The Call Ratio Backspread is an options strategy designed to capture unlimited profits from sharp upward moves while keeping risk capped if the market only rises modestly. The Call Ratio Backspread structure involves selling a smaller number of lower-strike calls and buying a larger number of higher-strike calls, typically at a 1:2 ratio.

The primary appeal of the strategy is its ability to create large gains if the underlying asset rallies powerfully, while the downside is limited to a certain maximum loss, usually occurring if the price ends just above the short strike at expiration.

What is a Call Ratio Backspread?

A Call Ratio Backspread is an options trading strategy that profits from strong upward moves in the underlying asset by combining a short call at a lower strike with two or more long calls at a higher strike.

The most common configuration is a 1:2 ratio—selling one at-the-money (ATM) or in-the-money (ITM) call and buying two out-of-the-money (OTM) calls.

The primary objective of the Call Ratio Backspread is to benefit from explosive rallies, typically with little or no upfront cost. The net position creates a P&L curve that is flat or negative if the underlying remains flat, with a maximum loss when the price lands between the strikes, and unlimited profit if the price surges well above the long calls.

This makes it an attractive choice for traders expecting a breakout or volatility spike, but who want to avoid the large losses possible with naked long calls.

Unlike simple vertical spreads, the Call Ratio Backspread introduces positive gamma and vega exposure, meaning profits accelerate if the market moves quickly or implied volatility rises after entry.

How Does a Call Ratio Backspread Work?

A Call Ratio Backspread works by selling a lower-strike call and buying more higher-strike calls, creating a position that profits from a big rally in the underlying asset, with limited risk if the move is only modest.

The most common version is a 1:2 ratio: you sell one at-the-money (ATM) call and buy two out-of-the-money (OTM) calls, all on the same expiry, using NIFTY or any Indian stock as an example.

Let’s say NIFTY is at ₹22,000. You anticipate a sharp move upward, perhaps after an important market event. To set up a Call Ratio Backspread, you might sell one NIFTY 22,000 call at ₹220 and buy two NIFTY 22,300 calls at ₹70 each. Your net premium is ₹220 received minus ₹140 paid (₹70 x 2), so you start with a net credit of ₹80.

If NIFTY stays at or below ₹22,000 at expiry, all options expire worthless. You keep the full ₹80 credit as profit. This is your best-case outcome if the market does not move.

Now, suppose NIFTY rises but closes at ₹22,300. The 22,000 call you sold is worth ₹300 (intrinsic value), while the two 22,300 calls you bought are at-the-money and expire worthless.

Your loss is the ₹300 payout on the short call minus your ₹80 credit, so maximum loss is ₹220 (₹300 − ₹80). This loss occurs if NIFTY finishes exactly at the long call strike.

However, if NIFTY makes a much bigger move and closes at ₹23,000, all options are in the money. The 22,000 call is worth ₹1,000, and each 22,300 call is worth ₹700 (₹23,000 − ₹22,300).

You receive ₹1,400 from your two long calls, pay out ₹1,000 on your short call, and add the original ₹80 credit. Your total profit is ₹480 (₹1,400 − ₹1,000 + ₹80). The higher NIFTY closes above ₹22,300, the greater your profit, with no upper limit.

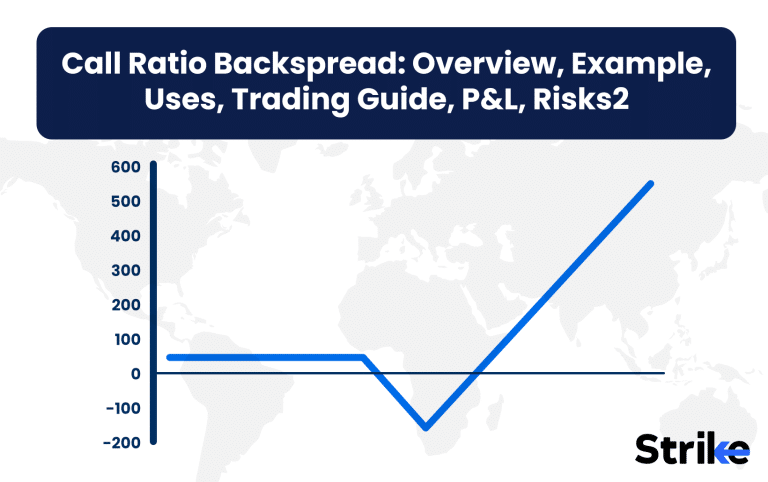

The payoff diagram for a Call Ratio Backspread in rupees is shaped like a shallow valley between ₹22,000 and ₹22,300, then rising steeply upward for higher prices.

