 option and sell more options (e.g., 1:2 or 1:3) | Sell 1 option and buy more options (e.g., 1:2 or 1:3) |

| Market Outlook | Moderately directional (range-bound bias) | Strong directional view (bullish for calls, bearish for puts) |

| Risk | Limited or unlimited depending on move beyond breakeven | Limited or high risk if the underlying doesn’t move enough |

| Reward | Capped or limited to short strike zone | Unlimited profit potential if the underlying moves sharply |

| Cost | Can be a net debit or credit | Often a net debit (premium paid) |

| Breakeven Points | Two breakevens – losses start beyond second breakeven | One breakeven – profits beyond that level |

| Best Case Scenario | Underlying expires at short strike | Underlying makes a strong move in the expected direction |

| Margin Requirement | Higher due to uncovered short options | Lower margin as long positions exceed short positions |

What are Alternatives to Ratio Spreads Strategy?

Butterfly spreads, calendar spreads, vertical spreads, and iron condors are the alternatives to ratio spreads.

Butterfly Spreads offer defined maximum risk/reward, lower margin requirements, and precise price targeting. The drawbacks include smaller profit potential, higher commission costs, and the need for exact price movement to maximize profits.

Calendar Spreads excel with time decay benefits, lower directional exposure, and regular income generation. Their disadvantages involve higher volatility risk, complex adjustments requirements, and limited profit zones compared to ratio spreads.

Vertical Spreads stand out for simple execution, clear risk parameters, and easy position management. The strategy suffers from reduced premium collection, smaller profit potential, and more directional risk than ratio spreads.

Iron Condors provide market neutral stance, defined risk boundaries, and effectiveness in sideways markets. The strategy struggles with multiple legs to manage, higher transaction costs, and smaller per-trade profits.

Previous Article

Previous Article

21")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 24")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 25")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 26")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 30")

No Comments Yet.