Long Strangle Strategy involves purchasing both out-of-the-money (OTM) call and put options with the same expiration date but different strike prices to profit from significant price movements in either direction.

Long Strangle Strategy emerged in the 1970s alongside the establishment of organized options exchanges, gaining popularity among Indian traders seeking to capitalize on market volatility without predicting directional bias.

Traders purchase lower strike puts and higher strike calls, creating a position that profits during large market swings while limiting risk to premium paid. The strategy requires substantial price movement beyond breakeven points to overcome the cost of both options. Implemented effectively during events like Union Budget announcements or quarterly results, the strategy thrives in volatile environments.

What is a Long Strangle?

Long Strangle Strategy entails simultaneously purchasing an out-of-the-money call option and an out-of-the-money put option on the same underlying asset with identical expiration dates but different strike prices.

Long Strangle Strategy creates a position benefiting from significant price movements in either direction while limiting potential loss to the premium paid for both options.

The approach provides exposure to market volatility without requiring a directional bias on the underlying asset. Unlike directional strategies that profit only from upward or downward movements, strangles capitalize on substantial price swings regardless of direction.

Structurally designed for volatility speculation, the strategy positions the call strike price above current market price and the put strike below it. This configuration forms a “strangle” around the current price, capturing profits from breakouts in either direction.

The size of the “window” between strike prices affects both cost and profit potential. Wider windows reduce premium paid but require larger price movements to become profitable. Narrower windows increase costs but need smaller price movements to generate returns.

Both options must be purchased simultaneously to properly execute the strategy, with maximum risk limited to combined premium and break-even points occurring at strike prices plus/minus the total premium paid.

How Does a Long Strangle Work?

Long Strangle Strategy functions by establishing a position that profits from significant price volatility regardless of direction. Long Strangle Strategy requires purchasing both an out-of-the-money call option and an out-of-the-money put option on the same underlying security with identical expiration dates but different strike prices.

Buy an OTM call option (higher strike) and an OTM put option (lower strike). The call option provides unlimited profit potential if prices rise substantially, while the put option delivers profits if prices fall significantly. Purchased together, these options create a position capturing gains from major market movements in either direction.

Profit potential remains unlimited if the price moves sharply in either direction. Should the underlying asset price increase dramatically, the call option’s value rises proportionally while the put expires worthless. Conversely, during substantial price decreases, the put option’s value increases while the call expires worthless.

Premiums paid for both the call and put represent the maximum potential loss. This occurs if the underlying asset price remains between the two strike prices at expiration, causing both options to expire worthless.

Time decay works against long strangles, eroding option value as expiration approaches. Success depends on timing entry around anticipated volatility events while selecting appropriate strike prices and expiration dates.

Why Use a Long Strangle Strategy?

Traders implement long strangle strategies to profit from significant price volatility without predicting directional bias, making them ideal for uncertain market conditions. The strategy capitalizes on major price swings regardless of direction, positioning traders to benefit from volatility itself rather than directional accuracy.

Ideal for volatile markets, strangles perform best during periods of anticipated price turbulence but uncertain direction. The strategy thrives when underlying assets experience substantial movements exceeding the combined premium cost of both options.

Events like quarterly earnings announcements trigger optimal conditions for long strangles in the Indian context. Companies such as JSW Steel, Hindalco, and Sun Pharma historically experience 8-15% price swings post-earnings, creating profitable scenarios for properly positioned strangles.

Regulatory announcements affecting specific sectors create ideal conditions, exemplified by pharmaceutical companies facing USFDA decisions or telecom operators awaiting TRAI rulings. Volatility spikes surrounding these events often exceed 40-60%.

The strategy limits risk to premium paid while maintaining unlimited profit potential, appealing to risk-conscious traders. Additionally, strangles offer flexibility through adjustments prior to expiration, allowing traders to capitalize on interim volatility or limit losses.

When to Use a Long Strangle?

Deploy long strangles during periods of anticipated significant market volatility, particularly before events capable of triggering substantial price movements in unpredictable directions.

Traders establish these positions when expecting dramatic market action but remaining uncertain about directional bias.

