A diagonal spread, also called a calendar spread, involves holding an options position with different expiration dates but the same strike price. A diagonal spread is established by buying a longer-term option and selling a shorter-term option of the same type, either puts or calls. This allows traders to capitalize on the effect of time decay.

To construct a long diagonal call spread, for example, one would buy a call option with an expiration date that is one to six months further out while simultaneously selling a call with a nearer expiration date but the same strike price. As the sold call expires sooner, it will lose value faster due to time decay, benefitting the overall position.

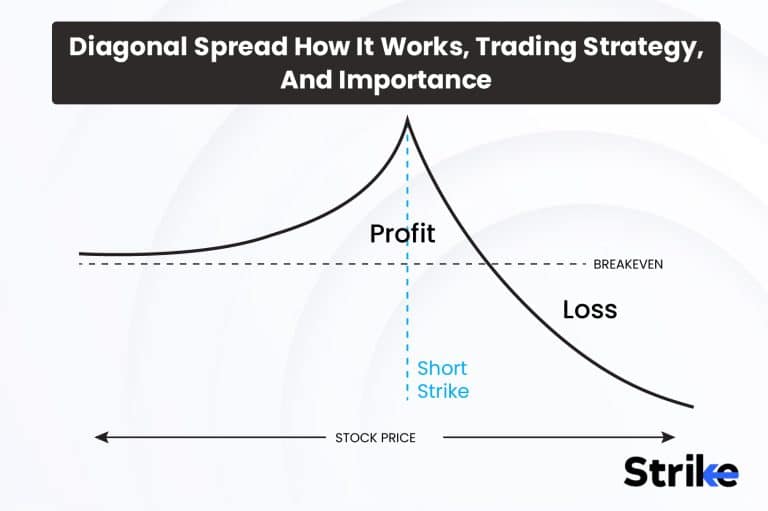

A profit is made if the underlying asset stays stable or moves moderately in favor of the spread before the close expiration of the short option. Maximum profit is achieved if the stock closes outside the strike at that time but inside the strike at the expiration of the long option. This keeps the long call in the money to offset time decay losses. The minimum risk is the net debit paid to open the position.

Diagonal spreads give leveraged exposure to an underlying underlying price movement over an extended period compared to vertical spreads. They are less capital-intensive than calendar spreads, and their profitability isn’t reliant on big price jumps. Time is an effective ally in these positions.

What is Diagonal Spread?

A diagonal spread is an options trading strategy that utilizes both a bull call spread and a bear put spread together in one spread position. The Diagonal Spread strategy involves the purchase and sale of options across expiration months rather than utilizing options that expire in the same month. As such, it “spreads” the options positions diagonally across two different expiration months.

A diagonal spread combines a bullish call spread with a bearish put spread. For the bullish portion, an investor will buy a call option with a further expiration date compared to the call option they sell. For example, they could buy a January expiration call and sell a closer September expiration call at the same or lower strike price.

For the bearish put spread portion, the investor sells a put option with the closer expiration month and buys a put option with the further expiration month, both at the same strike price. Continuing the example, they could sell a September put and buy a January put at the same strike. By combining these two spreads, the trader establishes a diagonal spread position.

The overall trade creates a position that is neutral to mildly bullish in its outlook on the underlying security. It allows for some upside participation if the stock price rises above the short call’s strike price while also providing downside protection if the stock price falls below the short put’s strike.

The maximum profit scenario occurs if the stock price at the expiration of both options is above the short call’s strike price but below the short put’s strike price. In this situation, both the call and put spreads will be worth their maximum intrinsic values to offset each other for a maximum profit equal to the premium collected when opening the position. A diagonal spread provides leverage compared to a straight stock position since less cash is needed to open the trade when properly sized.

The positions are spread across different expiration months, reducing the impact of time decay compared to same-month spreads where decay accelerates near expiration. Opening the position with further dated long options provides more time for the underlying stock to move favorably, reducing risk compared to strategies reliant on quick moves. The moderate net credit received from selling options helps reduce the cost basis, allowing for profits even if the stock moves little or declines mildly. Downside risk is defined and limited mostly to the premium spent, with the long put helping define maximum risk if the stock falls sharply.

