Options Income Strategies are widely used by professional traders and the conservative investors to generate steady cash flow in the markets. Options Income Strategies generally deliver 1-3% monthly return (15-30% annualized) with 65-85% win rates on Nifty/Bank Nifty. They are best used by those investors who want disciplined, repeatable returns, or those investors who want options to be more professionally traded.

What is an Options Income Strategy?

An Options Income Strategy is a trading approach where the primary goal is to generate regular, consistent income by selling (writing) options and collecting the option premium, rather than speculating on large price moves. These approaches focus on time decay and high-probability trades where options expire worthless, rather than directional bets on price movements.

Guaranteed Profit Option Strategies

There are no guaranteed option strategies in the market, but there are strategies with the highest probability of winning. The strategies are mentioned below in the table.

| Strategy | Market View | Max Profit / Max Loss | Risk Level |

| Iron Condor | Sideways / Range-bound | Limited profit (net premium) / Limited loss | Medium |

| Covered Call | Neutral to mildly bullish | Limited profit (premium + capped upside) / High loss (stock downside) | Low–Medium |

| Cash-Secured Put | Neutral to bullish | Limited profit (premium) / High loss (stock falls sharply) | Medium |

| Credit Spread (Bull Put / Bear Call) | Mildly bullish / bearish | Limited profit / Limited loss | Medium |

| Iron Butterfly | Strongly sideways | Limited profit (higher than Iron Condor) / Limited loss | Medium–High |

These strategies do not offer guaranteed profits. They are high-probability income strategies where success depends on market conditions, risk management, and disciplined execution.

Most Successful Options Strategies

The most successful option strategies are mentioned below in the table

| Strategy | Market View | Max Profit / Max Loss | Risk Level |

| Covered Call | Neutral to mildly bullish | Limited profit / High loss (stock downside) | Low–Medium |

| Cash-Secured Put | Neutral to bullish | Limited profit / High loss | Medium |

| Iron Condor | Sideways | Limited profit / Limited loss | Medium |

| Credit Spread | Mildly bullish / bearish | Limited profit / Limited loss | Medium |

| Calendar Spread | Sideways to mildly directional | Limited profit / Limited loss | Medium |

These strategies are considered successful because they focus on consistency, probability, and controlled risk rather than chasing large one-time profits.

Low / Zero Risk Option Strategies (Capital & Strategy Risk Controlled)

Low / zero risk option strategies are mentioned below in the table.

| Strategy | Market View | Max Profit / Max Loss | Risk Level |

| Protective Put | Bullish (with protection) | Unlimited profit / Limited loss | Low |

| Protective Collar | Neutral to mildly bullish | Limited profit / Limited loss | Low |

| Iron Condor (Hedged) | Sideways | Limited profit / Limited loss | Low–Medium |

| Credit Spread | Mild directional | Limited profit / Limited loss | Medium |

| ZEBRA Strategy | Directional | Stock-like profit / Limited loss | Low–Medium |

These strategies are called low or controlled risk because they limit downside losses, not because profits are guaranteed. Proper position sizing and discipline are still essential.

High Probability Option Strategies

The high probability option strategies are mentioned below in the table.

| Strategy | Market View | Max Profit / Max Loss | Risk Level |

| Iron Condor | Sideways | Limited profit / Limited loss | Medium |

| Iron Butterfly | Strongly sideways | Limited profit (higher) / Limited loss | Medium–High |

| Credit Spread | Mild trend | Limited profit / Limited loss | Medium |

| Covered Call | Neutral | Limited profit / High loss | Low–Medium |

| Cash-Secured Put | Neutral to bullish | Limited profit / High loss | Medium |

These strategies have a higher chance of success because they align with time decay and market probabilities, but disciplined risk management is essential to protect capital.

Most Profitable Options Strategies

Most profitable options strategies are mentioned below in the table.

| Strategy | Market View | Max Profit / Max Loss | Risk Level |

| Long Call / Put | Strong directional | Unlimited profit / Limited loss | High |

| Short Straddle | Strongly sideways | High limited profit / Unlimited loss | Very High |

| Ratio Spread | Mild directional | High profit potential / Unlimited loss | Very High |

| Deep OTM Buying | Breakout / Event | Multi-bagger profit / 100% loss | High |

| ZEBRA Strategy | Directional | Stock-like profit / Limited loss | Medium |

These strategies can generate very high returns, but they also involve higher risk and skill. They are best used with strict risk control, experience, and proper position sizing.

Cash Flow Options Strategies

Cash flow options strategies are mentioned below in the table.

| Strategy | Market View | Max Profit / Max Loss | Risk Level |

| Covered Call | Neutral | Regular income / Stock downside | Low–Medium |

| Cash-Secured Put | Neutral to bullish | Regular income / Stock downside | Medium |

| Iron Condor | Sideways | Regular income / Limited loss | Medium |

| Credit Spread | Mild trend | Regular income / Limited loss | Medium |

| Option Income ETFs | Neutral | Steady income / Market risk | Low |

These strategies focus on generating steady and repeatable income, making them suitable for traders who prioritize cash flow, consistency, and risk control over large one-time profits.

