The Options Spread strategy involves simultaneously buying and selling options of the same underlying asset but with different strike prices or expiration dates to limit risk and maximize potential returns. Options Spread techniques represent approximately 35% of all options trading volume in India, with a 27% year-over-year growth observed in 2024 according to NSE data.

Traders employ spread strategies to capitalize on specific market views while maintaining defined risk parameters. Bull spreads profit from rising prices, bear spreads from falling prices, and neutral spreads from sideways movement.

Traders gravitate toward vertical spreads due to their simplicity and capital efficiency. SEBI regulations require spread positions to maintain adequate margin requirements, typically 25-40% lower than naked options positions. Calendar spreads exploit time decay differences between near-term and longer-dated options. Diagonal spreads combine strike price and expiration date differences to create asymmetric payoff structures.

Risk management demands setting stop-loss levels and position sizing appropriate to account value. Spreads limit maximum losses to the net premium paid for debit spreads or margin requirements for credit spreads. Indian options traders face additional challenges from higher implied volatility and lower liquidity in certain strikes compared to developed markets. Successful spread trading requires understanding option Greeks—particularly delta, theta, and vega—to quantify risk exposure during market movements.

What is an Options Spread Strategy?

The Options Spread strategy combines multiple options positions on the same underlying security to create a single trading position with specific risk-reward characteristics. Options Spread involves simultaneously buying and selling options of the same class (calls or puts) but with different strike prices, expiration dates, or both.

Traders execute spreads to limit risk while maintaining profit potential in targeted market scenarios. Bull spreads benefit from price increases, bear spreads profit from price decreases, and neutral spreads capitalize on minimal price movement.

Indian derivatives markets saw 78% growth in options trading volume during FY 2023-24, with spread strategies accounting for approximately 40% of retail options activity. NSE data indicates spread strategies reduced average trading losses by 23% compared to naked options positions. Brokerage firms in India offer dedicated spread order screens to simplify execution. SEBI regulations provide margin benefits for recognized spread positions, reducing capital requirements by 30-60% versus individual positions.

Advanced traders modify basic spreads into complex structures like butterflies and condors to target specific price ranges in high-volatility Indian markets.

How Does an Options Spread Strategy Work?

An options spread strategy works by combining the buying and selling of the same type of options—calls or puts—at different strike prices, to manage risk and potential reward. This approach allows traders to profit from specific expectations about the market’s direction or volatility while limiting their maximum loss.

A spread always involves both buying and selling. If you sell an option with a higher premium and buy a cheaper one, you create a credit spread, which results in a net credit (money received upfront). Credit spreads are used when you expect the underlying asset will move only mildly and that time decay (theta) will erode option value in your favor.

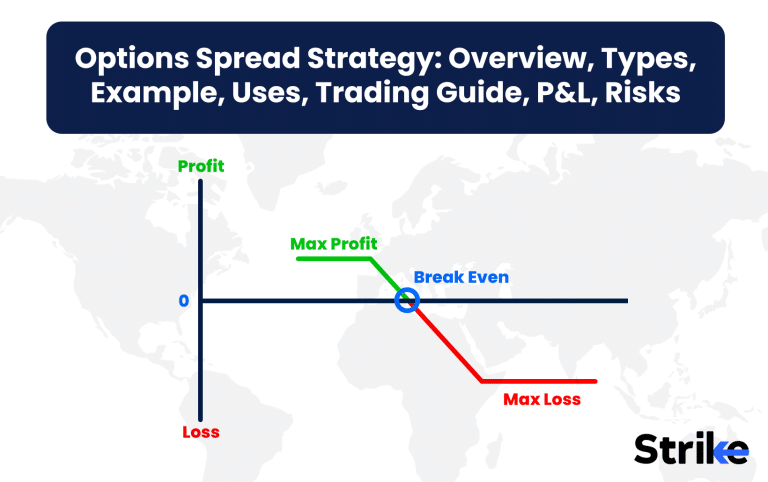

Below is the payoff diagram.

In contrast, buying a higher-premium option and selling a lower-premium one creates a debit spread, resulting in a net debit (money paid upfront). Debit spreads are used when a trader expects a strong move in the underlying asset and a rise in volatility, since time decay works against you unless the move is quick.

Below is the payoff diagram.