What is the importance of Diagonal Spread?

The diagonal spread strategy holds importance for options traders as it provides a means to establish positions that balance income generation, retained upside exposure, and downside risk control, all within a customizable structure comprising long and short options of varying dates, helping to reduce overall portfolio risk.

Perhaps most notably, the diagonal spread is significant because it allows traders to participate in potential price moves of the underlying asset while simultaneously putting defined risk parameters in place. By establishing both calls and putting spreads across different expiration dates, the maximum possible loss is capped at the debit paid to open the trade. This is valuable for traders who want downside protection rather than unlimited risk profiles of other strategies.

In addition, the structure of using further dated long options gives the position more time to work before facing severe time decay pressures. Other short-term spreads are at the mercy of rapid theta decay as expiration nears, but the staggered expirations of a diagonal spread help mitigate that limitation. This makes the trade a more viable longer-term hold, again reducing risk through a longer time horizon.

Another reason diagonal spreads hold importance is that they serve either an income generation or a moderate bullish bias role within a portfolio. By selling premiums through short strikes, income is collected upfront, which lowers the net entry price and improves the probability of profitability. However, the long strikes permit participation if the market pushes past the shorts. This variable role in both generating yield as well as retaining upside exposure creates diversification against straight long stock positions.

Relatedly, the income generation component is meaningful because it works to reduce the net cost basis, potentially setting the trade up for success even if the underlying stock sees modest declines or flat price action over the life of the positions. This ability to adapt to neutral markets sets diagonal spreads apart from plays that rely strictly on directional assumptions. The premium sold acts as a buffer against sideways prices.

Additionally, because the strikes are staggered at varying distances from the current price, the position has implicit leverage embedded within it without taking on disproportionate risk. Less cash is tied up relative to an equivalent shares-based position, amplifying any profitable moves that occur. The long options allow participation beyond what a sold premium position usually entails.

The flexibility of diagonal spreads allows traders to craft their risk/reward priorities, which is also a major factor in their significance. Different combinations of long and short strikes, as well as dates, dramatically shift the profile from higher probability, lower payout designs to the inverse. This personalization means the strategy is highly customizable to specific traders’ objectives and market outlooks in a way that isolated legs cannot replicate.

What is the main goal of Diagonal Spread?

The overarching goal that a trader attempts to achieve through employing a diagonal spread is balancing the objectives of capitalizing on favorable stock price movements while also limiting their downside risk exposure. More specifically, the main priority targeted is generating a positive return through a combination of options premium collection and retained upside participation, all while having a defined maximum possible loss.

This risk-managed profit potential is accomplished thanks to the unique structure of the diagonal spread, as it combines bullish and bearish positions across different expiration months rather than utilizing strikes that converge at the same maturity date. By layering staggered calls and putting spreads together, traders take advantage of directional moves within a protected range.

More granularly, the intention behind a long call/short call calendar spread portion is participating above the short call’s strike price if the underlying stock rises from the opening price levels over the lifespan of the positions. This creates upside exposure for realized gains to offset the debt paid to initiate the trade.

Simultaneously, the short put/long put calendar spread side looks to glean income from premium selling when establishing the bearish legs. This generated premium helps contribute to an overall profitable result if the stock stays between the call spreads. Together, the dual calendars aim to not only collect this upfront premium credit but also retain the ability to benefit should the market push significantly past the short strikes.

So, the core goal combines limited risk with retained upside potential – a balanced objectives profile. A secondary benefit that further amplifies achieving the primary aim is the time decay advantages provided through the trade’s diagonal structure. Spanning options across multiple expiration dates rather than within the same month helps mitigate the impact of theta, improving the probability of profits or smaller losses as natural option time decay takes effect.

How does Diagonal Spread work?

A diagonal spread works by simultaneously buying a longer-term option and selling a nearer-term option, both with the same strike price. The goal is to profit from the difference in the premiums between the two options. The basic mechanics involve being long one call or put option with an expiration further in the future while simultaneously being short another options contract with the same trigger (call or put) but a closer expiration date and different strike price. This sets up a diagonal line when charting the strikes against time.

