A bear call spread is an options strategy designed to profit from a decline or sideways movement in the underlying asset’s price. A bear call spread involves buying a call option at a higher strike price while simultaneously selling a call option at a lower strike price on the same underlying asset and expiration date.

This strategy creates a net short-call position that benefits from a fall in the underlying price. The maximum profit is capped at the net premium received from the difference between the sold lower strike call and the purchased higher strike call. The maximum loss is limited to the difference between the strike prices minus the premium received.

The bear call spread offers defined, limited risk and capped profit potential. It is used when moderately bearish on an asset. It allows profitable positioning for a downward move while defining max loss. The sold call’s premium income lowers the cost basis compared to just buying a naked call option.

The advantages of a bear call spread include lower capital requirements than shorting stock, limited risk, and the ability to profit from a sideways or declining market. The main disadvantages are the capped profit potential and negative vega exposure if implied volatility declines. Overall, the bear call spread offers a flexible, lower-risk way to capitalize on a neutral to bearish outlook.

What is a Bear Call Spread?

A bear call spread is an options trading strategy that is used when the trader expects the price of the underlying asset to decrease or remain relatively stable. Bear call spread involves simultaneously buying and selling call options on the same underlying asset, with the same expiration dates but at different strike prices.

Specifically, a bear call spread is created by the following.

Buying a call option with a higher strike price (this option has a lower premium since it is farther out of the money).

Selling a call option with a lower strike price (this option has a higher premium since it is closer to being in the money).

The trader buys the higher strike call to offset unlimited losses if the underlying price increases dramatically. However, the net effect of the two call options creates a bearish position that profits if the asset price stays below the lower strike price at expiration.

The maximum profit potential on a bear call spread is equal to the net premium received from the two call options. This profit is realized if the underlying price is below the lower strike price at expiration. In this case, both options expire worthless, and the trader keeps the net premium.

The maximum loss is capped at the difference between the strike prices minus the net premium received. This loss occurs if the underlying price rises above the higher strike call option at expiration. In this case, the purchased higher strike call expires worthless while the written lower strike call is assigned, and the trader has to buy the asset at the lower strike price.

An example of a bear call spread would be the following.

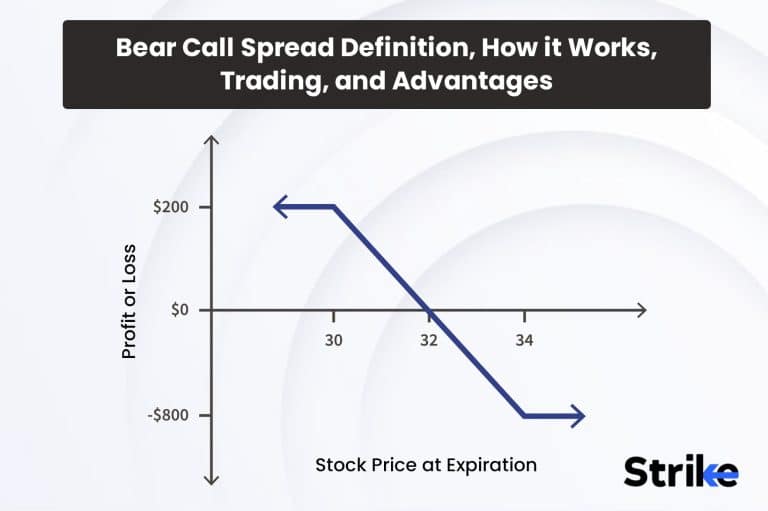

- Buy 1 XYZ 60 call for Rs. 100.

- Sell 1 XYZ 50 call for Rs. 300.

Net Premium Received = Rs. 300 – Rs. 100 = Rs. 200

Maximum Profit = Net premium received = Rs. 200

Maximum loss = difference in strike prices – Net Premium received

= Rs. 1000 – Rs. 200 = Rs. 800

Both call options expire worthless if XYZ stock closes below Rs. 50 at expiry, and the trader keeps the Rs. 200 credit. The 50 call is assigned if XYZ closes over Rs. 60. The trader then purchases XYZ for Rs. 50 and sells it for the higher market price, with a maximum loss of Rs. 800.

The breakeven point is the lower strike price plus the net premium received. In this case, it would be Rs. 50 + Rs. 200 = Rs. 52. Below Rs. 52, the trade is profitable, while above Rs. 52, it loses money.

The bear call spread benefits from time decay, just like individual short calls. As expiration approaches, the time value of the options declines, working in the trader’s favor. Volatility also helps the bear call spread. Higher implied volatility increases the premiums and potential profit.

This strategy generates income but is limited by the width between the strike prices. Wider spreads mean higher potential profit but also larger capital requirements. The maximum loss also increases with wider spreads.

Bear call spreads are used when neutral to moderately bearish on the underlying. They offer defined, limited risk compared to shorting the stock or selling naked calls. Traders often use them to generate income from high implied volatility or when they expect volatility to decline.

The risks are that the underlying price increases dramatically and exceeds the higher strike call. Upside moves sometimes quickly erase profits from the net premium. Time decay also accelerates in the last month, so early assignments prior to expiration sometimes result in losses.

Is Bear Call Spread the same as call credit spread?

Yes, a bear call spread is the same trading strategy as a call credit spread. The two terms are interchangeable and refer to the same options trade construction.

A call credit spread, also known as a bear call spread, is executed by selling a call option at a lower strike price and buying a call option at a higher strike price, with both having the same underlying asset and expiration date. This generates a net credit or premium received into the trader’s account; hence, the name “credit” spread.

