A Long call refers to the act of buying a call or “Going Long” in an option contract. A call option is a derivative which gives its buyer the right but not a necessity to buy its underlying asset at a pre-decided price and at a pre-decided time.

You calculate the value of a long call by considering 4 components. Call Premium is the price a buyer pays to the option seller to purchase the call option. Strike Price is the pre-decided price at which the call option buyer has the right to buy its underlying asset. Expiration Date is the date on which the option contract expires. You also have to consider the current price of the underlying asset of an option contract. The difference between the market price of the underlying asset at the time of exercise and the strike price minus the initial premium paid for the option is considered when determining the potential profit or loss from a long call.

The long call also offers 2 major benefits to its buyer. Option buyers use the call option in order to counterbalance their existing portfolio. They use different options strategies according to the market conditions in order to hedge their long-term positions.Call option buyers earn unlimited profit if the market keeps going higher. Their risk is also defined by the premium they have paid. Option buyers will not lose more than the contract’s premium.

What does Long Call mean for buyers?

A long call means for buyers to go long indirectly in the contract’s underlying asset for buyers. Buyers go long in a call option when they believe that the market is bullish. Option buyers have the right but not the obligation to buy the underlying asset at a specific price on or before its expiry.

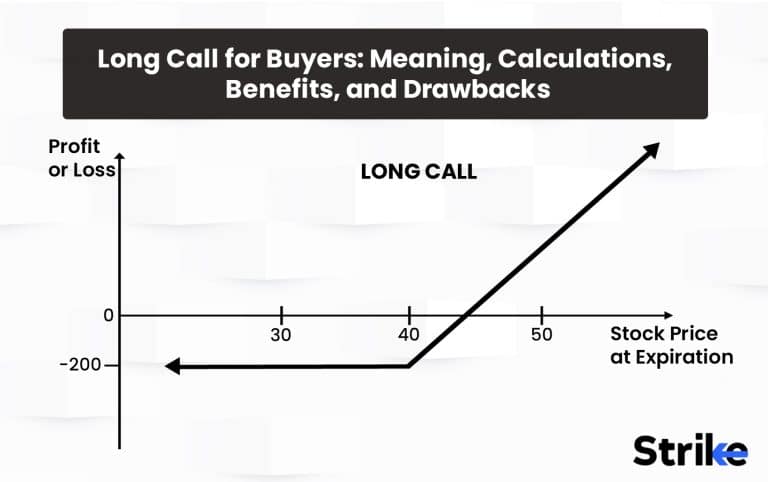

The long call will only earn profit when the underlying asset rises significantly. However, the buyer will incur losses if the underlying asset is stagnant or the price of the underlying asset decreases.

The profit potential for buyers in a long call is unlimited. The loss for the buyer is limited as the buyer only incur a loss on the option premium he/she has paid.

The buyer also benefits from a long call because he/she is getting leverage. Oftentimes traders are unable to buy a specific asset in large quantities due to shortage of funds. However, options let you use leverage. Meaning, option contracts allow you to buy the long call of that asset in the same quantity and at a much lesser price.

What is the importance of the Long Call in option trading?

A Long Call is an important and a widely used contract in options trading because of its role in providing investors with different opportunities to manage their risk makes it a crucial tool in trading.

A Long Call lets its buyer speculate in a short span of time. Traders use the long call to make money from the expected price increases in the market. This way, traders earn profit from a relatively short upfront investment.

A Long Call is used in conjunction with other option strategies. This creates more complex option strategies like spreads and straddles. Buyers adjust strike prices and expiry dates of a long call based on market situations.

Long Call options are effectively used for managing risk. For example, a trader buys a call option as a hedge against the potential price increase in the market, if they have a long-term short position in the market and don’t want to see all his/her gains wash away with short-term price rises in the market.

One should also note that even if a long call is crucial in the market, it does have risks like time decay. You should not buy or sell options until you totally understand the risks associated with options trading. You should always remember that only experts make money from options trading.

