Call ratio spread is a trading strategy in the derivatives market that formed NSE introduced weekly options in 2019. Call ratio spread involves buying one call option at a lower strike price and simultaneously selling two call options at a higher strike price, with all options having the same expiration date.

The core appeal of the call ratio spread lies in its asymmetric risk-reward profile. Maximum profit is achieved if the underlying closes at the strike price of the short calls at expiry, as the long call gains maximum value while the short calls expire worthless.

But in case of the underlying asset rising significantly beyond the short strike, the strategy exposes the trader to unlimited risk because the losses from the additional short call(s) outweigh the gains from the long call. This necessitates active management and a solid understanding of options pricing, as factors like implied volatility, time decay, and margin requirements play a critical role in both the profitability and risk of the trade.

The strategy is best suited for experienced traders who is able to monitor positions closely and adjust or hedge when market conditions change unexpectedly.

What is a Call Ratio Spread?

Call ratio spread is an options strategy that involves buying one call option and selling multiple call options at a higher strike price, typically in a 1:2 or 1:3 ratio.

Call ratio spread is used when the trader expects the underlying asset to increase in price, but not excessively beyond the short strike price. The goal is to profit from a moderate price increase while limiting risk.

The maximum profit occurs when the underlying asset expires at the short strike price, where the long call gains value and the short calls expire worthless. The maximum loss happens if the underlying asset expires below the long strike, where the premium paid for the long call is lost. Call ratio spreads offer limited risk but potential for high reward when the price stays near the short strike.

During the mid-life of the trade, positive theta generates consistent profits through time decay, while negative vega benefits from volatility decline. Delta stays relatively neutral near the short strikes, providing steady position management.

How Does a Call Ratio Spread Work?

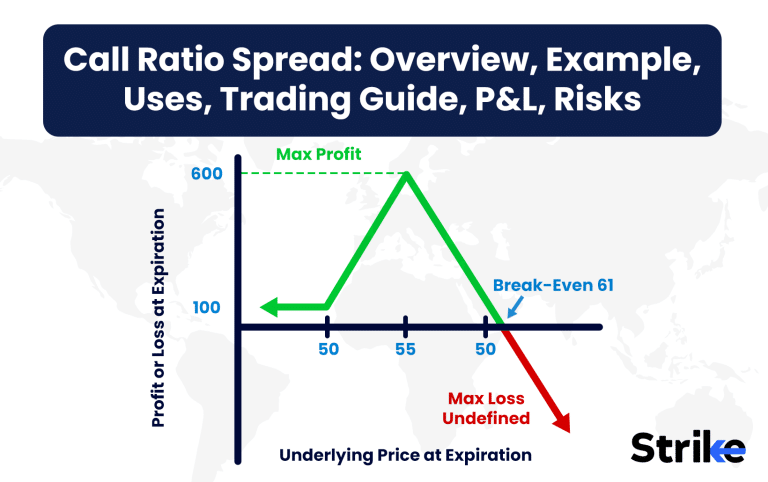

Call ratio spread works by buying one ATM call option at a lower strike price and selling multiple OTM call options at a higher strike price, usually in a 1:2 or 1:3 ratio. The strategy profits if the underlying asset rises but stays near the OTM short strike, with limited risk if the price remains below the ATM long strike. Let us look at an example to understand this better.

IRCTC has recently bounced off its long-term support level, showing signs of a potential bullish continuation. Given the stock’s recovery, there is a high likelihood it could break through the resistance level of ₹750 by the expiry date. Based on this outlook, a 1:2 call ratio spread has been deployed to secure a fixed loss and capitalize on potential profits within the upper price range.

Below is the payoff diagram for the same.

The position involves buying 1 ATM 730 CE at ₹18 and selling 2 lots of 760 CE at ₹7, creating a 1:2 ratio. The net premium paid is ₹4 per lot, resulting in a total upfront cost of ₹3,500. The maximum loss occurs if IRCTC expires below ₹730, with a fixed loss of ₹3,500 per lot.

The maximum profit is achieved if the stock expires at ₹760, with the long call gaining ₹12 per lot (₹10,500) and the short calls providing ₹12,250. The total maximum profit is ₹22,750. The breakeven point on the upside is ₹786, beyond which the position starts incurring losses due to the net short call.

