The Protective put is a risk management strategy used by investors to limit downside risk while maintaining upside potential in the stock market. Protective put combines a long position in an underlying asset with the purchase of a put option on the same asset.

Investors utilize this strategy during volatile market conditions in exchanges like NSE and BSE, particularly for high-value stocks such as Reliance, TCS, and HDFC Bank. The strategy works by establishing a price floor below which losses stop accumulating, regardless of how far the stock price falls.

Trading protective puts requires calculating cost-efficiency based on option premiums prevalent in derivatives markets. The investor pays the premium upfront, which represents the maximum cost of the insurance. options typically expire on the last Thursday of each month, making timing crucial for strategy execution.

Profit and loss calculations remain straightforward – profits from stock appreciation offset the fixed premium cost, while downside protection limits losses to the difference between purchase price and strike price plus premium paid. NSE’s option chain provides all necessary data for implementation.

Risk factors include time decay affecting option value, particularly pronounced in India’s sometimes illiquid options markets. Premium costs reduce overall returns, especially significant given higher options premiums in markets compared to developed markets. Consider tax implications under capital gains tax rules before implementation.

What is a Protective Put?

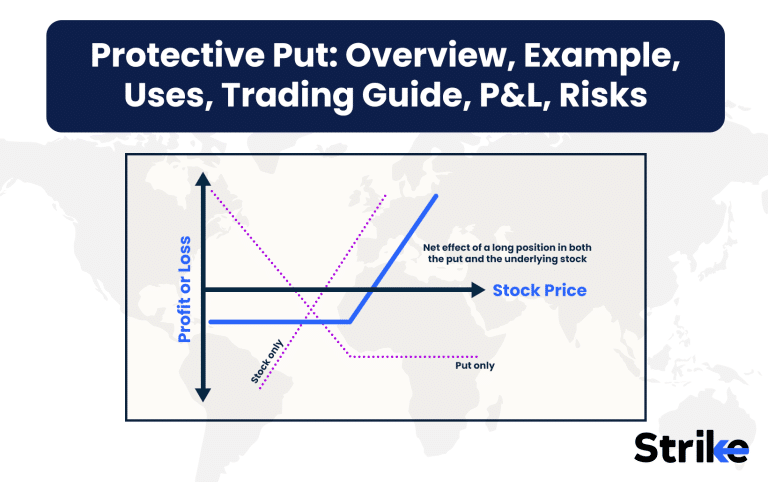

A protective put is a risk management options strategy that combines owning shares of an underlying stock while simultaneously purchasing put options for an equivalent number of shares. Protective put serves as a form of investment insurance, establishing a price floor below which an investor’s losses are limited regardless of how far the underlying stock price falls.

The goal of protective put focuses on limiting downside risk while maintaining unlimited upside potential. investors utilize this strategy particularly during volatile market phases or when holding significant positions in blue-chip stocks like Reliance Industries, HDFC Bank, or TCS. The strategy creates asymmetric risk-reward by paying a premium (the cost of the put option) to eliminate catastrophic downside scenarios.

Implementation involves purchasing put options with strike prices typically 5-15% below the current market price on exchanges like NSE and BSE like in the image below.

The maximum loss becomes limited to the difference between the current stock price and the put’s strike price, plus the premium paid. The maximum gain remains unlimited as the stock rises, reduced only by the put premium paid.

How Does a Protective put Work?

A protective put works by combining a long stock position with a long put option on the same stock, creating a price floor that limits downside risk. Protective put establishes this insurance-like protection through the right to sell shares at the put’s strike price regardless of how low the market price falls. Look at the below image.

In this example, a Nifty futures contract is bought at 24,376, and an ATM put with a strike price of 24,200 is purchased at a premium of 200. Consider Nifty falls below the breakeven of 24,176 (adjusted for the premium). Then the loss is capped at a fixed amount due to the put option. Conversely, in a case where Nifty rises above 24,376, profits increase exponentially, while losses are minimized within the range between the futures price and the breakeven. Below is a payoff diagram.

Here,

Position Structure (Protective Put)

Buy 1 Index Future at ₹24,376

Buy 1 ATM Put Option with Strike = ₹24,200 at a premium of ₹200

Lot size = 75

This strategy is deployed when a trader or investor already holds a long position in the equity or futures segment of the stock and looks forward to hedge the position, hence buys the put option later during the day.