How does Long Call work for buyers?

A Long Call works for buyers by giving them the right but not a necessity of buying the shares of its underlying asset at a predetermined price on or before its expiry. A Long Call strategy provides its buyer with the opportunity to earn from the price rises in its underlying asset.

A Long Call also works for buyers by posing as a hedging tool. Buyers use a long call as a tool for hedging in order to counterbalance their existing portfolio. This helps them in managing risks during difficult times.

What does the Unlimited Profit Potential in Long Call mean?

Unlimited profit potential in a long call means that there are no defined upper limits to the degree to which an investor profits in a trade. Meaning, the call option will continue to show profits if the underlying asset keeps shooting to the upside. There are no limits to the upper side. However, the buyer will have to either book profits or exercise his/her rights upon the expiration date. The Unlimited Profit Potential is one of the major reasons why traders long for a call option.

What are the key components of a long call option contract that buyers should understand?

Option buyers must have a good understanding of the key components of a long call option contract. Here are 5 main components of a long call option.

- Strike Price: Strike price or exercise price is the predetermined price on which the buyer has the right to buy the underlying asset on or before expiry. It is also known as the price at which the buyer and seller of the option contract agree to transact.

- Expiry Date: Expiration date is the date on which the option contract loses all of its value and becomes void or null. Traders will either let the option become valueless or exercise their rights by this date.

- Premium: Premium is the sum of money a buyer has given to the seller to buy the option contract. It is the cost of acquiring the right to potentially buy its underlying asset at its strike price.

- Option Type: There are 2 types of options. Call options and put options. Buying a call option represents bullish sentiment while buying a put option represents bearish sentiments. Buyers should know this to make informed trading decisions.

- Option Style: There are 2 styles of options. American options and European options. The only difference between these two is that the American options allow its buyers to exercise their rights on or before expiry whereas buyers have to exercise their contracts only on expiry when using European options.

Understanding these components is a crucial part in option trading success. Knowing about these components helps traders in effectively implementing their strategy and managing their positions.

How is the profit potential determined for buyers who hold a long call position?

The profit potential for option buyers who hold a long call is determined by factors like strike price of the call option, premium of the option contract, underlying asset’s price at the expiry and the cost of commissions and fees of the broker.

The long call option is only profitable when the stock price is higher than the strike price plus the premium paid on the expiry date. The formula for calculating the profit is.

Profit = (Current Market Price – Strike Price) – Premium paid

However, the long call ends up giving losses if the underlying asset’s price is below the contract’s strike price on the expiry day.

What factors should buyers consider when selecting specific long-call options to purchase?

Option buyers must consider crucial factors when selecting specific long-call options to purchase. Here are 6 most important factors that buyers should always look at before buying an option.

Premium

Premium is the price paid for acquiring an option contract. Buyers should always analyze the premium in relation to their risk appetite and potential gains. Options with higher premiums offer great profits but they also increase the breakeven point.

Strike Price

The strike price is the price at which the buyer has a right to buy the underlying asset at. The strike price should always align with the buyer’s expectations of the underlying asset’s future price movement. The buyer chooses a lower strike price for profit maximization if he/she strongly believes that the underlying asset’s price rise significantly.

Expiration Date

The expiration date is the date on which an option contract expires or becomes void. This is an important factor to consider because if the underlying asset doesn’t rise in this period then the buyer will incur losses.

Break Even Point

The break even point refers to the price at which the option is even meaning it is neither making a profit nor incurring a loss. For call options the breakeven point is.

Break Even point = Strike Price + Premium Paid.

Market Volatility

Options buyers must analyze the current market mood before entering in a trade. Higher volatility generally leads to higher premiums while lower volatility increases the chances of incurring losses.

Risk Management

Options buyers must have a clear understanding of the risk they are taking while buying options. They must also get familiar with the methods that help in managing risks associated in options trading.

Options trading is for experts who understand the complexities of these derivatives. It is crucial to stay updated, constantly educate yourself and continuously refine your strategies to excel in options trading.