For example, a trader decides whether to buy the January Rs.50 call and sell the November Rs.45 call on the same underlying stock, or they could establish a bearish view by going long the January Rs.50 put while shorting the November Rs.45 put. Both setups yield a range of profit and loss outcomes defined between the strikes.

The primary aims of this structure are to generate premium from the short option sale, benefit from the impacts of declining implied volatility and intrinsic time value erosion, and participate in price moves beyond the short strike. It seeks to balance these factors against the cost of establishing the position. The maximum risk is known and limited when entering such a trade. In the above example, the maximum loss would be incurred if the stock closed below Rs.45 per share at the November expiration, as both the long January call and short November call would expire worthless.

The maximum gain is unlimited but becomes difficult beyond the short strike. Several outcomes are possible between the entry of the position and the expiration of the front-month contract. Time decay eating into the short premium works in the trader’s favor if the underlying security trades within the range between strikes. As each day passes, the intrinsic value left in that leg diminishes.

What is an example of a Diagonal Spread?

Let’s imagine an investor is evaluating XYZ Corp stock, which is currently trading at Rs.100 per share. The investor likes the company long-term but is unsure if the stock will rise or fall in the next six months. To capitalize on upside potential while limiting downside risk, a diagonal spread is an appealing strategy.

The trader sets up a diagonal spread with the positions like the ones given below.

They buy 1 January XYZ 90 call for Rs.5, establishing their long call at a lower strike price. Then they sell 2 September XYZ 90 calls for Rs.2.50 each, shorting calls at the same lower strike but with a closer expiration date.

Additionally, the trader sells 3 September XYZ 100 puts for Rs.3 each, shorting puts at a higher strike than the calls but again with the closer expiration. To complete the spread, they buy 1 January XYZ 100 put for Rs.4, establishing their long put at the same higher strike as the short puts.

The total debit to open this diagonal spread trade is Rs.5 – Rs.5 = Rs.0 since the premium received from selling the calls and puts exceeds the premium paid for the long calls and puts. This allows the trader to establish their bullish view on XYZ with limited cash exposure.

This diagonal spread established a balanced, low-cost position for the trader. The upside to Rs.90 was retained through the long January call, while the long January put protected downside to Rs.100. Together, these created an expected Rs.90-Rs.100 range for the underlying over the months. Selling the September calls and puts at strikes of Rs.90 and Rs.100, respectively, reduced the net cost basis through the premium received. In total, the structure allowed for a cautiously bullish view to be taken on the stock with limited upfront capital requirements.

Over the next six months, XYZ traded in a range of Rs.95-105 but finished at Rs.98 at the September expiration. As a result, the September short call expires worthless since XYZ closed below the Rs.90 strike. The September short put also expired worthless because the stock finished above Rs.100. During the months the position was open, time decay eroded the values of the long January call and put. Therefore, both short options expire worthless, benefiting the trader’s position as XYZ closed within the expected range.

However, the investor retains the Rs.5 total premium received from opening the trade. With no intrinsic value remaining across any legs, they close out the position for a Rs.5 profit versus the Rs.0 entry price.

In this example, the stock ended modestly higher but within the expected range. By layering calls and putting positions across different expirations, time decay was minimized while the upside was retained and downside protected within a defined window. The premium received improved the probability of profits irrespective of direction.

Of course, the trade could also have resulted in losses if XYZ spiked above Rs.90 or plunged below Rs.100. Monitoring would be needed to cut losses or remove risk if it breached these boundaries sharply. But overall, this demonstrates how a straddled diagonal spread achieves gains through premium collection and range-bound, low-volatility price action.

The takeaway is that diagonal spreads provide a flexible strategy for profiting from neutral markets or small moves, especially when the timing and structure are tuned accordingly. By leveraging different expiration months, they access a blended risk-reward profile between advanced spreads and covered positions. With experience, traders implement them effectively based on their market views and risk tolerance levels.

How to perform Diagonal Spread?

The key steps to performing a diagonal spread effectively are to analyze the underlying stock, select appropriate long and short strikes and expirations while considering risks, enter and manage the position closely, define exit rules, close legs at maturity, and refine the strategy over numerous trades through learning from each experience.

