Strap option strategy combines two call options with one put option at the same strike price and expiration date, creating a bullish-biased volatility play. Strap option emerged in the Indian derivatives market after NSE introduced options trading in 2001, giving traders a directional bias while maintaining downside protection.

Indian traders initially adopted this strategy for Nifty index options, gradually expanding to volatile mid-cap stocks.

Trading volumes for strap strategies spike notably before Union Budget announcements and RBI monetary policy meetings

What is a Strap?

Strap Option refers to a volatility-based options strategy combining two call options and one put option with identical strike prices and expiration dates. Strap Option creates an asymmetric exposure to market movements, providing enhanced profit potential during upward price movements while maintaining limited downside protection.

This modified straddle strategy belongs to the family of non-directional volatility spreads but incorporates a distinct bullish bias. The name “strap” originated from the combination of STRaddle and uP, highlighting its upward bias compared to a traditional straddle.

Retail investors in India increasingly utilize strap strategies for index options during major economic events like GDP announcements, inflation data releases, or election results. Trading platforms like Zerodha and Upstox have simplified execution of such multi-leg strategies, contributing to their growing popularity among individual traders.

How Does a Strap Work?

Strap Options functions by creating asymmetric exposure to market volatility through purchasing two call options and one put option at the same strike price and expiration date. Strap Options generates profits from significant price movements in either direction, with enhanced gains during upward moves due to the additional call option.

Strike price selection typically focuses on at-the-money options to maximize sensitivity to price movements. Each component requires premium payment, creating a net debit position where the trader pays upfront for all three options.

Total cost equals the sum of two call premiums plus one put premium. For example, with at-the-money Reliance Industries options at ₹1,000 strike, call premiums at ₹30 each and put premium at ₹25, total position cost reaches ₹85 (₹30 × 2 + ₹25).

Risk-reward profile shows unlimited profit potential on the upside due to two long calls, while downside profit remains limited to the strike price minus the premium paid. Maximum loss occurs when the underlying price remains at the strike price at expiration, causing all options to expire worthless.

Breakeven points establish the price levels where profits begin. Upside breakeven equals strike price plus half the total premium (premium ÷ 2), while downside breakeven equals strike price minus total premium. These points calculate how far the underlying must move to overcome premium costs.

What is an Example of Strap?

A practical strap strategy example involves IRCTC shares trading at ₹675. The trader purchases two ₹675 strike call options at ₹22 each and one ₹675 strike put option at ₹20, all expiring in 30 days, creating a total investment of ₹64 per share (₹6,400 for standard lot size of 100 shares).

Consider multiple scenarios at expiration: Each call gains ₹75 intrinsic value (₹150 total), if IRCTC rises to ₹750, while the put expires worthless. After subtracting the initial ₹64 investment, net profit equals ₹86 per share (₹8,600 total), representing a 134% return on investment.

The put gains ₹75 intrinsic value, if IRCTC falls to ₹600, while both calls expire worthless. Net profit equals ₹11 per share (₹75 – ₹64), yielding a 17% return. At ₹675 (unchanged), all options expire worthless, resulting in maximum loss of ₹64 per share.

