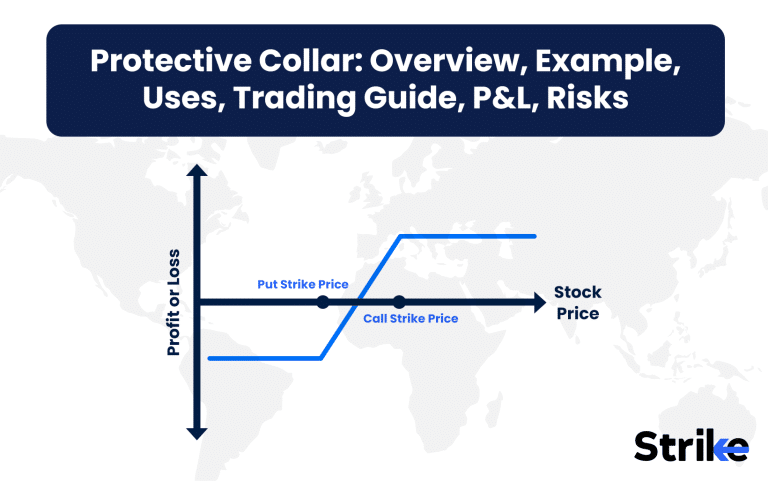

The Protective Collar is a defensive options strategy designed to protect an existing long stock position from potential downside risk while limiting upside potential. Protective Collar combines purchasing a put option while simultaneously selling a call option on the same underlying stock, creating a range where profits are protected.

Trading the collar successfully requires monitoring price movements closely and adjusting positions when market conditions change. Profit potential becomes limited once the stock price exceeds the call strike price, representing the primary drawback.

What is a Protective Collar?

Protective Collar is an options strategy that safeguards an investor’s existing stock position against significant downside risk while limiting potential upside gains. Protective Collar involves three components working together: owning the underlying stock, buying a put option, and selling a call option on the same stock with identical expiration dates.

The strategy begins with ownership of shares in a company. Purchase a put option at a strike price below the current market price to establish a price floor, effectively creating insurance against substantial losses. Sell a call option at a strike price above the current market price to generate premium income that offsets the cost of the put purchase. Both options typically share the same expiration date.

Consider an investor holding 100 shares of Larsen & Toubro at ₹2,500 per share. The investor buys a put option with a strike price of ₹2,300, paying a premium of ₹50 per share. Simultaneously, the investor sells a call option with a strike price of ₹2,700, collecting a premium of ₹40 per share. The net cost equals ₹10 per share (₹50 – ₹40).

The strategy establishes clear boundaries for both losses and gains. The maximum profit occurs if shares rise above the call strike price, while maximum loss happens if shares fall below the put strike price.

How Does a Protective Collar Work?

Protective Collar works by combining three elements: owning shares, buying a put option, and selling a call option on the same underlying asset. Protective Collar creates a range of protection by establishing both a floor and ceiling for your investment’s value, effectively limiting potential losses while also capping potential gains.

The strategy functions through the interplay between its components. Own the underlying stock first, representing the core investment requiring protection. Buy a put option with a strike price below the current stock price to establish a price floor – this guarantees the right to sell shares at the strike price regardless of how low the market price falls.

Sell a call option with a strike price above the current stock price to generate premium income, though this creates a ceiling on potential profits since you must sell shares at the call’s strike price if the stock rises beyond that level.

This strategy offers superior cost efficiency compared to simply buying protective puts. The premium received from selling the call substantially offsets the cost of the protective put. Many investors implement zero-cost collars where the call premium completely covers the put premium, providing downside protection at virtually no cost.

The collar excels during uncertain market conditions like those following national elections or RBI policy changes. Provides a predictable risk-reward profile that appeals to institutional investors and high-net-worth individuals managing significant positions in blue-chip stocks.

What is an Example of Protective Collar?

Let us take an example of Bajaj Auto shares to understand protective collar better.

A protective collar applies to an investor holding 100 shares of Bajaj Auto at ₹4,800 per share who wishes to protect against downside risk while generating income. The investor buys one put option contract (1 contract = 100 shares) with a strike price of ₹4,500 for a premium of ₹120 per share and simultaneously sells one call option contract with a strike price of ₹5,100 for a premium of ₹100 per share, both expiring in 30 days.

