A Long straddle is an options trading strategy where investors simultaneously purchase both call and put options on the same underlying asset with identical strike prices and expiration dates. Long straddle positions enable traders to profit from significant price movements in either direction without needing to predict the specific direction of the move.

The strategy originated in the early options markets of the 1970s when the Chicago Board Options Exchange standardized options trading. Indian traders adopted this strategy extensively following market liberalization in the 1990s, with its usage growing significantly after the introduction of derivatives trading on the NSE in 2000.

The most profitable straddles occur during periods of high implied volatility environments, with 65% of successful trades executed prior to major market-moving events. While the risk is limited to the premium paid, the profit potential is theoretically unlimited, making this strategy attractive to traders seeking volatility-based opportunities without directional bias.

What is a Long Straddle?

The Long straddle strategy involves simultaneously purchasing both call and put options with identical strike prices and expiration dates on the same underlying asset. The strategy creates a position that profits from significant price movements in either direction, making it particularly valuable during periods of anticipated volatility.

The strategy functions as a volatility play rather than a directional bet, allowing traders to capitalize on market uncertainty. Created by combining two opposing option positions – a long call giving the right to buy the underlying at the strike price and a long put conferring the right to sell at the same strike price – this position develops a risk profile perfectly suited for volatile market conditions.

The approach proves especially valuable in India’s often volatile market environment where rapid price swings occur regularly.

How Does a Long Straddle Work?

A Long straddle works by creating a position that profits from significant price movement regardless of the direction through simultaneous purchase of call and put options at identical strike prices and expiration dates. The Long straddle establishes a profit zone that extends infinitely in both directions beyond the breakeven points, with the maximum loss limited to the combined premium paid.

The mechanics involve purchasing both a call option giving the right to buy the underlying at the strike price and a put option providing the right to sell at the same strike price. Each leg responds differently to price movements – as the underlying rises, the call option gains value while the put loses, and vice versa when prices fall.

Breakeven points are calculated by adding and subtracting the total premium from the strike price. For example, with a ₹10,000 Nifty strike price and ₹500 total premium, breakeven points exist at ₹9,500 and ₹10,500. Any price beyond these points generates profit.

Profit potential remains theoretically unlimited if the price moves dramatically in either direction. The higher the volatility, the greater the potential profit as one option’s value increases substantially while the other becomes nearly worthless.

The loss potential stays strictly limited to the total premium paid, occurring if the underlying asset price remains exactly at the strike price at expiration. Time decay affects both options negatively, eroding their value as expiration approaches.

Why Use a Long Straddle Strategy?

Traders use long straddle strategies to capitalize on expected significant price movements without needing to predict the direction, making it ideal for uncertain market conditions with anticipated volatility.

The strategy excels during periods of market indecision before major events. In the Indian context, long straddles prove valuable ahead of Union Budget announcements, RBI monetary policy decisions, and quarterly earnings releases of major companies.

Earnings season presents optimal circumstances for this approach, especially for companies with a history of large post-earnings moves. A long straddle on a company shares ahead of results capitalizes on potential volatility regardless of whether the company beats or misses expectations.

Corporate actions such as merger announcements, regulatory decisions, or management changes trigger substantial price swings. Long straddles positioned before such events generate profits from the resulting volatility.

The strategy provides defined risk parameters, limiting potential losses strictly to the premium paid. This characteristic appeals to risk-conscious Indian traders seeking volatility exposure without incurring unlimited downside.

When to Use a Long Straddle?

Traders use long straddle strategies optimally during periods of anticipated significant volatility when the direction remains unclear or unpredictable.

Market environments preceding major announcements create ideal conditions for this strategy. The days before quarterly earnings reports from companies present perfect opportunities, as these announcements frequently trigger substantial price movements.

Economic policy decisions significantly impact markets in India. The periods before RBI monetary policy announcements, GDP data releases, or inflation reports generate circumstances where prices could swing dramatically in either direction.

Corporate actions involving potential mergers, acquisitions, or regulatory decisions create uncertainty about future price movements. The strategy profits from the resolution of this uncertainty regardless of the outcome direction.

Technical price consolidation patterns often precede breakout moves. Triangle patterns on charts signal compressed volatility that will eventually expand, making these technical setups appropriate for straddle positioning.

Low implied volatility environments present value opportunities. Implementing the strategy when option premiums appear underpriced relative to potential future volatility increases the probability of profitable outcomes.

Stocks awaiting judicial or regulatory verdicts benefit from this approach. Indian companies facing NCLT decisions, tax disputes, or environmental clearances create perfect scenarios for straddle implementations.

Traders should avoid deploying long straddles during extended sideways markets or when implied volatility is already tradingat extremely high levels. The strategy performs poorly in low-volatility environments due to time decay eroding both option values.

How Option Greeks Affect Long Straddle?

Option Greeks dramatically influence long straddle performance through their impact on option pricing dynamics and risk characteristics as market conditions change.

