Theta decay steadily erodes an option’s value as time passes, impacting both calls and puts. Theta decay is most severe for at-the-money contracts, especially as expiry approaches. As the expiration date nears, the chance for a significant price move drops, causing time value to disappear rapidly.

Option sellers, particularly in short-term trades, profit from this effect, while buyers must overcome constant value loss. Strategies like covered calls, iron condors, and credit spreads are designed to benefit from theta decay. While theta decay cannot be avoided, traders can manage or exploit it for consistent and controlled returns.

What Is Theta Decay in Options Trading?

Theta decay is the process by which an option loses value as time passes, specifically representing the reduction in its extrinsic or “time” value each day until expiration. In options trading, every contract has a finite lifespan, and the probability of a profitable move in the underlying asset decreases as expiration gets closer. This diminishing opportunity is reflected in the premium you pay or receive for an option.

Theta is one of the five main “Greeks” used by traders to measure risk and reward in options trading. It quantifies how much the price of an option will fall due to the passage of a single day, assuming everything else remains constant. For example, if a call option has a theta of –3, its premium will drop by Rs. 3 every day, all else being equal.

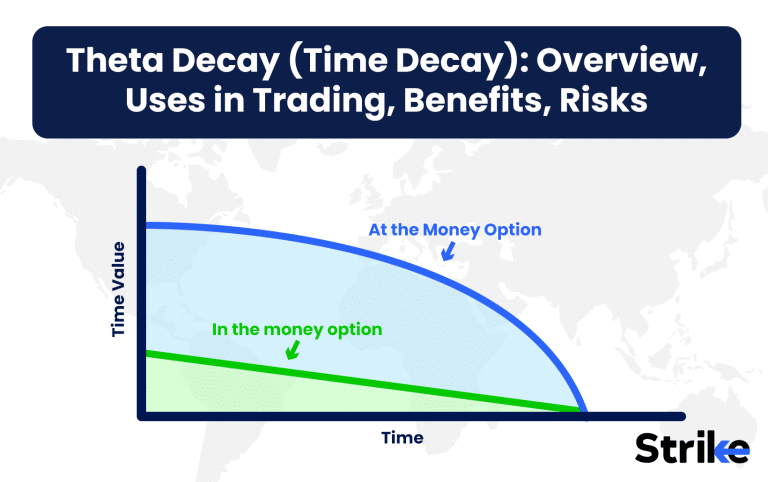

This daily loss is most significant for options that are at-the-money (ATM), where the likelihood of moving in-the-money (ITM) or out-of-the-money (OTM) is highest and uncertainty is greatest. As expiration approaches, the time value decays faster, meaning options lose value at an accelerating rate.

Why Does Theta Decay Happen?

Theta decay happens because options lose their time value as their expiration date approaches, reflecting the shrinking window for a profitable price move in the underlying asset. The price of an option consists of intrinsic value (if any) and extrinsic value, which is mainly time value and volatility premium.

- Relationship with Expiration: The closer an option is to expiry, the less time remains for the underlying asset to experience a significant move. As a result, the probability of a dramatic price change falls, and so does the value of the option’s time component.

- Time Value in Pricing: Early in an option’s life, time value is high because there is a greater chance for large price swings. As time passes, that chance diminishes, leading to a steady but accelerating loss in extrinsic value.

- Impact on OTM, ITM, ATM: At-the-money options experience the fastest time decay because they are closest to being profitable or worthless with small price moves. OTM options decay as the likelihood of finishing ITM drops. Deep ITM options retain more value, but their time value also dissipates.

- Volatility’s Role: High implied volatility increases time value and partially resists theta decay. When volatility is low, theta’s effect is more pronounced and options lose value faster.

A graph of theta decay would show a slow decline in option value when far from expiration, steepening dramatically in the final weeks, especially for ATM options. This curve visually demonstrates how theta accelerates as the deadline approaches, making time management essential in all option strategies.

How Does Theta Decay Impact Options Pricing?

Theta decay steadily erodes the market value of all options, but its impact is greatest on short-term, at-the-money contracts and is felt differently by buyers and sellers. For buyers, theta is a hidden cost that reduces the likelihood of profit as time passes. For sellers, it is a source of income, as the option’s premium declines in their favor.

- Effects on Value: As expiration nears, an option’s extrinsic value drops sharply. An option with 30 days left loses time value slowly, but in the final week, daily losses become significant—sometimes Rs. 5–10 per day for liquid ATM contracts.

- Short vs. Long Positions: Long positions suffer from theta decay, requiring a strong price move to remain profitable. Short positions benefit, as every day without a big move increases the chance of keeping the premium.

- Variation by Expiry: Longer-dated options have lower theta and lose value slowly. Short-term contracts exhibit high theta, especially in the last ten days.

