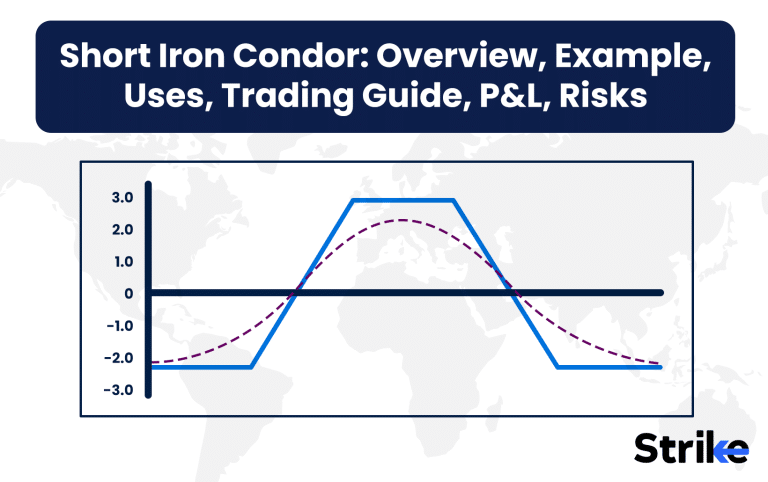

Short iron condor involves selling an out-of-the-money (OTM) call spread and an OTM put spread simultaneously with the same expiration date.

This strategy is widely deployed on index derivatives like Nifty 50 and Bank Nifty, which together account for over 90% of total options trading volume on the NSE. According to SEBI data, index options trading has grown over 150% in the last three years, making iron condors a staple strategy for market makers and retail traders seeking stable income generation.

A Short Iron Condor involves selling an out-of-the-money (OTM) call spread and an OTM put spread with the same expiration date, effectively creating a profit zone between the two short strikes.

What is a Short Iron Condor?

A short iron condor represents a limited-profit, limited-risk options strategy combining two credit spreads – one bull put spread and one bear call spread with the same expiration date. A short iron condor consists of four options legs: selling a put option at a lower strike price, buying a put option at an even lower strike price, selling a call option at a higher strike price, and buying a call option at an even higher strike price.

Market makers utilize this strategy extensively in the Indian derivatives segment, particularly on Nifty and Bank Nifty indices. The position benefits from time decay and volatility contraction, with maximum profit achieved at expiration between the short strikes. Professional traders implement this strategy with 30-45 days until expiration, targeting 45-60% of the maximum potential profit.

Position management demands active monitoring with adjustment triggers at 15-20% adverse moves. Market makers maintain strict position sizing at 2-3% of portfolio value, ensuring sustainable risk management.

How Does a Short Iron Condor work?

Short iron condor works through a specific four-legged options structure creating a range-bound profit zone. Short iron condor executes by simultaneously selling one OTM put at a lower strike price, buying one OTM put at an even lower strike price, selling one OTM call at a higher strike price, and buying one OTM call at an even higher strike price.

The strategy implementation starts with selling a put option at a strike price below the current market price, followed by buying a protective put at an even lower strike. The next step involves selling a call option above the current market price and buying a protective call at an even higher strike. All options share the same expiration date, typically 30-45 days out in Indian markets. The position generates immediate premium credit at entry, averaging ₹5,000-7,000 per lot on Nifty options.

Traders select strikes based on probability analysis, with short options placed at 30-delta and long options at 15-delta. Market data shows optimal results with strikes spaced 100-200 points apart on index options. The maximum profit materializes at expiration with the underlying price settling between the short strikes.

Position management requires monitoring option Greeks, particularly delta and theta values. Market makers maintain consistent width between spreads, typically 200-300 points on Bank Nifty options. The structure provides defined risk-reward parameters, limiting potential losses to the difference between strikes minus the credit received.

What is an Example of Short Iron Condor?