The call options were sold and purchased from a spread trade with defined risk and capped profit potential. The short call generates income, while the long call caps the loss if the underlying rises. The net credit lowers the breakeven point and provides downside protection.

A call credit spread has a bearish bias, seeking to profit from the underlying stock or asset trading sideways or declining moderately through expiration. The maximum gain is equal to the net credit received upfront. The maximum loss is the difference between the strike prices minus the initial credit.

The breakeven point is the strike of the short call plus the net credit. Below this level at expiration, the short call expires worthless, and the trader keeps the full credit as profit. The spread begins to lose money if the stock is higher than breakeven at expiration.

How does Bear Call Spread work?

A bear call spread is an options strategy constructed to profit from a neutral to moderately bearish outlook on the underlying asset. It involves the simultaneous purchase and sale of call options at different strike prices to create a net credit position.

Specifically, a bear call spread is established by the following.

- Buying a call option at a higher strike price.

- Selling a call option at a lower strike price.

- Both calls share the same expiration date and underlying security.

Since the call sold is at a lower strike and, therefore, has a higher premium, a net credit is received when entering the trade.

The mechanics behind a bear call spread are as follows.

The long call option with the higher strike price is brought to protect against unlimited losses in case the underlying stock makes a sharp move to the upside. This call essentially functions as a hedge.

Meanwhile, the short call option at the lower strike price is sold to generate income in the form of credit received. This call is closer to being in-the-money and thus commands a higher premium.

The net effect of the long and short call positions creates a bearish options trade. The maximum gain is capped at the net credit amount, realized if the underlying is below the short call strike at expiration.

The maximum potential loss is also defined. It is limited to the difference between the strike prices minus the net credit. Losses are capped because the long higher strike call protects the position from any further losses if the underlying rallies above that strike.

As expiration approaches, if the underlying is trading below the short call strike, both options expire worthless, and the trader keeps the full credit. This is the optimal outcome.

The short call expires in-the-money and is executed or assigned if the stock is between the strike prices. The long call expires worthless. Here, the trader’s loss depends on the stock price but is capped at the defined maximum.

Above the long call strike, losses are maximal but limited. The long call offsets further losses upon exercise.

A key benefit of the bear call spread is that it relies on time decay, just like individual short call positions. As expiration approaches, the time value of both options declines, which favors the net credit position.

Volatility also impacts this strategy. An increase in implied volatility will tend to increase the premiums and, therefore, the potential profit. A decrease in volatility raises the chance of a favorable expiration.

Proper position sizing is critical to effectively utilize a bear call spread. The maximum loss dictates how many contracts are traded, given one’s risk tolerance. Strike width also impacts sizing and risk parameters.

What is the importance of Bear Call Spread in Options Trading?

A bear call spread is an important options trading strategy that serves multiple purposes and provides flexibility for options traders. Here are six of the key reasons why bear call spreads are an important component of an option trader’s repertoire.

Defines Risk

One of the primary benefits of a bear call spread is it clearly defines risk. The maximum loss on the trade is limited to the difference between the strike prices of the short and long calls minus the initial net credit received. This allows the trader to enter a bearish options position, knowing the full extent of the potential downside. The long call cap on the spread prevents unlimited loss below the higher strike price. Defined and limited risk is an important prerequisite for responsible trading.

Generates Income

The proceeds collected from selling the initial call option when opening the bear call spread provide immediate income. This premium credit lowers the breakeven point and offers downside protection in the form of cash in the trader’s pocket. Generating income through options premiums plays an integral role for traders in meeting profit goals. The bear call spread is one practical strategy to accumulate credits.

High Probability of Profit

Due to the cushion provided by the net credit, a bear call spread has a high probability of producing a profitable trade if properly managed. The market only needs to trade sideways or fall moderately to expiration for the short call to expire worthless and allow the trader to capture the full credit. This probabilistic edge is an important advantage the strategy offers compared to long options trades or simply shorting a stock.

Lower Capital Requirements

Bear call spreads allow options traders to put on positions with a defined, capped risk with less capital outlay than other approaches. Only the difference between the long and short call strike prices is required, not the full amount for buying an outright long call or shorting shares of stock. The ability to participate in options trading while conserving capital and diversifying across more trades is an important practical aspect of this strategy.

Hedge Against Long Stock Positions

For traders holding long stock positions, bear call spreads present an opportunity to partially hedge against potential declines. By selling calls against long shares, the premium income cushions the downside. While capping unlimited upside potential, a bear call spread on a long stock portfolio limits losses. This hedging capability makes it an important tool for risk management.

Take Advantage of High Implied Volatility

Options traders profit from high option premiums by using bear call spreads when they anticipate a period of increased but decreasing implied volatility. By selling expensive short-term calls, traders benefit from the expectation for falling IV and expiration decay. As volatility reverts lower, the short calls lose value, allowing the spread to gain profit.

How does Bear Call Spread differ from other Vertical Spreads?

A bear call spread is a type of vertical spread strategy constructed using call options. Other common vertical spreads include bull call spreads, bear put spreads, and bull put spreads. While vertical spreads share some similarities, bear call spreads have distinct characteristics versus other vertical constructions.

The six key traits that differentiate bear call spreads are the following.

Bearish Bias

Unlike bull call and bull put spreads, which have a bullish bias, bear call spreads have an outright bearish bias. They seek to generate profit from the underlying stock or asset falling or experiencing limited upside through the options expiration. The other verticals aim to profit from upside momentum. This divergent market outlook is a core differentiation.

Credit Received

Bear call spreads result in a net credit or premium received into the trader’s account when initiating the trade. This contrasts with bull call and bull put spreads, which create net debits. The proceeds from the short call sold to reduce the cost of the long call purchased. This lowers breakeven and provides downside protection.