What are The Types of Call Ratio Spread?

There are 4 types of call ratio spreads, each designed to profit from specific market conditions and volatility environments. These variations offer traders different approaches to leverage options for directional views, ranging from moderately bullish to strongly directional positions, while managing risk through various ratio combinations.

1. Call Ratio Front Spread

A Call Ratio Front Spread differs from an ordinary Call Ratio Spread in that it involves buying an ITM (In-the-Money) Call option, whereas in a regular Call Ratio Spread, an ATM (At-the-Money) or OTM (Out-of-the-Money) Call is purchased.

Reliance Industries has recently found strong support, and with a higher probability of a gradual upward movement, the stock is expected to approach the upper end of its price range near resistance. Given the mildly bullish outlook, this position has been established to ensure a fixed minimal loss while positioning for maximum profit if the stock moves toward the upper price band near resistance.

As there are 7 days to expiry, a strong bullish momentum is unlikely, while the price may experience a slow and sluggish momentum on the upper side. To take advantage of this, here is a 1:3 Call Ratio Front spread.

The example we’re covering involves a Near-Zero Cost Ratio Spread, not a net credit. The upfront cost is small relative to the total exposure and potential payoff. With a ₹13 debit, we can build a 70-point-wide range (1190 to 1260), qualifying this spread as a “Near-Zero Cost” structure, since the debit is under 20% of the spread width.

In this position, an ITM 1190 CE (1 lot) is bought at ₹40, and a ratio of 1:3 is created by selling three 1260 CE lots at ₹9. The net premium results in a ₹13 debit per lot, leading to a total upfront cost of ₹6,500. This amount represents the fixed minimal loss if Reliance expires below ₹1190.

Max profit occurs when Reliance expires at ₹1260. The total max profit is ₹28,500, consisting of ₹15,000 from the 1190 CE and ₹13,500 from the 3x short 1260 CE.

The breakeven point on the upside is ₹1288.50. If Reliance expires below ₹1190, the position incurs a fixed loss of ₹6,500.

the position involves more short calls than long calls, the theta (time decay) is in favor of the position. A sluggishly bullish move will benefit the position as the 3 short calls decay faster than the long ITM call.

With 1 long call and 3 short calls, the position is Vega-negative. Rising volatility will hurt the position, but falling volatility will favor it as the 3 short calls lose value.

2. Call Ratio Back Spread

A Call Ratio Back Spread involves buying more call options than selling, typically with a 2:1 or higher ratio. This strategy is used when a significant upward movement in the underlying asset is expected, offering unlimited profit potential with a limited risk, as the premium received from the short calls offsets the cost of the long calls. Look at the below example.

Bharti Airtel is currently at a key resistance level, a price point where the stock may either break out and continue its bullish momentum or reverse into a bearish trajectory. The price is unlikely to remain range-bound at this level. Given the potential for significant movement in either direction, a Call Ratio Back Spread has been implemented.

A Call Ratio Back Spread is designed for situations where the underlying asset is expected to either reverse sharply or continue its trend. This strategy becomes profitable only if the price moves significantly in one direction. If the price remains range-bound, the position will incur losses. Therefore, for this trade to succeed, the underlying asset must experience a notable price move in either direction.

From the payoff graph below, it is evident that if Bharti Airtel breaks past its resistance level and continues its bullish movement, the profit potential increases exponentially based on the price at expiry. This strong bullish breakout would result in significant profits as the price moves higher.

However, even if the breakout fails and the stock reverses downward, the position will still incur a fixed minimal profit. The only scenario in which this strategy results in a loss is if the price remains range-bound at the resistance level, failing to break out in either direction.

The position structure involves selling one 1720 CE at ₹50 and buying two 1800 CEs at ₹8, creating a 1:2 ratio back spread. The net premium results in a ₹34 credit per lot, amounting to ₹16,150 in total upfront credit, which represents the fixed minimal profit if Bharti Airtel expires below ₹1720. This strategy provides limited risk, a fixed profit if the stock stays below ₹1720, and unlimited upside potential if the stock price rises.