- Below ₹22,000: maximum profit is the net credit (₹80).

- At ₹22,300: maximum loss (₹220).

- Above ₹22,300: unlimited profit (grows by ₹2 for every ₹1 NIFTY rises above ₹22,300, since you hold two long calls for each short call).

This structure is attractive because loss is always capped and known in advance, while profit is unlimited if the market spikes upward. The trade is also positive vega—if implied volatility rises after entry, the position’s value increases.

Why Use a Call Ratio Backspread Strategy?

The main reason to use a Call Ratio Backspread strategy is to profit from explosive upside moves while capping risk to a small range above the short strike. This approach appeals to traders expecting a significant rally or volatility surge, especially when entering for a net credit or low net debit.

The strategy allows participation in major bullish moves without the large upfront cost or unlimited risk of buying naked calls. The position benefits not only from sharp price rallies, but also from increases in implied volatility after entry, making it especially attractive before earnings or big news events.

Since risk is limited to the area between the short and long strikes, traders know their maximum loss before entering the trade.

Another key advantage is flexibility in constructing the spread: by adjusting strike selection or the ratio, it’s possible to tailor the risk/reward profile to match market expectations and personal risk tolerance.

The Call Ratio Backspread’s positive gamma profile means profits accelerate as the underlying rises, unlike many other bullish spreads that plateau above a certain level.

When to Use a Call Ratio Backspread?

A Call Ratio Backspread is best deployed when a trader expects a large upside move, usually ahead of earnings, major news, or after periods of low volatility and consolidation. Market conditions should indicate a strong bullish bias and the potential for increased volatility, like in the image below.

The strategy is especially useful when implied volatility is relatively low but likely to rise, as this increases the value of the long calls after entry. It fits traders who have limited risk capital but want exposure to big moves, allowing them to participate in breakouts without risking large losses.

Call Ratio Backspreads are also favored when technical analysis or market sentiment suggests a strong, one-sided move is imminent.

During earnings season, before Federal Reserve announcements, or preceding product launches, traders use this setup to capture potential upside without being exposed to large losses on a failed move.

The structure is less effective in range-bound or quiet markets, where time decay will erode the position’s value before the anticipated move occurs.

How Option Greeks Affects Call Ratio Backspread?

The option Greeks affect the Call Ratio Backspread by making it highly sensitive to large price moves (positive gamma), increasingly bullish as the stock rises (positive delta), vulnerable to time decay (negative theta), and profitable when implied volatility rises (positive vega). See the table below.

| Greek | At Entry | After Big Move Up | Near Expiry (Flat) |

| Delta | Slightly + | Strongly + | Neutral/Small + |

| Gamma | High | Highest | Drops to 0 |

| Theta | Negative | Less negative | Strongly negative |

| Vega | Positive | Negative (if deep ITM) | Negative |

At entry, the delta is slightly positive, becoming strongly positive if the underlying rallies.

Gamma is a key feature: as the underlying price shoots higher, profits grow at an accelerating rate, rewarding traders for correct timing and direction.

Theta works against the position, as time decay erodes the value of the long calls faster than it benefits the short call, especially if the underlying fails to move.

Vega exposure is positive, so increases in implied volatility after entry add value to the spread, making it especially suited to pre-event trades.

How Implied Volatility Affects Call Ratio Backspread?

Implied volatility has a significant impact on the Call Ratio Backspread, with higher volatility increasing the value of the long calls and making the strategy more profitable. The best time to enter is when IV is low and expected to expand, as this makes options cheaper to purchase and more valuable after a volatility spike.

An IV increase after entering the trade is highly beneficial, since the value of the long calls rises faster than the short call, adding to the position’s profit potential.

However, after a major event like earnings, implied volatility often collapses (“vol crush”), which can rapidly reduce the value of the spread if the underlying hasn’t moved enough. This makes proper timing and volatility forecasting essential for success.

The Call Ratio Backspread works best when paired with catalysts that are likely to create both movement and volatility expansion. By entering before such events and exiting shortly after, traders take full advantage of favorable IV shifts and price rallies.

How to Trade using Call Ratio Backspread?

Trading a Call Ratio Backspread involves selecting the underlying asset, choosing a near-the-money short call strike, picking an appropriate out-of-the-money long call strike, and executing the trade in a 1:2 ratio using a multi-leg order.

This structure is generally deployed when there is a strong bullish bias or an expectation of a sharp volatility breakout.

The logic behind the setup is that the price will either continue in its original bullish direction or reverse sharply to the downside. If it remains range-bound, the strategy starts incurring losses.

