A Bear Call Ladder is a multi-leg options strategy designed to earn from strong upward market moves or rangebound conditions, while limiting losses in case of a decline. This approach uses a combination of selling and buying call options at different strikes to create a unique profit and loss graph that appeals to advanced traders during specific market scenarios.

The origin of the Bear Call Ladder traces back to the evolution of options strategies when traders sought alternatives that could generate profits from both volatility expansions and directional moves, without the unlimited risk of naked options.

Over the years, this strategy has earned credibility on major exchanges, especially during periods of event-driven volatility, such as earnings announcements or macroeconomic releases, when traders expect a breakout but wish to avoid large losses on the downside.

What is a Bear Call Ladder?

A Bear Call Ladder is an options trading strategy that involves selling one at-the-money call and buying two out-of-the-money calls at progressively higher strikes, creating a unique payoff profile. This structure caters to traders who expect either a sharp upward move in the underlying asset or minimal decline, while desiring limited risk if the market falls.

The Bear Call Ladder’s defining feature is its three-leg construction. The trader first sells one call option at the current market price (ATM), then buys one call option at a higher strike (OTM), and finally purchases another call at an even higher strike (further OTM).

This setup results in a net debit position, meaning the trader pays a small premium upfront for the potential to earn much more if the underlying asset rallies strongly.

The strategy’s name comes from its visual payoff graph, resembling a ladder, and the initial position’s bias, which is neutral to slightly bearish due to the short ATM call. However, its real strength lies in its response to a sudden bullish breakout.

The risk profile is carefully engineered: maximum loss occurs if the underlying closes between the two bought strikes, while upside profit is theoretically unlimited if the price surges well above the highest bought call.

How Does a Bear Call Ladder Work?

A Bear Call Ladder works by selling an at-the-money call, buying a higher out-of-the-money call, and purchasing a further out-of-the-money call, creating a net debit position that profits from strong rallies or stable prices.

The structure ensures that risk is capped on the downside, while profits become substantial if the underlying asset makes a significant upward move.

To build this setup, the trader begins by selling one ATM call, which generates premium income. Next, they buy one OTM call at a higher strike to limit losses if the underlying rises moderately. Finally, an additional further OTM call is bought, which removes the profit cap above the second strike and enables unlimited gains if the stock surges.

The net result is a position that costs a small sum upfront (net debit) rather than providing a credit. This upfront payment is the maximum amount at risk if the market drops or stays flat, as both long calls expire worthless and the short call premium is offset by the long calls’ cost.

The Bear Call Ladder’s payoff profile is distinctive: if the underlying closes below the sold call, all legs expire worthless, and the trader loses the net debit. If the price closes between the strikes of the bought calls, the trader suffers the maximum loss, as the short call is in-the-money but the long calls are not profitable enough to offset the loss..

This structure’s main goal is to benefit from a large upside move or a stable market, while ensuring losses do not spiral out of control if the underlying asset falls. The Bear Call Ladder’s net debit nature means the trader’s risk is defined at entry, offering peace of mind compared to strategies that involve naked short options.

Why Use a Bear Call Ladder Strategy?

A Bear Call Ladder strategy is used to potentially profit from a strong bullish breakout or a stable market while keeping downside risks limited. This makes it a powerful tool for traders who expect a sharp rally but want to avoid the high costs and risks associated with outright long calls or straddles.

When the market is expected to be neutral to bullish—especially after a period of low volatility or preceding an important announcement—the Bear Call Ladder becomes an ideal choice. Its structure offers higher rewards if the stock rallies sharply after a breakout, as the unlimited profit zone begins above the highest long call strike.

This is particularly attractive compared to traditional spreads, where gains are capped.

The Bear Call Ladder’s limited downside risk is another major advantage. The net debit paid at initiation acts as the maximum loss, regardless of how much the underlying falls. This defined risk provides significant comfort to traders compared to naked long or short strategies, where losses can spiral.

Additionally, this strategy offers a more profitable alternative to straddles or naked long calls in scenarios where a big move is expected, but the trader does not want to risk a large premium or face unlimited downside. The Bear Call Ladder’s unique payoff profile makes it especially useful during anticipated breakouts from consolidation zones or technical support levels.

Profitability in this strategy is accentuated when the stock or index experiences a strong rally after a period of low implied volatility. The increased volatility and sharp price movement cause the long calls to gain value exponentially, far outpacing the cost of the initial debit.

