Short strangle involves selling an out-of-the-money call option and an out-of-the-money put option simultaneously on the same underlying asset with identical expiration dates. Short strangle generates income through premium collection while betting on low price volatility.

Originating in the 1970s during options market formalization, this strategy gained popularity among Indian traders after NSE introduced options trading in 2001. SEBI data shows neutral strategies like short strangles account for approximately 18% of all options strategies used by Indian retail traders.

What is a Short Strangle?

Short strangle represents an options trading strategy where a trader simultaneously sells an out-of-the-money call option and an out-of-the-money put option on the same underlying security with identical expiration dates. Short strangle generates income from the premiums collected from both options sold while betting on limited price movement of the underlying asset.

The strategy creates a profit zone between the two strike prices where the trader keeps the maximum profit if the underlying closes within this range at expiration. Traders implement this market-neutral strategy during periods of high implied volatility to capitalize on inflated option premiums.

The distance between strike prices determines profit probability and maximum potential income. Indian options traders frequently employ short strangles on index options during consolidation phases. The strategy thrives in sideways markets where prices fluctuate within a predictable range.

Lower-volatility securities offer reduced premium income but higher probability of success. Higher-volatility securities provide greater premium collection opportunities with increased risk profiles.

How Does a Short Strangle Work?

Short strangle operates by selling both an out-of-the-money call option and an out-of-the-money put option simultaneously on the same underlying asset. Short strangle creates a price range between the two strike prices where maximum profit occurs if the underlying asset remains within this zone until expiration.

The trader sells a call option with a higher strike price and a put option with a lower strike price. Premiums collected from both options are the trader’s maximum potential profit. The maximum loss is unlimited if the price moves significantly beyond the strike prices.

The strategy works best in markets expecting minimal price movement. Selling both options creates positive theta, meaning the position benefits from time decay as options naturally lose value approaching expiration.

The position requires continuous monitoring as significant price movements in either direction create exponential losses. Margin requirements remain substantial due to the unlimited risk profile, typically requiring 20-25% of the contract value in Indian brokerages.

Strike selection plays a crucial role in determining risk-reward, with many traders selecting strikes outside one standard deviation from the current price. Professional traders adjust positions proactively by rolling strikes or adding hedges if the underlying price approaches either strike.

What is an Example of a Short Strangle?

An example of a short strangle involves Apollo Hospitals with shares trading at ₹5,500. A trader sells the Apollo Hospitals ₹5,700 call option for a premium of ₹80 and simultaneously sells the ₹5,300 put option for a premium of ₹70. The combined premium collected equals ₹150 per share, representing the maximum potential profit.

The upper breakeven point calculates to ₹5,850 (₹5,700 + ₹150), while the lower breakeven point equals ₹5,150 (₹5,300 – ₹150). Apollo Hospitals historically demonstrates range-bound trading during non-earnings periods, making it ideal for this strategy.

The trader expects the stock to remain between ₹5,300 and ₹5,700 until option expiration in 30 days. Healthcare stocks typically demonstrate lower volatility compared to technology or banking sectors, further supporting the strategy selection.

Both options expire worthless, if Apollo Hospitals closes at ₹5,550 at expiration, allowing the trader to keep the entire ₹150 premium as profit. However, significant losses occur if the stock moves beyond either break even point.

For instance, the trader faces a loss of ₹100 per share (₹6,100 – ₹5,850 – ₹150), if Apollo announces unexpected regulatory approvals causing the stock to surge to ₹6,100. Margin requirements for this position would typically range from ₹40,000 to ₹60,000 depending on the broker’s policies.

Why Use a Short Strangle Strategy?

Traders implement short strangle strategies to capitalize on periods of price consolidation while generating income through premium collection. The strategy proves most effective in range-bound markets where prices oscillate within predictable boundaries.

Profit from low volatility emerges as a primary advantage since the strategy performs optimally when the stock remains between the strike prices of the sold options. Profit from time decay represents another compelling benefit as both sold options continuously lose value as expiration approaches, working in favor of the option seller.

Short strangles excel during periods of elevated implied volatility when option premiums become inflated, allowing traders to sell overpriced options. India’s equity markets frequently experience consolidation phases after significant trending movements, creating ideal conditions for short strangle implementation.

