A delta neutral strategy is an options approach designed to eliminate price movement risk by balancing positive and negative deltas so that the total portfolio delta is zero. The term “delta neutral” originates from the Greek letter delta (Δ), which measures how much an option’s price changes for every one-point move in the underlying asset. When a position is delta neutral, its net delta—meaning the combined delta of every option and the underlying asset in the portfolio—equals zero.

This setup ensures that small price changes in the underlying asset do not impact the portfolio’s value, making it “neutral” to price direction. The primary purpose of constructing a delta neutral position is to isolate and profit from other factors like volatility (vega) or time decay (theta), rather than market direction.

What Is a Delta Neutral Strategy?

A delta neutral strategy is an options trading technique aimed at making the portfolio’s value insensitive to small moves in the underlying asset, by achieving a net portfolio delta of zero.

A delta neutral strategy is done by carefully combining long and short positions in options, and sometimes the underlying asset, so that the total effect of price changes cancels out.

The core idea is to avoid making profits or losses from the direction of the market. Instead, delta neutral traders focus on profiting from other sources such as changes in implied volatility, time decay, or mispricing between options and the underlying.

Delta neutral strategies are widely used by hedge funds, institutions, and professional traders. These traders rely on sophisticated models and technology to constantly monitor and rebalance their positions, keeping the net delta close to zero at all times.

Some of the most common delta neutral tactics include straddles, strangles, iron condors, and calendar spreads. Each of these uses a different combination of options to achieve a zero delta exposure, while allowing the trader to benefit from other market factors.

How Does the Delta Neutral Strategy Work?

A delta neutral strategy works by combining options and/or the underlying asset so that positive and negative deltas offset each other, resulting in a net portfolio delta of zero. This means the position’s value is largely unaffected by small changes in the underlying asset’s price.

The mechanics involve the below.

- Buying and selling options (calls and puts) in specific ratios.

- Sometimes including long or short positions in the underlying asset (like Nifty futures or stocks) to fine-tune the overall delta.

Key points in the working are below.

- Net delta = 0: Achieve this by balancing positive delta (from long calls or stocks) with negative delta (from puts or short calls).

- Payoff profile: Focuses on making money from volatility changes (vega) or capturing time decay (theta), not from price moves.

- Gamma vs. theta tradeoffs: Positive gamma benefits from large price swings, but usually comes with negative theta (losses from time decay).

For example, a trader might buy an at-the-money straddle (one call, one put at the same strike), which starts delta neutral. If the underlying asset moves sharply, the trader can adjust (rebalance) the position to remain delta neutral, capturing gains from volatility.

Delta neutral strategies are dynamic and require frequent monitoring. As prices, volatility, and time to expiry change, so does delta, so traders must adjust positions regularly to maintain neutrality.

How to Construct a Delta Neutral Position

To construct a delta neutral position, a trader selects an underlying asset, chooses options, and adjusts the combination so that the total delta exposure is zero. The process has a few key steps, and precision is vital for effectiveness.

- Choose the underlying asset and expiry: Decide which stock or index and the time frame you want to trade.

- Select options and possibly the underlying: Pick appropriate strikes, expiry dates, and whether to include the underlying asset.

- Calculate total delta exposure: Use options pricing models or a trading platform (like Zerodha Kite or Upstox in India) to sum up the deltas of all positions.

- Adjust positions: Buy or sell additional options or underlying shares to bring the net delta as close to zero as possible.

- Model Greeks: Use a platform to continuously monitor delta, gamma, theta, and vega to ensure ongoing neutrality.

For example, suppose a Nifty option call has a delta of 0.5 and a put at the same strike has a delta of -0.5. Buying one of each creates a delta neutral setup. If the market moves, delta will shift, so the trader might need to buy or sell Nifty futures to rebalance.

This construction is not a one-time task. Traders need to rebalance as market conditions change, which can mean daily or even intraday adjustments.

Why Use a Delta Neutral Strategy?

Delta neutral strategies are used to reduce directional risk and profit from volatility or option pricing inefficiencies, rather than betting on market direction. This makes them valuable for traders seeking more stable and predictable returns.

- Reduce directional risk: The position’s value is not affected by small up or down moves in the underlying asset.

- Profit from volatility: These setups can benefit when implied volatility rises, as option premiums increase.

- Useful in sideways or range-bound markets: When markets lack a clear trend, delta neutral strategies can generate income from time decay or volatility.

- Enhanced capital efficiency: Traders can deploy less capital compared to outright long or short strategies, due to hedging.