When to Use a Bear Call Ladder?

A Bear Call Ladder is best employed after major news or earnings releases, when limited downside risk is expected and a large move is anticipated. This timing leverages the strategy’s unique risk-reward structure, which seeks to capitalize on sharp rallies or stable markets while keeping losses contained.

The optimal environment for this strategy is when implied volatility is relatively low, but there is a strong expectation of a significant move—typically after events like earnings, policy announcements, or technical support bounces. In these scenarios, traders are looking for a cost-effective way to position for a breakout, without overpaying for expensive options.

Traders often deploy this strategy post-news or earnings when the risk of a major drop is low and the potential for a breakout rally is high. The Bear Call Ladder’s net debit nature allows traders to participate in upside moves while avoiding the high cost of straddles or outright longs.

The strategy also performs well in markets where volatility is expected to rise after entry. Entering during periods of low implied volatility means the options are cheaper, and a subsequent increase in volatility boosts the value of the long calls, enhancing profitability.

How Option Greeks Affect Bear Call Ladder?

The Bear Call Ladder’s performance is heavily influenced by the Option Greeks, with delta, theta, gamma, and vega each playing distinct roles in risk and reward. Understanding these sensitivities is crucial for effectively managing the strategy and maximizing its profit potential.

Initially, delta is negative because of the short at-the-money call, reflecting a slight bearish or neutral bias. As the underlying asset moves upward, delta quickly shifts to positive due to the two long out-of-the-money calls, resulting in increasing profits as the price rallies further.

This dynamic change in delta is one of the strategy’s defining characteristics, as it transforms from neutral or bearish to strongly bullish with price movement.

Theta, or time decay, works against the Bear Call Ladder because it is a net debit strategy. The value of the long calls erodes with time, especially if the underlying does not move significantly, causing losses to accumulate as expiry approaches. This makes the strategy less favorable in stagnant or rangebound markets, where time decay is most pronounced.

Gamma measures the rate of change of delta and is relatively high in this strategy. Sharp moves in the underlying cause delta to swing dramatically, creating rapid changes in the position’s profit and loss profile. This high gamma is beneficial during breakouts, as profits accelerate quickly on strong rallies.

Vega, which tracks sensitivity to changes in implied volatility, is positive for the Bear Call Ladder. Rising volatility after entry benefits the strategy, as the long calls gain value more rapidly than the short call loses value. This makes the Bear Call Ladder an excellent choice when volatility is expected to expand after a quiet period.

How Implied Volatility Affects Bear Call Ladder?

Low implied volatility at entry enhances the Bear Call Ladder’s potential, as the strategy benefits from a subsequent rise in volatility and the widening of breakeven points. This interplay between volatility and payoff makes timing crucial for maximizing gains and minimizing risks.

Entering the Bear Call Ladder when IV is low means the premiums for long calls are cheaper, reducing the net debit and limiting potential losses if the strategy underperforms. The rationale is that after key events—like earnings or news releases—implied volatility will likely expand, boosting the value of long calls and increasing overall profitability.

A rise in volatility after position entry elevates the prices of all legs, but the effect is more pronounced on the long calls than the short call. This asymmetry generates additional gains and widens the range of profitable outcomes, especially if the underlying asset makes a significant move.

In high IV environments, the breakeven points of the Bear Call Ladder widen, making it more challenging to achieve profitability unless an even bigger move occurs. The net debit increases, raising the maximum risk and requiring a sharper rally to generate meaningful profits.

A key risk arises if implied volatility drops sharply after placing the trade, known as an “IV crush.” This typically happens if the strategy is used just before an event, and afterward the market remains stable. The drop in IV erodes the value of the long calls faster than the short call premium, resulting in losses even if the underlying does not move much.

How to Trade Using Bear Call Ladder?

To trade using a Bear Call Ladder, the trader must anticipate a strong upward move or at least a stable market. The strategy is best suited when the expectation is for the underlying—like Nifty in this case—to move directionally higher.

It is not ideal for rangebound scenarios, as a stagnant price between certain strike levels can lead to a loss.

Even if the price expires below the lower breakeven, the position offers a minor fixed profit. However, the risk increases if the spot price closes between the two higher strike prices. This is where the strategy hits its maximum loss zone due to the structure of selling one ATM call and buying two OTM calls.