- Strategy Impact: Buyers of options need the underlying to move quickly in the favorable direction to overcome theta loss. Sellers can profit from sideways or range-bound markets by collecting premium as theta eats away at the contract value.

- Example: A Rs. 60 call option with a theta of –4 will lose Rs. 4 each day if the underlying price and volatility remain stable. In five days, the option could be worth Rs. 40 even if the stock price does not move.

Theta decay is a crucial consideration for every options strategy, influencing which contracts to buy or sell and when to exit a trade.

How to Use Theta Decay in Option Trading?

Let us understand how to use theta decay in option tradings through an example. You can observe Theta values directly in an option chain. For instance, at the 25450 strike.

: Overview, Uses in Trading, Benefits, Risks 7")

- For 03 JUL 2025 expiry: Theta ≈ –31.45

- For 10 JUL 2025 expiry: Theta ≈ –8.39

- For 17 JUL 2025 expiry: Theta ≈ –5.61

- For 24 JUL 2025 expiry: Theta ≈ –4.46

This shows that nearer expiries have higher daily time decay, while farther expiries decay more slowly but last longer.

For taking advantage of rapid time decay, selling options close to expiry is effective. For example, selling a 25450 CE or PE for the 03 JUL expiry gives you a Theta of about –31.45 per day. That means the premium can drop quickly—sometimes in a few hours—especially if the price stays near the strike.

: Overview, Uses in Trading, Benefits, Risks 8")

This is a classic short straddle or expiry-day trade, where the goal is to profit from rapid premium erosion. However, if the underlying asset makes a big move, losses can outweigh Theta gains. In such cases, hedging becomes essential.

Theta can also be used in a calendar spread, where you sell the near-term option with higher Theta and buy a longer-term option with lower Theta.

: Overview, Uses in Trading, Benefits, Risks 9")

Example setup

- Sell 25450 CE (03 JUL expiry) → Theta ≈ –31.45

- Buy 25450 CE (10 JUL expiry) → Theta ≈ –8.39

This creates a net Theta of –23.06 per day in your favor. If the price stays near 25450, the short leg decays faster, giving you profit, while the long leg decays slowly and provides Vega protection in case of a volatility spike or directional move.

How to Profit from Theta Decay in Options Trading?

Profiting from theta decay requires selling options or option spreads and collecting premium as time value erodes, particularly in calm or range-bound markets. Sellers position themselves to benefit from the natural decline in extrinsic value, often targeting short-term contracts where theta is most rapid.

- Covered Calls: Hold the underlying stock and sell call options, earning premium as time passes.

- Iron Condors: Sell both OTM calls and puts, profiting if the stock stays within a defined range.

- Credit Spreads: Sell a higher-premium option and buy a lower-premium one for protection, limiting risk.

- Selling Puts: Collect premium by selling OTM puts, especially effective if the underlying is stable or rising.

- Short Straddles/Strangles: Sell both ATM calls and puts to maximize theta, suitable for very stable markets.

The wheel strategy for premium income also benefits from theta decay because it repeatedly sells cash-secured puts and covered calls to collect option premium.

Theta is highest in the final 30 days before expiry, making short-term option selling strategies more profitable. For example, selling a weekly Rs. 80 call with a theta of 6 could yield Rs. 30–40 in time decay over five days if the stock price stays flat.

How to Benefit From Theta Decay in Options Trading?

The best way to benefit from theta decay is to sell options—especially those with short expiries—so that time works in your favor and premium is collected as options lose value. This approach is particularly effective in neutral or mildly bullish/bearish markets.

- Selling Options: Covered calls, naked puts, and short iron condors are popular because they generate income as time passes.

- Time Decay in Neutral/Bearish Strategies: If expecting little movement, strategies like iron condors or credit spreads efficiently capture theta.

- Short-Term Profit: Theta is highest in options with less than 30 days to expiration. Selling weekly or bi-weekly contracts maximizes the benefit.

- Practical Example: Selling a Rs. 120 put option with a theta of 5, if the underlying stays above the strike, Rs. 25–30 could be gained over a week with little price movement.

- Combining Greeks: Smart traders also monitor delta (directional risk) and vega (volatility risk) to ensure their portfolio isn’t overly exposed to unexpected moves or IV spikes.

By consistently selling high-theta options and managing risk, you will be able to create a steady stream of income from time decay, even if the underlying asset hardly moves.

How to Manage Theta Risk in Your Trades?

Managing theta risk means structuring your trades and portfolio so that you aren’t overly exposed to the rapid loss of option value as expiration nears, especially if you hold long positions. Since theta is unavoidable, mitigation and balance are essential.

- Limit Long Option Exposure: Only buy options when a strong, swift move is expected. Hold for short periods.