The choice of strike prices shapes the risk and reward profile of a spread. Spreads can be built as Out of The Money (OTM), At The Money (ATM), or In The Money (ITM), each offering different risk characteristics,

OTM spreads use strikes further from the current market price. Because OTM options have no intrinsic value, time decay heavily favors credit spreads here, making them relatively safe with defined, typically small, risk and reward. However, OTM debit spreads require a strong, fast move in the underlying for profitability, making them riskier.

ATM spreads center around the current market price. These are moderately risky because option premiums are highly sensitive to price moves. Their value can shift quickly from OTM to ITM, meaning risk and reward may change rapidly due to market movement.

ITM spreads use strikes within the current price range of the underlying. These options have high intrinsic value and are less affected by time decay, but they entail higher risk and higher potential reward. ITM credit spreads are often used by advanced traders when they strongly expect a particular trend.

Time decay (theta) and implied volatility (IV) are crucial in spread trading. Time decay benefits credit spreads, as option values drop approaching expiry, but it works against debit spreads. Implied volatility, which fluctuates with market sentiment, increases debit spread value when it rises, but can create risk for credit spreads if the underlying moves sharply.

What are The Different Types of Options Spread?

1. Bear Put Spread

A bear put spread is a type of debit spread created by buying a put option at a higher strike price and selling a put option at a lower strike price, both with the same expiration date and underlying asset. The term “bear” reflects the expectation of a price decline from a certain level or strike price.

Traders use a bear put spread when they speculate that the underlying asset is likely to undergo a bearish move but only expect a limited downside. Since it is a debit strategy, it is most useful when volatility is expected to increase, which helps the long put gain value.

However, if volatility does not rise or a bearish move does not materialize, the spread can become ineffective. The risk and reward for this strategy are both defined: the maximum profit occurs if the underlying falls below the lower strike price, calculated as the difference between the strike prices minus the net premium paid.

The maximum loss is equal to the net premium paid if the asset remains above the higher strike price at expiration. The breakeven point is the higher strike minus the net premium paid. The risk is limited to the premium paid, while the reward is also capped, unlike holding a naked long put.

2. Bull Call Spread

The bull call spread is a debit spread strategy that involves buying a call option at a lower strike price and selling another call option at a higher strike price, both based on the same underlying asset and expiration date. This strategy is suitable for traders who anticipate a bullish move in the underlying asset but expect the upside to be limited. It is particularly effective in low to moderate volatility environments where there is a possibility of rising volatility or short covering.

The maximum profit for a bull call spread is realized if the underlying asset closes at or above the higher strike price at expiration, with the profit being the difference between the two strike prices minus the net premium paid.

The maximum loss occurs if the asset finishes at or below the lower strike price and is limited to the net premium paid to initiate the trade. The breakeven point is the lower strike price plus the net premium paid. Both the risk and the reward for this strategy are limited and clearly defined, making it a popular choice among traders.

3. Bear Call Spread

A bear call spread is a credit spread executed by selling a call option at a lower strike price (which carries a higher premium) and buying another call option at a higher strike price (with a lower premium), both sharing the same expiration date and underlying asset. Traders deploy this spread when they expect the price of the underlying asset to remain below a certain level, often a resistance point, or to move in a bearish direction.

This strategy is ideal when implied volatility is high and anticipated to contract. The bear call spread is most effective when the asset is expected to remain consolidated or bearish. The maximum profit is achieved if the underlying asset closes at or below the lower strike price at expiration and is equal to the net premium received. The maximum loss occurs if the underlying closes at or above the higher strike price and is calculated as the difference between the strike prices minus the net premium received.

The breakeven point is the lower strike plus the net premium received. While the risk is limited, it is higher than the reward, which is restricted to the premium collected when initiating the trade.

4. Bull Put Spread

A bull put spread is a credit spread executed on the put side. It gets its name from the expectation that the price will not fall below a certain strike price. The spread is established by selling a put option with a higher premium and buying a put with a lower premium as a hedge.

This strategy is used when traders expect a trend reversal or correction to the upside, or at least expect the asset to remain consolidated, often finding support at a significant price point. The bull put spread works well when volatility is high and expected to decrease. The maximum profit is achieved if the underlying closes at or above the higher strike price by expiration, which equals the net premium received. The maximum loss occurs if the underlying closes at or below the lower strike price and is the difference between the strike prices minus the net premium received. The breakeven point is the higher strike minus the net premium received.

Both risk and reward are limited and predefined, with the risk occurring if the underlying falls below both strikes, and the reward limited to the credit received when opening the spread.