The net cost equals ₹20 per share (₹120 – ₹100), or ₹2,000 total for the position. The strategy creates a protected range between ₹4,500 and ₹5,100. The put option guarantees the investor the right to sell shares at ₹4,500 regardless of how far the stock price might fall. The call option obligates the investor to sell shares at ₹5,100 if the stock rises above that level.

| Breakeven Point | Formula | Value |

| Lower Breakeven | Entry Price + Net Cost | ₹4,820 |

| Upper Breakeven | Call Strike – Net Cost | ₹5,080 |

Multiple outcomes exist at expiration. Scenario 1: Bajaj Auto drops to ₹4,200. The put option provides protection, limiting the loss to ₹300 per share (₹4,800 – ₹4,500) plus the net cost of ₹20, totaling ₹320 per share. Scenario 2: Bajaj Auto rises to ₹5,300. The investor must sell at ₹5,100, limiting the gain to ₹300 per share (₹5,100 – ₹4,800) minus the net cost of ₹20, totaling ₹280 per share.

| Stock Price at Expiry (₹) | Put Value (₹) | Call Value (₹) | Net Payoff per Share (₹) | Total Payoff (₹) |

| 4,200 | +300 | 0 | -320 | -32,000 |

| 4,500 | 0 | 0 | -320 | -32,000 |

| 4,800 | 0 | 0 | -20 | -2,000 |

| 5,100 | 0 | 0 | +280 | +28,000 |

| 5,300 | 0 | -200 | +280 | +28,000 |

The payoff diagram resembles a horizontal channel, showing limited downside risk at ₹4,500 and capped upside at ₹5,100. The breakeven points occur at ₹4,820 (entry price plus net cost) and ₹5,080 (call strike minus net cost).

Why Use a Protective Collar Strategy?

Investors implement protective collar strategies to safeguard valuable stock positions against significant downturns while partially or fully offsetting the cost of that protection. The strategy offers particular value for long-term investors who want to maintain ownership of shares while navigating through periods of anticipated volatility or uncertainty.

Protection against stock price declines serves as the primary motivation for investors using collars. The purchased put option acts as insurance, establishing a definitive floor price for the stockholding regardless of how severely the market drops. This protection proves invaluable during events like general elections, geopolitical tensions affecting crude oil prices, or unexpected regulatory changes impacting specific sectors.

The strategy reduces protection costs by generating income through the written call option. Consider an investor holding Sun Pharmaceutical shares who pays ₹80 per share for protective puts. Selling calls against the position brings in ₹70 per share, reducing the net protection cost to just ₹10 per share – a 87.5% cost reduction compared to buying puts alone.

Volatile markets, common in India’s developing economy, create the ideal environment for collar strategies. The BSE Sensex frequently experiences significant swings during quarterly earnings seasons and global market turbulence. The collar provides predictability by defining maximum loss and gain parameters, allowing investors to maintain positions without making emotional decisions during market extremes.

Portfolio managers particularly value this strategy for managing core positions in essential sectors like IT, banking, and pharmaceuticals, where long-term ownership remains desirable despite short-term volatility concerns.

When to Use a Protective Collar?

Protective collar strategies prove most effective during periods of anticipated market volatility or uncertainty when investors seek to protect existing profits while maintaining stock ownership. The strategy works particularly well after substantial price appreciation in a stock or ahead of known risk events that threaten to increase market volatility.

Market conditions favoring collar implementation include pre-election periods in India when policy uncertainty rises, quarterly earnings seasons for major companies, Union Budget announcements, or Reserve Bank of India policy meetings.

Ideal candidates for collar strategies include stocks with liquid options markets and moderate to high implied volatility. Blue-chip stocks on the Nifty 50 typically offer the most efficient collar execution due to tight bid-ask spreads and multiple strike prices.

Apply collars to stocks that have experienced significant gains where protecting profits becomes a priority, such as ITC or Maruti Suzuki after 30%+ price increases. The strategy suits stocks approaching technical resistance levels or facing specific company events like management changes or merger announcements.

Investors benefit from implementing collars on stocks with upcoming events showing high historical volatility, including pharmaceutical companies awaiting regulatory decisions or technology firms ahead of major client contract announcements. The strategy provides defined risk parameters during these critical periods of uncertainty.

How to Trade using Protective Collar?

Selecting the right stock is a critical step in building an options strategy. Aarti Industries, after a period of significant losses, currently appears poised for profit-taking and may close higher as expiry approaches in 25 days.

To construct a protective collar for this scenario, the strategy involves combining a long position in the stock’s futures contract with a long put option and a short out-of-the-money (OTM) call option. Since the expiry is near, it is prudent to protect the long futures position with an at-the-money (ATM) put, while simultaneously selling an OTM call to offset some of the protection cost and to cap potential profits. The attached illustration (not shown here) visually represents the selected strike prices for these options.

