A double calendar spread is an advanced options strategy designed to profit from time decay and changes in implied volatility, often employed by traders seeking market-neutral exposure. A double calendar spread involves simultaneously selling a call and a put at one strike price with a near-term expiration, while buying a call and a put at the same strike prices but with a longer-term expiration.

By doing so, traders position themselves to take advantage of the faster time decay in the near-term options compared to the slower decay in the longer-term options.

What is a Double Calendar Spread?

A double calendar spread is an options strategy that combines two calendar spreads—one using calls and the other using puts—at different strike prices but with matching expiration structure.

The core idea is to sell a near-term call and put at selected strike prices and simultaneously buy a longer-term call and put at the same strikes, creating a position that profits from time decay and rising volatility.

The double calendar spread involves a net debit, meaning you pay more for the longer-term options than you receive from selling the near-term ones. This setup creates a profit zone between the two strikes, with the maximum reward occurring if the underlying price settles near the short strikes as the front-month options expire.

Traders often choose strikes just out-of-the-money (OTM) to maximize their chances of profit, especially when the underlying is expected to stay within a certain range.

How Does a Double Calendar Spread Work?

A double calendar spread works by exploiting the difference in time decay between short-term and long-term options at two different strike prices, creating a market-neutral profit profile.

To set up the trade, consider a stock trading at Rs 100: you sell a near-term call at Rs 105 and buy a longer-term call at the same Rs 105 strike, while simultaneously selling a near-term put at Rs 95 and buying a longer-term put at Rs 95.

This results in a position that benefits from the faster decay of the short-term options relative to the slower decay of the long-term options.

The trade is initiated for a net debit, as the longer-dated options cost more than the premium received for the shorter-dated ones.

Maximum profit is achieved if, at the expiration of the near-term options, the stock price closes somewhere between the two strikes (Rs 95 and Rs 105). In this scenario, both the short call and short put expire worthless, while the long options retain value due to their longer time to expiration.

Incase the underlying price moves sharply outside the strike range, the risk is limited to the net debit paid upfront. The structure’s flexibility allows for adjustments, such as rolling the short options forward or shifting the strikes, depending on market movement or changes in volatility.

This setup is especially effective ahead of anticipated volatility increases or when price action is expected to remain range-bound.

Why Use a Double Calendar Spread Strategy?

Traders use double calendar spreads because the strategy profits from time decay and volatility expansion, providing a market-neutral way to benefit from sideways price action.

By selling options that lose value quickly and buying those that decay slower, the double calendar spread generates positive theta, meaning the position naturally gains value as time passes—assuming the underlying price doesn’t move too far from the strike zone.

Another key benefit is the strategy’s positive vega, making it an ideal choice in periods of low implied volatility when an increase is anticipated.

For example, traders frequently deploy double calendars ahead of earnings announcements, major economic data releases, or Federal Reserve meetings, aiming to capitalize on the expected jump in volatility. The risk profile is defined by the net debit paid, making losses predictable and manageable.

Market neutrality is another appeal; the spread doesn’t require a directional bet, so it suits traders expecting choppy or range-bound markets.

Flexibility is also a hallmark, as traders can adjust strikes, roll short options, or close the position early in response to changing market conditions. This adaptability, combined with the strategy’s structural advantages, makes it a favorite for those seeking steady, controlled returns in calm or uncertain markets.

When to Use a Double Calendar Spread?

A double calendar spread is best used when implied volatility is low but expected to rise, and when the underlying asset is likely to trade within a defined range. This setup is especially attractive ahead of scheduled binary events, such as earnings or central bank announcements, where volatility typically increases as the event approaches.

Deploying the strategy during sideways or choppy market periods allows traders to profit from time decay without betting on a specific direction.

However, it’s important not to hold the position through the actual event, as an immediate drop in implied volatility can erode gains. The most favorable environment is when the underlying trades quietly, implied volatility is suppressed, and a catalyst is on the horizon to boost volatility.

Selecting a liquid underlying is crucial to ensure tight bid/ask spreads and efficient execution. Double calendar spreads thrive when the timing of volatility expansion aligns with the decay of the short-term options, so careful planning around market events and volatility cycles is essential for success.

How Option Greeks Affects Double Calendar Spread?

Double calendar spreads exhibit distinct Greek exposures, benefitting from positive theta and vega, while carrying near-zero to slightly negative gamma.

Positive theta means the position accrues value as the near-term options decay faster than the long-term ones, generating profit every day the underlying remains within the defined range. This time decay accelerates as expiration approaches, making active management critical.