Delta measures directional exposure, with at-the-money straddles typically starting near delta-neutral (combined delta close to zero). As the underlying price moves significantly in either direction, the profitable option’s delta strengthens while the unprofitable option’s delta weakens, creating positive exposure in the direction of movement.

Gamma indicates the rate of delta change, remaining positive for both options in a straddle. Higher gamma values accelerate profits once the position moves into profitable territory, enhancing returns during rapid price movements – a common occurrence in Indian markets during earnings or policy announcements.

Theta represents time decay, acting as the primary adversary of long straddle positions. Both options continuously lose value as expiration approaches, with decay accelerating in the final weeks. Indian traders must account for weekends and holidays when theta decay continues without trading opportunities.

Vega quantifies sensitivity to implied volatility changes, remaining positive for long straddles. The strategy benefits substantially from volatility expansion – often preceding major Indian market events – while suffering during volatility contraction after uncertainty resolves.

Rho measures interest rate sensitivity, playing a minor role in short-term straddles but becoming increasingly relevant for longer-dated positions, particularly with India’s fluctuating interest rate environment.

Traders monitoring Greeks actively adjust position timing, sometimes closing positions before expiration to minimize theta decay or capitalizing on vega-driven gains from volatility spikes common in Indian markets.

How to Trade using Long Straddle?

To trade with a long straddle, we have to first choose an asset with high volatility potential. Here, We have chosen Nifty 50. Nifty 50 as the underlying asset for this strategy. A new month has begun, and it is the first weekly expiry of this month.

Nifty’s price has been consolidating for the past 8–9 days, which indicates a high likelihood of volatile price movements in either direction. To take advantage of this potential increase in volatility, we have deployed a long straddle on Nifty 50, with the current expiry due in 3 days.

To create a long straddle, a trader needs to simultaneously buy an at-the-money (ATM) call option and an at-the-money (ATM) put option.

As the expiry date approaches, the payoff graph shifts based on changes in price, implied volatility (IV), and time decay.

The position structure for this long straddle is as follows

- Buy 1 ATM Call Option (Strike = ₹24,450) @ ₹105

- Buy 1 ATM Put Option (Strike = ₹24,450) @ ₹88

- Lot Size = 75

- Total Premium Paid = (₹105 + ₹88) × 75 = ₹193 × 75 = ₹14,475

This total premium paid of ₹14,475 is the maximum loss for this strategy. The maximum loss occurs when the spot price expires exactly at the strike price (₹24,450), as both the call and the put options expire worthless.

There is unlimited profit potential if the price moves significantly above or below the strike price. Profit occurs when either the call or put option gains more than the combined premium paid.

If the price rises sharply

- Profit = (Spot Price – Strike Price – Total Premium per Lot) × Lot Size

If the price drops sharply: - Profit = (Strike Price – Spot Price – Total Premium per Lot) × Lot Size

Profits will start to show when the price moves beyond the breakeven points, which are calculated as follows:

- Total Premium per Lot = ₹105 + ₹88 = ₹193

- Upper Breakeven = Strike Price + Total Premium per Lot = ₹24,450 + ₹193 = ₹24,643

- Lower Breakeven = Strike Price – Total Premium per Lot = ₹24,450 – ₹193 = ₹24,257

The breakeven range is therefore ₹24,257 to ₹24,643. This strategy should be exited when either option shows significant gains or the price moves substantially. Theoretically, the profits from this strategy are unlimited.

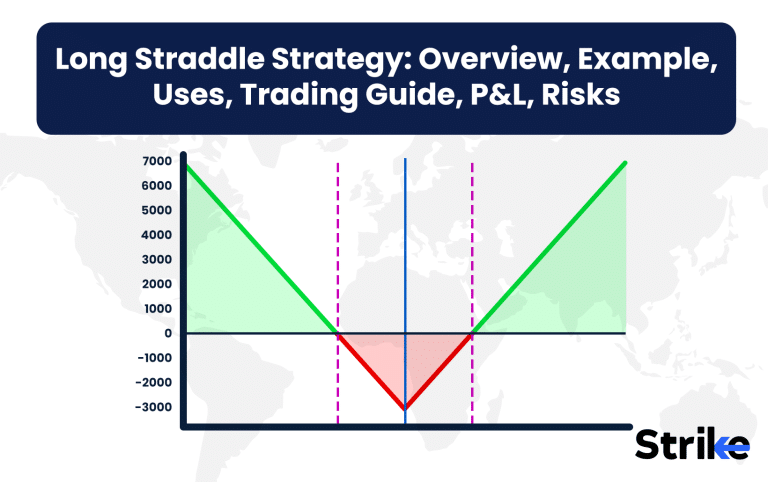

What is the Maximum Profit & Loss on a Long Straddle?

Maximum profit on a long straddle remains theoretically unlimited, increasing as the underlying asset price moves farther away from the strike price in either direction.