What are the Common Option Income Strategies?

Common option income strategies primarily involve selling options to collect premiums, leveraging theta decay for consistent cash flow in neutral or range-bound markets. Some of the most common Option income strategies are mentioned below.

1. Iron Condor Strategy

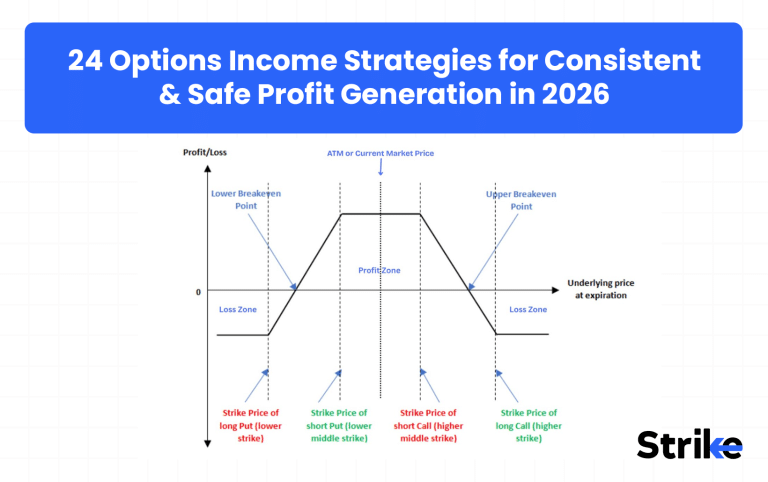

The Iron Condor is a neutral options strategy which gives profits during low volatility and range-bound market conditions. Iron Condor Strategy involves selling of two out-of-the-money (OTM) credit spreads, which includes a bull put spread below the current price and a bear call spread above, collecting net premium upfront while defining maximum risk.

Here is how you can create an Iron Condor Strategy

Identifying Market Condition: Identify the range-bound or sideways market preferably with low to falling volatility.

Strike selection: Sell out-of-the-money (OTM) Call option near resistance and out-of-the-money (OTM) put option near support creating a range. Buy further out-of-the-money (OTM) call and put options as a hedge. It is important to keep equal distance between short and long strikes.

Trade Execution: Execute all the four legs of the strategy at once to avoid price mismatch and execution risk.

Risk Management: Exit the trade once the market breaks the selected range decisively. Avoid trading iron condors during major events, as these events increase the volatility.

| Iron Condor Strategy | |

| Market Direction | Sideways |

| Volatility (IV) | High |

| Risk Profile | Defined |

| Capital Requirement | Medium |

| Complexity | Intermediate |

Iron Condor is one of the most popular weekly income strategies due to its defined risk and high probability setup.

2. Covered Call Strategy

The Covered Call Strategy is a conservative option income strategy where an investor holds the stock and simultaneously sells the call option of the same stock. This helps traders and investors to earn regular premium income while holding the stock, especially in sideways to slightly bullish markets.

You can create this strategy through 5 simple steps

Identifying Market Condition: Identify a sideways to slightly bullish market where stock is expected to stay stable or rise gradually.

Stock Selection: Select a fundamentally strong and liquid stock that you can comfortably hold short to medium term. High Liquidity provides better premium and smooth execution.

Strike Selection: Sell out-of-the-money (OTM) call option above the current market price, typically near resistance which allows some upside participation but still earning some decent premium.

Trade Execution: Buy or hold the stock and sell the call option simultaneously to avoid price mismatch. The premium is credited upfront and starts benefiting from time decay (theta).

Covered calls are widely used by investors to generate passive income from existing stock holdings.

Risk Management: If the stock moves above the strike price, be prepared to deliver the stock at the strike price, accepting capped upside. If the stock falls sharply, consider exiting the position or rolling the call to manage downside risk.

| Covered Call Strategy | |

| Market Direction | Mild Bullish |

| Volatility (IV) | Low–Neutral |

| Risk Profile | Stock Risk |

| Capital Requirement | High |

| Complexity | Beginner |

3. Cash-Secured Put Strategy

Cash-Secured Put Strategy is a conservative option income strategy which involves selling of a put option while keeping enough cash to buy the stock if it falls. This strategy is mainly used by investors who want to buy good quality stocks at lower prices while earning the premium.

Identifying Market Condition: Identify and look for a sideways to mildly bullish market with stable volatility. Try to avoid weak or highly volatile stocks.

Stock Selection: Select a fundamentally strong and liquid stock that you could hold if it falls.

Strike Selection: Select an out-of-the-money (OTM) put option near a strong support level to balance premium and safety.

Trade Execution: Sell out-of-the-money (OTM) put option to collect the premium while keeping enough cash to buy the stocks if they fall.

Risk Management: If the stock falls sharply, be prepared to buy the stock or exit the position early to limit losses.

Cash-secured puts are often used as the first step of the Wheel Strategy and are ideal for investors who want to generate income while accumulating stocks at lower prices.

| Wheel Option Strategy | |

| Market Direction | Mild Bullish |

| Volatility (IV) | Neutral |

| Risk Profile | Stock Risk |

| Capital Requirement | High |

| Complexity | Intermediate |

4. Wheel Option Strategy

The Wheel Option Strategy is a conservative and symmetric option strategy which cycles between cash-secured put and covered calls on the same underlying to generate premium income rapidly either without owning the stock or while holding it.