5. Diagonal Spread

A diagonal spread is a more advanced options strategy that combines elements of both vertical and calendar spreads. It involves buying and selling the same type of option (either calls or puts) with different strike prices and different expiration dates. Typically, the option with the nearer expiration is sold to take advantage of time decay, while an option with a later expiration is purchased as a hedge, providing protection if volatility rises.

Traders use diagonal spreads when they expect moderate movement in the underlying asset and wish to benefit from time decay on the short-term option.

This strategy is best deployed if volatility is expected to rise, as the long-term hedge benefits from increased volatility. The diagonal spread can be adjusted to suit bullish, bearish, or neutral market views by selecting appropriate strike prices. The maximum profit depends on how the underlying asset moves concerning both strike prices and how volatility and time decay play out, with profit typically maximized if the underlying price hovers near the short strike at the short option’s expiration.

The maximum loss can be significant, usually equal to the net premium paid or the loss in value if the long option decays too much or moves far out of the money. The breakeven point is complex to calculate, as it fluctuates with volatility and price movement. The risk is generally limited to the net premium paid, though risks may rise if the position is not managed as the short leg expires.

The reward is flexible and can be attractive if the price remains near the short strike, with the long leg benefiting from volatility increases and the short leg from theta decay. Advanced traders may roll profits from the hedge if volatility rises unexpectedly.

6. Vertical Spread

A vertical spread refers to any options trading strategy involving the simultaneous buying and selling of the same type of option—either call or put options—on the same underlying asset and expiration date, but at different strike prices.

All the previously discussed strategies, except the diagonal spread, are forms of vertical spreads. The vertical spread classification includes the bear put spread, bull call spread, bear call spread, and bull put spread.

Each variant offers defined risk and reward characteristics and can be tailored to bullish or bearish market expectations, allowing traders to profit from directional moves while managing risk more effectively than with single-leg options trades.

Why Use an Options Spread Strategy?

Options spread strategies provide traders with defined risk-reward parameters while reducing the capital required compared to outright options or futures positions. Traders employ spreads to capitalize on specific market views while protecting against the full impact of adverse price movements, time decay, and volatility shifts.

Cost reduction stands as a primary advantage, especially relevant in the Indian market where options premiums often run higher than global averages due to persistent volatility. A Nifty call option purchased individually might cost ₹12,000, while implementing a bull call spread reduces this outlay to ₹5,000-6,000 while maintaining substantial upside potential.

Risk mitigation represents another crucial benefit – credit spreads like iron condors cap maximum losses regardless of how far the underlying moves against the position, eliminating the unlimited risk associated with naked option selling.

Spreads effectively neutralize specific market forces that harm standalone options positions. Time decay devastates long options but impacts certain spread configurations minimally. Implied volatility changes impact spreads less severely than single options positions, creating more predictable outcomes.

Traders face substantial margin requirements for naked options selling – often 25-40% of the contract value as per SEBI regulations – but spread strategies reduce these requirements by 50-70%, enhancing capital efficiency.

When to Use an Options Spread Strategy?

Options spread strategies prove most effective during specific market conditions that align with the particular spread’s profit profile and risk characteristics. Traders deploy different spread configurations based on price direction expectations, anticipated volatility changes, and desired risk-reward parameters.

Bullish spreads like bull call or bull put spreads excel during gradual uptrends seen in sectors like IT after positive quarterly results announcements. Bear spreads perform optimally during controlled downtrends, as witnessed in pharma stocks following regulatory concerns. Neutral strategies including iron condors and butterflies generate consistent returns during consolidation phases, particularly evident in Nifty during pre-Budget periods where markets typically trade sideways awaiting policy clarity.

High implied volatility environments signal opportunities for credit spreads – many Traders successfully deployed these during the market uncertainty surrounding the 2024 general elections. Conversely, low volatility periods favor debit spreads, especially ahead of known volatility catalysts like earnings releases or monetary policy announcements.

Calendar and diagonal spreads capitalize on term structure anomalies in the volatility curve, most profitable during transitions between volatility regimes.

Indian options markets display unique timing considerations – weekly expiry cycles create additional spread opportunities compared to international markets.

Market data from NSE reveals spread strategies implemented on Mondays or Tuesdays (early in expiry week) outperform those executed later in the week by approximately 18%. Traders time spread implementations according to specific technical levels rather than arbitrary entry points, establishing positions when price approaches significant support/resistance zones that correspond with strike price selection.

How Option Greeks Affects Options Spread Strategy?

Option Greeks determine the behavior of spread strategies by quantifying how each component responds to changes in price, time, volatility, and interest rates. Spread positions manipulate these sensitivity measures to create favorable risk profiles that capitalize on specific market views while neutralizing undesired exposures.