Capped Maximum Profit

The maximum profit potential on a bear call spread is limited to the initial net credit amount received. Bull call and bull put spreads have unlimited maximum profit potential. The long call in the bear call spreads caps upside profit if the underlying declines sharply. There is no profit cap to the upside in bull spreads.

Lower Capital Requirements

More attractive capital requirements are possible with bear call spreads. Only the difference between the strike prices and the credit is required. Bull spreads require full payment of the spread width to open the trade. The efficient use of trading capital is a key benefit of the bear call spread.

Defined Maximum Risk

Maximum loss is strictly defined as the difference between the call strike prices minus the initial credit for bear call spreads. Bull spreads have similarly defined risk parameters. All vertical spreads exhibit capped and known worst-case loss scenarios.

Management Differences

Bear call spreads are often managed differently than bull spreads. Bear call spreads sometimes are closed early, around 50% profit targets. Bull spreads are typically held until expiration or just before to maximise the open-ended profit.

While vertical spreads share commonalities, bear call spreads diverge from other vertical constructions based on their bearish bias, net credit received, capped profit upside, lower capital needs, and differentiated management tactics.

What is the maximum profit on a Bear Call Spread?

The maximum profit on a bear call spread is equal to the net credit received when opening the options position. This credit comes from selling the lower strike call option and buying the higher strike call.

Specifically, the formula is as stated below.

Maximum profit = Net Premium Received.

Where,

Net premium Received = Premium from Short Call – Premium from Long Call

For example, consider this bear call spread mentioned below.

- Sell 1 XYZ 50 Call at Rs. 2.00.

- Buy 1 XYZ 55 Call at Rs. 1.00.

The net credit received is as stated below.

Rs. 2.00 (short call premium) – Rs. 1.00 (long call premium) = Rs. 1.00

Therefore, the maximum profit potential on this bear call spread is Rs. 1.00.

This Rs. 1.00 net credit is the most the trader can make on the position. It represents the difference between the premium collected on the short call and the premium paid for the long call.

The maximum profit is achieved if the underlying stock price is below the short call strike price at expiration. In that case, both call options expire worthless, and the trader gets to keep the full net credit taken in.

Essentially, the formulas show that the maximum gain on the spread is defined and limited to the credit amount collected at the outset when putting on the bearish call spread.

Unlike positions with unlimited profit potential, the bear call spread has a clearly defined maximum gain. This definitively quantifies the reward component of the options position.

What is the maximum loss on a Bear Call Spread?

The maximum loss on a bear call spread is equal to the difference between the strike prices of the short and long calls minus the initial net credit received.

The formula is as follows.

Maximum loss = Strike Price of Short Call – Strike Price of Long Call – Net Premium Received

Where,

Net premium Received = Premium from Short Call – Premium from Long Call

For example, consider this bear call spread mentioned below.

- Sell 1 XYZ 50 Call at Rs. 2.00.

- Buy 1 XYZ 55 Call at Rs. 1.00.

The net credit received is Rs. 2.00 – Rs. 1.00 = Rs. 1.00

The strike prices are 50 for the short call and 55 for the long call.

Plugging this into the formula, we get the following.

Maximum Loss = 50 – 55 – 1.00 = Rs. 4.00

Therefore, the maximum loss on this bear call spread is Rs. 4.00.

This Rs. 4.00 represents the most the trader can lose on the position. It is the difference between the strike prices reduced by the net credit collected.

The maximum loss occurs if the underlying stock price rises above the long call strike at expiration. In this case, the long 55 call expires worthless while the short 50 call gets assigned, forcing the trader to buy the stock at Rs. 50.

The key takeaway is that the maximum loss is defined and capped on a bear call spread. The long call hedge protects against the unlimited downside. This quantitatively defines the risk of the trade.

How do traders break even in Bear Call Spread?

The breakeven point for a bear call spread is the strike price of the short call plus the initial net credit received when opening the position. At this underlying price, the trade breaks even – neither making nor losing money.

The formula for the breakeven is the one stated below.

Breakeven = Strike Price of Short Call + Net Premium Received

Where,

Net premium Received = Premium from Short Call – Premium from Long Call

For example, consider this bear call spread mentioned below.

- Sell 1 XYZ 50 Call at Rs. 2.00.

- Buy 1 XYZ 55 Call at Rs. 1.00.

Net Premium Received = Rs. 2.00 – Rs. 1.00 = Rs. 1.00

Short Call Strike Price = 50

Plugging this into the formula, we get the following.

Breakeven = 50 + 1.00 = Rs. 51

In this case, the breakeven point is Rs. 51. At this underlying price, the bear call spread would neither make nor lose money. Below Rs. 51, it profits; above Rs. 51, it starts losing.

Essentially, the short call strike plus the net credit amount represents the ‘pivot point’ at which the trade goes from positive to negative territory.

The intuition is that the net credit lowers the effective breakeven versus just the short-call strike alone. This credit cushion helps the position remain profitable at higher prices.

Four keynotes on bear call spread breakeven points are listed below.

- Wider spreads mean higher breakevens and a wider breadth of profitability.

- Try to establish spreads with breakevens close to the current stock price for higher probability of success.

- The breakeven sets the floor for where the position turns profitable.

- Breakevens rise when more credit is collected upfront.

What is the ratio for Bear Call Spread?

The ratio of a bear call spread refers to the number of short-call option contracts sold relative to the number of long-call option contracts purchased when establishing the position. The standard ratio is 1:1 – meaning one short call for every long call option bought.

For example, a typical bear call spread is as stated below.