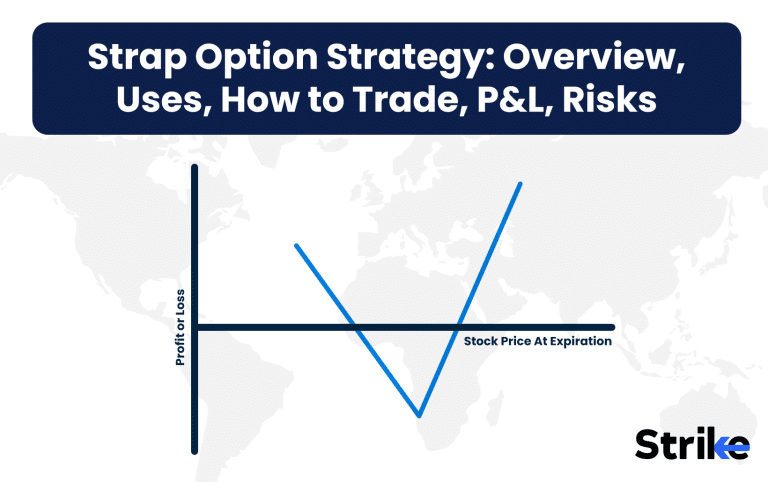

The payoff diagram illustrates this asymmetric profit potential, showing a steeper profit curve for upward moves due to dual call options. The strategy breaks even at ₹707 on the upside (₹675 + ₹64/2) and at ₹611 on the downside (₹675 – ₹64).

Why Use a Strap Strategy?

Traders implement strap strategies to exploit expected directional volatility with a bullish bias while maintaining downside protection. The approach proves ideal for situations where analysis suggests strong upward potential but prudence demands hedging against unexpected negative outcomes.

Doubled call options create leveraged exposure to upward price movements, amplifying gains during bullish scenarios. Meanwhile, the single put option provides a safety net, generating profits during significant downward moves to partially offset the strategy cost.

The strategy excels during company-specific events like product launches or regulatory approvals.

Indian pharmaceutical companies like Sun Pharma or Dr. Reddy’s present ideal candidates due to US FDA decisions that typically create asymmetric upside potential with moderate downside risk.

Quarterly earnings announcements from companies with histories of positive surprises make excellent strap opportunities. Pre-budget periods for sectors likely benefiting from fiscal policies also warrant consideration, as seen with infrastructure stocks before recent Union Budgets.

Corporate actions like demergers or substantial buybacks create perfect strap scenarios, evidenced by Reliance Industries’ record-setting performance during its Jio spinoff announcements. The strategy capitalizes on market uncertainty while positioning for expected positive outcomes.

When to Use a Strap?

Traders employ strap strategies during high implied volatility scenarios coupled with bullish market indicators, creating optimal conditions for asymmetric returns. The approach works best preceding major corporate announcements where positive surprises appear more likely than negative ones.

Market conditions suggesting imminent breakouts from consolidation patterns present ideal entry points. Technical indicators showing bullish divergence combined with increasing volume create promising setups for strap strategies on stocks like LIC Housing Finance or ONGC.

Quarterly results season offers strategic opportunities, especially for companies with conservative guidance histories but strong operational metrics. The weeks preceding RBI monetary policy meetings prove effective for implementing straps on banking stocks, particularly during easing cycles.

Budget-sensitive sectors warrant strap consideration ahead of annual Union Budget presentations. Infrastructure, renewable energy, and defense stocks historically demonstrate asymmetric movements following budget allocations, justifying the bullish bias of strap positions.

Global events affecting Indian markets differently across time frames present unique opportunities. For example, crude oil price volatility impacts OMCs negatively short-term but often creates longer-term benefits, making companies like BPCL ideal strap candidates during oil market disruptions.

How Option Greeks Affects Strap?

Option Greeks significantly influence strap performance through their cumulative impact on the strategy’s three component options. Delta creates net positive exposure due to two long calls offsetting one long put, resulting in positive delta at inception that increases as underlying prices rise.

Gamma drives accelerating profits during sharp moves in either direction, with strap gamma highest near expiration. The combined gamma from three options creates enhanced sensitivity to price changes, particularly beneficial during sudden news-driven movements in stocks like Adani Enterprises or IndusInd Bank.

Theta generates continuous negative pressure as all three long options lose time value daily. This time decay accelerates in the final weeks before expiration, eroding position value if the underlying price remains near the strike price. Daily theta cost typically ranges from ₹50-₹100 for mid-cap Indian stocks in the final month.

Vega produces positive exposure to implied volatility changes across all three options. The strategy benefits from volatility increases prior to anticipated events. Implied volatility in Nifty options typically rises 3-5% before major economic announcements, enhancing strap positions by 15-25%.