The strategy serves as an ideal income generation tool for traders expecting minimal price movement but unwilling to take directional positions. During quarterly results seasons, companies often experience temporarily inflated implied volatility followed by post-results consolidation, creating profitable short strangle opportunities.

When to Use a Short Strangle?

Deploy short strangles during periods of market consolidation when prices trade within established ranges with minimal directional momentum. Market conditions featuring range-bound trading patterns with clear support and resistance levels provide optimal environments for short strangle implementation.

Technical indicators suggesting mean reversion offer additional confidence for executing this strategy. Periods following significant news events often create ideal short strangle opportunities as markets digest information and enter consolidation phases.

High implied volatility environments increase premium collection potential while providing wider breakeven points, enhancing the probability of success. Sectors experiencing seasonal trading patterns with predictable price boundaries present recurring short strangle opportunities for experienced traders.

Indian indices like Nifty and Bank Nifty frequently exhibit range-bound behavior during certain market phases, creating reliable short strangle setups. Implementation works effectively during pre-budget consolidation phases when markets await policy announcements without clear directional bias.

How Option Greeks Affect Short Strangle?

Option Greeks significantly influence short strangle performance, creating dynamic risk parameters that evolve throughout the trade duration.

Delta measures directional exposure with short strangles initially maintaining delta neutrality due to offsetting negative deltas from both sold options.

Gamma represents the position’s delta sensitivity to price changes, turning increasingly negative as the underlying approaches either strike price and accelerate potential losses. Vega quantifies the position’s sensitivity to implied volatility changes with short strangles maintaining negative vega, benefiting from volatility contraction but suffering during volatility expansion.

Theta generates the primary advantage for short strangles by creating positive time decay, with premium erosion accelerating during the final weeks before expiration. Short strangles typically start with minimal directional bias but develop directional exposure if the underlying moves toward either strike price, requiring potential adjustments.

Rho measures interest rate sensitivity, though this Greek typically exerts minimal influence on short-term options strategies. Most Indian options traders prioritize theta and vega management when trading short strangles, actively monitoring these metrics throughout the position lifecycle.

Professional traders establish specific thresholds for each Greek, triggering adjustment decisions when values exceed predetermined levels.

How Implied Volatility Affects Short Strangle?

Implied volatility fundamentally drives short strangle profitability by directly influencing option premium levels and subsequent position behavior. High volatility environments increase option premiums for both calls and puts, enhancing initial credit received and widening the profit zone between break even points.

Volatility contraction following trade entry accelerates time decay and premium erosion, potentially allowing earlier profit taking through position closing at reduced prices. Implied volatility spikes represent the greatest threat to short strangles, potentially increasing option values despite favorable price movement within the expected range.

Volatility term structure influences optimal expiration selection, with flatter volatility curves suggesting shorter-term options while steep curves favor longer durations. Sector-specific volatility patterns require consideration, as industries like information technology and pharmaceuticals typically demonstrate higher implied volatility in Indian markets.

Volatility skew affects strike selection strategy, with steeper skews encouraging asymmetric strike positioning rather than equidistant placement from the current price. Professional traders monitor volatility percentile rankings to identify optimal entry points when implied volatility sits in upper percentiles relative to historical readings.

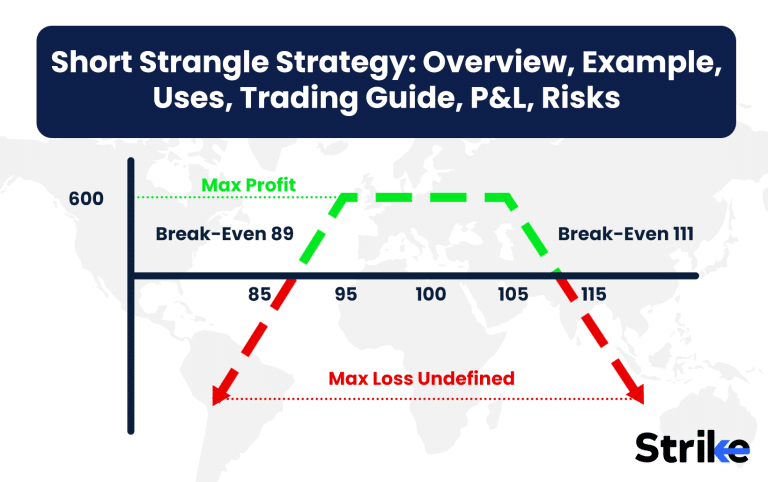

How to Trade using Short Strangle?