How is Long Call calculated?

A Long Call is calculated by considering 6 important factors. Here are the 6 factors used in the calculation of a Long Call.

Determining the current price of the underlying asset. It is important to find the current market price of the underlying asset on which the option contract is based on.

Identifying the strike price. The strike price is the price at which an option buyer has a right to purchase the underlying asset. This price is pre-determined at the time of buying the option.

Calculating the intrinsic value. The intrinsic value is the difference between the current price of the underlying asset and the strike price of the call option contract. The intrinsic value is positive when the underlying asset’s price is higher than the strike price. Otherwise, it is zero.

Intrinsic Value = Current Price of the Asset – Strike Price of Option

Determining the time value. The time value of an option contract is calculated by subtracting the intrinsic value from the total option price. It represents the premium paid for the possibility of a price increase in the underlying asset before the option expires.

Time Value = Option Price – Intrinsic Value

Considering other factors. We have to consider other factors such as volatility, interest rates and time to expiration also affect the option’s pricing. These factors are considered when calculating options prices through models like the Black-Scholes model.

Calculating the total value. Total value of a call option contract is the sum of intrinsic value and the time value.

Total Value = Intrinsic Value + Time Value.

Pricing an option is very complex. This is why there are professional software nowadays that do this job for you. They also keep track of the live price changes in an option contract too.

How does Long Call differ from other Option Payoffs?

Every option strategy has a different payoff chart. A long call’s payoff chat differs from the rest of option payoffs in 3 ways.

The profit potential of a long call is theoretically unlimited. If the underlying asset’s price keeps on shooting upwards, the following option contract will keep increasing in value.

The total risk of a call option buyer is limited to the premium paid for acquiring the option contract. The buyer only incurs a loss when the underlying asset fails to move above the option’s strike price. Even in the worst-case scenario, the option buyer will only lose the amount he/she invested.

Long call option is affected by time decay. Time decay is also known as the theta value of an option. The value of an option decreases as the days pass. This means that if the underlying asset is stagnant, the option expires worthless on the data of expiry.

It is advisable to have a good understanding of options before you take a trade. You even consult with a financial professional before engaging in options trading.

Do Long call options have a limited lifespan?

Yes, Long Call options have a limited lifespan. There are two types of contracts In India – Monthly and Weekly. Both of these contracts expire and become worthless on their respective expiration dates.

What is the concept of “in the money,” regarding long call options?

A call option is “in the money” or (ITM) when the current price of its underlying asset is higher than the option’s strike price. This situation is profitable for the buyer. For example, the option is in the money by Rs. 10 if the strike price of a call option is Rs. 50 and the current price of the underlying asset is Rs.60.

What is the concept of “at the money,” regarding long call options?

A call option is “at the money” or ATM when the current price of its underlying asset is identical with the strike price of the option contract. Here, the option contract does not have any intrinsic value and is solely composed of time value. For example, the option is ATM if the strike price of a call option is Rs. 50 and the current price of the underlying asset is Rs.50.

What is the concept of “out of the money” regarding long call options?

A call option is “out of the money” when the current price of its underlying asset is lower than the strike price of the option contract. This situation is a loss-making one for the buyer. For example, the option is out of the money by Rs.10 if the strike price of a call option is Rs.50 and the current price of its underlying asset is Rs.40.

How does Long Call behave under different market scenarios?

The performance of a long call depends upon different market scenarios. Long Call behaves differently in 3 different market scenarios like.

A long call option will be immensely profitable in a bullish market. The underlying dynamics of the long call is built so that it rises in value drastically during a bull market.

The value of a long call will keep increasing as its underlying asset rises because there is no limit. However, the buyer will have to decide whether to exercise his/her rights or book the profit on the option’s expiration date.

A long call option will be devastating in a bearish market. A long call option will lose its value drastically during a market where prices are falling.

The value of a long call option will keep on decreasing as its underlying asset’s price falls. The value of the call option will turn to zero on its expiration date if the buyer does not book his/her loss .