This strategy profits only when there’s a significant move in either direction. Therefore, it is best suited for scenarios where consolidation is least expected.

From the payoff graph, we can see that if Bharti Airtel breaks out above resistance and continues its upward movement, the profit grows exponentially. This is because the long OTM calls start gaining significant value as the price rises.

Even if the stock reverses and moves below the strike of the sold ITM call, the position still earns a minimal fixed profit. The only scenario where the position results in a loss is if the price consolidates around the current level.

Position structure: Sell 1 lot of ITM 1720 CE @ ₹50 and buy 2 lots of 1800 CE @ ₹8 each. This creates a ratio of 1 sell to 2 buys.

Net premium received is ₹50 (from the ITM call) minus ₹16 (for the two OTM calls), resulting in a ₹34 credit per lot.

Since the lot size is 475, the total upfront credit is ₹34 × 475 = ₹16,150. This amount becomes the fixed minimal profit if Bharti Airtel expires below ₹1720 and all options expire worthless.

Thus, this Call Ratio Back Spread offers limited risk, fixed minimal profit, and unlimited upside potential.

What are the Maximum Profit & Loss on a Call Ratio Backspread?

Maximum profit for a Call Ratio Backspread is unlimited if the underlying rises well past the long strike, while maximum loss is limited and occurs if the asset finishes between the short and long strikes at expiration. The breakeven point depends on the net premium and the distance between strikes.

For a net debit trade, breakeven is calculated as the upper strike plus the total premium paid. Net credit trades shift breakeven lower, making it easier to reach profitability. I

The worst scenario is when the asset settles between the strikes, where the short call is in the money but the long calls have not yet offset the loss.

Here, the loss is capped at the difference between the strikes minus the net credit or plus the net debit. In summary, the Call Ratio Backspread offers a rare combination—unlimited upside for a fixed, known risk if the price only rises modestly.

What are the Risks of Call Ratio Backspread?

The principal risks of a Call Ratio Backspread are losses if the underlying rises only modestly, time decay eroding value, assignment risk on the short call, and the need for precise timing and volatility analysis.

Theta decay works against the backspread, steadily reducing the value of the long calls as expiration approaches without a significant price move.

Assignment risk looms if the short call goes in the money near expiry, potentially forcing the trader to deliver shares or manage an unwanted position. Entering the trade at the wrong time—when implied volatility is high or the market is not primed for a move—reduces the probability of profit.

Additionally, incase the stock gaps up just above the long strike but not enough to offset losses on the short call, the position may still lose money. Liquidity concerns arise in contracts with low volume, making it difficult to enter or exit efficiently. Careful strike selection, timing, and risk management are critical to avoid these pitfalls and achieve the strategy’s potential.

Is Call Ratio Backspread Strategy Profitable?

Yes, rhe Call Ratio Backspread strategy is profitable when the underlying makes a large, quick upward move after entry. Its unlimited profit potential is realized only in trending markets with strong, swift rallies.

It delivers high returns for limited risk, making it attractive for aggressive and disciplined traders when properly timed around catalysts or volatility expansions.

Is Call Ratio Backspread Bullish or Bearish?

A Call Ratio Backspread is a bullish strategy, designed to benefit from substantial price appreciation in the underlying asset. The position’s structure profits from rising prices, with risk capped on the downside and unlimited upside if the asset surges.

Traders use it when they anticipate a breakout or strong move higher rather than a moderate or sideways trend.

What are Alternatives to Call Ratio Backspread Strategy?

Alternatives to the Call Ratio Backspread include the long call spread, long straddle, call debit spread, call ratio spread (1:1), and synthetic long stock, each with its own risk/reward and volatility profile.

The long call spread offers lower cost and capped profit, while the straddle is neutral but needs high volatility.

The call debit spread also defines risk and reward, making it less aggressive than a backspread. The call ratio spread (1:1) carries less bullish exposure, and the synthetic long stock replicates a bullish position with different risk dynamics. Here’s a comparison.

| Strategy | Max Risk | Profit Potential | Volatility Sensitivity |

| Call Ratio Backspread | Limited | Unlimited | High (positive vega) |

| Long Call Spread | Limited | Capped | Moderate |

| Long Straddle | High | Unlimited | Very high |

| Call Debit Spread | Limited | Capped | Moderate |

| Call Ratio Spread | Moderate | Moderate | Moderate |

| Synthetic Long Stock | Unlimited | Unlimited | Moderate |

Choosing the right alternative depends on market outlook, volatility expectations, and risk tolerance.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 20")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 21")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 22")

: Overview, 10 Types of Indicators, Settings for Different Markets 23")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 26")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 29")

No Comments Yet.