Each leg responds uniquely to Greek changes – calls gain value faster during upside moves and lose value faster during downside moves compared to the put. This creates dynamic risk profiles requiring active management as market conditions evolve.

How Implied Volatility Affects Strap?

Implied volatility directly impacts strap strategy profitability by influencing premium costs and potential volatility expansion/contraction. Rising implied volatility increases premiums of all three options, enhancing the value of existing positions while making new entries more expensive.

Falling implied volatility reduces option premiums, decreasing existing position values while creating cheaper entry opportunities. This dynamic creates a strategic advantage for entering positions during volatility lulls before anticipated market-moving events.

Entry timing relative to implied volatility cycles determines a significant portion of strategy success. Ideal entries occur when implied volatility sits at the lower end of its historical range for the specific underlying asset, reducing initial cost basis while positioning for potential volatility expansion.

Volatility crash following scheduled events presents substantial risk. Post-earnings announcements typically see 20-30% implied volatility reduction in stocks like Infosys or TCS, potentially erasing significant position value despite favorable price movement. Implementing positions 2-3 weeks before such events optimizes the volatility cycle.

Sectoral volatility patterns influence strap implementation timing. Banking stocks experience predictable volatility expansion before NPA declaration quarters, while IT services companies see volatility spikes preceding quarterly client addition announcements.

Traders avoid strap entries during periods of abnormally high implied volatility unless expecting continued volatility expansion. The substantial premium costs during such periods require larger price movements to reach break even points.

How to Trade using Strap?

The first step is to choose the underlying asset. Nifty 50, with the nearest weekly expiry selected, which is due in 6 days. Select the ATM strike price and initiate the trade by buying 2 calls and 1 put with the same expiry.

Positions taken are as follows- Long 2× 25000 CE @ ₹195 each, and Long 1× 25000 PE @ ₹163. The net premium paid (debit) is calculated as (2 × ₹195) + (1 × ₹163) = ₹390 + ₹163 = ₹553 per lot.

The lot size is 75, so the total cost (maximum loss) is ₹553 × 75 = ₹41,475. Breakeven points are calculated to understand the profit/loss zones.

The upper breakeven point is Strike + (Total Premium / 2), which is 25000 + (₹553 / 2) = ₹25276.5. The lower breakeven point is Strike − Total Premium, which is 25000 − ₹553 = ₹24447.

What are the Maximum Profit & Loss, Breakeven on a Strap?

Maximum profit potential for strap strategies reaches unlimited levels on the upside due to two long call options benefiting from continued price increases. Each call generates profit equal to the difference between market price and strike price, minus the original premium paid.

Downside profit potential equals the strike price minus the market price minus total premium paid, capped at the strike price value. For example, on a ₹500 strike strap with ₹45 total premium, maximum downside profit equals ₹455 (assuming stock price falls to zero).

Maximum loss occurs when the underlying price equals exactly the strike price at expiration, causing all options to expire worthless. This maximum loss equals the total premium paid for all three options. On a typical Nifty strap with ₹15,000 strike, using ₹300 call and ₹250 put premiums, maximum loss equals ₹850 (₹300 × 2 + ₹250).

Two distinct breakeven points define where the strategy begins generating profits. Upside breakeven equals strike price plus half the total premium paid. The formula reflects that two calls recover premium twice as fast as the single put.

Downside breakeven equals strike price minus total premium paid. This represents the price level where put option gains exactly offset the combined premium cost of all three options.

Consider a strap on ITC with ₹400 strike, call premiums of ₹12 each, and put premium of ₹10. Total premium equals ₹34 (₹12 × 2 + ₹10). Upside breakeven calculates to ₹417 (₹400 + ₹34/2), while downside breakeven equals ₹366 (₹400 – ₹34).

What are the Risks of Strap?