Let’s understand how to trade Wheel Option Strategy in four steps.

Market condition and stock selection: Identify the sideways market with stable volatility, and select fundamentally strong and liquid stock that you are comfortable owning even if the price falls. In this strategy, liquidity is important for smooth execution.

Sell Cash- Secured Put Option: Sell out-of -the-money put option of selected stock while keeping enough cash to buy the stock if price of the stock falls.

- If the price of stock stays above strike price, collect the premium after expiry and repeat the process.

- If the price of stock drops near the put option strike, buy the stock at the strike price

Sell Covered Call (After Assignment): Once you own the stock, follow the covered call strategy and sell out-of -the-money call options to earn a premium.

- If the price of the stock stays below the strike price, collect the premium after expiry and repeat the process.

- If the price of stock reaches the strike price, sell the stock at strike price with profit.

Repeat the Cycle (The Wheel): After the stock is sold, go back to selling puts again, continuing the cycle.

| Cash-Secured Put Strategy | |

| Market Direction | Bullish |

| Volatility (IV) | Neutral |

| Risk Profile | Defined (Cash Backed) |

| Capital Requirement | High |

| Complexity | Beginner |

The Wheel Strategy is ideal for traders who want steady income, defined rules, and discipline-based execution rather than fast trading.

5. Selling Call Options Strategy

Selling Call option strategy is an option income strategy, where a trader sells the out-of-the-money call option expecting stock or index to remain below selected strike price until expiry. This strategy works best in sideways to bearish markets or near strong resistance levels. Since selling naked call options is risky, it is important to buy a hedge to manage the risk.

You can trade Selling Call Options Strategy by following five simple steps.

Market condition and stock selection: Select fundamentally strong and highly liquid stocks which are under sideways to bearish trend or trading near important resistance zones.

Strike Selection: Sell out-of-the-money call option above the resistance zone, where the probability of the price staying below that level is high.

Trade Execution: Execute the trade and collect premium upfront. Make sure your position is covered with hedges.

Risk management: Once the price moves above the selected OTM strike, hedge the positions or exit the trade to control the loss.

| Selling Call Options (Naked) | |

| Market Direction | Bearish |

| Volatility (IV) | High |

| Risk Profile | Undefined |

| Capital Requirement | High |

| Complexity | Advanced |

Selling calls is widely used for income generation and hedging long stock positions, but strict risk management is essential.

6. Selling Put Options Strategy

Selling Put option strategy is an option income strategy, where a trader sells the out-of-the-money put option expecting stock or index to remain above selected strike price until expiry. This strategy works best in sideways to bullish markets or near strong support levels. Since selling naked put options is risky, it is important to buy a hedge to manage the risk.

You can trade Selling Put Options Strategy by following five simple steps.

Market condition and stock selection: Select fundamentally strong and highly liquid stocks which are under sideways to bullish trend or trading near important support zones.

Strike Selection: Sell out-of-the-money put options above the support zone, where the probability of the price staying above that level is high.

Trade Execution: Execute the trade and collect premium upfront. Make sure your position is covered with hedges.

Risk management: Once the price moves below the selected OTM strike, hedge the positions or exit the trade to control the loss.

| Selling Put Options (Naked) | |

| Market Direction | Bullish |

| Volatility (IV) | High |

| Risk Profile | Undefined |

| Capital Requirement | High |

| Complexity | Advanced |

Selling puts is often used as a stock acquisition strategy—you either earn income or buy the stock at a discounted price.

7. Credit Spreads Strategy

Credit Spreads Strategy is a defined-risk options income strategy where a trader earns premium upfront by selling near-to-the-money option and buying a further out-of-the-money option of the same type (Call or Put) and same expiry. This strategy works best in sideways to mildly trending markets.

You can trade this strategy by following four simple steps

Identify the market condition: Identify a sideways to slightly bullish or slightly bearish market

Select the spread type: Depending upon the direction of the market, credit spread can be of two types.

- Bull Put Spread, used when market is sideways to bullish

- Bear Call Spread, used when market is sideways to bearish

Strike Selection: Sell out-of-the-money option and buy far out-of-the-money option for hedging and keep reasonable distance between strikes to balance risk to reward.

Execution: Execute both the legs together to receive net credit and avoid execution risk.

Risk management: Exit the trade once price reaches or breaks adversely the sold strike level. Avoid trading during major events.

| Credit Spreads Strategy | |

| Market Direction | Bullish / Bearish |

| Volatility (IV) | High |

| Risk Profile | Defined |

| Capital Requirement | Low |

| Complexity | Intermediate |

Credit spreads are ideal for traders who want consistent income with controlled risk, making them a popular choice for weekly option selling.

8. Short Straddle Strategy

The short straddle Strategy is a neutral option income strategy where a trader expects a market to stay near the same price level until expiry with very low volatility and minimal price movement. This strategy involves selling of at-the-money call and put option of same strike to collect maximum premium upfront.