The first step in performing a diagonal spread is to analyze the underlying stock or ETF and determine if it is suitable. Make sure there is adequate liquidity in the options market with tight bid-ask spreads. Avoid highly volatile names prone to gaps or binary events. Pick an issuer exhibiting stable, range-bound price action. Next, select the appropriate expiration months for the long and short options. Generally, a 3-6 month separation works best, balancing time for profits while limiting decay.

Time decay, which is too short, increases risk; too far reduces probability. Monitor upcoming earnings dates as well. Choose strike prices that correlate to areas of expected support/resistance or technical levels where the stock pauses. OTM strikes enhance leverage but lower the chances of profiting. ITM strikes boost probabilities at the cost of reduced profits. Find the right balance.

Calculate the total initial capital needed based on the option prices. Diagonals are best done with spreads to limit outlay. Decide your maximum risk tolerance for the trade. Only 1-2% of buying power is advisable to start. Place the order to open the diagonal by simultaneously entering the long call, short call, short put, and long put. Look to collect a net credit from selling premium upfront if possible to lower your cost basis. Once filled, monitor the position closely during its lifespan.

Dynamic environments require adjustments sooner rather than later. Track changes in implied volatility. Consider closing early for profits before decay consumes them. Define exit rules beforehand based on profit targets, loss cutoffs, or breaches of key levels. Controlling losses is just as vital as letting winners run. Be prepared to act swiftly when exit triggers are tripped.

As expirations approach, the short strikes expire first. Close the long legs if the intrinsic value remains to lock in profits. Let them expire worthless for the full net credit retained as the outcome if not.

After expiration, assess the trade results versus your goals and expectations. Note what went well and any areas needing improvement for the next time. Studying outcomes helps refine strategy performance over numerous instances.

How can a diagonal spread strategy be effectively used to manage risk and potentially enhance returns?

The diagonal spread is an options strategy that offers an advantageous way to balance risk and returns. At its core, it establishes both bullish and bearish positions across varying expiration months rather than solely relying on directional assumptions. This structure inherently manages risk while retaining upside exposure. To enhance returns and control risk effectively with diagonals, traders should establish spreads wide enough to limit trades to 1-2% of buying power. The farther-dated wings give room for profit without undue hazard. Larger positions force premature exiting versus letting profits naturally compound.

Using multiple, narrower spreads also helps. For example, entering 2-3 diagonals covering different strikes minimizes the influence of any one trade’s success or failure. Outcomes even out across the positions in tandem, lowering the volatility of results.

Selling premiums through short strikes is vital for maximizing return potential. The upfront credits shrink the cost basis and set the minimum threshold for breaking even. Modest movements favor profitability through premium retention alone before factoring in intrinsic gains. Targeting stocks demonstrating historically lower beta and reasonable IV levels improves probability. Wide swings disrupt maximum profit zones. Range-bound names tend to respect support/resistance areas useful for short strikes.

Monitoring positions and adjusting expiry timing maintains prime leverage and decay exposure. Delaying long option sales prevents leaving profits exposed needlessly. Early closing ensures capturing a fair portion of the premium sold. Preset risk parameters, including loss cutoffs, avoid doubling down on failures, and minimize behavioral risk. Discretionary adjustment ignores structure and invites overtrading versus systematic execution. Strict risk stops enforcing discipline.

Keeping position deltas and vega low via expiration and strike selection reduces directional bias necessity while muting volatility exposure. Sideways and low-volatility markets suit diagonal structures the best. Learning from past trades through documentation and review enhances strategy evolution. Noting what underlying market conditions and technical analysis worked or failed informs improved future setups based on experience. Over many trades, refined techniques emerge.

How long is the timeframe to properly execute Diagonal Spread?

There is no definitive timeframe that applies universally to all uses of the diagonal spread strategy. However, in general terms, the optimal timeframe for properly executing a diagonal spread strategy is to generally target holds of at least a few months and preferably 4-6 months on average after entry while closely monitoring positions for circumstances necessitating adjustments ahead of schedule. The staggered nature of the long and short options across different expiration cycles is what gives diagonals their utility. But this also means sufficient time is required between entry and the farther-dated long option’s maturity for the positions to properly work.