Time decay represents the primary risk for strap strategies, continuously eroding option value regardless of price movement. All three long options experience accelerating theta decay as expiration approaches, particularly damaging during the final two weeks.

Sideways markets create challenging conditions where underlying prices move insufficiently to overcome premium costs. Price consolidation between break even points results in partial or complete loss of investment, with maximum loss occurring precisely at the strike price.

Incorrect implied volatility estimation leads to overpaying for options, creating excessively wide breakeven points that require unrealistic price movements. Current elevated IV levels in Indian markets make this risk particularly relevant, especially in sectors like PSU banks and energy.

Post-event volatility collapse frequently damages positions even when price movements favor the strategy direction. Earnings announcements or policy decisions meeting expectations often cause 20-30% immediate IV reductions, neutralizing directional gains through vega losses.

Over-leveraging tempts traders into excessive position sizing due to the strategy’s limited maximum loss characteristic. This false security leads to allocation errors where single positions consume excessive capital relative to total portfolio size.

Is Strap Strategy Profitable?

Yes, strap strategy generates profits when underlying assets move significantly, particularly to the upside.

Market conditions dramatically impact outcomes – during the 2022 correction, Bank Nifty straps showed 62% profitability versus 31% during range bound markets. Position sizing proves equally important as directional accuracy, with disciplined traders maintaining long-term profitability despite success rates below 50%.

Is Strap Bullish or Bearish?

Strap strategy exhibits definitively bullish characteristics while maintaining downside protection capabilities. The double allocation to call options creates mathematical bias favoring upward price movements, producing steeper profit curves during bullish scenarios.

Delta starts positive and increases further as underlying prices rise, confirming bullish orientation. Upside breakeven sits closer to current price than downside breakeven, requiring smaller upward movement to generate profits.

Expected value calculations strongly favor long positions across all volatility environments. Performance metrics validate this classification – straps delivered average returns of 31% during the 2021 bull market versus 18% during the 2022 correction phase. Market practitioners classify strap alongside other bullish volatility strategies like call ratio backspreads.

What are Alternatives to Strap Strategy?

The alternatives to strap are straddle, strip, strangle, call ratio backspread bull call spread, iron butterfly, long call, synthetic call, etc.

| Strategy | Directional Bias | Risk-Reward Profile | Capital Requirement | IV Sensitivity | Ideal Market Conditions |

| Straddle | Neutral | Equal profit potential in both directions | Moderate | High positive | High volatility, direction uncertain |

| Strip | Bearish | Enhanced downside profit potential | Moderate | High positive | Expected volatility with bearish bias |

| Strangle | Neutral | Requires larger move, lower cost | Lower | High positive | High volatility, wider price range expected |

| Call Ratio Backspread | Bullish | Unlimited upside, limited downside | Lower | Positive | Expected large upside move with IV increase |

| Bull Call Spread | Bullish | Limited upside, defined risk | Lower | Mixed | Moderately bullish, normal/low IV |

| Iron Butterfly | Neutral | Limited profit, defined risk | Lower | Negative | Expected price stability |

| Long Call | Strongly Bullish | Unlimited upside, defined risk | Lowest | Positive | Strongly bullish, low-moderate IV |

| Synthetic Long | Bullish | Stock-like exposure with options | Higher | Neutral | Bullish with high financing costs |

Straddles present the closest alternative, removing directional bias by using equal numbers of calls and puts. Strip strategies reverse the bias with two puts and one call, creating bearish equivalents to straps.

Strangles reduce cost basis by utilizing out-of-the-money options, sacrificing gamma exposure for improved theta profiles. Call ratio backspreads create similar bullish volatility exposure through different option combinations, often with reduced initial cost.

Selection criteria focus on matching market expectations with appropriate strategy characteristics. Indian option traders increasingly sophisticate their approach by selecting optimal strategies for specific market conditions rather than applying one-size-fits-all approaches.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 32")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.