Let us look at example of short iron condor, involving nifty. Nifty’s weekly expiry is due today. A Short Iron Condor is composed of two credit spreads on Call and put side, which are deployed simultaneously. It produces a fixed reward and loss outcome.

The chart shows a trading setup for a short iron condor options strategy on the Nifty 50 index (currently at 24381.55) on expiration day. It displays price levels with two blue horizontal lines marking the profit zone boundaries, indicating that profits can be booked if the price closes between these lines by 3:30 PM.

The specific options positions are detailed on the right: one OTM Call at 24400 (selling at 13.9), one Far OTM Call at 24450 (buying at 8.2), one OTM Put at 24250 (selling at 10.55), and one Far OTM Put at 24200 (buying at 7.85). Below is the payoff diagram.

The position structure involves selling an OTM Call at 24400 for ₹13.90 and an OTM Put at 24250 for ₹10.55, while buying protection with a Far OTM Call at 24450 for ₹8.20 and a Far OTM Put at 24200 for ₹7.85.

This strategy generates a net credit of ₹8.40 per share, totaling ₹630 for the standard lot size of 75 shares. The net credit is calculated by subtracting the total premium paid (₹16.05) from the total premium received (₹24.45).

The maximum profit equals the net credit received (₹630) and occurs when all options expire worthless, which happens if the Nifty 50 closes between 24250 and 24400 at expiration. This range represents the “sweet spot” where the trader captures the entire premium.

The maximum loss is limited to ₹3,120, calculated by subtracting the net credit (₹630) from the maximum intrinsic value of the spread (₹3,750). This loss occurs if the Nifty 50 moves significantly, closing either below 24200 or above 24450.

The breakeven points establish the profit zone boundaries. The lower breakeven point is approximately 24242.0 (calculated as 24250 minus ₹8.40), while the upper breakeven is around 24408.0 (calculated as 24400 plus ₹8.40).

This strategy is ideal for traders expecting low volatility, with the underlying asset remaining within a specific range through expiration. The defined risk-reward profile makes it suitable for traders seeking controlled exposure to market movements.

Why Use a Short Iron Condor Strategy?

Traders use short iron condor strategies as they provide traders with a market-neutral approach to generate income in range-bound markets while defining maximum risk and reward from the outset. This options strategy involves simultaneously selling an out-of-the-money (OTM) call spread and an OTM put spread with the same expiration date. The beauty of this strategy lies in its ability to profit when the underlying asset trades within a specific price range, making it ideal when you expect low volatility.

Iron condors appeal to traders seeking consistent premium collection rather than attempting to predict significant directional moves. The strategy requires less capital than naked option selling while still offering attractive risk-reward profiles. The maximum profit occurs when the underlying asset closes between the two sold strikes at expiration.

This strategy works particularly well in markets displaying range-bound characteristics with implied volatility higher than realized volatility. Historical data shows that markets tend to spend significant time trading within established ranges rather than making dramatic moves. Iron condors capitalize on this tendency and benefit from time decay, which accelerates as expiration approaches.

Risk management becomes straightforward as maximum loss is clearly defined by the difference between strike prices minus the premium received. Traders appreciate the defined risk aspect compared to other premium-selling strategies like naked strangles. The position benefits from multiple factors working simultaneously—theta decay, volatility contraction, and price stability.

Unlike directional strategies that require precise timing, iron condors offer a significant “sweet spot” for profitability. The wider the spread between your short strikes, the higher your probability of profit. This adaptability allows traders to adjust the risk-reward profile to match their market outlook and risk tolerance.

When to Use a Short Iron Condor?

The best time to use short iron condor is during periods of market consolidation or when price action suggests an established trading range will persist. This strategy shines brightest in environments where the market lacks clear directional conviction but displays elevated implied volatility levels. Below is a similar situation.

Earnings seasons often present prime opportunities for implementing iron condors. Statistics reveal that while implied volatility typically rises before earnings announcements, approximately 75% of stocks move less than expected after releasing results. This volatility overpricing creates favorable conditions for selling premium through structured strategies like iron condors.