In this example, a Bear Call Ladder is built using equidistant strike prices, maintaining a 1:1:1 ratio. One ATM call at ₹24,600 is sold, and two OTM calls at ₹24,850 and ₹25,100 are bought.

The premiums involved are ₹237 received for the short call, ₹122 paid for the first long call, and ₹56 for the second long call. The net debit becomes ₹122 + ₹56 − ₹237 = −₹59.

This net debit of ₹59 per unit results in a total initial cost of ₹59 × 75 = ₹4,425. This is the maximum profit, which occurs if all options expire worthless and the spot closes at or below ₹24,600.

Maximum loss happens if the spot expires between ₹24,850 and ₹25,291. For example, if the spot is at ₹24,850 at expiry, the ₹24,600 call becomes worth ₹250 while the long calls expire worthless.

The net payoff in that case is ₹250 − ₹0 − ₹0 − ₹59 = ₹191 per unit. With a lot size of 75, the total maximum loss becomes ₹191 × 75 = ₹14,325.

Breakeven levels give insights into the price zones to watch. The lower breakeven is calculated as the short call strike plus the net debit, i.e., ₹24,600 + ₹59 = ₹24,659.

The upper breakeven uses a derived formula for equidistant Bear Call Ladders: Highest Strike + (Net Debit − Distance Between Strikes). Here, that becomes ₹25,100 + (₹59 − ₹250) = ₹25,100 − ₹191 = ₹25,291.

So the trade benefits from strong bullish moves above ₹25,291 or stability below ₹24,659, but remains vulnerable to losses if the spot lands between these two breakeven points.

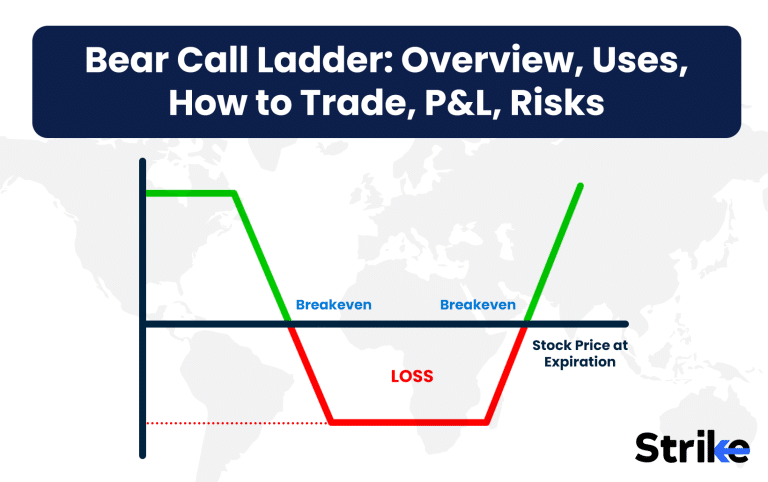

What are the Maximum Profit & Loss, Breakeven on a Bear Call Ladder?

The Bear Call Ladder offers unlimited maximum profit if the stock rallies far above the highest long call, while the maximum loss occurs if the underlying closes between the two bought call strikes at expiry.

| Scenario | Payoff |

| Below Short Call (Strike A) | Net Debit (Max Loss) |

| Between Bought Calls (Strike B & C) | Max Loss = (Strike B – Strike A) – Net Debit |

| Above Highest Bought Call (Strike C) | Unlimited Profit (Profit = Price – Strike C – Max Loss) |

| Lower Breakeven | Strike A + Net Debit |

| Upper Breakeven | Strike C – [(Strike B – Strike A) – Net Debit] |

Maximum profit is achieved when the underlying asset closes well above the highest strike price of the long calls. In this scenario, both long calls are deep in-the-money, and the short call’s loss is offset by the exponential gain from the higher calls.

Since there is no cap on the upper leg, profits increase for every rupee the stock moves above the highest strike, minus the initial net debit paid.

Maximum loss takes place if the underlying asset expires between the two bought call strikes. Here, the short call is in-the-money and incurs a loss, while the long calls have not appreciated enough to offset that loss and the initial net debit.

The formula for maximum loss is: Maximum Loss = (Strike 2 – Strike 1) – Net Debit. This loss is strictly limited and does not worsen if the underlying falls further.