Delta measures directional exposure, with spreads strategically balancing positive and negative deltas to achieve desired directional bias. Bull spreads maintain positive net delta, benefiting from upward moves in stocks, while bear spreads establish negative net delta, profiting from declines in overvalued sectors.

Theta quantifies time decay effects, with credit spreads harvesting positive theta as sold options lose value faster than purchased options – Traders exploit this dynamic through iron condors on Bank Nifty during low-volatility periods.

Vega represents volatility sensitivity, crucial in India’s market where implied volatility fluctuates dramatically around events. Calendar spreads create positive vega positions, thriving during pre-earnings volatility expansions on stocks.

Vertical spreads typically reduce vega exposure compared to naked options, making them suitable during uncertain volatility regimes. Gamma measures the change in delta as prices move, with spreads reducing gamma risk that frequently destabilizes naked option positions during sharp market moves.

Professional Indian options traders meticulously monitor net Greek exposures across spread portfolios, targeting specific values based on market outlook. NSE data indicates successful spread traders maintain delta-to-theta ratios between 3:1 and 5:1 during trending markets, shifting to 1:3 during sideways conditions.

Advanced platforms from Indian brokerages now offer Greek calculators specifically calibrated to local market volatility patterns, enabling more precise spread construction and management.

How to Trade using Options Spread Strategy?

The proper way to trade using an options spread contains five key steps. Below are the details.

1. Identify Asset

Asset selection forms the foundation of successful spread trading, requiring analysis of liquidity, volatility characteristics, and technical setups. Traders prioritize high-volume underlyings with tight bid-ask spreads to minimize execution costs and slippage. Nifty and Bank Nifty options lead in popularity due to their exceptional liquidity, with average daily volumes exceeding 4.2 million contracts and bid-ask spreads typically under 0.15%.

Large-cap stocks offer ideal spread opportunities due to their robust options chains and predictable volatility patterns. Sector-specific ETFs provide targeted exposure for thematic spread strategies without single-stock risk. Avoid illiquid underlyings showing bid-ask spreads exceeding 1% of premium value, as these create execution difficulties and reduce profitability.

Technical analysis guides timing decisions, with successful Indian spread traders entering positions near key support/resistance levels.

Consider the example of a trader identifying ICICI Bank approaching strong resistance at ₹1,150 after a 15% rally.

Rather than directly shorting the stock, the trader implements a bear call spread to benefit from limited upside while defining maximum risk. Fundamental catalysts like upcoming earnings or policy announcements influence volatility expectations, crucial for selecting appropriate spread structures.

2. Determine Strike Price, Expiration Dates

Strike price and expiration selection directly impacts risk-reward parameters and probability of success for spread strategies. Traders analyze implied volatility skew, technical levels, and time horizon to optimize these critical variables. Strike selection balances probability of profit against potential return, with wider spreads increasing both maximum gain and risk.

For directional spreads, successful Traders position short strikes at technical resistance (for bear spreads) or support (for bull spreads) levels. Options with 30-45 days remaining typically provide optimal balance between premium collection and time decay acceleration.

Strike width affects capital efficiency and leverage – a 2023 study of Traders revealed most successful spreads employed strike differences of 5-7% of underlying price. Volatility term structure influences expiration selection, particularly for calendar spreads where traders exploit differences between near and far-dated implied volatility. During the 2024 Union Budget announcement, savvy traders implemented Nifty calendar spreads selling February options (elevated IV of 22%) while purchasing March options (normal IV of 16%), capitalizing on post-event volatility contraction.

Moneyness selection correlates with win rate – NSE data shows credit spreads with short strikes at 0.25-0.30 delta achieve 68% success rates compared to 57% for at-the-money spreads. Traders adjust these parameters based on implied volatility percentile rankings, selecting farther OTM strikes during high volatility periods and closer strikes during low volatility environments to maintain consistent probability thresholds.

3. Execute The Trade

Trade execution requires strategic order placement to minimize slippage while ensuring complete fill of all spread components. Traders employ specialized order types and execution techniques to optimize entry and exit prices in India’s fast-moving options markets. The spread order type, available with most major Indian brokerages, executes all legs simultaneously at specified price differentials.

Mid-market pricing provides the starting point for limit orders, with adjustments based on order book depth and urgency. Liquidity affects execution quality significantly – a 2024 NSE study demonstrated spreads on index options typically executed within 0.2% of mid-market compared to 1.2% for less liquid single-stock options.