Market condition and stock selection: Select a highly liquid stock or index which is under strong range bound condition with low to falling volatility.

Strike Selection: Sell at-the-money (ATM) call and put option of same strike and same expiry to collect the maximum premium.

Trade Execution: Execute both the leg simultaneously to avoid price mismatch and ensure proper premium capture

Risk Management: Exit the trade immediately once price sharply moves in either direction. Traders also reduce risk by adding predefined stoploss or converting the position into Iron Fly.

| Short Straddle Strategy | |

| Market Direction | Sideways |

| Volatility (IV) | Very High |

| Risk Profile | Undefined |

| Capital Requirement | Very High |

| Complexity | Advanced |

Short straddles are high-risk, high-reward strategies and should be used only by experienced traders with strong risk management.

9. Short Strangle Strategy

The short Strangle is a neutral option income strategy where a trader expects a low volatility and range bound price movement. This strategy involves selling out-of-the-money call option near resistance and out-of-the-money put option near support of same expiry expecting the market to expire within this range.

Market condition and stock selection: Select a highly liquid stock or index which is under sideways consolidation with low to falling volatility.

Strike Selection: Sell out-of-the-money (OTM) call option, typically near resistance and out-of-the-money (OTM) put option, typically near support of the same expiry.

Trade Execution: Execute both the leg simultaneously to avoid price mismatch and ensure proper premium capture

Risk Management: Exit the trade immediately once price sharply breaks beyond either strike. Traders also reduce risk by converting the position into Iron Condor.

Short strangles are suitable for experienced traders only due to unlimited risk, and are often hedged or adjusted into Iron Condors or Iron Fly if price starts trending.

| Short Strangle Strategy | |

| Market Direction | Sideways |

| Volatility (IV) | Very High |

| Risk Profile | Undefined |

| Capital Requirement | Very High |

| Complexity | Advanced |

Short strangles provide wider safety zones than straddles but still demand strict monitoring and volatility awareness.

10. Butterfly Options Strategy

The Butterfly Options Strategy is a low-risk, limited reward strategy used by traders in expectation of underlying stock or index to remain near a specific price level. This strategy involves the combination of three strike prices of the same expiry. This strategy benefits from low-volatility and range bound markets.

Identify Market Condition: Identify sideways or low-volatility markets where you expect the price to stay near a particular level till expiry.

Choose Strike Prices: To create a butterfly using a call option, buy one in-the-money (ITM) call option, sell two at-the-money (ATM) call options, and buy one out-the-money (OTM) call option. To create a butterfly using the put option, follow the same procedure using the put option. Note that all options must have the same expiry.

Execute the Trade: Execute all four legs together to create a net debit position and avoid price mismatch.

Risk Management & Exit: Our maximum loss is capped to the net premium paid. Exit early if price moves sharply away from the middle strike or target is achieved before expiry.

| Butterfly Options Strategy | |

| Market Direction | Sideways |

| Volatility (IV) | Low–Neutral |

| Risk Profile | Defined |

| Capital Requirement | Low |

| Complexity | Intermediate |

A Put Butterfly follows the same structure using put options and is suitable when you expect price stability near a specific support level.

11. Iron Butterfly Strategy

The Iron Butterfly Strategy is also a range bound market strategy with limited risk and limited reward where traders expect the underlying stock or index to remain near a specific price level till expiry. This strategy is nothing but a straddle with out-of-the-money (OTM) options as hedges.

Identify Market Condition: Identify sideways or low-volatility markets where you expect the price to stay near a particular level till expiry.

Select Strike Prices: Sell one at-the-money (ATM) call and put options and protect this naked selling by buying one out-the-money (OTM) call option and out-the-money (OTM) put options as hedges. All these strikes must have the same expiry.

Execute the Trade: Execute all four legs together to create a net debit position and avoid price mismatch.

Risk Management & Exit: Maximum loss is limited and will only occur when price moves beyond either hedge strike. You can also close your positions early once 70-80% of maximum profit is achieved.

| Iron Butterfly Strategy | |

| Market Direction | Sideways |

| Volatility (IV) | High |

| Risk Profile | Defined |

| Capital Requirement | Medium |

| Complexity | Intermediate |

Iron Butterfly is a lower-cost alternative to a short straddle, offering protection against sharp moves while still generating steady income.

12. Calendar Spread Strategy

The Calendar Spread Strategy, also known as Time Spread is a neutral to slightly directional option strategy that takes advantage of time decay and volatility difference between different expiries of the same strike. It involves buying a long-term option and selling a near-term option of the same strike. This strategy performs best when the near-term sold option expires near the chosen strike.

Identify Market Condition: Identify and select a sideways to slightly directional market with low to moderate volatility, specially when nearterm volatility is higher than far-term volatility.

Select the Strike Price: Select the same strike, mainly at-the-money (ATM) or slightly out-the-money (OTM), where you expect the price to stay until short-term expiry.

Choose Expiries: Select two different expiries of the same strike, one near-term and one long-term expiry. Buy the far-term expiry option and sell the near term expiry option.