- Sell 1 XYZ 50 Call

- Buy 1 XYZ 55 Call

Here, the ratio is 1:1, with one short call for every long call. This is considered the standard ratio.

However, traders adjust the ratio to be higher or lower depending on their objectives.

Higher ratio – More aggressively bearish

A higher ratio means selling more short calls than long calls purchased.

For example:

- Sell 3 XYZ 50 Calls

- Buy 1 XYZ 55 Call

This creates a more bearish 3:1 ratio spread. The higher number of short calls sold generates more premium income but also increases risks if the stock rises.

Lower ratio – More conservative

A lower ratio involves purchasing more long-call contracts than short-calls sold.

For example:

- Sell 1 XYZ 50 Call

- Buy 2 XYZ 55 Calls

This 1:2 ratio spread has a more conservative tilt. The extra-long call provides more upside protection but also costs more to establish the trade.

The standard 1:1 ratio bear call spread is balanced in terms of risk versus reward. Adjusting the ratio allows for fine-tuning the payoff profile.

Higher ratios are more aggressive, with higher profit potential but also greater risks.

Lower ratios are more conservative with lower breakevens but also limit profit upside.

Traders weigh their level of risk tolerance and desired premium income when choosing a ratio. Some traders always use the 1:1 and simply adjust other parameters like expiration or strike width.

How to initiate a Bear Call Spread strategy?

Executing a bear call spread involves methodically establishing the long and short call option positions. Follow the steps mentioned below.

First, decide on the ideal options to use for the spread.

1. Select the underlying stock you have a neutral to bearish outlook on. Analyze its trends, support/resistance, and fundamentals.

2. Choose the expiration date for the options contracts. Pick a suitable time frame aligned with your market thesis. Nearer-term expirations require a stronger directional conviction.

3. Determine the ideal strike prices to use for the spread’s call options. Typically, the short strike is at, near, or slightly below the current stock price. The long strike is farther out-of-the-money. Consider volatility and risk parameters when selecting strikes.

4. Decide on the ratio for the spread – the number of short calls versus long calls. The standard 1:1 ratio is a balanced approach. Use higher or lower ratios to fine-tune the risk-reward profile.

Once the ideal options chain is identified, execute the trade.

5. First, sell the desired number of call option contracts at the lower strike price to open the short call position. Be sure to sell the calls at an appropriate limit price to collect your minimum desired premium.

6. Next, buy the desired number of call contracts at the higher strike price to establish the long call hedge position. Try to get fills at or below the limit prices to control the net debit spent.

7. Monitor the fills to ensure execution at favorable prices. The net credit should align with profit goals. Adjust limits as needed.

8. Upon execution, confirm the net credit received by subtracting the long call premium paid from the short call premium collected. This net credit represents the maximum potential profit.

9. Calculate the maximum risk, which equals the difference between the strike prices minus the net credit. Also, determine the breakeven point, which is the short strike plus net credit.

Following these steps allows a trader to efficiently initiate a new bear call spread position with a clear sense of the risk-reward parameters and probability of profit. Precise execution, favorable option pricing, and constant monitoring of fill prices are vital for optimizing the spread.

What is the best Bear Call Spread strategy?

The best bear call spread strategy balances the ability to generate attractive potential income against managing risks if the underlying stock moves higher. Specifically, the ideal approach involves the following.

Legging into the Spread

Rather than entering the long and short calls simultaneously, leg into the spread by first selling the short call and then waiting to buy the long call. This allows selling the short call at the best possible premium, then legging into the long call at an ideal entry point. Timing the entries thoughtfully improves overall pricing.

Managing Risks

Carefully select the strike prices to limit maximum potential losses if the stock rallies. Wider spreads increase risk. Define risk tolerance and ensure the spread width aligns. Also, engage in active trade management as the stock price changes.

Maximising Credit at Entry

Sell the short calls strategically at times of high implied volatility to collect larger premiums. Also, use limit orders to ensure filling the short strike at optimal prices. The higher the initial credit, the greater the chance of profitability.

Exploiting Volatility Skew

Volatility skew refers to out-of-the-money put options having higher IV than OTM call options. As call skew limits the possible earnings from call credit spreads, put credit spreads should be preferred when skew is substantial.

Adjusting the Ratio

Use a higher call ratio when neutral outlooks prevail to increase credit income. But reduce the ratio when bearishness strengthens to limit downside risks. Dynamically adjust the ratio to optimize the risk-reward profile.

Managing Early if Needed

To avoid a maximum loss, close the spread if the stock climbs swiftly towards the long call strike early in the deal. Protect capital to fight another day rather than hoping for a reversal.

Setting Realistic Profit Goals

Given the capped upside on bear call spreads, set achievable profit targets, such as aiming to capture 30-50% of the maximum income. Limit expectations and close winners early.

When is the best time to enter a Bear Call Spread?

There are certain optimal market conditions and timing factors that provide the best opportunities to enter a bear call spread. The best times to enter a bear call spread are when the following occurs.

Implied Volatility is High

Periods of elevated implied volatility provide richer call option premiums and greater income potential when selling calls. Higher IV results in greater extrinsic value priced into calls, enabling selling at inflated premiums to maximize credit. Initiating bear call spreads when the IV percentile is at the upper end Historically provides ideal conditions to get the most bang for the buck.

Price Trend is Bearish or Range-Bound

Technical analysis showing an established downtrend or sideways price action offers an advantageous backdrop for profiting from a bear call spread. With limited upside momentum expected, short calls are unlikely to face heavy assignment pressure. Recent lower highs and lower lows confirm near-term bearishness.