Technical analysis indicators suggesting strong support and resistance levels provide additional confirmation for iron condor implementation. Look for assets that have respected price boundaries multiple times or demonstrate clear consolidation patterns on charts. The presence of well-defined price channels increases the probability of the underlying remaining within your profit zone.

Market environments following major economic announcements often transition into consolidation phases ideal for iron condors. The initial volatility spike from events like Federal Reserve meetings or employment reports frequently subsides into range-bound trading. These post-announcement periods offer attractive premium-selling opportunities while the market digests information.

High implied volatility rank (IVR) or implied volatility percentile (IVP) readings serve as quantitative signals for iron condor consideration. Research indicates that options strategies selling premium perform substantially better when implemented during periods of elevated IVR compared to low IVR environments.

Seasonal patterns also influence iron condor effectiveness, with certain calendar periods historically exhibiting lower volatility. Summer months often demonstrate reduced market movement, creating favorable conditions for premium-selling strategies. The statistical tendency for decreased volatility during specific time frames provides another timing element for optimal iron condor deployment.

How Option Greeks Affects Short Iron Condor?

Delta exposure in short iron condors remains relatively neutral at initiation, making the position less sensitive to small directional moves in the underlying asset. This balanced delta profile stems from the offsetting nature of the strategy’s four options components. The short call delta approximately equals the negative value of the short put delta when structured properly around the current price, while long options provide protective delta boundaries.

Vega exposure creates a vulnerability for iron condors since the position benefits from decreasing implied volatility after entry. The negative vega characteristic means the position loses value if volatility increases unexpectedly during the trade.

Research demonstrates that iron condors implemented when implied volatility sits above the 75th percentile historically outperform those established during lower volatility environments, as they benefit from the statistical tendency of volatility to revert toward mean levels.

Gamma risk increases dramatically as expiration approaches, particularly if the underlying price approaches either short strike. This accelerating gamma effect creates potential for rapid position deterioration if the underlying makes a sudden move near expiration.

Experienced traders often manage positions before entering this high-gamma period, typically closing trades when they’ve captured 50-75% of maximum potential profit regardless of days remaining.

Rho impacts iron condors less significantly than other Greeks but becomes more relevant in high interest rate environments or for longer-dated positions. The relationship between interest rates and option pricing affects the skew between put and call pricing, potentially altering the symmetry of your iron condor setup.

The differential impact of rate changes on puts versus calls requires consideration during initial position structuring to maintain appropriate risk balance.

The interplay between Greeks creates dynamic position characteristics throughout the trade lifecycle. Early in the trade, vega exposure typically dominates performance, while theta becomes increasingly influential as expiration approaches.

How to Trade using Short Iron Condor?

To trade with a short iron condor strategy, choose range-bound stock movements, specifically when the price consolidates between two defined levels during the option contract’s lifetime. This strategy works best when a stock shows signs of losing momentum and enters a period of consolidation.

For Bajaj Finance, technical analysis suggests the stock may trade within the two blue lines shown in the chart until expiration in 29 days.

The iron condor involves four option legs that create a position with defined risk and reward parameters. In this specific trade, we’ve sold an OTM put at ₹7900 for ₹50 and bought a protective far OTM put at ₹7700 for ₹30. We’ve also sold an OTM call at ₹9300 for ₹60 and bought a protective far OTM call at ₹9400 for ₹50.

These four options combined create a net credit of ₹30 per share, which equals ₹3,750 total credit for the 125 lot size. This net credit represents the maximum profit potential if Bajaj Finance stock expires between the short strikes of ₹7900 and ₹9300. All options would expire worthless in this scenario, allowing us to keep the entire premium.

The position is structured with asymmetric risk, having less risk to the upside than the downside. This reflects a specific market bias or risk preference built into the trade setup. The payoff diagram clearly illustrates this risk-reward relationship with its characteristic shape showing limited profit potential and defined maximum loss.