Vega exposure is also positive, so an increase in implied volatility—especially in the longer-dated options—boosts the value of the position. This makes double calendars a favorite ahead of volatility events, as rising vega offsets the cost of holding the trade.

Gamma, meanwhile, is close to zero or slightly negative, indicating the position isn’t highly sensitive to sudden price swings; however, gamma risk grows as expiration nears, so large moves in the underlying can erode profits or expand losses.

How Implied Volatility Affects Double Calendar Spread?

Implied volatility (IV) has a major impact on double calendar spreads, with IV expansion boosting profits and IV contraction causing early losses. Incase of IV rising after entering the trade, especially in the longer-term options, the value of the entire spread increases—making the position more profitable.

This sensitivity to vega is why traders seek to open double calendars when IV is low and poised to rise.

Conversely, entering the trade during periods of high IV—particularly if that volatility is likely to decline sharply—poses significant risk. An “IV crush,” commonly seen after earnings or major news events, reduces the value of the back-month options, potentially wiping out gains or increasing losses.

To time entries, traders use tools like IV rank and IV percentile, which compare current IV levels to historical ranges, helping to identify optimal moments for deploying the strategy.

Avoiding double calendars in high-IV environments with anticipated IV drops is crucial. Instead, these spreads work best when volatility is temporarily suppressed yet a catalyst looms that could drive it higher. Proper IV analysis and timing can make the difference between a winning and losing calendar spread.

How to Trade using Double Calendar Spread?

Trading a double calendar spread begins with selecting a liquid underlying and ends with active management near expiration. Start by choosing a stock or index with ample options liquidity.

In the current setup, one OTM Call at 25100 is sold in the current expiry for ₹63.4. Simultaneously, one OTM Put at 24200 is sold in the current expiry for ₹62.85.

To hedge and benefit from longer-term volatility, a Call at 25100 is bought in the farther expiry for ₹197.4. Likewise, a Put at 24200 is bought in the farther expiry for ₹171.95.

The net debit or cost of entering this trade is calculated as the difference between total premium paid and total premium received. That is, ₹197.4 + ₹171.95 – ₹63.4 – ₹62.85 = ₹243.10 per lot.

With a lot size of 75, the total debit comes to ₹243.10 × 75 = ₹18,233. This is the maximum loss the strategy could incur if all options expire worthless.

Maximum profit in this setup occurs when both short legs expire worthless. In this case, the long-dated options still retain some time value, allowing a profit to be made.

The maximum profit is estimated at ₹8,247. This peak profit usually happens near the strikes of the short options where price remains range-bound until expiry.

A Double Calendar Spread typically has four breakeven points. These are due to the mismatch in time decay between the two expiries.

The breakeven zones for this trade are approximately 24085.0, 24550.0, 24642.0, and 25323.0. Price staying within this range increases the chance of profitability.

This structure profits from time decay and works best in a low to moderate volatility environment. The profit peaks at the strike prices of the short options, which in this case are 25100 and 24200.

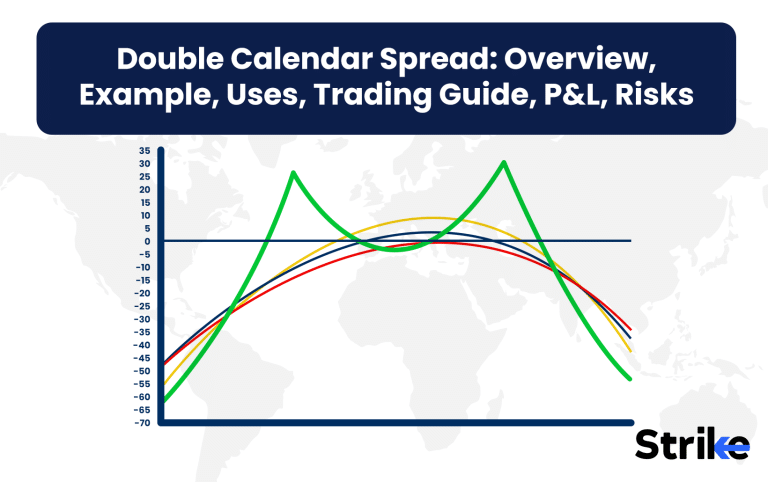

What are the Maximum Profit & Loss, Breakeven on a Double Calendar Spread?

Maximum profit on a double calendar spread occurs when the underlying price is at or near the short strikes at front-month expiration, while the maximum loss equals the net debit paid to enter the trade.

The ideal scenario is for both the short call and short put to expire worthless, leaving the long-term options with residual value due to their remaining time premium.