Days Before Earnings or Events

In the one to two-week lead-up to known binary events like earnings reports, product releases, or FDA rulings, uncertainty rises along with IV. However, post-event volatility crashes due to the elimination of uncertainty. This provides a bear call spread opportunity to sell elevated IV and benefit from post-event mean reversion.

Upcoming Dividends or Ex-Dividend Dates

Stocks tend to trade range-bound and exhibit muted volatility leading up to dividend payout dates as investors avoid taking positions. Instituting bear call spreads during ex-date periods offers an edge due to expectations for limited price movement.

Overbought Technical Conditions

The expected upside seems constrained when an underlying asset exhibits technically overbought conditions, such as an upward trend that peaks above the upper Bollinger Band or hits resistance. Reversion back toward the average presents propitious timing for bearish call spreads.

When to Exit a Bear Call Spread?

Determining the ideal time to exit a bear call spread requires balancing maximizing potential profit while efficiently utilizing capital and risk limits. Here are the six best times and reasons to consider closing out a bear call spread trade.

At 50-60% of Maximum Profit

The maximum gain on a bear call spread is capped at the initial net credit received. However, time decay is not linear. It occurs faster initially and then decelerates later. By closing at 50-60% of the maximum profit, solid returns are captured quickly, allowing funds to be compounded into a new position. The last portion of profit near expiration often requires tying up capital for lower ROI.

A Test of the Short Call

It is wise to close out the whole spread if the price of the underlying asset increases swiftly and appears likely to challenge the short call strike at expiration. Buying back the short call limits loss exposure if it continues above the strike. Removing the trade before breakeven is reached avoids incurring the maximum loss.

To Capture Rising Implied Volatility

During the bear call spread trade, if IV jumps dramatically higher, the short call’s value sometimes rises quickly. Exiting the spread locks in profits and allows selling new short calls at the inflated premium levels due to rising IV.

In the Event of a Better Opportunity

It’s acceptable to close a winning bear call spread before reaching its full profit in order to free up capital to place a new trade with a better risk-reward payoff. Opportunity cost makes it worthwhile to close decent gainers in favor of higher potential new trades.

At a Predetermined Stop Loss

A stop loss set at a fixed percentage below the maximum profit should trigger an exit. This follows prudent risk management rules by capping the downside in case the forecast doesn’t play out as expected. It’s better to take a small loss early rather than the maximum loss later.

As Expiration Nears

Time decay slows dramatically in the last two weeks before expiration while commission costs remain fixed. Exiting slightly before expiration avoids excessive time erosion and realization of the last bits of profit that aren’t worth the commissions paid.

How to manage risk and prolong a Bear Call Spread?

To effectively manage risk and extend the duration of a bear call spread, follow these eight key steps.

Leg In Gradually

Sell the short call first to capture optimal premium income. Delay purchasing the long call until its premium decays to lower the cost basis. Legging in achieves a better net credit and lowers breakeven.

Size Appropriately

Risk only a small percent, about 2-5%, of total capital on any single bear call spread. Proper position sizing ensures intact capital remains to trade another day.

Set a Stop Loss

Define and stick to a stop loss level, such as closing the trade if it reaches 50% of the maximum profit. This caps the downside if the forecast doesn’t materialize.

Monitor Time Decay

Keep an eye on time value erosion. The passage of time should steadily reduce the short call premium. Alternatively, close the position or reevaluate the thesis.

Watch Implied Volatility

Time decay on the brief call is accelerated if IV decreases dramatically. However, the value of a short call sometimes increases more quickly than a lengthy call if the IV surges. Be ready to adjust or close spreads if IV changes drastically.

Buy Back Short on Assignment

Buy the short call back right away to eliminate the danger of early exercise if it is issued before expiry. Re-open a new short-call position to stay in the trade.

Roll Prior to Expiration

Close the spread a few weeks prior to expiration if the maximum profit has not yet been reached, and the thesis remains intact. Then roll to a new bear call spread at further dated expirations to continue profit potential.

Book Profits at Targets

Have an upside profit target, such as 50% of the maximum gain, where partial or full profits will be captured. Disciplined profit-taking helps achieve consistent success.

Through proper position sizing, active management, rolling, and taking profits at predefined parameters, bear call spreads are extended while applying prudent risk and money management principles. This sustains their profit potential for a longer period.

How are Bear Call Spreads hedged against losses?

Bear call spreads have defined maximum loss, but various adjustments further hedge against losses, increase credits received, and lower total risk. Here are five effective hedging methods listed below.

Widen the Strikes

Moving the long call further out-of-the-money while keeping the short call the same reduces maximum loss. The greater distance between the strike prices lowers the loss amount if both options are in-the-money at expiration. This directly reduces maximum risk exposure.

Leg In Gradually

Selling the short call first, then waiting for the long call premium to decay before purchasing reduces the cost basis. Taking advantage of time erosion on the long call before entry leads to a larger net credit. More income credit cushions against losses.

Sell Additional Short Calls

Selling extra short calls against the long call at intermediate strike prices brings in more premium income. For example, shorting both the 50 and 55 calls while buying the 60 calls increases the credit received. More income provides a larger loss buffer.

Turn Into Iron Condor

Adding a long put vertical spread leg transforms the bear call spread into an iron condor with a wider total spread width. This further lowers overall risk exposure while generating additional net credit via the put credit spread.

Collar With Covered Calls

Those with long stock positions sometimes hedge the downside with bear call spreads. Selling covered calls raises extra income. Combining the call credit spread and covered call credit into a collar tightens breakeven and hedges a long stock position.

Hedging through adjustments that increase credits and decrease worst-case loss provides an additional probabilistic edge.

How does implied volatility affect Bear Credit Spread profitability?