The structure for this protective collar in Aarti Industries is below.

The purpose of this strategy is to limit both downside risk and upside profit. It is commonly used when an investor expects only a moderate upside, or when the primary goal is to protect a long futures position at a reduced net cost, while giving up gains above a certain price level.

Regarding the net cost, the total premium paid for the protective put is ₹17,650, while the premium received from selling the call is ₹5,050. Thus, the net premium or cost of setting up this protective collar is ₹12,600. This amount represents the maximum cost for downside protection and forms the net investment for the options part of the strategy.

The following table details the potential payoff scenarios at expiry, assuming a lot size of 1000.

| Scenario | Spot Price | Futures P&L | Put Option P&L | Call Option P&L | Net Premium | Total P&L |

| Price falls below ₹450 (e.g. ₹420) | ₹420 | (420-453.05) × 1000 = -₹33,050 | (450-420) × 1000 = ₹30,000 | 0 (expires worthless) | -₹12,600 | -₹15,650 |

| Price stays at ₹450 | ₹450 | (450-453.05) × 1000 = -₹3,050 | 0 (expires worthless) | 0 (expires worthless) | -₹12,600 | -₹15,650 |

| Price rises to ₹470 | ₹470 | (470-453.05) × 1000 = ₹16,950 | 0 (expires worthless) | 0 (expires worthless) | -₹12,600 | ₹4,350 |

| Price rises to ₹500 | ₹500 | (500-453.05) × 1000 = ₹46,950 | 0 (expires worthless) | 0 (ATM, no value) | -₹12,600 | ₹34,350 |

| Price rises above ₹500 (e.g. ₹520) | ₹520 | (520-453.05) × 1000 = ₹66,950 | 0 (expires worthless) | (500-520) × 1000 = -₹20,000 | -₹12,600 | ₹34,350 |

This table shows that the maximum potential loss of the protective collar is ₹15,650, which occurs if the stock price stays at or below the put’s strike price. The maximum profit is capped at ₹34,350, which is achieved if the stock price rises to or above the call’s strike price. Any additional upside beyond ₹500 is offset by the loss on the short call, so the total profit does not increase further.

What are the Maximum Profit & Loss on a Protective Collar?

The maximum profit equals the difference between the call strike price and the stock purchase price, minus the net cost of the options. The maximum loss equals the difference between the stock purchase price and the put strike price, plus the net cost of the options.

Calculation of potential profit scenarios begins with the call option strike price boundary. Consider an investor holding Infosys shares purchased at ₹1,500 with a collar using ₹1,400 puts and ₹1,600 calls, with the options having a net cost of ₹20. The maximum profit occurs at or above the call strike price of ₹1,600, equaling ₹80 per share (₹1,600 – ₹1,500 – ₹20). The maximum loss manifests at or below the put strike price of ₹1,400, equaling ₹120 per share (₹1,500 – ₹1,400 + ₹20).

Break-even points identify price levels where the strategy produces neither profit nor loss. The upper break-even point equals the stock purchase price plus the net debit paid for the options (₹1,500 + ₹20 = ₹1,520). The lower break-even equals the stock purchase price minus the net credit received, or in cases of net debit, the purchase price minus the difference between the put protection and the net debit.

How Option Greeks Affects Protective Collar?

Option Greeks significantly influence the performance and dynamics of a protective collar strategy by altering the value of the component options as market conditions change. The combined Delta, Theta, and Vega characteristics of the long stock, long put, and short call positions create a unique risk profile that responds differently to price movements, time passage, and volatility changes compared to simple stock ownership.

Delta impacts the strategy through its measure of directional exposure. The stock position carries a delta of +1, while the purchased put adds negative delta and the written call subtracts positive delta. This combination creates a position with diminishing sensitivity to price changes as the stock moves away from the middle of the range. Near the collar boundaries (put and call strikes), the position’s delta approaches either 0 (below put strike) or 0 (above call strike), effectively neutralizing further price exposure.

Theta works favorably for collar strategies through time decay of the short call component. The written call generates positive theta, meaning the strategy benefits as time passes and the call loses value. This positive effect partially offsets the negative theta from the long put.

Vega affects collars through volatility changes. Collars generally maintain negative vega exposure, meaning the strategy benefits from declining implied volatility. This characteristic provides a particular advantage in the market where events like quarterly earnings and economic policy announcements often create volatility spikes followed by normalization periods.