- Use Spreads: Vertical spreads (buy one, sell another) or calendar spreads (different expiries) help offset theta loss by pairing a long option with a short.

- Select Longer Expiry: Longer-dated options decay more slowly. Buying these limits daily theta loss.

- Portfolio Balance: Hold both short and long options to offset theta risk across positions.

- Adjust or Roll: Close or roll forward long positions as theta accelerates in the final week.

- Risk Management: Always use stop-losses and set profit targets to avoid letting theta erode gains.

For example, a calendar spread profits as the short-dated option decays faster than the long-dated one, keeping your net theta risk in check. Consistently reviewing theta across your trades helps avoid nasty surprises from sudden time value drops.

How Theta Decay Works Across Different Expirations

Theta decay picks up speed as expiration nears, causing short-term options to lose value at a much faster rate than long-term options. This differential decay is a vital consideration for strategy selection and risk management.

- Short-Term Options: In the last 30 days, and especially the final week, theta is highest. ATM weekly options can lose 10–15% of their value daily.

- Long-Term Options: Contracts with 90, 120, or more days to expiry lose value slowly—often less than 1% per day.

- Strategy Adjustment: Sell short-term options to maximize theta decay, or buy longer-term options to minimize time value loss.

- Expiration Date Impact: Expiry selection determines your risk-reward profile. Short-term options offer rapid decay and quick results, but higher risk from small price moves.

- Example: An ATM weekly call could lose Rs. 6–8 per day as expiry approaches, while a six-month ATM call might lose only Rs. 2 per day.

Understanding how theta differs by expiry enables you to fine-tune your trades, using time to your advantage or defending against its risks.

How Theta Decay Differs from Other Greeks?

Theta measures time-based loss in option value, while other Greeks represent different market risks—delta for price movement, gamma for rate of price change, and vega for volatility. Each Greek plays a unique part in an option’s pricing behavior.

- Theta vs. Delta: Delta measures how much an option’s price changes for a Rs. 1 movement in the underlying, while theta measures loss per day.

- Theta vs. Gamma: Gamma shows how much delta will change with price movement. High gamma generally appears near expiry and is often paired with high theta.

- Theta vs. Vega: Vega tracks how much option price changes with 1% change in implied volatility. High vega means the option is sensitive to volatility, which can offset or increase theta decay.

- Trading Impact: A position with high theta and low delta profits from time rather than price movement. Adding vega or delta through other positions balances risk.

- Portfolio Example: A trader might use a short straddle (high theta, low delta) in a calm market and buy vega-rich options when expecting volatility spikes.

Understanding and combining Greeks allows for sophisticated, risk-managed option strategies.

Is Theta Decay the Same for Calls and Puts?

Yes, theta decay affects both call and put options in the same way, eroding time value as expiration approaches, with the greatest impact on at-the-money contracts. Whether you hold a call or a put, if you are long, you lose value to theta every day.

This symmetry in theta’s effect makes time value management crucial for all option buyers.

How Fast Does Time Decay Happen in Options?

Time decay is slow when there’s plenty of time to expiry but becomes much faster in the final month, especially the last week—this effect is sharpest for ATM options. Theta is not linear; it accelerates as expiration nears.

- 90+ Days to Expiry: Decay is slow; options lose only a small percent of value daily.

- 30 Days to Expiry: Decay becomes noticeable; Rs. 2–4 per day loss is common for ATM options.

- 7 Days to Expiry: Decay is rapid; ATM contracts can lose Rs. 5–10 or more daily.

- Half-Life Concept: Roughly half of an option’s time value evaporates in the last third of its life.

A Rs. 40 ATM option with 10 days left could be worth Rs. 20 just five days later without any price movement. This pattern means sellers focus on short-dated options to capitalize on rapid theta decay.

Does Theta Decay Speed Up as Expiration Nears?

Yes, theta decay accelerates significantly as expiration approaches, reaching its peak in the final days—this is especially true for at-the-money options, which lose value at the fastest rate. The curve of time value loss is exponential, not linear.

In the last 10 days, options can lose 60–80% of their remaining time value. For high-liquidity contracts in popular indices, this means losing Rs. 10–20 per day in the final week.

This rapid acceleration is why many traders avoid holding long options close to expiry. Sellers, on the other hand, target this period to maximize collected premium.

Is There Any Way to Stop Theta Decay?

No, there is no way to stop theta decay—time passes and option value erodes regardless of market conditions, making it an unavoidable aspect of options trading. All long option holders experience theta loss, while sellers profit from time decay.

Although you cannot escape theta decay, you can manage and benefit from it with the right strategies and risk controls.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 16")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 17")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 18")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 22")

No Comments Yet.