The upper breakeven is calculated at ₹1846, where the position starts to yield exponential profits. If the price moves above this level, the position benefits significantly. On the downside, the lower breakeven is ₹1754; below this level, the position will begin to incur fixed minimal profits, as all options expire worthless. This strategy is profitable if the stock breaks out in either direction but incurs fixed minimal profits if it stays within the range.

Why Use a Call Ratio Spread Strategy?

Call ratio spread strategy is used to capitalize on specific market conditions while managing costs and risks through balanced option positions. Traders execute this strategy to profit from moderate price movements, volatility changes, and time decay.

The strategy leverages multiple options contracts to create positions with defined risk parameters. Selling more options than buying reduces or eliminates the initial cost, sometimes generating immediate credit. Time decay works favorably through the faster erosion of short options premiums.

Position flexibility allows traders to adjust their exposure based on market outlook. The multiple strike prices create various profit zones, maximizing returns within specific price ranges. Break-even points provide clear risk management guidelines.

Greeks management becomes straightforward through balanced delta exposure near short strikes. Positive theta generates consistent time decay profits. Vega sensitivity varies based on the specific ratio structure chosen.

The strategy excels in range-bound markets with slight directional bias. Premium collection from short options offsets the cost of long options. Risk remains limited on the downside while maintaining upside potential.

Position adjustments roll forward during profitable scenarios. Exit strategies implement at predetermined profit targets, typically 50-75% of maximum potential. Stop-loss implementation protects against adverse market moves.

When to Use a Call Ratio Spread?

You should use a call ratio spread when you expect moderate bullish movement in the underlying asset but want to limit downside risk. This strategy is ideal when you believe the price will rise to a specific level but not significantly exceed it.

It’s also effective if you anticipate a range-bound or slightly upward movement, as it allows you to benefit from the time decay of short options. A call ratio spread works best when you expect the price to approach the short strike at expiry, maximizing profits from the difference between the bought and sold calls.

It is typically used when you want to create a position with limited risk and defined profit potential, while keeping costs relatively low. However, it sometimes leads to significant losses if the price moves too far beyond the short strike.

How Option Greeks Affects Call Ratio Spread?

Option greeks affect call ratio spreads through distinct interactions that influence position profitability and risk management. Delta exposure varies based on the ratio structure, creating neutral to slightly positive directional bias near the short strikes. The position delta increases as price moves above short strikes, accelerating potential gains or losses.

Gamma risk intensifies near expiration, particularly around strike prices. Multiple short options generate negative gamma exposure, requiring active position management. The strategy benefits from positive theta through faster time decay of short options. Time premium erosion accelerates in the final month before expiration.

Vega sensitivity depends on the specific ratio configuration. Short options provide negative vega exposure, benefiting from volatility decline. The long option partially offsets vega risk through positive volatility exposure. Overall position vega typically remains slightly negative.

Rho impact remains minimal due to balanced long and short options. Interest rate changes marginally affect position value. Greeks management focuses on maintaining desired exposure through position adjustments. Delta-neutral positioning achieves through strike price selection and ratio balancing.

Break-even points shift based on changes in implied volatility and time decay, both of which are key components of Option Greeks. Position monitoring emphasizes delta and gamma exposure near expiration, making it essential to understand Option Greeks when managing risk. Roll adjustments maintain optimal Greeks exposure during profitable scenarios.

How to Trade using Call Ratio Spread?

To trade using a call ratio spread, first, identify the underlying asset you want to trade and determine your outlook. You expect moderate bullish movement with limited risk, select a strike price for the long call (typically ATM or ITM) and choose a higher strike price for the short calls (typically OTM). The most common ratio is 1:2, where you buy one call and sell two calls at the higher strike.

Next, execute the trade by purchasing the long call and selling the short calls. The goal is for the price to move towards the short strike, where maximum profit occurs. Monitor the position closely, as you benefit from time decay on the short options, but the price should not exceed the short strike significantly, as this can lead to unlimited losses. Adjust the position if necessary, and close the position before expiry to lock in profits or minimize losses.

Implement risk management through position sizing and stop-loss discipline. Document trade performance for strategy refinement. Review market conditions and volatility environment before each trade.

What is the Maximum Profit & Loss on a Call Ratio Spread?

The maximum profit in a call ratio spread materializes at the short strike price at expiration.