- Better risk control: Losses from big market moves are limited, as the position can be adjusted quickly.

For example, during periods of expected high volatility (like earnings announcements or policy decisions), delta neutral strategies allow traders to earn from volatility spikes without taking a view on direction. In India, this is a common approach in Nifty and Bank Nifty weekly options.

When to Use Delta Neutral Strategies

Delta neutral strategies are best used when you lack a strong directional view or expect volatility to increase, especially around events or in range-bound markets. Timing is crucial to maximize effectiveness.

- Low conviction about price direction: When technical or fundamental analysis offers no clear trend.

- Expecting volatility spikes: Before key events such as RBI meetings, corporate results, or global announcements.

- Sideways or range-bound markets: When indices or stocks are trading in a tight band.

- Desiring controlled market exposure: Traders want to earn premiums or volatility without taking outright directional bets.

These strategies are especially popular ahead of known events with uncertain outcomes. For example, during budget announcements or US Fed meetings, option premiums become expensive due to uncertainty. Delta neutral traders enter positions to benefit from possible post-event volatility, while keeping risk tightly managed.

How Option Greeks Affect a Delta Neutral Strategy

Option Greeks—delta, gamma, theta, and vega—determine the risk and reward of a delta neutral strategy, affecting profits, losses, and adjustments required. Understanding these is crucial for effective trading.

- Delta (Δ): Measures price sensitivity. Delta neutral means net delta ≈ 0.

- Gamma (Γ): Measures how much delta changes as the underlying moves. Positive gamma means profits from sharp price moves, but also requires frequent rebalancing.

- Theta (Θ): Represents time decay. Most delta neutral setups (like straddles) have negative theta, causing daily losses as expiry approaches.

- Vega (ν): Sensitivity to volatility. Positive vega means profits if implied volatility rises, while negative vega setups lose if volatility drops.

For example, a delta neutral straddle on Nifty.

- Net delta: ≈ 0, so unaffected by small moves.

- Gamma: Positive (e.g., 0.25 per lot); beneficial if Nifty moves sharply.

- Theta: Negative (e.g., Rs. -80 per day); loses value as time passes.

- Vega: Positive (e.g., Rs. 250 per 1% rise in volatility).

Traders must monitor all Greeks, not just delta, and adjust positions as market conditions evolve.

What Are Examples of Delta Neutral Strategies?

Examples of delta neutral strategies include straddles, strangles, butterfly spreads, iron condors, calendar spreads, and gamma scalping. Each uses different option combinations to achieve a near-zero net delta.

- Long Straddle: Buy one at-the-money call and one put with the same strike and expiry. Profits from large moves in either direction.

- Long Strangle: Buy out-of-the-money call and put. Costs less than a straddle but requires a bigger move to profit.

- Butterfly Spread: Buy one in-the-money, sell two at-the-money, and buy one out-of-the-money option. Profits if price stays near the middle strike.

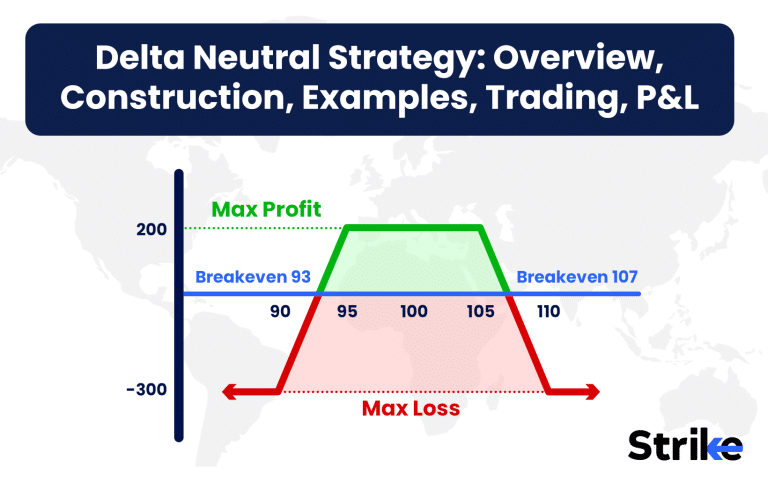

- Iron Condor: Sell one out-of-the-money call and one put, buy further OTM call and put for protection. Profits if the underlying stays within a defined range.

- Calendar Spread: Buy a long-dated option and sell a short-dated option at the same strike. Profits from changes in volatility or time decay differences.

- Gamma Scalping: Dynamic method that involves rebalancing delta as the underlying asset moves, locking in profits from volatility.