Cost (Premium Paid)

₹200 × 75 = ₹15,000

This is your maximum cost for the downside protection.

Below is a payoff diagram with different scenarios.

| Spot at Expiry | Futures P/L | Put P/L | Net P/L (Approx) |

| ₹25,000 | ₹624 × 75 = ₹46,800 | 0 | ₹46,800 − ₹15,000 = ₹31,800 profit |

| ₹24,376 | 0 | 0 | −₹15,000 loss (premium only) |

| ₹24,000 | −₹376 × 75 = −₹28,200 | ₹200 × 75 = ₹15,000 | −₹28,200 + ₹15,000 − ₹15,000 = −₹28,200 |

| ₹23,800 | −₹576 × 75 = −₹43,200 | ₹400 × 75 = ₹30,000 | −₹43,200 + ₹30,000 − ₹15,000 = −₹28,200 |

| ₹23,200 or lower | −₹1,176 × 75 = −₹88,200 | ₹1,000 × 75 = ₹75,000 (max intrinsic value) | −₹88,200 + ₹75,000 − ₹15,000 = −₹28,200 |

The protective put strategy caps maximum loss at ₹28,200 (premium-adjusted) while allowing unlimited upside potential if Nifty rises above ₹24,376.

What is an Example of Protective Put?

In the below example of protective put, Maruti appears bullish as it is closing above the support structure. It is assumed that Maruti’s price will continue to rise and expire above the upper breakeven. A future contract is bought, and to protect this position and mitigate the risk of unlimited losses, an OTM put option is purchased later if the trader decides the position needs safety.

This fixes the possibility of unlimited losses. Note that buying an OTM put increases the risk and shifts the breakeven closer to the current market price (CMP), whereas buying an ITM put decreases the risk and shifts the breakeven further away from the CMP. This strategy is typically deployed when a trader or investor already holds a long position in equity or futures and seeks to hedge the position by purchasing a put option later in the trading day.

Below is a payoff diagram.

In this example of a protective put, the position structure involves buying one Maruti future at ₹12,267 and simultaneously purchasing one out-of-the-money (OTM) put option with a strike price of ₹11,900 at a premium of ₹150. The lot size for Maruti is 50. This setup is designed to provide downside protection while maintaining the potential for upside gains.

The premium cost, or the cost of protection, is calculated as ₹150 × 50, which equals ₹7,500. This amount represents the maximum cost incurred for the downside protection and is also the maximum loss if Maruti’s price remains above ₹12,267, as the put option would expire worthless.

The maximum loss for this strategy occurs when the spot price of Maruti drops to or below ₹11,900. At this level, the put option becomes active but does not sufficiently offset the loss from the futures position combined with the premium paid.

Specifically, the futures loss is ₹18,350, calculated as (₹12,267 − ₹11,900) × 50. Since the put option expires worthless at ₹11,900, its value is ₹0. Adding the premium cost of ₹7,500 to the futures loss results in a total maximum loss of ₹25,850.

Why Use a Protective put Strategy?

A protective put strategy is used by investors to create an insurance policy against significant market downturns while maintaining unlimited upside potential. This hedging mechanism establishes a price floor for investments, guaranteeing a minimum selling price regardless of how severely the market crashes.

Investors holding substantial positions in volatile stocks like Adani Enterprises or Zomato implement protective puts to sleep peacefully during turbulent markets.

Flexibility and control characterize protective puts beyond simple hedging. Investors choose specific protection levels by selecting different strike prices and expiration dates based on their risk tolerance.

The strategy allows continued ownership of shares without forced liquidation, preserving voting rights and dividend income. investors maintain their stakes in companies like HDFC Bank or Reliance Industries while eliminating catastrophic downside.

Protective puts offer advantages over traditional stop-loss orders in the market context. Stop-losses execute at unfavorable prices during gap-down openings, common after negative overnight developments. The 2023 Adani Group crash demonstrated this limitation when many stop-losses triggered far below intended prices. Protective puts guaranteed execution prices regardless of market gaps.

Earnings and event protection drives widespread adoption of protective puts around quarterly results season on NSE and BSE. Companies like TCS, Infosys, and HDFC Bank often experience significant post-earnings volatility. The strategy enables investors to participate in potential upside following positive results while limiting losses if results disappoint.