Maximum loss varies based on the ratio structure. Front spreads limit downside risk to the initial debit or provide small credit, while back spreads cap losses at the difference between strikes minus net credit received. Unlimited loss potential exists above upper break-even points due to naked short calls.

Break-even points is calculated by adding net debit/credit to lower strike and solving for upper break-even using ratio parameters. The strategy profits between these points through time decay and moderate price movement.

Risk-reward ratios improve through optimal strike selection and ratio configuration. Front spreads target 1:2 risk-reward, while back spreads seek 1:3 or better. Position sizing aligns with maximum loss tolerance.

Profit realization accelerates near expiration through time premium erosion. Exit strategies implement at 50-75% of maximum profit potential. Stop-loss triggers activate at predetermined loss levels to protect capital.

What are the Risks of Call Ratio Spread?

The risks of call ratio spread include significant exposure above the upper break-even point due to naked short calls. Sharp upward price movements create substantial losses through unlimited risk on the uncovered portion of short options. Early assignment risk exists on short calls, particularly during dividend periods.

Market gaps beyond break-even points trigger rapid position deterioration. Volatility spikes inflate short options values, creating mark-to-market losses. Time decay works against back spreads through multiple long options.

Delta risk intensifies as price approaches and exceeds short strikes. Gamma exposure accelerates losses during adverse price movements. Liquidity constraints in far-strike options increase execution costs and adjustment difficulties.

Position management becomes challenging during high volatility periods. Roll adjustments require additional capital and create new risk parameters. Margin requirements increase with market volatility, demanding higher capital allocation.

Technical failures at support/resistance levels invalidate position thesis. Break-even points shift unfavorably with implied volatility changes. Assignment risk escalates near expiration, requiring careful position monitoring.

Risk mitigation requires strict position sizing and stop-loss implementation. Exit strategies must execute promptly during adverse scenarios. Capital requirements increase with position adjustments and rolls.

Is Call Ratio Spread Strategy Profitable?

Yes, call ratio spread strategy generates consistent profits through careful position selection and management. The strategy profits from time decay, volatility changes, and moderate price movements. Premium collection from multiple short options reduces position cost or creates immediate credit.

Break-even points provide clear profit zones. Risk management through proper position sizing ensures sustainable returns. Markets with range-bound price action and elevated implied volatility enhance profitability.

Is Call Ratio Spread Bullish or Bearish?

Call ratio spread is moderately bullish to strongly bullish, depending on the specific structure chosen. Front spreads benefit from gradual upward movement, targeting maximum profit at short strike prices. Back spreads profit from sharp bullish moves through multiple long calls. The strategy combines bullish directional bias with premium collection advantages.

Position delta increases as price approaches short strikes. Market conditions favoring upward trends enhance returns. Strike selection determines bullish exposure level. Break-even points establish profit zones aligned with bullish outlook. Position management maintains desired directional exposure through adjustments.

What are Alternatives to Call Ratio Spread Strategy?

Alternatives to a call ratio spread include vertical call spread, butterfly spread, iron condor and covered call.

| Strategy | Pros | Cons |

| Vertical Call Spread | • Limited risk and defined reward• Lower margin requirements• Simple execution and management• Clear break-even points | • Limited profit potential• Requires directional accuracy• Less premium collection• Time decay varies by position |

| Butterfly Spread | • Defined risk and reward• Maximum profit at specific price• Lower cost structure• Benefits from volatility decline | • Narrow profit range• Complex position management• Higher commission costs• Limited adjustment flexibility |

| Iron Condor | • Regular income generation• Non-directional profit potential• Benefits from time decay• Adjustable risk parameters | • Multiple leg management• Risk from both directions• Higher margin requirements• Complex adjustment process |

| Covered Call | • Consistent premium income• Downside stock ownership• Simple position management• Lower option knowledge needed | • High capital requirement• Limited upside potential• Stock assignment risk• Downside exposure |

| Poor Man’s Covered Call | • Lower capital requirement• Leveraged position• LEAPS provides time value• Regular premium collection | • Complex position sizing• Roll management needed• Delta risk exposure• Time decay on long option |

Each alternative offers unique advantages based on market outlook and risk tolerance. Strategy selection aligns with trading goals, capital availability, and market conditions.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 31")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.