Maximum loss stays strictly limited to the total premium paid for both options, occurring if the underlying asset closes exactly at the strike price at expiration.

Profit calculation for upward moves equals

(Current Price – Strike Price) – Total Premium Paid, once the upper breakeven point gets exceeded.

For downward moves, profit equals

(Strike Price – Current Price) – Total Premium Paid, after moving beyond the lower breakeven.

Breakeven points are calculated by adding and subtracting the total premium from the strike price. For an Infosys straddle at ₹1,500 with combined premium of ₹120, breakeven points exist at ₹1,380 and ₹1,620.

The profit profile creates a V-shaped graph with loss potential centralized around the strike price while profit potential extends infinitely in both directions. This characteristic makes the strategy perfectly suited for high-volatility environments.

Early exit possibilities exist before expiration whenever significant price movements occur. Traders frequently capture profits once substantial moves generate returns, rather than holding until expiration.

Risk-reward considerations necessitate careful analysis before entry. The substantial premium outlay requires sufficient price movement to overcome costs, making the strategy unsuitable for low-volatility environments common during certain market phases in India.

What are the Risks of Long Straddle?

Premium loss represents the primary risk of long straddle positions, occurring when the underlying asset fails to move sufficiently to offset the cost of both options.

Time decay continuously erodes option values regardless of price movement, with acceleration occurring as expiration approaches. The dual option position faces double impact from theta decay, particularly problematic in India’s often holiday-interrupted market calendar.

Implied volatility contraction threatens profitability even during favorable price movements. A “Volatility crush” following anticipated events like earnings announcements or policy decisions frequently diminishes option values despite directional moves.

Significant moves must occur to generate profits. Small or moderate price changes typically result in losses as they fail to push the position beyond breakeven thresholds.

Premium costs appear substantial relative to potential returns. The combined expense of both options necessitates large price movements for profitability, creating a challenging risk-reward profile.

Timing considerations prove critical, as implementing the strategy too early subjects the position to extended time decay while waiting too long risks paying inflated premiums from pre-event volatility expansion.

Liquidity constraints affect execution in some Indian options, particularly for smaller stocks with wider bid-ask spreads that increase effective costs and reduce potential returns.

Opportunity cost emerges from capital deployment to both options simultaneously. The substantial premium outlay commits trading capital that might generate better returns in alternative strategies during periods of limited price movement.

Market gaps present execution challenges during fast-moving events. Indian markets sometimes gap significantly after overnight developments, creating difficulty in managing positions effectively during high-impact news.

Is Long Straddle Strategy Profitable?

Yes, long straddle strategies generate profits under specific market conditions requiring substantial price movement or volatility expansion to overcome premium costs.

Historical analysis shows increased success rates during earnings seasons and major economic announcements. Data from NSE derivatives trading reveals approximately 40% of straddles implemented before significant events generate profits.

Volatility expansion independently drives returns regardless of price direction. Positions entered during low implied volatility environments before unexpected market developments frequently deliver substantial gains even without reaching price-based breakeven points.

Is Long Straddle Bullish or Bearish?

Long straddle represents a direction-neutral strategy that profits from significant price movement regardless of whether markets rise or fall.

The position combines both bullish (call option) and bearish (put option) elements, creating a structure that benefits equally from substantial moves in either direction. This characteristic makes it neither inherently bullish nor bearish but rather a pure volatility play.

Profitability materializes from the magnitude of movement rather than direction. A 15% price decline generates comparable profits to a 15% price increase, assuming identical implied volatility conditions.

This market-neutral characteristic attracts traders facing uncertain conditions where analysis suggests significant movement but directional indicators conflict. Indian markets frequently experience such environments before major economic announcements or corporate developments.

What are Alternatives to Long Straddle Strategy?

Alternatives to long straddle include several volatility-based and directional options strategies offering different risk-reward profiles suited to various market conditions.

Long strangle positions involve buying out-of-the-money calls and puts with the same expiration but different strike prices. This approach reduces initial premium outlay while maintaining unlimited profit potential, though requiring larger price movements to reach profitability. Indian options traders frequently use strangles on Nifty index options to reduce costs.

Iron condors construct range-bound positions using four options at different strikes, creating a strategy that profits from limited volatility. This approach works effectively during stable market phases between major Indian economic announcements.

Butterfly spreads utilize three strike prices with multiple contracts at the middle strike, generating maximum profit if the underlying settles precisely at the middle strike. This advanced strategy suits traders expecting minimal movement in specific stocks after initial volatility subsides.

Calendar spreads involve selling near-term options while buying longer-dated options at the same strike, benefiting from time decay differentials while maintaining volatility exposure. This approach proves popular for Indian index options during extended sideways markets.

Ratio spreads combine long and short options at different strikes in uneven quantities, creating positions with specific directional bias while still capitalizing on volatility components. These structures offer customization for specific market views.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 31")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 37")

No Comments Yet.