The first step in executing a short straddle is to pick a stock or index with low implied volatility or one where no major price movements are expected. In this case, we have chosen Nifty 50, which has been trading in a narrow range. If the index consolidates for another three days, the position is likely to yield profits within the breakeven zone. The expectation is that Nifty will continue to exhibit low implied volatility.

Next, we select the strike price. For maximum premium collection, the strike price should be At-The-Money (ATM). A short straddle is created by selling both a call and a put option at the same strike price and expiry. In this trade, we have sold the 24,450 strike call and put options.

Position Structure (Short Straddle)

Sell 1 ATM Call Option (Strike = ₹24,450) @ ₹105

Sell 1 ATM Put Option (Strike = ₹24,450) @ ₹88

Lot Size = 75

The total premium collected from this position is (₹105 + ₹88) × 75 = ₹193 × 75 = ₹14,475. This amount represents the maximum profit possible from the trade.

It is important to monitor implied volatility and time decay once the position is live. As the expiry date approaches, the shape of the payoff graph shifts depending on how the price, implied volatility, and time decay behave. Regular assessment of the position helps in deciding if adjustments are necessary.

The maximum profit occurs when the Nifty expires exactly at the strike price of ₹24,450. In this scenario, both the call and put options expire worthless, and the trader retains the full premium of ₹14,475.

A major risk of a naked short straddle is the possibility of unlimited losses if the index moves significantly away from the strike price.

- If the price rises sharply:

Loss = (Spot Price − Strike Price − Total Premium per lot) × Lot Size - If the price falls sharply:

Loss = (Strike Price − Spot Price − Total Premium per lot) × Lot Size

This unlimited loss risk can be mitigated by buying cheaper options on either side. Doing so would convert the position into an Iron Condor, which carries defined risk and reward.

There are two breakeven levels in this strategy.

- Upper Breakeven = ₹24,450 + ₹193 = ₹24,643

- Lower Breakeven = ₹24,450 − ₹193 = ₹24,257

So, the breakeven range lies between ₹24,257 and ₹24,643. The position remains profitable as long as Nifty stays within this range by expiry.

When to Exit a Short Strangle?

Exit short strangles based on predefined profit targets, time elapsed, or risk management parameters rather than emotional reactions to market movements. Profit target achievement provides the most straightforward exit signal, with many traders closing positions after capturing 50-75% of maximum potential profit rather than risking gains for marginal additional returns.

Time decay acceleration during the final 10-14 days before expiration creates optimal exit windows balancing risk and reward. Breach of technical support/resistance levels beyond strike prices signals potential trend development, warranting immediate defensive action regardless of profit/loss status.

Position adjustment needs arise when delta values reach predetermined thresholds (typically ±0.25), indicating excessive directional exposure requiring risk recalibration. Implied volatility spikes necessitate reevaluation even with favorable price action, as increased volatility elevates option values contrary to strategy objectives.

Experienced traders establish specific exit criteria before trade entry, removing emotional decision-making during position management. Professional options traders maintain mechanical exit discipline, adhering to predetermined rules regardless of market sentiment or personal bias.

Early exit execution prevents catastrophic losses during black swan events or unexpected news developments impacting the underlying asset.

What are the Maximum Profit & Loss, Breakeven on a Short Strangle?

Maximum profit in a short strangle equals the total premium received from selling both the call and put options. Using a real example with TCS, selling the ₹3,800 call for ₹45 and the ₹3,600 put for ₹55 generates a total premium of ₹100 per share, representing the maximum potential gain.

This maximum profit materializes if TCS closes between ₹3,600 and ₹3,800 at expiration, allowing both options to expire worthless. Maximum loss theoretically remains unlimited on both sides. Downside losses accelerate below the lower breakeven point (put strike minus premium received), while upside losses increase above the upper breakeven point (call strike plus premium received).