Choose Strategy Type: Create Call Calendar strategy if the market bias is slightly bullish or create Put Calendar strategy if the market bias is slightly bearish.

Execute the Trade: Execute both legs together to create a net debit position.

Risk Management & Exit: Exit after the short-term option expires or close position early if price moves sharply away from the strike. Calendar spreads benefit from faster time decay of the short-term option and often gain when implied volatility rises in the far-term option.

| Calendar Spread Strategy | |

| Market Direction | Neutral |

| Volatility (IV) | Low |

| Risk Profile | Defined |

| Capital Requirement | Low |

| Complexity | Intermediate |

Calendar spreads benefit from time decay (theta) and often perform better when implied volatility rises in the longer-term option.

13. Diagonal Spread Strategy

The Diagonal Spread Strategy is a flexible and limited risk strategy which involves a combination of both, a calendar spread and a vertical spread. This involves buying a long-term option and selling a short-term option of different strike price. This strategy is used when traders have a mild directional bias.

Identify Market Bias: Decide your market view, either mildly bullish or mildly bearish, but not strongly directional.

Select Option Type: Create Call diagonal spread for a mildly bullish view or create a Put diagonal spread for mildly bearish view.

Choose Expiries: Select two different expiries, one near-term and one long-term expiry. Buy the far-term expiry option and sell the near term expiry option.

Choose Strike Prices

- For bullish diagonal spread, buy lower strike call (far-term expiry) and sell higher strike call (near-term expiry).

- For bearish diagonal spread, buy higher strike put (far-term expiry) and sell lower strike put (near-term expiry).

Execute the Trade: Execute both legs together for net debit and to avoid price mismatch.

Risk Management & Exit: Adjust or close if the price sharply moves against the bias or exit after near-term option expiry.

| Diagonal Spread Strategy | |

| Market Direction | Mild Trend |

| Volatility (IV) | Low–Medium |

| Risk Profile | Defined |

| Capital Requirement | Medium |

| Complexity | Intermediate |

Diagonal spreads offer more flexibility than calendar spreads and are ideal when you expect slow, controlled price movement rather than a sharp trend.

14. Ratio Spread Strategy

Radio Spread Strategy is an option strategy where the number of sold options are greater than the number of bought options at different strike pieces of the same expiry. Traders create this strategy with expectation of limited directional movement. This strategy can be created with low margin, but it curries unlimited risk on one side if the market moves sharply.

Identify Market View: Select the market with a moderate trending view, not a strong trending view.

Choose Strategy Type: Create Call Ratio Spread for mildly bullish view and Put Ratio Spread for mildly bearish view.

Select Strike Prices: Buy one in-the-money (ITM) or at-the-money (ATM) call or put option depending on strategy type and sell two out-the-money (OTM) call or put option depending on type of strategy. Make sure that the strikes are of the same expiration.

Execute the Trade: Execute all legs together. The trade can be net debit, net credit, or zero-cost, depending on strikes chosen

Risk Management & Exit: As the risk is unlimited beyond the breakeven point on the sold side, it is important to exit or hedge once price moves strongly beyond the sold side. It is advised to close the trade to avoid gamma risk.

| Ratio Spread Strategy | |

| Market Direction | Directional |

| Volatility (IV) | Medium |

| Risk Profile | Undefined |

| Capital Requirement | Medium |

| Complexity | Advanced |

Ratio spreads are advanced strategies and should be used only with strict risk management. Many professional traders convert ratio spreads into butterfly or hedge them dynamically if price moves unexpectedly.

15. Poor Man’s Covered Call Strategy

The Poor Man’s Covered Call (PMCC) is a capital-efficient option strategy alternative to the traditional covered call strategy. This strategy involves buying a deep in-the-money (ITM) long-term call option (LEAPS) instead of buying the stock, and selling a short-term out-the-money (OTM) call option against it. This strategy generates regular income with much lower capital requirement while maintaining limited risk.

Identify Market View: Identify and select a bullish or sideways-to-bullish stock or index with stable price action and good liquidity.

Buy a Long-Term ITM Call (LEAPS): Select deep in-the-money call option with high delta (0.70–0.90) of far expiry which will act as a stock substitute.

Sell a Short-Term OTM Call: Select a near-term expiry out-the-money (OTM) strike which will generate regular premium income.

Execute the Trade: Enter both legs together for a net debit and avoid price mismatch.

Risk Management & Exit: If price rises sharply, roll the sold call higher or exit if the long term bullish view changes.

| Poor Man’s Covered Call (PMCC) | |

| Market Direction | Bullish |

| Volatility (IV) | Low–Medium |

| Risk Profile | Defined |

| Capital Requirement | Medium |

| Complexity | Intermediate |

PMCC works best in steady uptrends and avoids the heavy capital required to buy shares outright.

16. LEAP Options Strategy

The LEAP Options Strategy involves buying Long-Term Equity Anticipation Securities (LEAPS) options with long expiries with lower capital investment.The traders and investors with a strong directional view mostly adopt this strategy to take advantage of price movement in the long term.

Steps to Trade a LEAP Options Strategy

Identify Long-Term View: Select a fundamentally strong stock or index with a clear long-term bullish or bearish outlook.