Rushing in and out of the spreads in a very short window defeats part of the purpose, as it does not allow decay to sufficiently benefit the long strikes compared to the shorts. Trying to day or swing trade diagonals also exposes the position to increased volatility and imbalance. Most experts recommend establishing the spreads with at least a 3-6 month time separation between the front month shorts and back month longs.

This grants some padding for directional price action without subjecting the long wings to severe erosion from the passage of time. Of course, markets do not always cooperate with predefined timelines. Active traders mainly opt to close positions earlier and recycle profits if objectives are met. But passive investors are best off letting trades exist over months as intended.

Regardless of the time frame used, ongoing monitoring remains essential. Unexpected spikes in implied volatility, upcoming news events, or swift directional moves require adjustments like rolling or taking profits ahead of schedule versus holding indefinitely.

In practice, an initial target holding period of 4-6 months after entry tends to afford the best probability of success. This allows multiple expiration cycles to come and go while still cutting risk exposure before time decay dominates.

How can market volatility affect Diagonal Spread?

Volatility is one of the most important market factors that impact the performance of a diagonal spread trade. Due to its nature involving both bullish and bearish option positions, a diagonal spread is affected by changes in implied volatility (IV) in different ways. Higher IV generally causes options prices to increase across the board. For positions already open, this exerts upward pressure on premium values, boosting the value of long options positions if IV spikes.

However, it also increases the liability of short options. Higher IV translates to higher premiums collected on short strikes, lowering the cost to enter positions when establishing new diagonal spreads. But it also means the thresholds to profitability are higher due to more premiums requiring retention. Sudden IV increases pose risks if they coincide with adverse moves in the underlying stock price. Sharp rallies or selloffs combined with volatility spikes cause losses to exceed the initial premium credits quickly. Tighter stops are needed. On the other hand, declining IV presents headwinds.

Though it aids the liability of short positions, it decreases the premium available for collection on new entries. Lower premiums make it more difficult to break even, diminishing the upside. In volatile, whipsawing markets, the maximum profit zones defined by the short strikes become increasingly challenging to reach before positions are forced to close. Two-sided price fluctuations disrupt probability. The optimal markets for diagonal spreads feature subdued, sideways volatility where options premiums are reasonably priced, and price behavior respects defined support/resistance levels. Sporadic volatility undermines the strategy.

For these reasons, implied volatility should be a primary factor assessed when analyzing potential underlying stocks. Lower average IV readings and limited extreme spikes enhance the odds of success over time. Calmer behavior suits the approach. Constant monitoring of IV changes lets traders address quickly rising volatility through adjustments like rolling positions or taking profits preemptively versus facing harmful synchronous moves. Early flexibility protects profits and capital.

What are the common mistakes in performing Diagonal Spread strategy?

Proper strategy and position management are key to successfully implementing a diagonal spread over multiple periods. However, there are some common pitfalls traders encounter if they do not closely follow best practices. Below are the top 10 mistakes to avoid when utilizing this options technique.

1. Not properly analyzing the underlying stock. Rushing into trades without thoroughly evaluating basics like liquidity, volatility, upcoming events, and technical levels leads to unsuitable choices. This negatively impacts probabilities.

2. Using overly tight or far strikes. Strikes that are too close together reduce upside, while those too far apart increase directional assumptions and leverage beyond defined risk levels. Balance is important.

3. Not allowing enough time for trades. Diagonals work best with 3-6 month separations between expirations to escape decay. Setting up spreads with fronts too soon squeezes time for profits and increases reliance on quick moves.

4. Taking excessive directional views. While retaining upside exposure, diagonals are not meant for betting large on specific moves. Structuring positions directionally neutral within a range optimizes the strategy.

5. Overleveraging buying power. Sizing trades larger than 1-2% of available funds ignores proper position management. Outsized positions force premature exits against natural time decay benefits.

6. Not establishing sound risk management rules. The plan should define maximum acceptable loss, profit targets, and catalysts requiring closure to mitigate behavioral “letting it ride” tendencies.

7. Relying solely on net premium collection. While credits help, the goal is to leverage appreciation through retained upside to call strikes. Premium alone is not able to overcome time decay on marginal trades.

8. Ignoring ongoing monitoring requirements. Diagonals still require ongoing evaluation of strikes, durations, volatility changes, and price action. Quick adjustments preserve profits versus hope.