Similarly, protective puts shield portfolios during major events like Union Budget announcements, RBI policy meetings, and general elections where market reactions prove unpredictable but potentially severe.

When to Use a Protective Put?

A protective put should be used when investors anticipate increased market volatility but wish to maintain equity exposure. Market conditions favoring this strategy include periods of high VIX (India VIX exceeding 18), impending monetary policy decisions by the Reserve Bank of India, upcoming Union Budget announcements, or during general elections.

The strategy proves particularly valuable after extended bull runs, such as India’s 2024 market rally, where investors seek to protect accumulated gains without triggering capital gains tax through selling.

Best time frames for protective puts align with specific event horizons plus additional buffer time. For earnings protection, investors select expiration dates 1-2 weeks beyond the announcement date. For longer-term portfolio insurance, monthly expiries 30-45 days out provide optimal time value efficiency. The strike price selection balances cost against protection level, with 5-10% out-of-the-money puts offering reasonable cost-to-coverage ratios in the context.

Protective puts demonstrate advantages over alternative hedging strategies in directionally uncertain markets. Protective puts preserve unlimited upside, unlike covered calls that cap upside potential.

Compared to collars (combining protective puts with covered calls), pure protective puts require higher premium outlay but maintain full upside participation. Zero-cost collars gain popularity among cost-conscious investors, while deep-pocketed institutions favor outright protective puts for maximum flexibility.

How Option Greeks Affect Protective Put?

Option Greeks impact protective puts by influencing the option premium’s behavior and the overall strategy effectiveness.

| Greek | Definition | Impact on Protective Puts | Market Examples / Notes |

| Delta (Δ) | Measures change in option price relative to stock price | Higher (closer to -0.50) delta offers stronger protection but higher cost; lower delta (-0.30 to -0.40) offers cheaper hedging | Volatile stocks may require higher delta puts for effective protection |

| Theta (θ) | Measures time decay of option value | Erodes put value over time; accelerates near expiry | NSE options (e.g., HDFC Bank, Reliance) decay at 0.01–0.02 early, 0.03–0.05 near expiry; long-dated options reduce theta impact |

| Vega (ν) | Measures sensitivity to implied volatility changes | Volatility spikes increase put value | India VIX jumps (e.g., 15–20% from RBI events) can raise put value by 5–10% overnight |

| Gamma (Γ) | Measures rate of change in delta | High gamma provides rapidly increasing protection during sharp drops | Weekly Nifty options favored during 2023 banking crisis for high gamma protection |

| Rho (ρ) | Measures sensitivity to interest rate changes | Minor effect; long-dated options more sensitive | RBI rate hike of 25 bps can affect protective puts’ premium by 1–2% |

Traders adjust their protective put selection based on anticipated RBI actions, preferring shorter expirations during rate hike cycles.

How to Trade using Protective Put?

To trade using a protective put, you need of two key elements- selecting the right stocks and put strike price selection.

The stock selection for deploying a protective put strategy should be based on strong technical indicators, as the strategy relies on the potential for bullish price movements. In this case, with an upcoming expiry in 24 days, HeromotoCorp has been identified as an ideal candidate, showing promising technical strength and momentum.

Alternatively, the strategy may be used when a trader already holds the stock or a naked long futures position and seeks to safeguard against downside risk. By purchasing a put option, the trader effectively hedges the position, ensuring defined risk protection while retaining the opportunity to benefit from upward price movement.

The following payoff chart represents a protective put strategy, where an at-the-money (ATM) put option is purchased simultaneously with a long futures position on the underlying stock. This combination acts as a hedge, limiting downside risk while preserving the potential for upside gains.

The payoff structure demonstrates a well-balanced risk-reward profile: losses are capped below the put strike price due to the option’s protection, while profits remain uncapped above the breakeven point, minus the premium paid. This strategic setup is particularly useful in uncertain markets, allowing traders to participate in bullish trends while ensuring defined risk in case of adverse price movements.

In contrast, when an in-the-money (ITM) put option is used as a hedge alongside a long futures position, the downside risk is significantly reduced due to the higher intrinsic value of the put. This stronger protection results in a shifted breakeven point towards the upside, as the premium paid for the ITM put is relatively higher.