A long call option gives profits as well as losses during a volatile market. The buyer will profit when the price of the underlying asset rises above the strike price of the option. Conversely, the buyer will incur losses if the underlying asset falls below the strike price of the option.

One should also note that the behavior of a long call option also depends on factors like the time remaining until expiry, Implied Volatility (IV), current interest rates, etc. These factors will have an impact on the pricing of the option under any market scenario.

What are some common strategies that buyers employ when managing their long call positions?

Long Call options are usually used in hedging. However, here are 3 of the common strategies that buyers employ when managing their long call positions.

Holding Until Expiration

One of the simplest things to do is to hold the long call option until its expiration date whenever the option is going in your favor. The buyer then decides whether to book his/her profits or exercise the rights on the expiry date.

Rolling the option contract

Rolling the option contract means to shift the current expiry’s option contract with the next month’s or week’s contract while keeping the strike price identical. A buyer does this when the underlying asset hasn’t performed as per the expectations of the option buyer and he still believes that the underlying asset will perform well in the coming days.

Hedging with other options

Option buyers deploy option hedging strategies to safeguard their long call positions. One way to do this will be to buy the put options of the same underlying asset to counterbalance the potential losses if the price declines.

Choosing an option strategy depends on the option buyer’s market outlook, risk appetite and his/her overall trading goals. Always remember, it is important to adapt to changing market conditions and make informed trading decisions based on the evolving market situations.

Are there potential benefits with Long Call positions for buyers?

Yes, there are potential benefits with long call options for buyers. Here are 3 of the potential benefits that buyers have with long call positions.

Long Call’s strategic flexibility is one of the major reasons why buyers are attracted towards buying it. A long call is strategically used in diversifying as well as hedging an existing portfolio. It is combined with other option strategies to form a spread or a collar.

Long call options provide leverage. Meaning, you will control a larger position in the underlying asset by making a small upfront investment. This enhances the potential returns of a buyer if the expected price move occurs in the underlying asset.

The buyer’s risk when buying a call option is only limited to the premium he is paying. Meaning, a buyer will only lose the capital he has invested and not his/her whole account even if the underlying asset’s price falls to zero.

One should also note that a long call also has risks like time decay, etc. One should not get influenced by the mere benefits. Option trading is risky and one should always make informed trading decisions after studying the following topic closely.

How to Enhance the Long Call Position for buyers?

Buyers of long call positions enhance their profits by deploying strategies. Here are 3 strategies that enhance the profit potential of the long call for buyers.

Pyramiding refers to the act of adding quantities in your existing trade every time there is a drop in the price of the asset. This is only applicable when the underlying asset is moving in your favor.

Pyramiding is based on the fact that markets do not rise in a straight line. They rally a bit and they retrace, this is when you should be adding more call options.

You should also note that this is a risky way to enhance your long call option position but expert traders all around the globe do it.

You enhance your long call position by buying call options with a longer time to expiration. This will give more time to the underlying asset to move in your desired direction. Longer expiration option contracts also provide greater flexibility and thus increase your chances of being profitable.

Buying a call option with a lower strike price increases the chances of the option being in-the-money. This is because the underlying asset will not need to rise much to reach the strike price.

These were 3 of the ways using which you improve your potential profits. However, you should practice these techniques on paper first if you are a beginner, as they are very risky in the real market.

What are the potential risks involved with Long Call positions for buyers?

Long call positions for buyers contain limited risks. Here are the 3 potential risks involved with long call positions for buyers.

Limited Lifespan

A long call has a limited lifespan. Meaning, the option contract expires valueless if the underlying asset does not move in the buyer’s desired direction before the expiration date. Time Decay

Options have a time value which decreases from the time the contract is created. This time decay decreases the value of the option even if the underlying asset’s price moves in your favor. The value of an option contract decreases if the price of the underlying asset does not move quickly.