9. Not learning from past trades. Documentation and review help identify successful characteristics to replicate and failed elements preventing recurrence. Eliminates repetitive mistakes over time.

10. Overreliance on technical patterns. While useful for initial levels, diagonals depend heavily on implied volatility, liquidity, and time decay components outside simple price charts alone. Balance indicators with theoretical mechanics.

Avoiding these pitfalls through prudent strategy construction, sound risk handling, and experience-driven evolution helps traders better realize the risk-defined returns diagonal spreads potentially offer.

What are the potential challenges that may be encountered in performing DIagonal Spread strategy?

Ten key risks to be aware of when employing a diagonal spread strategy, each of which requires close attention and the ability to adjust positions promptly, are given below which include volatility spikes, unstable underlying, liquidity problems, earnings surprises, fast trends, expiration challenges, limited upside potential, accelerated time decay, short timelines, and behavioral weaknesses undermines the strategy if not actively managed.

1. Volatility spikes: Sudden increases in implied volatility cause losses to compound rapidly if coupled with adverse price moves beyond the short strikes. Requires quick adjustments.

2. Lack of price stability: Highly volatile underlying stocks that make large, unpredictable moves make it difficult for positions to reach maximum profit zones before forced closure.

3. Liquidity issues: Thinly traded options result in wide bid-ask spreads, increasing costs to enter and exit positions. Also impacts the ability to make timely adjustments.

4. Earnings surprises: News events like earnings cause gaps that overshoot defined risk parameters. Needs early closing before releases to avoid undue influence.

5. Fast directional moves: Quick, strong trends up or down outpace the spreads, preventing profits before breaching short strikes. Requires ATP monitoring.

6. Expiration challenges: Being wrong as monthly options expire tests the ability to roll positions smoothly and cost-effectively versus taking losses. Experience helps.

7. Limited upside: Maximum profit potential is capped based on short strikes. Large, unexpected jumps hugely surpass what spreads capture.

8. Time decay acceleration: As the front month expires, decay accelerates non-linearly, challenging the probability of retaining sufficient premium differential.

9. Short timeline: Unexpected events force closing spreads prematurely before sufficient time for natural premium and optionality benefits to accrue.

10. Behavioural weaknesses: Tendencies like over-trading, failure to cut losses, and lack of discipline in sticking to plans to undermine the strategy if not mitigated with formal processes.

Surmounting these difficulties through preparation, ongoing learning, and refinements to withstand inevitable market surprises separates good traders from the rest over extended usage of the method.

What market structure is best for Diagonal Spread strategy?

The ideal market structure for a diagonal spread strategy is one characterized by low volatility with a sideways or ranging price action. Diagonal spreads are well suited for markets that consolidate within a relatively narrow trading range rather than trending sharply in one direction. This gives both the short and long legs room to remain in the money through expiration. Ranging markets allow theta and vega to erode option premiums over weeks or months as intended. In strongly trending environments, one leg risks expiring worthless before decay takes hold if it moves past the short strike.

The risk-defined characteristics between the strikes also perform better when the underlying price does not experience sudden sharp movements outside this window. Calm, low-volatility markets tend to see less volatility in the underlying and option prices themselves. This provides a stable environment for diagonals to capture time decay without daily P&L fluctuating dramatically based on implied volatility changes. Sideways consolidation also maintains the optionality inherent to diagonals. Sharp trends quickly eliminate upside or downside potential, diminishing their flexibility. Two-sided, ranging price behavior keeps both calls and puts exposures in play for longer.

Is bullish market perfect for Diagonal Spread?

No, a bullish market environment is not necessarily the ideal type of market structure for implementing a diagonal spread strategy. While diagonals are still traded profitably in bullish conditions, their performance potential is generally better realized in more neutral, range-bound market backdrops. In a strongly bullish market environment with consistent upside momentum, it becomes increasingly difficult for the prices of the underlying stocks to remain nested within the defined range bounded by the short call and put strikes of the diagonal spreads. Prolonged rallies increase the risk of breaches.

Is a bearish market perfect for Diagonal Spread?