Implied volatility is a key factor that has a significant influence on the profitability of bear credit spreads. The usual impact of IV on bear call spread trading is as follows.

Higher IV at Entry – Positive for Profit

Higher implied volatility is advantageous and raises the possibility of profiting when taking new bear call spread bets. Higher IV results in greater extrinsic value priced into the call options. This enables selling the short calls at inflated premium levels and receiving larger credits. More credit received provides greater downside protection and raises the probability of achieving maximum profit.

Falling IV After Entry – Positive for Profit

This is also a good thing if IV drops after starting the bear call spread. As IV reverts lower over the life of the trade, the short call loses extrinsic time value faster. Its premium decays at an accelerated pace while the long call loses value more slowly. This IV crush after entry enhances the spread P&L and enables locking in profits faster.

Rising IV After Entry – Can Hurt Profit

However, if IV starts trending higher after establishing the bear call spread, it will negatively impact P&L. The short call sold will increase in value faster than the further out-of-the-money long call. This IV expansion erodes the spread credit and could lead to a loss if forced to close the position.

Vega Risk Management

Since implied volatility creates vega risk, it should be monitored closely in bear call spreads. It is sometimes wise to abandon the trade and lock in winnings if IV surges dramatically higher. The long calls are sometimes then sold to capture value from rising IV rather than suffer losses in the spread from IV growth.

IV Differentials

Not just the absolute level but also the difference between near-term and longer-term IV affects bear call spreads. A higher IV skew, with front month IV much higher than back month IV, is beneficial for bear call spreads that benefit from IV decreasing into expiration.

How does time decay impact Bear Call Spread value and performance?

A bear call spread is an options trading strategy used when the trader expects the price of the underlying asset to decline. It involves buying a call option with a higher strike price and selling a call option with a lower strike price, both with the same expiration date. The trader hopes to profit from the difference in premiums between the long call they purchased and the short call they sold.

Time decay, also known as theta, impacts the value and performance of a bear call spread in four key ways, as described below.

As expiration approaches, the time value component of an option’s premium deteriorates. This benefits the bear call spread trader, as the short call they sold decays in value faster than the long call they purchased. The declining value of the short call allows the bear call spread trader to buy it back at a lower price to close the position and realize their profit. Time decay accelerates in the last month before expiration, so the trader profits more from theta as expiration nears. The maximal profit is attained if both options expire out of the money.

However, time decay sometimes also works against a bear call spread if the forecasted price decline does not occur by expiration. The long call gains value if the price of the underlying asset increases, whereas the short call loses value quickly because of time decay. This dynamic widens the spread and increases the potential loss, especially close to expiration. The maximal loss occurs if the underlying price closes above the higher strike price of the long call at expiration. Time decay diminishes the value of both legs, limiting the ability to realize a profit on the upside.

Due to time decay, bear call spreads typically need a moderately strong price move downward within weeks or months to see the best returns. Theta reduces the long call leg’s value if it is held for too long, causing its premium to converge with the short call premium and wiping out the majority of profits. Traders often close out bear call spreads at 50% or more of maximum profit to capture returns before time decay impacts further upside. However, this strategy caps the profit potential if the forecasted decline fully materializes.

To mitigate the risks of time decay, traders utilize tactics like choosing options expiring in 3-6 months to allow more time for the bearish forecast to develop. They also select options with high liquidity and tighter bid-ask spreads to close positions easily if needed. Rolling the options forward in expiration is another way to combat time erosion if the bear call spread is not profitable enough near the initial expiration date. This extends the trade at a net credit or small debit.

How might market conditions influence a Bear Call Spread?

A bear call spread is an options strategy used when the trader expects the underlying asset price to decline. Market conditions play a key role in the performance and management of this spread. Here are six ways market conditions impact bear call spreads.

In a low-volatility environment, options premiums tend to be lower across the board. This reduces the income generated from selling short calls against long calls when opening a bear call spread. Low implied volatility makes it more difficult to profit on the spread between the call premiums. Traders wait for a volatility spike before putting on a bear call spread to get better pricing. However, low volatility also means smaller price swings, which sometimes work in favor of the bearish thesis.

In high volatility conditions, options premiums become inflated due to uncertainty and rapid price swings. Bear call spreads are advantageous in some circumstances despite the fact that volatility is often considered a positive indication. Put premiums rise more quickly than call premiums when volatility spikes during a slump in the market, widening the gap between put and call prices. Traders capitalize on high volatility to sell expensive calls and buy relatively cheaper puts instead for a bearish position.

During a sustained uptrend, markets push higher over weeks and months. This environment makes it difficult for bear call spreads to be profitable. The persistent bullish momentum will likely drive the underlying price above the higher strike price of the spread, causing the maximum loss at expiration. Traders opt to avoid bear call spreads in a strong bull market and look for alternative bearish options strategies better suited for the conditions.

Conversely, bear call spreads are very effective when markets are stuck in downtrends or trading sideways in a bearish pattern. The underlying price is more likely to drop or oscillate below the lower strike price of the spread, allowing the short calls to expire worthless for maximum profit. Selling volatility also generates greater premiums as uncertainty rises in declining markets.

For markets experiencing high inflation or rising interest rates, bear call spreads capitalize on the downward pressure these monetary environments exert on stocks and other asset classes. The probability of a price decline improves for bearish trades, enhancing the chances the spread will be profitable. Still, traders must be wary of potential volatility spikes that could impact the spread.

During significant binary events that substantially impact markets, like elections, interest rate decisions, or economic reports, traders will price in greater uncertainty ahead of the event. This lifted volatility raises options premiums but also expands the range of potential market reactions. Traders utilize wider bear call spreads to accommodate unknown outcomes. Adjusting strikes closer to the current price when volatility jumps also helps manage risk.