Choose Option Type and strike: Buy LEAP ITM or ATM Call option for long-term bullish view or buy LEAP ITM or ATM Put for long-term bearish or hedging view. All these strikes must be of long term expiry to allow the thesis time to play out.

Execute the Trade: Enter the trade for a net debit (premium paid upfront).

Risk Management & Exit: Cut the positions if the long-term view is changed, otherwise the maximum loss is limited to the premium paid.

| LEAP Options Strategy | |

| Market Direction | Bullish |

| Volatility (IV) | Low |

| Risk Profile | Defined |

| Capital Requirement | High |

| Complexity | Beginner |

LEAP strategies are ideal for positional traders and investors who want leverage with controlled risk and patience.

17. Deep OTM Options Strategy

The Deep OTM (Out-of-the-Money) options strategy involves buying far OTM (Out-of-the-Money) options at a cheap price. These options are cheap because the probability of price crossing this OTM is low. Traders use this strategy to capture a sharp unexpected move with small capital, but carries high probability of loss.

Identify High-Momentum or Event-Based Setup: Identify the market situations like breakouts, trend reversals, results, budget, policy announcements, or global cues where a big move is expected.

Choose Option Type: Buy a deep OTM call option if a strong upside move is expected or buy a deep OTM put option if a strong downside move is expected.

Choose Expiry: Choose near-term expiry for fast moves which gives high reward but with high risk, or slightly longer expiry if the move is expected to take time.

Execute the Trade: Execute the trade with small capital and accept the possibility of full premium loss.

Risk Management & Exit: Avoid holding the trade till expiry unless the move is clearly in favor and keep booking profits aggressively on spikes. Here the maximum loss is 100% of premium paid.

| Deep OTM Options Strategy | |

| Market Direction | Neutral |

| Volatility (IV) | High |

| Risk Profile | Undefined |

| Capital Requirement | Low |

| Complexity | Advanced |

Deep OTM option buying is more like a probability-based bet, not a consistent income strategy. Position sizing and timing are critical.

18. ZEBRA Options Strategy

The ZEBRA Options Strategy also known as Zero Extrinsic Back Ratio Spread is a stock replacement strategy which mimics the stock movement with minimal time decay. This strategy is created by buying two ITM options and selling one ATM option of the same expiry rounding up a net delta close to one. Delta 1 makes the position behave like owning the stock, but with less capital.

Identify Directional View: Identify the market and decide the clear view on markets such as bullish or bearish.

Choose Option Type: Create Call ZEBRA for bullish market view or create Put ZEBRA for bearish market view.

Select Expiry and Strike Prices: Choose a medium to long-term expiry to reduce frequent adjustments and buy 2 ITM options with high delta, low extrinsic value and sell 1 ATM option. Ensure the net debit is close to intrinsic value, minimizing time decay.

Execute the Trade: Enter all legs together for a net debit.

Risk Management & Exit: Exit if directional view of strategy changes, otherwise this strategy can be held longer than normal option strategy. The maximum loss is limited to net debit paid.

| ZEBRA Options Strategy | |

| Market Direction | Bullish |

| Volatility (IV) | Low |

| Risk Profile | Defined |

| Capital Requirement | Medium |

| Complexity | Advanced |

ZEBRA is ideal for traders who want stock-like exposure without buying shares and want to avoid

19. Pocket Options Strategy

Pocket Options Strategy is a short-term momentum based options buying style of strategy, where traders attempt to trade small-to-medium price changes in quick options by buying near-the-money options. The concept is to get into trades when the market breaks an important support or resistance or into a low-resistance pocket or or strong momentum candle, and exit quickly with controlled risk.

Identify Strong Momentum Setup: Look for a short term momentum after a breakouts, range expansion, trend continuation, or high-volume candles on the underlying stock or index.

Select Strike Price: Choose ATM or slightly ITM options for better liquidity and faster premium movement. Buy call in case of bullish momentum or buy put option in case of bearish momentum.

Select Expiry: Use near term expiry to benefit from quick price movement.

Execute the Trade: Enter immediately after confirmation of momentum such as breakout or retest of any key level.

Risk Management & Exit: Exit quickly if momentum fails and avoid holding if price goes sideways. Put strict stoploss on premium or underlying level.

| Pocket Options Strategy | |

| Market Direction | Neutral |

| Volatility (IV) | Medium |

| Risk Profile | Defined |

| Capital Requirement | Low |

| Complexity | Advanced |

Pocket options trading is not an income strategy. It is a high-speed, execution-driven approach best suited for intraday or very short-term traders.

20. Short Box Options Strategy

Short Box Options Strategy is a non directional arbitrage based strategy, which enables the trader to borrow in the options market. The trader takes a credit upfront and a cash payment at expiry by combining a bull call spread and bear put spread of the same strikes and expiry. The difference between the two is the interest cost, thus, an interest-rate arbitrage approach instead of a market-directional strategy.

Identify Arbitrage Opportunity: Look for pricing inefficiencies where the options combination gives higher credit than fair value. This is very rare to find and usually available only to advanced traders or institutions.