No, a bearish market is not perfect for a diagonal spread. However, diagonal spreads are still traded during bearish market conditions, and the environment is generally less optimal compared to range-bound or sideways markets. Potential downside breaches beyond the short put strike become more likely as downward momentum increases. Prolonged selloffs heighten the risk of the put leg working against the position.

This exposes the trade to amplified losses from intrinsic value growth on those shorts. At the same time, implied volatility typically rises substantially amid sustained bear markets. Elevated IV causes option premiums, including those collected on the short puts, to decrease in value more rapidly. This accelerates the loss of materialization when coupled with declining prices.

It also becomes harder to sell attractively priced out-of-the-money put premiums in sharply falling environments. Markets rapidly adjust quotes to reflect heightened downside risk. This undermines the income generation aspect of diagonals through limited selling opportunities.

Time decay benefits the long puts and calls less when short strikes move deep in the money from breaches. Profit zones shrink as support levels are pressured. It challenges letting trades naturally expire for maximum credit retention. Position management requires more vigilant monitoring and discipline to exit prematurely versus riding declines. Early adjustment is needed to avoid directional biases overwhelming defined risk parameters.

While diagonals still profit tactically from short-term bearish trend legs, sustained downtrends subject the strategy to heightened volatility and compressed zones amid ongoing price weakness. Two-sided, range-bound contexts better optimize utility.

Is Diagonal Spread better than other strategies?

While the diagonal spread offers appealing risk management benefits through defined risk zones, lowered costs, upside participation, compounding returns, flexibility in varied markets, and income generation potential, no single strategy is definitively better in every case, as alternatives each have strengths best suited to individual investor profiles and changing environments.

Is Diagonal Spread better than Butterfly spread strategy?

Yes, the diagonal spread is generally better suited for managing risk across different market conditions due to its greater flexibility, defined risk windows, reduced volatility sensitivity from staggered expirations, higher upside participation, ability to generate premium income, and fewer positions required. The risk management characteristics differ between the two spreads. The diagonal spread defines a clear risk window between the short call and put strikes. In contrast, the butterfly sees losses accumulate more on moves outside the wings, as its risk is less defined.

In terms of volatility handling, diagonals are less impacted by changes in volatility due to their staggered expirations reducing theta effects. Butterflies, on the other hand, profit most from stable, low implied volatility environments. The upside participation is also greater with diagonal spreads as the long call wing allows for profits beyond the short strike from extended moves. Butterflies, in their range-bound structure between the two short strikes, are unable to participate as much in extended moves. Fewer diagonals are generally needed to gain the desired exposure compared to butterflies, owing to their defined risk structure.

Butterflies require three-leg positions to be opened for each view. Diagonals also offer more flexibility in choosing individual long and short strikes and expirations. In contrast, butterfly combinations are more limited once the desired price range is set. The separate option legs of diagonals provide better liquidity than the multi-leg butterfly package, allowing for tighter spreads to be worked more easily. Additionally, premium sales on diagonals produce income to lower net costs, whereas butterflies rely solely on premium retention.

However, butterflies do offer tighter defined profit zones and higher leverage from lower buying power needs, profiting more directly from consolidation without needing time to decay. They are better for stable, low-volatility environments.

Is Diagonal Spread better than Ratio Spread strategy?

Yes, the diagonal spread is better than the ratio spread strategy. While both the diagonal spread and ratio spread strategies have their merits, the diagonal spread provides a clearer risk boundary, greater flexibility in strikes and expirations chosen, more capital-efficient usage, reduced sensitivity to time decay through staggered expirations, and potentially more predictable behavior within its defined risk zones for traders primarily seeking downside protection over various market backdrops, versus the nonlinear risk amplification suits of ratio spreads.

Is Diagonal Spread better than Vertical Spread strategy?

Yes, sometimes, the diagonal spread is better than the vertical spread strategy. The risk profiles of the two spreads differ. With a vertical spread, the risk is capped between the strikes. However, with a diagonal spread, the short leg establishes a range, leaving some directional exposure. In terms of capital efficiency, a standard diagonal spread requires a similar amount of buying power to an outright position. Meanwhile, vertical spreads provide more leverage due to their narrower range between strikes.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 40")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 41")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 42")

: Overview, 10 Types of Indicators, Settings for Different Markets 43")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 46")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 49")

No Comments Yet.