Market conditions favoring high volatility provide optimal environments for long strangles. The strategy performs effectively during consolidation phases preceding major breakouts, offering exposure to the eventual directional move without requiring prediction of its direction.

Events triggering heightened volatility include quarterly financial announcements from Nifty companies, typically generating 5-15% price movements suitable for strangle profitability. Indian pharmaceutical companies facing DCGI approvals or USFDA inspections experience similar volatility spikes, creating advantageous conditions.

Indications supporting strangle implementation include rising implied volatility in options pricing, signaling market expectations of increased turbulence. The India VIX index crossing above 20 often precedes major market movements conducive to strangle success.

Technical analysis revealing triangle formations, narrowing Bollinger Bands, or decreasing trading volumes suggests imminent breakouts, presenting opportune timing for strangle establishment. Historical volatility patterns showing cyclical increases also signal favorable conditions.

Appropriate for traders seeking balanced risk-reward profiles, long strangles limit potential losses while maintaining unlimited upside. The strategy suits portfolios requiring hedging against unpredictable directional risks during uncertain market periods.

How Option Greeks Affect Long Strangle?

Option Greeks significantly influence long strangle performance through their combined impact on price sensitivity, time decay, and volatility exposure. Both call and put options maintain positive delta values that respond differently as underlying prices move, creating the position’s distinctive risk-reward characteristics.

Delta measures directional exposure, with the call option gaining positive delta as prices rise while the put develops negative delta. The combined delta approaches zero near the position’s establishment, increasing as prices move toward either strike price. This creates accelerating profits once breakeven points get crossed.

Gamma leads to larger changes in delta as the stock moves toward the strike prices. High gamma values cause the profitable leg’s delta to increase rapidly while the unprofitable leg’s delta diminishes, amplifying gains during strong directional movements. Near expiration, gamma effects intensify, potentially creating outsized profits during late-stage breakouts.

Vega represents volatility sensitivity, with high implied volatility increasing the value of both call and put options. Indian markets frequently experience volatility spikes before major events, benefiting strangle positions through vega exposure. A rising India VIX index generally enhances strangle values independent of price movement.

Theta works against the strategy through continuous time decay. If the underlying asset fails to move significantly, both options steadily lose value as expiration approaches. This effect accelerates during the final weeks, creating urgency for the anticipated price movement to materialize.

The relationship between these Greeks changes dynamically throughout the position’s lifecycle. Early stages feature higher vega sensitivity and moderate theta decay, while later stages experience intensified gamma effects and accelerated theta erosion.

How Implied Volatility Affects Long Strangle?

Implied volatility dramatically influences long strangle profitability by directly affecting option premiums and position valuation throughout its lifecycle. The strategy benefits significantly from increased implied volatility, which elevates the value of both call and put options regardless of price direction.

Volatility impact manifests through both legs of the strangle position, creating opportunities for profit even before significant price movement occurs. Rising implied volatility inflates premium values, potentially allowing profitable exits prior to the anticipated price movement materializing.

Implied volatility raises the premium of both the call and put options through their vega exposure. Each percentage point increase typically enhances option values by their respective vega multipliers, creating substantial gains during volatility spikes common before major Indian market events.

Best results emerge in high IV environments with expectations of large moves. Indian market events like Union Budget announcements, RBI policy decisions, and quarterly results seasons create ideal conditions, with implied volatility often rising 30-50% before these catalysts.

The “volatility smile” phenomenon affects strangles uniquely, with out-of-the-money options experiencing disproportionate IV increases during uncertainty periods. This skew benefits properly structured strangles by enhancing value in both legs simultaneously.

How to Trade using Long Strangle?

The first step to trade using long strangle is to choose an asset with high volatility potential. Nifty 50 has been experiencing significant momentum for 9 consecutive days, indicating a high probability of volatility in the underlying asset.

Given this scenario, an expiry next to the current expiry, which is due in 9 days, has been chosen. The underlying price is expected to show movement on either side, making it an ideal condition for a long strangle strategy.

In this strategy, both a call and a put option are purchased at different strike prices but with the same expiration date. Strangles involve long positions on out-of-the-money (OTM) call and put options. Based on the uploaded option chain, the chosen strikes are ₹24,500 for the call option and ₹24,150 for the put option.