What is an example of Bear Call Spread?

A bear call spread is an options trading strategy used when the trader expects the underlying asset price to decline. It involves buying a call option with a higher strike price and selling a call option at a lower strike price, both with the same expiration date. The trader hopes to profit from the difference in premiums between the long and short calls.

Let’s walk through an example of how a bear call spread works.

Suppose a trader is bearish on stock XYZ, currently trading at Rs. 50 per share. The trader initiates a bear call spread by buying 1 call option contract with a strike price of Rs. 55 expiring in 2 months for a premium of Rs. 2.00. At the same time, they sell 1 call option contract on XYZ at a Rs. 45 strike price for a premium of Rs. 1.00, expiring on the same date.

The net cost to enter the spread is the price of the long call less the income from the short call, which is Rs. 2.00 – Rs. 1.00 = Rs. 1.00. This Rs. 1.00 net debit is also the maximum possible loss if XYZ closes above the Rs. 55 strike at expiration.

The maximum potential profit is the difference between strike prices and the net debit. Here the spread between strikes is Rs. 55 – Rs. 45 = Rs. 10. Subtracting the Rs. 1.00 net debit leaves Rs. 9.00 as the maximum gain if XYZ finishes below Rs. 45 at expiration.

As time passes, both options lose value due to time decay. But the short Rs. 45 call decays faster, allowing the trader to potentially buy it back at a lower price to secure some gains if XYZ drops below Rs. 50 before expiration.

At expiration, there are three potential scenarios, as mentioned below.

1) Both of the options expire worthless if XYZ is less than Rs. 45. The trader keeps the Rs. 1.00 net premium as profit.

2) The short Rs. 45 call is executed, and the trader is given 100 shares of XYZ every contract at Rs. 45 to cover if XYZ is between Rs. 45 and Rs. 55. The long Rs. 55 call expires worthless. The trader’s cost basis is Rs. 45 from being assigned, plus the Rs. 1.00 debit. This reduces the loss.

3) The greatest loss occurs if XYZ is greater than Rs. 55 at expiry. Both calls are exercised, and the trader buys shares at Rs. 55 and sells at Rs. 45 for an Rs. 10 loss plus the Rs. 1.00 debit, totaling the Rs. 11 maximum loss.

This example demonstrates how a bear call spread offers defined and limited risk. The trader profits from time decay and the expected decline in the price of XYZ. Their loss is capped at the cost of entering the spread if XYZ rises significantly. Bear call spreads are a versatile options trading strategy to capitalize on moderately bearish market forecasts.

What are the advantages of Bear Call Spread?

A bear call spread is an options trading strategy involving the simultaneous purchase of a call option with a higher strike price and the sale of a call option with a lower strike price on the same underlying asset and expiration date. The advantages of employing a bear call spread include the following seven.

1.Defined and Limited Risk

The maximum loss on a bear call spread is limited to the net debit paid to establish the position. The spread limits losses if the underlying stock price rises significantly above the higher strike price. Defined risk allows for appropriate position sizing and capital allocation.

2. Higher Probability of Profit

By selling a call option to offset the cost of purchasing a call, the breakeven point is lowered. The stock price only needs to fall modestly or remain neutral for the bear call spread to yield a profit. This improves the probability of earning a return.

3. Profit from Time Decay

As options near expiration, time decay accelerates. This erodes the value of the short call faster than the long call. Both calls expire worthless, and the trader keeps the whole credit paid if the stock price remains below the lower strike at expiry.

4. Take Advantage of High Volatility

Periods of high implied volatility boost option premiums. Traders capitalize by selling overvalued calls against undervalued puts in a spread. High volatility also signals uncertainty and potential price swings.

5. Hedge Against Substantial Declines

While primarily bearish, a bear call spread limits losses in the event of a sharp downturn. The purchased lower strike call protects capital against a major decrease in the stock beyond the spread’s risk threshold.

6. Customizable Risk-Reward Profile

Strike price selection provides flexibility to achieve a desired risk-reward profile. Wider spreads further limit risk at the expense of capping gains. Narrower spreads increase profit potential but cost more to establish.

7. Access to Leverage

The ability to pay a small net debit to control a larger number of shares improves leverage. Gains are amplified relative to the invested capital if the trader’s bearish price prediction proves accurate before expiration.

Bear call spreads offer defined, low-risk bearish exposure with room for leveraged gains. Traders utilize this strategy to profit from moderately declining or stagnant prices over the options contract period. Careful selection of strike prices makes this a versatile tool to match specific risk tolerances.

What are the disadvantages of Bear Call Spread?

A bear call spread involves buying a call option at a higher strike price and selling a call at a lower strike to generate income. While offering defined risk, bear call spreads have seven disadvantages to consider.

1.Capped Profit Potential

The maximum gain is limited to the difference between the call strikes minus the debit paid. Even if the stock falls sharply, the bear call spread trader only earns the fixed maximum profit. The sold call limits further upside beyond the spread width.

2. Requires Strong Directionally Bearish Forecast

To achieve the maximum profit, the stock needs to fall below the lower strike price by expiration. The bearish forecast must materialize quickly enough before time decay erodes premiums. Losses develop if the price stays the same or goes up.

3. Time Decay Can Hurt If Stock Rises

While time decay generally helps by eroding the short-call premium faster, it sometimes works against the trader. Losses on the long call side are accelerated by time decay if the stock price increases sufficiently. Upside gains are limited, while downside risk increases with time.

3. Bid-Ask Spread Transaction Costs

Bear call spreads involve two option legs, so traders must account for the bid-ask spread on each leg. The transaction costs of establishing the position and closing it might diminish net gains. Options with wide bid-ask spreads should be avoided.