Timing execution to market microstructure patterns improves results – experienced Traders avoid order placement during the first 15 and last 30 minutes of trading when spreads widen due to volatility and position squaring. Breaking larger orders into smaller tranches reduces market impact for institutional-sized positions. A Mumbai-based fund manager executing 500-lot Nifty iron condors employs this approach, splitting orders into 50-lot increments placed at 15-minute intervals.

Advanced traders utilize volatility-based execution triggers rather than price-based entry signals. Indian derivatives platforms increasingly offer specialized spread trading screens showing theoretical values, Greek exposures, and margin requirements to streamline the execution process.

4. Profit Booking & Stop Loss

Profit booking and stop-loss implementation provide critical discipline to spread trading, ensuring winners reach targets while preventing catastrophic losses. Research from Indian brokerages shows traders with documented exit rules achieve 35% higher annual returns than those trading without predetermined exit parameters. Strategic exits maximize winning trades while minimizing drawdowns.

Target-based exits typically occur at 50-70% of maximum theoretical profit rather than waiting for 100%, increasing winning percentage while freeing capital for new opportunities. A high-frequency options trader at a Bengaluru prop firm documented superior results exiting Nifty bull call spreads at 60% of maximum profit, achieving 18% higher annual returns compared to holding until expiration. Time-based exits close positions that haven’t reached profit targets within specified durations, preventing capital lockup in underperforming trades.

Stop losses for debit spreads typically trigger at 50-60% of initial investment, while credit spread stop losses activate when losses reach 150-200% of initial credit received. These parameters balance loss prevention against avoiding premature exits during normal market fluctuations. Consider a recent case where an Ahmedabad-based trader implemented Bank Nifty put credit spreads receiving ₹4,200 premium with a mechanical stop loss at ₹8,400 loss (200% of credit received), which triggered during a sharp market decline, preventing further losses as the index continued dropping.

5. Manage Position

Position management transforms static spread trades into dynamic strategies responding to changing market conditions and evolving risk parameters. Proactive adjustments protect profits, minimize losses, and extend favorable positions based on market developments.

Rolling techniques extend profitable trades while avoiding expiration risks. Consider a documented example where a Chennai-based options trader rolled a profitable TCS bull put spread forward from April to May expiration, maintaining the same strikes while collecting additional premium and extending the profit window.

Defensive adjustments convert threatened positions into more favorable structures – transitioning an underwater bull call spread into a butterfly by selling higher strike calls reduces maximum loss while maintaining upside potential if the underlying recovers.

Greeks management involves rebalancing position sensitivities as market conditions evolve. Traders maintain delta exposure within predetermined ranges relative to account size, typically 0.5-1.5% of equity per position.

Early closure prevents weekend gap risk for weekly options positions. Position correlation monitoring prevents overexposure to specific market factors – many institutional spread traders in India limit sector concentration to 25% of portfolio allocation, preventing excessive damage from specific events. Sophisticated traders implement laddered positions across multiple expiration cycles, creating consistent income streams while diversifying time-based risks.

What is the Maximum Profit & Loss on an Options Spread Strategy?

Maximum profit and loss for options spread strategies remain precisely defined at the moment of trade execution, providing traders with clear risk parameters before market exposure begins. Each spread type creates unique profit and loss boundaries based on the specific combination of options purchased and sold.

Vertical debit spreads (bull call and bear put) limit maximum profit to the difference between strike prices minus the net premium paid. Consider a bull call spread with strikes at ₹3,000 and ₹3,100 costing ₹40 net premium – maximum profit equals ₹60 per share regardless of how high the stock price climbs. Maximum loss for these debit spreads equals the initial premium paid (₹40 per share in this example), occurring if the stock moves unfavorably beyond the spread’s profitable range.

Credit spreads (bull put and bear call) flip this relationship – maximum profit equals the net premium received, while maximum loss equals the difference between strike prices minus the net premium received. Traders gravitate toward credit spreads on index options due to consistent premium erosion characteristics. Iron condors combine two credit spreads, maintaining defined risk while expanding the profitable price range.

Calendar and diagonal spreads create curved profit/loss profiles with maximum values determined by volatility changes and price movement relative to strikes. Traders implement position management rules triggered at 50-70% of maximum boundaries rather than targeting absolute values.

What are the Risks of Options Spread Strategy?