The breakeven points for a double calendar spread aren’t fixed, as they depend on volatility and time remaining. However, a general rule is that breakevens are set just outside the short strikes, and traders may adjust the strikes to widen or narrow this range according to their market outlook.

The unique profit and loss profile creates a tent-shaped payoff diagram, with the peak at the strike prices and losses limited to the upfront premium if the underlying moves sharply outside the range.

To calculate breakeven, add and subtract the net debit from each strike price, though this is only an estimate since changes in volatility and time premium affect the result. A visual payoff diagram helps clarify this setup: profits peak in the middle, while losses are capped and only occur if the underlying makes a significant move away from the center.

What are the Risks of Double Calendar Spread?

The primary risk in a double calendar spread is losing the entire net debit paid if the underlying moves far beyond the short strikes, with additional dangers from volatility shifts and execution issues.

Leaving the trader exposed to the full loss of the premium paid. Implied volatility crush, often following a major event, is another significant risk that lowers the value of the longer-term options and damages the position’s profitability.

Gamma risk rises as the front-month options approach expiration, making the spread more sensitive to sudden price changes.

This means that even a small move in the underlying can quickly erode gains or turn a profitable trade into a losing one late in the cycle. Execution risk is also present, as multi-leg strategies require careful order entry and attention to liquidity, especially in less liquid names.

Margin requirements must be considered, as brokers may require additional capital for multi-leg spreads. Monitoring and adjusting the position, or closing early if price action threatens the profit zone, are key risk management practices. Awareness of these risks enables traders to size positions appropriately and act quickly when market conditions change.

Is Double Calendar Spread Strategy Profitable?

Yes, a double calendar spread strategy is potentially profitable when used in the right market conditions, as it benefits from time decay and volatility expansion.

The highest probability of success comes when traders deploy the spread in low-volatility environments with an anticipated rise in implied volatility. When executed correctly, the position can deliver steady, defined returns, especially if the underlying price remains within the chosen range.

However, profitability isn’t guaranteed. Losses occur if the underlying makes a strong move outside the profit zone, or if implied volatility drops sharply after entry. The net debit paid limits the downside, but repeat losses from poorly timed entries or holding through unfavorable volatility conditions can erode long-term returns.

Active management and disciplined entry criteria are essential to maximize the profitability of this strategy. By focusing on optimal market conditions and adjusting or closing trades as circumstances evolve, experienced traders use double calendar spreads to generate consistent, risk-controlled profits over time.

Is Double Calendar Spread Bullish or Bearish?

Double calendar spreads are neutral strategies, neither bullish nor bearish, as they profit from range-bound movement rather than directional price changes. The structure is designed to benefit if the underlying stays within a targeted range, maximizing gains when the price settles near the short strikes at front-month expiration.

While adjustments can tilt the bias slightly bullish or bearish—by shifting strike selection above or below the current price—the standard double calendar is market neutral. This makes it an attractive choice for traders who anticipate little directional movement but expect volatility to rise or remain stable.

The neutrality of the strategy is its biggest appeal, allowing traders to profit in sideways markets where other directional strategies would struggle. It’s a go-to option for those seeking to monetize time decay and volatility, without making big bets on market direction.

What are Alternatives to Double Calendar Spread Strategy?

Alternatives to double calendar spreads include the iron condor, butterfly spread, and single calendar spread, each offering distinct advantages and drawbacks.

| Strategy | Pros | Cons |

| Double Calendar | Profits from IV rise, wide profit zone, defined risk | Sensitive to IV crush, complex management |

| Iron Condor | Profits from high IV, easy adjustment, defined risk | Exposed to large moves, less Vega benefit |

| Butterfly Spread | Defined risk/reward, potential high return | Limited profit zone, lower probability |

| Single Calendar | Simpler, lower capital, easy to manage | Narrower profit zone, less flexibility |

The iron condor is also a neutral strategy but works best in high-volatility environments, profiting from the rapid decay of out-of-the-money options.

Its risk/reward profile is similar, but the iron condor benefits from IV contraction, whereas the double calendar thrives on IV expansion.

The butterfly spread provides a similar tent-shaped profit and loss profile, with defined risk and reward, but typically offers lower probability of success and a narrower profit range.

It’s less sensitive to volatility changes but requires precise timing and price targeting. The single calendar spread is a simpler version, using either calls or puts at one strike price; it requires less capital and is easier to manage, though its pro.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 20")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 21")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 22")

: Overview, 10 Types of Indicators, Settings for Different Markets 23")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 26")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 29")

No Comments Yet.