Both options are OTM, and the expectation is for the Nifty to experience significant volatility before expiry. This setup minimizes the impact of theta decay while capitalizing on potential momentum-driven moves in either direction.

The position structure involves buying one OTM call option at a strike of ₹24,500 for ₹145.75 and one OTM put option at a strike of ₹24,150 for ₹156.75. With a lot size of 75, the total premium paid amounts to ₹302.50 per lot, resulting in a maximum loss of ₹22,687.50 (rounded to ₹22,684).

This loss represents the total premium paid and occurs if the Nifty’s spot price at expiry lies between the two strikes (₹24,150 to ₹24,500), causing both options to expire worthless.

The strategy has theoretically unlimited profit potential on either side. If the spot price rises sharply above ₹24,500, the profit is calculated as (Spot Price – ₹24,500 – ₹302.50) × 75. Conversely, if the spot price drops sharply below ₹24,150, the profit is calculated as (₹24,150 – Spot Price – ₹302.50) × 75.

A significant one-sided movement in the Nifty can make the strategy highly profitable, and the position should be exited when either of the options shows substantial gains or when the asset price moves sharply.

The breakeven points for the strategy are calculated as ₹24,802 on the upside (Call Strike + Total Premium per lot) and ₹23,848 on the downside (Put Strike – Total Premium per lot). These breakeven levels mark the points beyond which the strategy begins to generate profits.

The total premium per lot amounts to ₹145.75 + ₹156.75 = ₹302.50, which determines the breakeven thresholds. The profitability zone thus lies outside the range of ₹23,848 to ₹24,802, with losses occurring if the Nifty remains within this range at expiry.

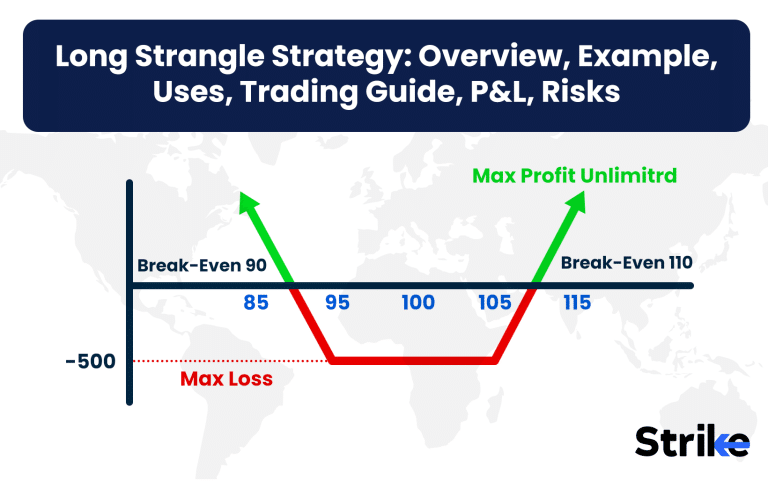

What is the Maximum Profit & Loss, Breakeven on a Long Strangle?

The financial parameters of a long strangle define its risk-reward characteristics through clearly established maximum profit potential, limited loss exposure, and specific breakeven thresholds that determine profitability zones. Maximum profit remains theoretically unlimited as the underlying asset price increases or decreases substantially beyond either strike price.

Maximum loss stays fixed at the total premium paid for both the call and put options. This represents the entire capital at risk, occurring when the underlying asset price settles between the call and put strike prices at expiration, causing both options to expire worthless.

Breakeven points establish the price thresholds where the strategy begins generating profits. The upper breakeven equals the call strike price plus total premium paid (call premium + put premium). The lower breakeven equals the put strike price minus the total premium paid.

For example, with Nifty at 22,000, a strangle using a 22,500 call purchased at ₹150 and a 21,500 put purchased at ₹130 creates a ₹280 total premium investment. The upper breakeven calculates to 22,780 (22,500 + 280), while the lower break even reaches 21,220 (21,500 – 280).

Profitability accelerates as prices move beyond breakeven points. Each rupee movement above the upper breakeven or below the lower break even translates directly to additional profit. This convexity creates asymmetric returns during substantial price movements.