Select Strike Prices and Expiry: Choose two strike prices, Lower Strike (K1) and Higher Strike (K2) of the same expiry.

Construct the Strategy: Sell ITM Call (K1), buy OTM Call (K2), Sell ITM Put (K2), and buy OTM Put (K1), creating a short box.

Execute the Trade: Execute all four legs together to receive a net credit.

Risk Management & Exit: Directional risk is neutralized, whereas real-world risks include execution cost, liquidity, margin, and early exercise mostly for American options.

| Short Box Options Strategy | |

| Market Direction | Neutral |

| Volatility (IV) | Low |

| Risk Profile | Defined |

| Capital Requirement | Very High |

| Complexity | Advanced |

In highly efficient markets, Short Box opportunities are extremely rare and mostly used by institutions and professional arbitrage desks. Retail traders usually avoid it due to low returns and high capital requirements.

21. Batman Options Strategy

Batman options Strategy is a non- directional, income based options strategy benefiting when underlying stays in a broad range or the underlying moves in a moderate direction, either way. It is a modified Iron Condor having additional short options close to the money that provides the payoff structure resembling the mask of Batman.

Steps to Trade a Batman Options Strategy

Identify Market Condition: Identify and select a sideways or mildly volatile market with low probability of big breakouts.

Choose the Expiry: Prefer near-term expiry (weekly or monthly) to maximize theta decay same for all legs.

Select Strike Structure: Buy far OTM Call (upper hedge), sell OTM Call, and sell near ATM Call. Repeat the same structure on the put side. This creates an extra premium collection near the center with protected wings.

Execute the Trade: Execute all legs together to receive a net credit.

Risk Management & Exit: Risk is limited due to long OTM hedges, you can exit or adjust the strikes if price moves strongly beyond the expected range. You can also book your profits early when 70-80% of the target is achieved to avoid late expiry risk.

| Batman Options Strategy | |

| Market Direction | Sideways |

| Volatility (IV) | High |

| Risk Profile | Defined |

| Capital Requirement | Medium |

| Complexity | Advanced |

The Batman strategy is suitable for advanced traders due to multiple legs and adjustment complexity. It offers higher income than Iron Condor but with a narrower comfort zone.

22. Protective Collar Strategy

The protective collar strategy is a risk-management options strategy used by investors to limit their downside risk of their holdings. This strategy involves buying a protective put and selling a covered call on the same stock with the same expiry. This strategy is ideal when you want to lock a price range for your holdings.

Steps to Trade a Protective Collar Strategy

Own the Stock: Buy a fundamentally strong stock that you want to hold and protect, especially during uncertain or volatile market conditions.

Adding a protection: Buy an OTM put below the CMP to protect the downside risk and sell an OTM covered call to receive a premium to fully offset the cost of the put. Ensure both the put and call have the same expiry.

Execute the Trade: Execute all the positions together to risk a price mismatch. This often results in a low-cost or zero-cost collar.

Risk Management & Exit: Hold till expiry or exit early if the view of the market changes. Roll the call or put to adjust protection or upside

| Protective Collar Strategy | |

| Market Direction | Neutral |

| Volatility (IV) | Low |

| Risk Profile | Defined |

| Capital Requirement | High |

| Complexity | Beginner |

The Protective Collar is widely used by long-term investors and portfolio managers to protect gains without exiting the stock position.

23. Married Puts Strategy

The Married Puts Strategy is a bullish options strategy that is protective in nature, where an investor buys a stock and at the same time sells a put option of the same stock with the same quantity and expiry. The put option here acts as insurance, which offsets the downside risk to the investor but does not limit the potential gains.

Steps to Trade a Married Puts Strategy

Buy the Stock: Purchase shares of a stock with a long term bullish expectation.

Buy a Protective Put: Buy an ATM or slightly OTM Put with expiry which covers the risk period you want protection from

Execute Together: Enter the stock and put option simultaneously to lock in protection from the start.

Risk Management & Exit: Maximum loss in this strategy is limited (stock price − put strike + premium paid) due to protective put. You can hold this trade till expiry or sell the put early if risk reduces. Exit entire positions once long term view changes.

| Married Puts Strategy | |

| Market Direction | Bullish |

| Volatility (IV) | Low |

| Risk Profile | Defined |

| Capital Requirement | High |

| Complexity | Beginner |

Married Puts are ideal for investors who want to participate in upside while sleeping peacefully during volatile phases.

24. Option Income ETF Strategy

The Option Income ETF Strategy is an investment in Exchange-Traded Funds (ETFs) which sell options (typically, covered calls or cash-secured puts) systematically to produce a steady stream of income. These ETFs aim to offer consistent cash flow through option premiums rather than high capital appreciation, making them suitable for income-focused and conservative investors.

Select an Option Income ETF: Choose ETFs that follow option-selling strategies such as, Covered Call ETFs (sell calls on index or stocks), Put-Write ETFs (sell cash-secured puts), Buy-Write ETFs (own index + sell calls)

Invest Like a Normal ETF: Buy these ETFs just like normal stocks through your trading account, without having any prior knowledge.