Consequently, for the overall position to become profitable, the underlying stock must exhibit clear and sustained bullish momentum, closing above the elevated breakeven level. While this setup offers enhanced risk control, it demands stronger upward price movement to achieve meaningful returns.

The following payoff represents a protective put strategy using an out-of-the-money (OTM) put option. In this scenario, the premium paid is lower due to the absence of intrinsic value, which lowers the breakeven point compared to an ATM or ITM hedge.

However, this comes at the cost of significantly higher downside risk, since the put only becomes effective after the stock drops below the strike price. While this approach is more cost-efficient, it offers limited protection and is more suitable when the trader expects a strong bullish move but still desires some form of minimal downside insurance.

The protective put strategy offers flexible risk management, with the choice of strike price—ITM, ATM, or OTM—allowing traders to balance cost, protection, and profit potential based on their market outlook.

Is Protective put Strategy Profitable?

Yes, protective put strategies prove profitable in specific market environments despite their premium costs. The strategy generates profits during strong uptrends exceeding the premium paid or during sharp market corrections below the put strike price like in the example below.

Tactical implementation during low-volatility periods minimizes premium expenses, enhancing long-term profitability. Strategic roll-downs as underlying stocks appreciate and create additional profit opportunities by capturing protection value.

The strategy’s true profitability extends beyond direct returns to include psychological benefits – enabling investors to maintain larger positions with controlled risk, potentially increasing overall returns through improved position sizing. Many successful portfolio managers utilize protective puts selectively rather than continuously, targeting periods of elevated risk to maximize their cost-effectiveness.

Is Protective put Bullish or Bearish?

Protective put strategies are fundamentally bullish with a cautious outlook. The core position remains a long stock holding, expressing directional bias toward appreciation. Investors maintain complete upside participation in stocks like Reliance Industries or HDFC Bank, benefiting from any bullish move exceeding the premium cost.

The put option component serves purely as insurance rather than a directional bet, functioning similar to purchasing homeowner’s insurance without hoping for damage. investors implement protective puts most frequently when maintaining a positive long-term view while acknowledging near-term risks. Market participants expecting sustained downtrends typically sell positions entirely rather than merely purchasing protection.

The strategy reflects optimism tempered by prudent risk management – bullish enough to maintain exposure yet cautious enough to establish downside safeguards. Protective puts epitomize the classic investment wisdom in markets: prepare for the worst while positioning for the best.

What are Alternatives to Protective put Strategy?

Alternative strategies to protective puts include stop-loss orders, collars, covered calls, and portfolio diversification.

| Strategy | Description | Risk Protection | Profit Potential | Cost | Best For |

| Protective Put | Buy a put option while holding a long position in the stock or futures. | Excellent downside protection; loss limited to premium + drop. | Unlimited upside above breakeven (stock + premium). | High (due to option premium). | Traders wanting defined risk protection while maintaining upside exposure. |

| Stop-Loss Order | Set a trigger price to automatically sell the stock if it falls to a set level. | No cost upfront; protection depends on execution at trigger. | Unlimited upside before the stop is hit. | None directly, but risk of poor execution. | Cost-conscious traders who want basic risk management without premiums. |

| Collar | Buy a protective put and sell a covered call simultaneously. | Downside limited (put strike); also caps upside (call strike). | Limited upside (due to short call); defined downside protection. | Low to neutral (put cost offset by call income). | Investors seeking low-cost hedging with a neutral to moderately bullish view. |

| Covered Call | Hold the stock and sell a call option on it. | No downside protection; exposed to full stock risk. | Limited upside (capped by strike of sold call). | Generates income through call premium. | Investors with neutral outlook looking to generate income on existing shares. |

| Diversification | Spread investments across assets/sectors to reduce overall risk. | Indirect protection; reduces unsystematic risk. | Varies depending on asset mix; no direct hedge per stock. | None, but may reduce returns. | Long-term investors reducing portfolio volatility rather than individual risk. |

These strategies—stop-loss, collar, and covered call—offer varying levels of risk control and reward potential, allowing traders to align their approach with market outlook and risk tolerance.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 48")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 49")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 50")

: Overview, 10 Types of Indicators, Settings for Different Markets 52")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 54")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 57")

No Comments Yet.