Risk-reward characteristics remain balanced in terms of directional exposure but require significant price movement to overcome the premium investment. The combined premium represents approximately 1.3% of the index value in this example, requiring movements exceeding this percentage for profitability.

What are the Risks of Long Strangle?

Premium decay represents the primary risk facing long strangle positions, continuously eroding option value through theta impact as expiration approaches. The strategy commits capital to two separate options that both experience time decay, creating a “race against time” dynamic requiring significant price movement or volatility increases to overcome.

Loss of the entire premium occurs if the underlying asset remains between strike prices through expiration. Both options expire worthless in this scenario, creating a 100% loss on invested capital. Statistics indicate approximately 60-65% of long strangles on Indian indices result in complete premium loss due to insufficient price movement.

Volatility risk manifests through vega exposure, causing potential value deterioration even during favorable price movement. Implied volatility typically spikes before anticipated events then collapses afterward, creating “volatility crush” scenarios where options lose substantial value despite moderate price changes in the anticipated direction.

Liquidity constraints emerge in certain Indian options, particularly in midcap stocks with limited trading volume. Wide bid-ask spreads increase effective costs while potentially complicating exit execution during rapidly changing market conditions.

Cost management challenges emerge during high implied volatility environments, with premium expenses increasing proportionally to volatility levels. Higher costs necessitate larger price movements to achieve profitability, reducing success probability.

Is Long Strangle Strategy Profitable?

Yes, long strangle strategies generate profits during significant price movements exceeding breakeven thresholds, though statistical analysis reveals only 35-40% achieve profitability across complete market cycles.

Profitability improves dramatically during black swan events or unexpected market developments. Strangles positioned before major geopolitical incidents have historically generated returns exceeding 300-500%, compensating for numerous smaller losses.

Is Long Strangle Bullish or Bearish?

Long strangle strategies maintain neutral directional bias, neither bullish nor bearish but instead volatility-positive in orientation. The strategy profits equally from substantial price movements regardless of direction, focusing entirely on magnitude rather than trajectory.

The position structure incorporates both bullish elements (through the call option) and bearish components (through the put option), creating balanced exposure to both scenarios. Success depends on significant price dislocation rather than directional accuracy. Indian markets frequently experience sector rotation rather than unidirectional movement, making strangles particularly appropriate.

What are Alternatives to Long Strangle Strategy?

Long straddles are considered a good alternative as it provides similar volatility exposure but position both call and put with identical strike prices, increasing cost but reducing the movement required for profitability.

Iron condors create limited-risk positions profiting from range-bound markets, essentially reversing the strangle outlook while defining maximum losses. This strategy performs effectively during consolidation phases in Indian indices between major economic announcements.

Butterfly spreads offer another neutral approach for low volatility environments, combining multiple strikes to create defined risk profiles with maximum profit at the central strike price. The strategy proves particularly effective during extended sideways movements common in Indian mid-cap stocks between earnings seasons.

Short straddles/strangles generate income during stagnant markets but carry unlimited risk during unexpected volatility spikes. Calendar spreads exploit time decay while maintaining directional neutrality through different expiration dates rather than different strike prices.

What’s the Difference Between Long Strangle vs Short Strangle?

Long strangles and short strangles represent directly opposing volatility strategies with inverted risk-reward profiles, premium flow directions, and market outlook assumptions. Long strangles purchase both call and put options to profit from significant price movement, accepting defined maximum loss (premium paid) for unlimited profit potential.

Short strangles sell those same options to generate premium income during periods of expected price stability. The short strangle collects premium upfront but assumes unlimited risk if significant price movements occur. The strategy profits from time decay and decreased volatility, performing optimally when prices remain between strike prices through expiration.

Long strangles benefit from volatility increases and suffer from time decay. Short strangles profit from time decay but suffer during volatility spikes. Position management differs substantially, with long strangles requiring minimal adjustment while short strangles demand active risk management to control potential losses during adverse price movements.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 20")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 21")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 22")

: Overview, 10 Types of Indicators, Settings for Different Markets 23")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 26")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 29")

No Comments Yet.