Premium Loss

An option buyer is susceptible to losing the whole premium amount of an option contract. The maximum loss you incur is calculated by multiplying the option’s lot size with the premium you have paid. For example, you incur a maximum loss of 2500, if the premium is 100 and the lot size is 25.

It is important for option buyers to carefully assess their risk appetite, investment goals and the market conditions before taking a trade in options. Understanding the risks associated with options helps option buyers in managing their risk effectively.

Are there downsides of Long Call for buyers?

Yes, there are downsides of long calls for its buyers. Option buyers must consider downsides like time decay, loss of premium, market volatility and limited time of the option contract before buying options.

How to manage the downsides in Long Call positions for buyers?

Managing the downsides in long call positions is the most crucial part of option trading.

Setting up a stop-loss order will automatically execute your exit from the trade once your option contract drops to the level you have set. The option premiums fluctuate immensely at times when the market is very volatile. Setting up a stop-loss order will help you limit your potential losses in case the trade does not go your way.

Monitoring your positions whenever you are in a trade is a good habit to follow whenever you are dealing with options. Also, you should stay updated on market conditions and news that have an impact on the underlying asset’s price. This will help you in making timely decisions in adjusting or exiting your positions. Keep taking partial profits whenever the market goes in your favor if you are trading with bigger positions. This will help you in locking some of those gains while still maintaining your exposure in the market.

Analyzing the potential downsides is very important as it helps you in understanding the risks associated with options trading. Always remember that a single trade will outplace you from the market. It is important to determine your risk and keep a stop loss which suits your risk tolerance.

What are the examples in real-life scenarios of Long Call positions for buyers?

Here are 2 real-life examples of using long calls.

First, let us assume that there is an investor who believes that the technology sector is going to boom. He found one company and now he wants to invest in this company to take advantage of the expected boom.

However, the investor buys a call option instead of buying the stocks of the company outright. And the investor’s prediction indeed comes true. The stock price rises. The investor then benefits from this, exercises his right and buys the stock at a lower price making a good profit.

This way, the investor enhanced his returns through the power of leverage provided by options.

For the second example, suppose there is an investor who is worried about the market rising. He has sold the futures of a stock. And now he is even more worried because he thinks that the market will fall even more.

The investor comes up with an idea in this situation. He purchases a long call of that same stock. This way, the loss of futures will be counterbalanced by the profit of the long options if the market rises from this level.

This is a primary example of how hedging is done using option contracts.

The examples above show how buyers use long call options to speculate as well as hedge in the market. However, it is important to note that these methods are risky and one should use these after gaining enough experience in the market.

What are the common mistakes the buyers make in relation to Long Call?

Ignoring time decay, delayed or early exit, etc. are common mistakes the buyers make in relation to long call. Here are the 3 most common mistakes the buyers make in relation to long calls.

Ignoring time decay

Time decay is an important component in the pricing of options. Buyers often ignore this fact and buy very out-of-the-money option contracts. These contracts will decrease in value even if the underlying asset moves. These buyers, as a result, end up making huge losses.

Not knowing when to exit

Buyers either keep holding onto the trade until the last minute of expiry or they exit in panic. This results in huge blows to their trading accounts as they do not have a predetermined level for exiting the trade. It is crucial to have a trading plan before each and every trade you take.

Ignoring implied volatility

Implied Volatility refers to the market participants expectation of the future price movements in the market. Option buyers should study implied volatility more as it does impact option prices. Implied volatility will impact the value of an option contract negatively when it decreases, even if the underlying asset moves favorably.

Buying options is lucrative but one must always remember the inherent risk in it. Successful options trading requires discipline and expertise. Fixing these common mistakes will help in maximizing the chances of your success.

How to avoid the common mistakes in Long Call for buyers?

Traders will be able to avoid common mistakes in long call by understanding the basics of options, conducting research, defining your trading goals, using proper position sizing and risk management techniques will help you in avoiding 90% of the mistakes other traders do.

Previous Article

Previous Article

37")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 40")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 41")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 42")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 46")

No Comments Yet.