4. Assignment Risk on Short Call

The short call leg gets allocated if the stock price closes above the lower strike at expiry. The trader has to buy the stock at a higher market price to cover the call assignment.

5. Difficult to Adjust or Manage

Once established, bear call spreads have defined risk parameters that are difficult to adjust. The whole spread often has to be closed out at the best price available if the forecast changes.

6. Opportunity Cost of Capped Gains

While losses are limited, so are gains. Traders forgo the potential for unlimited upside if the stock falls sharply below the long call strike. The sold call deprives the trader of larger gains.

Bear call spreads are best suited for moderately bearish expectations, not drastically negative forecasts. Defined risk comes with the trade-off of missing out on large directional gains. Weighing these disadvantages helps determine when to use a bear call versus other bearish option strategies.

Is Bear Call Spread Profitable?

Yes, bear call spreads have the potential to be profitable trading strategies under the right market conditions. The key factors that determine the profitability of a bear call spread are the following.

- Moderate downside movement in the underlying asset price.

- There is enough time for the bearish price forecast to materialize.

- Volatility remains stable or declines slowly.

- Ability to manage early if the trade goes against you.

With a bear call spread, your maximum profit is limited to the net credit received from the difference between the two call premiums. You need the asset price to fall below the lower strike price by expiration to realize the full profit. You will make less money if the price simply marginally declines or remains stable. Significant downward moves earn you the same capped gain.

You have to balance the width between strikes to allow room for some profit while limiting risk. Wider spreads cost less but have higher risk. Narrower spreads require more capital outlay but sometimes do earn larger gains. Proper strike selection and management of the trade are key.

Is Bear Call Spread worth it?

Overall, bear call spreads are worth implementing for certain traders in specific situations. However, they are not universally the best choice for all bearish options strategies. Here are three key considerations on whether bear call spreads are worth trading.

Bear call spreads offer defined, limited risk, which many traders find attractive. You know your maximum loss when you place the trade, allowing better capital management. For moderately bearish market outlooks, bear call spreads provide an inexpensive way to profit.

However, for very bearish forecasts, the limited profit potential sometimes does not justify bear call spreads. You are better off just buying puts to capture large downside swings. Bear call spreads strong directional movement to reach maximum profit within the expiration timeframe.

Bear call spreads are worth implementing when you expect a modest downside over the near term. In low and stable volatility environments, they offer an affordable bearish options strategy. Active management and rolling the options extend their profit potential.

Is Bear Call Spread Better than Bear Call Ladder?

There is no definitive answer on whether a bear call spread or a bear call ladder is the better bearish options strategy. Each has advantages and disadvantages depending on the market conditions, risk tolerance, and forecast outlook.

Bear call spreads offer fixed, defined risk and are easier to manage with just two call option legs. However, they have capped profit potential. Bear call ladders involve selling multiple sequential short calls at incrementally higher strikes for more income. This allows greater upside but requires more precise timing and active management.

Bear call ladders provide more flexibility to roll up the calls as the underlying price drops to lower the cost basis. But if prices rise, rolling sometimes gets more expensive. Bear call spreads avoid rolling costs but have fixed strikes once opened.

Bear call spreads are better for moderate bearish outlooks with lower volatility forecasts. Their simpler structure makes them more accessible for newer options traders. Bear call ladders allow skilled traders to maximize profits from large downward price swings with precise execution.

What is the difference between Bear Call Spread and Bull Call Spread?

A bear call spread and a bull call spread are options trading strategies that involve the simultaneous buying and selling of call options on the same underlying asset and expiration date. The key difference lies in the strike prices chosen and the market outlook they aim to profit from.

Bull call spreads are used when the trader expects the underlying asset price to rise moderately. They buy a lower strike call option and sell a higher strike call to offset some of the purchasing cost. The maximum profit is realized if the stock price climbs over the higher strike at expiry. The risk is limited to the net debit paid.

Bear call spreads take the opposite market view, expecting the asset price to fall modestly or trade sideways. The trader buys a higher strike call and sells a lower strike call, crediting some premium income in the process. The maximum profit occurs if the stock finishes below the lower strike price at expiration. Risk is limited to the net debit.

Both strategies have defined and limited risk parameters. However, bull call spreads have uncapped profit potential on the upside beyond the higher strike. Bear call spreads have a fixed maximum profit limited to the difference between the two strike prices. Their upside is limited even if the asset price falls sharply.

Bull call spreads are profitable when the stock price rises enough to offset the net debit paid to open the trade. Their breakeven point is the higher strike plus the debit amount. Bear call spreads only need the stock to fall slightly below the lower strike to earn the maximum profit. Their breakeven is the lower strike minus the credit received.

While bull call spreads rely on upside price movement, bear call spreads perform better with downward or sideways price action. Bull call spreads to profit from rising volatility, while high volatility sometimes hurts or helps bear call spreads depending on whether put prices rise faster than calls.

Bull call spreads allow directional exposure with capped risk suitable for bullish outlooks. Bear call spreads provide affordable limited risk for moderately bearish forecasts. Bull call spreads are more forgiving of time decay if the stock rises. But time decay sometimes hurts bear call spreads if prices increase.

The key differences come down to market outlook, risk parameters, and profit potential. Bull call spreads aim to profit from upside moves with defined risk. Bear call spreads look to benefit from modest downside or sideways moves while limiting capital at risk. Traders choose the strategy aligned with their forecast and goals.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 40")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 41")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 42")

: Overview, 10 Types of Indicators, Settings for Different Markets 44")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 46")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 50")

No Comments Yet.