Options spread strategies carry specific risks despite their defined maximum loss characteristics and strategic advantages over single options positions. These risks include gap risk, execution slippage, liquidity constraints, and assignment complications that frequently impact Traders.

Gap risk materializes during overnight price jumps exceeding spread boundaries, particularly following unexpected corporate events or global market disruptions.

A recent example occurred when Adani Group stocks gapped down 15-20% following a negative research report, rendering protective put spreads less effective than anticipated. Execution slippage erodes theoretical profits, especially in less liquid single-stock options where bid-ask spreads frequently exceed 1-2% of the option value.

Liquidity constraints affect position adjustments and closing trades, forcing suboptimal executions or preventing timely exits. The Indian options market exhibits pronounced liquidity stratification, with Nifty options trading over 4 million contracts daily while even large-cap single stocks sometimes struggle with depth.

Early assignment risk impacts credit spreads, particularly during dividend events when rational exercise becomes more likely. Pin risk occurs when expiration prices land near strike prices, creating uncertainty about assignment and requiring weekend risk management. Margin expansion during volatility spikes forces poorly capitalized traders to liquidate positions prematurely – SEBI regulations implemented in 2023 increased margin requirements for certain spread strategies during high volatility periods, catching many retail traders unprepared.

Is Options Spread Strategy Profitable?

Yes, options spread strategies prove profitable for disciplined traders applying proper selection criteria and risk management principles. Spread trading delivers consistent returns by exploiting specific market inefficiencies while defining maximum risk parameters.

Vertical spreads on index options demonstrate the highest win rates, exceeding 60% for positions aligned with prevailing trends. Traders enhance profitability through portfolio approaches, maintaining 8-12 concurrent spread positions across uncorrelated underlyings.

Time decay contributes a substantial edge to credit spread strategies, particularly in high implied volatility environments frequently seen in India’s markets. Risk-defined characteristics protect capital during adverse movements, creating superior long-term performance compared to directional options or futures positions.

Is Options Spread Strategy Bullish or Bearish?

Options spread strategies express both bullish and bearish market views depending on their specific configuration. The directional bias emerges from the particular combination of options purchased and sold rather than from the spread technique itself.

Bull call spreads and bull put spreads establish positive delta positions, profiting from upward price movements in stocks. Bear call spreads and bear put spreads create negative delta exposures, generating returns during price declines in sectors like metals or during broader market corrections. Neutral strategies including iron condors and butterflies maintain minimal directional bias, benefiting from price stability rather than directional movement. Traders select appropriate spread structures based on technical analysis and fundamental outlook.

What are Alternatives to Options Spread Strategy?

Alternatives to options spread strategy include Straddles and strangles, Iron condors, Covered calls and protective puts etc.

Straddles and strangles exploit high volatility environments by purchasing both calls and puts with identical or different strike prices. Traders frequently deploy these during uncertain events like Union Budget announcements or RBI policy meetings. A Nifty straddle implemented before the 2024 general election results delivered 85% returns as the market made significant moves following the outcome announcement. These strategies profit from price movement magnitude regardless of direction but require sufficient volatility to overcome the substantial premium outlay.

Iron condors capitalize on range-bound markets by combining a bull put spread with a bear call spread, creating a wide profitable price zone with defined maximum risk. These strategies thrive during consolidation periods commonly seen in Indian markets between earnings seasons. The strategy generates income through premium collection while defining maximum risk.

Covered calls and protective puts combine stock positions with options to modify risk characteristics. Traders holding blue-chip stocks frequently enhance portfolio returns by selling out-of-the-money calls against existing holdings. This strategy generates additional income while defining upside exit prices. Conversely, protective puts function as portfolio insurance, with institutional investors purchasing downside protection for core holdings during uncertain market periods.

These stock-option combinations modify return distributions compared to outright stock ownership or pure options strategies.

What’s The Difference Between Options Spread vs Straddle?

Options spreads combine multiple options at different strike prices to create defined risk-reward profiles with directional bias. Straddles consist of purchasing both calls and puts at the same strike price, profiting from significant price movement regardless of direction.

Spreads typically reduce cost basis through the sale of offsetting options, making them capital-efficient for directional plays on Nifty or Bank Nifty. Vertical spreads limit both potential loss and profit, appealing to risk-conscious Traders. Straddles require larger volatility to overcome their considerable premium outlay but offer unlimited profit potential during major market events. Traders deploy straddles before Union Budget announcements, RBI policy decisions, and corporate earnings releases.

Previous Article

Previous Article

58")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 60")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 61")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 62")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 66")

No Comments Yet.