Using the TCS example, the lower breakeven calculates to ₹3,500 (₹3,600 – ₹100) and the upper breakeven equals ₹3,900 (₹3,800 + ₹100). Any price beyond these points generates losses exceeding the collected premium.

Risk increases proportionally with price movement beyond breakeven points, requiring disciplined stop-loss implementation. Professional traders calculate risk-reward ratios based on expected trading range versus distance to breakeven points, targeting minimum 1:2 risk-reward profiles.

Margin requirements reflect this unlimited risk profile, with Indian brokers typically requiring substantial collateral proportional to position size.

What are the Risks of Short Strangle?

Unlimited loss potential represents the most significant risk facing short strangle traders, as extreme price movements in either direction create exponential losses exceeding collected premium. Assignment risk emerges when trading American-style options, particularly for deep in-the-money positions, potentially forcing unwanted share purchases or sales at unfavorable prices.

Volatility expansion risk threatens profitability even during favorable price action, as increasing implied volatility elevates option values contrary to the strategy’s objectives. Gap risk poses particular concern in the Indian market, where overnight price movements frequently exceed daily limits due to global events happening during market closure.

Liquidity risk affects position management, as wide bid-ask spreads during market stress periods increase adjustment costs and hamper effective risk management. Correlation breakdowns threaten portfolio-level risk management when multiple short strangles suddenly face directional pressure across different underlyings that historically moved independently.

Is Short Strangle Strategy Profitable?

Yes, short strangle strategies generate consistent profits under specific market conditions with proper implementation and risk management. The strategy delivers optimal returns during consolidation phases featuring low volatility and range-bound price action.

Statistical backtesting indicates probability of profit averaging 65-70% across broad market conditions when executed with appropriate strike selection and position sizing. Profitability depends primarily on disciplined implementation rather than market forecasting accuracy.

Experienced traders achieve higher success rates through systematic volatility analysis and technical parameter adherence rather than subjective market opinions. Risk-adjusted returns typically exceed market averages during low-volatility periods but underperform during trending or volatile market phases.

Is Short Strangle Bullish or Bearish?

Short strangle represents a perfectly neutral strategy with no inherent directional bias when properly structured. The position profits from limited price movement rather than directional trends, generating returns when the underlying asset trades within the range between sold call and put strikes.

The strategy performs identically whether the price drifts slightly upward, downward, or remains completely flat. Professional traders maintain neutrality through dynamic adjustments, rebalancing delta exposure if the position develops directional bias during market movement.

Delta-neutral positioning remains fundamental to proper short strangle implementation throughout the trade lifecycle. Directional exposure emerges only during significant price movements, requiring tactical adjustments to maintain the strategy’s intended market-neutral character.

What are Alternatives to Short Strangle Strategy?

Several alternative strategies address similar market outlooks while offering varied risk-reward profiles compared to short strangles. Iron condors provide similar neutral exposure with defined risk parameters by adding long options outside the short strikes, capping potential losses at the expense of reduced premium income.

Short straddles offer higher premium collection by selling both call and put at the same strike price, but require more precise price forecasting with narrower profit zones. Butterfly spreads create defined risk neutral positions with multiple strikes, offering precise profit targeting with limited risk.

Calendar spreads exploit time decay differentials between near and far-term options while maintaining a similar neutral outlook. Ratio spreads combine elements of directional and neutral trading by selling more options than purchased, creating asymmetric payoff profiles.

Indian market professionals frequently utilize modified versions incorporating index-specific characteristics, such as “Nifty Iron Fly” strategies combining butterfly and iron condor elements for optimized premium capture during expiry periods.

What’s the Difference Between Short Strangle vs Long Strangle?

Short strangle and long strangle represent precisely opposite strategies with fundamentally different objectives and risk profiles. Short strangles involve selling both call and put options to collect premium, profiting from limited price movement and time decay while accepting unlimited risk.

Long strangles require buying both options, accepting limited risk (premium paid) while potentially profiting from significant price movement in either direction. Short strangles thrive during low volatility periods while long strangles perform best during volatility expansion.

Time works against long strangles but benefits short strangles through positive theta. Risk parameters create the starkest difference—short strangles risk unlimited losses for limited gains while long strangles risk limited losses for unlimited potential gains.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 31")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 37")

No Comments Yet.