HDFC Bank options, for example, typically display elevated implied volatility before quarterly results, creating opportune conditions for establishing collars that benefit from the subsequent volatility decline.

What are the Risks of Protective Collar?

Protective collar strategies involve several significant risks despite their hedging benefits, primarily centered around opportunity costs, early assignment complications, and ongoing maintenance expenses. The strategy deliberately sacrifices unlimited upside potential in exchange for downside protection, creating a defined risk-reward framework that limits both losses and gains.

Capped upside potential represents the most significant opportunity cost. The written call option obligates the investor to sell shares at the strike price regardless of how high the stock climbs. In rapidly rising markets, particularly following major positive developments like GST rate reductions or favorable regulatory changes, this limitation proves costly. Many investors experienced this with technology stocks during the 2020-21 bull run, where collared positions underperformed unhedged holdings by substantial margins.

Risk of early assignment on the short call becomes pronounced with dividend-paying stocks. Options buyers frequently exercise calls just before ex-dividend dates to capture dividends, forcing the collar implementer to deliver shares prematurely.

Costs of rolling over options accumulate over time, eroding returns. Transaction fees, bid-ask spreads, and potentially higher implied volatility during roll periods increase the strategy’s expense. Investors maintaining collars on State Bank of India shares during multiple market cycles face these cumulative costs, which often exceed 2-3% annually when including all execution expenses.

Is Protective Collar Strategy Profitable?

Yes, protective collar strategies generate profits under specific market conditions while prioritizing risk management over maximum returns. The strategy proves most profitable during sideways or moderately bullish markets where stock prices rise slightly but remain below the written call strike price.

Profitability depends largely on the initial selection of strike prices and market behavior during the holding period. markets often experience periods of consolidation after major rallies, creating ideal environments for collar strategies. The technique excels particularly during volatile periods like those surrounding RBI monetary policy announcements or quarterly earnings seasons.

Many institutional investors implement collars during such periods, capturing moderate appreciation while limiting downside risk. The strategy outperforms simple stock ownership during market corrections, preserving capital that would otherwise diminish in value. Consider protective collars as insurance that occasionally generates modest returns rather than a primary profit-generation strategy.

Is Protective Collar Bullish or Bearish?

A protective collar represents a neutral to slightly bullish strategy that prioritizes risk management over directional bias. The position combines elements of both bullish and bearish outlooks while establishing defined boundaries for potential outcomes.

The strategy reflects modest bullishness through continued stock ownership and willingness to participate in some upside potential. Simultaneously, it incorporates bearish hedging through put protection and willingness to cap gains by selling calls. The strategy performs optimally in range-bound or slightly appreciating markets like those often seen in established sectors such as FMCG or banking following major index rallies.

Portfolio managers overseeing retirement funds or trust assets frequently employ collars on Bharti Airtel or Asian Paints positions to maintain exposure while limiting volatility. The approach acknowledges the inherent unpredictability of short-term market movements while expressing long-term confidence in the underlying company.

What are Alternatives to Protective Collar Strategy?

The most popular alternatives protective collar strategy are covered calls, protective puts, married puts, and iron condors.

Covered calls generate income through call option premiums while maintaining unlimited downside risk, unlike protective collars that include downside protection. This strategy proves preferable during stable or slightly bullish market phases, particularly with high-dividend stocks like Power Grid or NTPC where total return consists of both option premium and dividend income. investors favor covered calls during periods of elevated implied volatility following strong bull runs.

Protective puts provide downside insurance while preserving unlimited upside potential, differing from collars that cap gains. The strategy excels during periods of significant anticipated volatility with strong upside possibilities, such as pre-election periods or ahead of major policy announcements affecting specific sectors. The approach suits situations where investors remain highly bullish but require temporary protection.

Married puts combine stock purchase with simultaneous put purchases, creating insurance from the point of initial investment rather than protecting existing positions. This alternative works best for new positions with asymmetric risk-reward profiles, particularly in sectors like pharmaceuticals where regulatory decisions create binary outcomes.

Iron condors generate income through range-bound price expectations without requiring stock ownership, using four options to create defined risk spreads. The strategy thrives during extended consolidation periods common in major indices following strong directional moves. Bank Nifty positions often benefit from this approach during non-trending phases between major economic events.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 32")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 33")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 34")

: Overview, 10 Types of Indicators, Settings for Different Markets 37")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 38")

No Comments Yet.