The maximum loss occurs if the stock price moves significantly beyond either wing of the condor. With a spread width of 200 points, the maximum potential loss is ₹21,250 after accounting for the premium received. This loss would occur if the stock price drops below ₹7700 or rises above ₹9400 at expiration.

The breakeven points for this trade are ₹7870 on the downside and ₹9330 on the upside. Between these points, the trade will be profitable, with maximum profit occurring anywhere between the two short strikes. The wider this profit zone, the higher the probability of success but typically at the cost of reduced premium income.

Momentum in either direction poses a significant risk to this strategy. Strong bullish or bearish movements beyond the wings would result in the maximum defined loss. This makes the iron condor ideal for markets expected to trade sideways or within a range.

The success of this trade depends on correctly identifying a stock that will remain range-bound. Bajaj Finance’s technical indicators suggest consolidation between support and resistance levels, making it a suitable candidate for this strategy. If the stock behaves as expected and expires within the profit zone, the full premium of ₹3,750 will be realized as profit.

What is the Maximum Profit & Loss, Breakeven on a Short Iron Condor?

The maximum profit on a short iron condor is the net credit received when opening the position. This occurs when the underlying asset’s price stays between the two short strikes at expiration.

The strategy involves selling an out-of-the-money call and put while simultaneously buying a further out-of-the-money call and put, creating a range. The net credit received is your maximum gain, realized if the stock remains within the short strike boundaries.

The maximum loss is the difference between the strike prices of the call or put spread minus the net credit received. This happens if the stock moves beyond either of the long strikes, resulting in one of the spreads fully in-the-money.

Loss is defined and capped due to the protective long options on both sides. This makes it a popular strategy for traders who expect low volatility but still want risk limits.

The breakeven points are calculated by adding and subtracting the net credit from the short call and short put strike prices. These define the range where the strategy transitions from profit to loss.

The beauty of a short iron condor lies in its defined risk and reward structure. It rewards traders for accurately forecasting low volatility within a certain price range.

This structure makes it appealing for sideways markets. However, misjudging volatility or timing can result in quick losses if the price breaches the breakeven levels.

How to Adjust a Short Iron Condor?

To adjust a short iron condor, traders shift strikes or hedge with additional positions to reduce risk or enhance potential reward. Adjustments are typically based on how the underlying asset moves relative to the strike prices.

The position becomes vulnerable if the price begins approaching either short strike. One common adjustment is rolling the threatened side further out-of-the-money to maintain a safe zone.

Another method is to convert the condor into a butterfly or condor with wider wings. This gives the trade more room to breathe if the asset trends more than expected.

Widening the wings means buying or selling additional options to realign the risk profile. It’s a balancing act between collecting more premium and controlling loss exposure.

Hedging with directional options like calls or puts is also an effective adjustment. For instance, if the price moves toward the call side, buying a call can help offset losses.

These hedges reduce net exposure and provide partial protection. They’re often used temporarily while monitoring whether the move is sustained or a short-term fluctuation.

Another approach is to close the entire position early if the trade turns against you. This limits further losses and frees up capital for better opportunities.

Exiting early, especially when losses are small, is a disciplined way to preserve capital. Waiting too long could result in hitting the maximum loss quickly if volatility surges.

Timing and decisiveness are critical in adjusting a short iron condor. The earlier the adjustment, the higher the chance of retaining some premium or reducing risk.

Waiting until expiration week reduces flexibility. Adjusting with more than 10-15 days left ensures better pricing and options for realignment.

What are the Risks of Short Iron Condor?

The primary risk of a short iron condor is a strong move in the underlying asset that breaches the breakeven points. This leads to potential max loss if held to expiration.

When the stock surges or drops sharply, one side of the iron condor becomes fully in-the-money. The long option limits the loss, but it still results in a defined and unavoidable loss.

Another risk is increasing implied volatility, which inflates option premiums and hurts the position. Since the condor is a net seller of premium, volatility expansion works against it.

Even if the price remains near the center, volatility spikes can create unrealized losses before expiration. This may lead to premature exits or stressful decision-making.