Each strategy suits different market conditions. For example, a straddle is suitable for high volatility expectations, while an iron condor fits low volatility, range-bound markets.

How to Trade and Manage Delta Neutral Positions

A delta neutral strategy aims to create a position where gains or losses from price movement in the underlying asset are offset, at least initially. This allows you to benefit from volatility rather than direction. One common approach is a Long Straddle at the at-the-money (ATM) strike.

Example Setup

Let’s say the 25450 strike is ATM. From the option chain:

- Buy 1 lot 25450 Call at ₹64.45, Delta = +0.50

- Buy 1 lot 25450 Put at ₹63.65, Delta = –0.50

Each option lot size = 75

- Call cost: ₹64.45 × 75 = ₹4,833.75

- Put cost: ₹63.65 × 75 = ₹4,773.75

- Total Investment = ₹9,607.50

- Net Delta = +0.50 – 0.50 = 0 (Delta Neutral)

This setup profits from large movements in either direction while being protected against small price changes in the short term.

Breakeven Points

- Upper Breakeven = 25450 + ₹128.10 = 25,578.10

- Lower Breakeven = 25450 – ₹128.10 = 25,321.90

Profit and Loss Scenarios

- If Nifty moves to 25,600 or 25,300 (a ±150 point move), you earn about ₹1,650

- If Nifty stays at 25450, the entire premium of ₹9,607.50 is at risk (maximum loss)

Managing the Position

- If volatility is expected to rise, you can hold the position to benefit from increased premiums.

- You may close the trade once a profitable move occurs or if the trend becomes clear.

- Adjustments can be made if Delta drifts away from zero, by adding or reducing positions to bring the portfolio back to Delta neutral.

This strategy is best suited for times when a large move is expected but the direction is uncertain, and managing it involves tracking both price and volatility changes closely.

What Are the Profit Potential & Risks?

Delta neutral strategies offer profit opportunities from volatility spikes and effective gamma scalping, but risks include time decay, adverse volatility moves, and slippage from frequent adjustments. Profit and loss depend on the specific setup and market conditions.

Profit scenarios

- Volatility spike: Options premiums rise, increasing strategy value.

- Frequent rebalancing (gamma scalping): Capture profits from price swings.

Risk scenarios

- Time decay (theta): Most delta neutral strategies lose value daily.

- Volatility drop: If premiums shrink, positions lose value.

- Adjustment costs: Frequent trading to rebalance delta incurs costs.

| Strategy | Max Profit | Max Loss | Breakeven |

| Straddle | Unlimited | Premium paid | Strike ± premium |

| Iron Condor | Spread width | Spread width – net credit | Between sold strikes |

| Butterfly | Limited | Premium paid | Near middle strike |

Profit and loss diagrams for a straddle show a “V” shape, with losses limited to the premium paid (e.g., Rs. 3,000 per lot) and profit potential unlimited.

For iron condors, profit is capped, but so is the risk.

Is Delta Neutral Strategy Profitable?

Yes, delta neutral strategies are profitable if volatility increases, rebalancing is effective, and transaction costs are kept low. However, consistent profitability requires active management.

Professional traders and institutions use delta neutral strategies for steady income. In India, less than 20% of retail options traders are profitable, mainly due to high costs and lack of discipline.

What are the Alternatives to Delta Neutral Strategy?

Alternatives to delta neutral strategies include simple directional trades, vertical spreads, covered calls, and protective puts, each with unique risk and reward profiles.

| Strategy | Delta Neutral | Directional | Risk | Reward |

| Long Call/Put | No | Yes | High | Unlimited |

| Vertical Spread | No | Yes | Medium | Defined |

| Iron Condor | Yes | No | Low-Defined | Limited |

| Covered Call | No | Yes | Low | Limited |

| Protective Put | No | Yes | Low | Limited |

- Directional trades: Simple buy/sell calls or puts. High risk, high reward, suited for strong market views.

- Vertical spreads: Buy and sell options at different strikes. Lower risk, defined reward/loss.

- Iron butterfly/condor: Similar to delta neutral but focused on collecting premium in a tight range.

- Covered calls: Hold stock, sell call for extra income. Reduces risk but caps upside.

- Protective puts: Hold stock, buy put as insurance. Limits downside.

Choose based on your market view, risk appetite, and trading goals. Delta neutral strategies are ideal for volatility-focused, risk-controlled trading, while alternatives suit those with a strong market view or seeking simpler setups.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 34")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 35")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 36")

: Overview, 10 Types of Indicators, Settings for Different Markets 38")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 40")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 43")

No Comments Yet.