The Bear Call Ladder features two breakeven points. The lower breakeven is calculated as the short call strike plus the net debit paid (Strike A + Net Debit). The upper breakeven requires a more detailed calculation: Upper Breakeven = Strike C – (Difference between strikes – Net Debit), where Strike C is the highest bought call. Profit begins to accrue only when the underlying closes above this upper threshold.

What are the Risks of Bear Call Ladder?

The Bear Call Ladder’s primary risks include losses in rangebound markets, the complexity of adjustments, strike selection precision, and time decay. These factors require careful consideration before implementation to avoid unexpected outcomes.

A key risk is loss during consolidation or in a rangebound zone. Since the strategy is a net debit, time decay steadily erodes the value of the long calls if the underlying price stays stagnant, causing losses even if the market does not move against the position.

Another challenge is the complexity involved in managing multiple legs. Adjusting or unwinding the Bear Call Ladder requires precision, as small errors in execution or timing can turn a profitable trade into a losing one. The need to manage three separate options contracts adds to the execution risk.

Precision in strike selection is critical. Choosing strikes that are too close together increases the probability of maximum loss, especially if the underlying lingers between them at expiry. Conversely, selecting strikes that are too far apart raises the net debit and necessitates a larger move for profitability.

Theta decay is an ongoing risk, particularly in sideways markets. The value of long calls declines with each passing day, and if the underlying does not move decisively, the trader loses the entire net debit by expiry.

Is Bear Call Ladder Strategy Profitable?

Yes, the Bear Call Ladder strategy is profitable when the underlying asset rallies sharply beyond the highest long call strike or when implied volatility rises significantly post-entry. This profitability stems from its asymmetric risk-reward profile and the potential for unlimited gains with limited downside.

In scenarios where the underlying stock or index breaks out following a period of low volatility, the value of the long calls can soar, quickly outpacing the initial net debit. The strategy’s design ensures that as soon as the asset moves above the upper breakeven, profits increase with every additional rupee rise.

These periods are ideal for the strategy, as both the underlying price and implied volatility work in the trader’s favor.

However, profitability is also dependent on precise execution and timing. Losses may result if the underlying remains stagnant or if volatility collapses post-entry. The key is to use the strategy only when a significant move is likely and the risk of sideways action is minimal.

Is Bear Call Ladder Bullish or Bearish?

The Bear Call Ladder is generally a bullish strategy, despite its name, as it profits from upward moves in the underlying asset. The initial bias may appear neutral or slightly bearish due to the short at-the-money call, but the payoff profile rewards strong rallies with unlimited profit.

The construction of two long out-of-the-money calls transforms the risk-reward dynamic, shifting from neutral or bearish to strongly bullish as the underlying rallies past the higher strikes. Unlike the bear call spread, which is strictly bearish or neutral, the ladder provides significant upside exposure.

Traders choose the Bear Call Ladder when they expect a bullish breakout but want a cost-effective hedge against limited downside risk. Its bullish nature becomes increasingly pronounced as the underlying moves higher, especially above the upper breakeven.

What are Alternatives to Bear Call Ladder Strategy?

Alternatives to the Bear Call Ladder include the Bull Call Spread, Straddle, Strangle, and Call Ratio Backspread, each offering different risk-reward characteristics. Choosing the right alternative depends on market outlook, volatility expectations, and risk tolerance.

The Bull Call Spread is a simpler bullish alternative, involving the purchase of a lower strike call and sale of a higher strike call. This approach caps both profit and loss, offering a straightforward way to benefit from moderate upward moves while keeping risk defined.

The Straddle and Strangle are neutral strategies that profit from significant volatility, regardless of direction. Both involve buying call and put options at the same or different strikes, allowing traders to benefit from large moves either up or down, but at a higher premium cost.

The Call Ratio Backspread is another bullish breakout strategy, similar to the Bear Call Ladder but with a different structure. It involves selling fewer calls at a lower strike and buying more calls at a higher strike, resulting in limited loss and unlimited profit potential if the underlying rallies sharply.

Tthe best alternative depends on your market view and risk profile, with each strategy offering unique advantages for different trading scenarios.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 24")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 25")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 26")

: Overview, 10 Types of Indicators, Settings for Different Markets 28")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 30")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 33")

No Comments Yet.