Time decay works in favor of the short iron condor, but only if the price stays within the expected range. If the stock moves aggressively early in the trade, time decay won’t help.

Theta decay accelerates in the last few weeks of the trade. But if price breaches begin early, losses will mount faster than time decay offsets them.

One overlooked risk is assignment, particularly if one leg gets in-the-money before expiration. This creates unwanted stock positions and margin complications.

While most traders use European-style index options to avoid early assignment, stock options on equities can introduce this risk. Monitoring open interest and avoiding expiration week helps reduce it.

Liquidity and slippage also pose risks to managing and exiting the position. If the spreads are wide, getting filled at good prices becomes harder, especially during fast markets.

Poor liquidity leads to suboptimal adjustments or exits. It’s essential to use liquid underlyings with tight bid-ask spreads to manage this risk effectively.

Psychological risk plays a role. Traders often hesitate to adjust or exit due to hope or fear, turning manageable losses into full losses.

Is Short Iron Condor Strategy Profitable?

Yes, a short iron condor strategy is profitable when the underlying asset stays within a specific price range until expiration. The trader collects a net credit upfront, which becomes the profit if the options expire out-of-the-money.

The strategy thrives in low-volatility environments where the price remains stable. It rewards traders who correctly forecast that the underlying will trade within a defined range.

The profitability depends on proper strike selection, timing, and market conditions. Wider ranges offer more room but generate lower premiums, while narrow ranges offer higher rewards with tighter risk zones. Maximum profit is the net credit received and occurs when the price stays between the two short strikes. Profitability increases with repeated setups in calm markets and disciplined management.

However, returns are capped and losses, although limited, are larger than the potential profit. This skewed risk-to-reward ratio demands a high win rate to stay net profitable over time.

The strategy suits traders who prefer consistency and structure over large wins. With proper risk control and volatility assessment, it provides a steady edge in range-bound markets.

Short iron condors are often part of an income-based trading plan. They deliver better results when combined with technical levels, implied volatility analysis, and exit planning.

Is Short Iron Condor Bullish or Bearish?

A short iron condor is a neutral strategy, neither bullish nor bearish. It profits when the underlying asset remains between two strike prices without large price movements.

The strategy involves selling a call spread and a put spread, creating a zone of maximum profitability. This zone centers around the current price, reflecting a market-neutral stance.

Traders use it when they expect low volatility and minimal directional movement. The goal is to have all options expire worthless, allowing the trader to keep the full premium.

It performs poorly in trending or volatile environments, regardless of direction. A strong move higher or lower leads to losses as one spread becomes fully in-the-money.

Unlike bullish or bearish vertical spreads, the iron condor lacks directional bias. Its success depends on time decay and price stability, not on market trends. To align with slight directional expectations, traders shift the short strikes closer on one side. This creates a directional tilt while keeping the overall structure neutral.

What are Alternatives to Short Iron Condor Strategy?

Alternatives to the short iron condor include the iron butterfly, credit spreads, and strangles. Each offers a different balance of risk, reward, and directional bias.

An iron butterfly is similar to the iron condor but uses the same strike for both short options. This increases maximum profit but narrows the profitable range, making it more precise and potentially riskier.

A credit spread is a simpler directional trade using only one side—either a call or put spread. It suits traders with a bullish or bearish outlook and offers clearer management with fewer moving parts.

A strangle involves selling an out-of-the-money call and put without protection, offering unlimited risk. It provides higher premiums but requires far stronger risk control compared to the defined-risk structure of the condor.

Each strategy serves different market conditions and trader preferences. The iron condor fits best when expecting consolidation, while the butterfly suits low-volatility environments with more precise range predictions.

Credit spreads work well in trending markets with moderate conviction. Strangles are for experienced traders aiming to benefit from overstated implied volatility.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 56")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 57")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 58")

: Overview, 10 Types of Indicators, Settings for Different Markets 59")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 62")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 65")

No Comments Yet.