Income Generation: These ETFs will give you income from the collected option premium or partial dividend distribution.

Risk & Return Profile: The risk is minimal as upside is capped due to call selling and downside is partially protected. These ETFs generate more stability, however they underperform pure ETF in the bull market.

| Option Income ETF Strategy | |

| Market Direction | Neutral |

| Volatility (IV) | Low |

| Risk Profile | Low Risk |

| Capital Requirement | Low |

| Complexity | Beginner |

Option Income ETFs trade simplicity for flexibility; you earn steady income, but you give up control over strike selection, timing, and adjustments.

How to Choose the Best Option Income Strategy?

Choosing the best option income strategy involves evaluating your market direction, volatility, risk tolerance, capital availability, monitoring timing and goals like monthly premium targets

- Market Direction (Trend Bias): First identify whether the market is bullish, bearish, or sideways. Bullish views suit Cash-Secured Puts or Covered Calls, bearish views suit Bear Call Spreads, and sideways markets work best with Iron Condors or Calendar Spreads.

- Volatility (IV Level): Volatility decides option premium. High volatility favors option selling strategies, while low volatility is better for Calendar or Diagonal spreads. Prefer selling options when IV is high.

- Risk Comfort: Select a strategy based on acceptable loss. Defined-risk strategies like Credit Spreads and Iron Condors suit conservative traders, while Covered Calls and CSPs suit moderate risk profiles.

- Capital Availability: Limited capital works best with Credit Spreads or PMCC. Moderate capital allows Covered Calls and Iron Condors. Capital should always match risk.

- Time & Monitoring: Low monitoring suits Covered Calls and CSPs. Moderate monitoring suits Credit Spreads and Iron Condors. Advanced strategies need active management.

- Expiry Selection: Weekly expiries suit Credit Spreads and Iron Condors due to fast time decay. Monthly expiries are better for Covered Calls, CSPs, and Calendar Spreads.

The best option income strategy is the one that matches your market view, risk comfort, capital, and time availability, allowing you to earn consistent, repeatable premiums without stress.

What is the Best Option Income Strategy for Beginners?

The covered call is the best option income strategy for beginners due to its simplicity, low risk, and steady premium income on stocks you already own or plan to hold. This strategy generates 1-4% monthly returns in sideways or mildly bullish markets with 65-80% of winrate.

This strategy has limited risk—your downside is capped at the stock’s price movement minus the premium—making it safer than naked options while also teaching the basics of theta decay. If you’re still wondering What is Option Trading, it simply means buying and selling option contracts to potentially profit from price moves, time decay, or volatility. The other beginner-friendly option strategy is mentioned below in the table.

| Strategy Name | Market View | Risk Level | Why It’s Good for Beginners |

| Cash-Secured Put | Bullish / Neutral | Low | Earn premium and buy good stock at lower price if assigned |

| Bull Put Spread | Mildly Bullish | Low (Defined Risk) | Limited loss, low capital, clear risk–reward |

| Bear Call Spread | Mildly Bearish | Low (Defined Risk) | Safer way to earn income in falling or weak markets |

What is the Best Option Income Strategy for Advance Traders?

Iron Condor is the best income strategy for advanced traders due to its use in neutral market conditions. This strategy collects premium from four legend spread on highly liquid NSE Indices like NIFTY or Bank NIFTY. It provides a range of 3-8% monthly returns with set risk, suitable to those who have experience in Greeks and volatility management.

Other Option Income Strategies for Advance Traders are mentioned below.

| Strategy Name | Market View | Risk Level | Why It Suits Advanced Traders |

| Short Strangle | Sideways / Low Trend | High (Unlimited Risk) | High probability income, benefits from time decay and IV crush |

| Iron Condor (Wide) | Sideways | Moderate | Better risk–reward with wider ranges and adjustments |

| Iron Butterfly | Neutral (Pin Risk) | Moderate–High | High premium near ATM, needs precise entry & exit |

| Ratio Spread | Directional / Neutral | High (One-Sided Risk) | Low or zero cost setup with high reward potential |

| Calendar Spread (Active) | Neutral / Volatility Play | Moderate | Profits from time decay and volatility expansion |

| Diagonal Spread | Mild Directional | Moderate | Combines income with directional bias |

What is the Best Option Strategy for Regular Income?

Covered calls provide the best option strategy for generating regular income, offering consistent premiums from selling calls against owned stocks in stable or mildly bullish NSE markets like Nifty stocks.

Why Covered Calls for Steady Income? This strategy delivers monthly theta decay income (1-4% returns) with capped upside but limited downside risk offset by premiums, ideal for regular cash flow without high volatility exposure. It suits ongoing cycles: collect premium weekly/monthly, roll positions, and hold quality shares long-term.

What is the Best Option Strategy for Passive Income?

Cash-secured puts is considered to be the best option strategy for passive income because it generates consistency upfront premium with limited risk. You will sell puts, and hold a sufficient sum of cash to buy the stock once it falls, which removes leverage and margin stress.

When the option goes out of the money, you get a stable income in the form of the premium, when it declines, you purchase a quality stock at a discount. It is passively and repeatedly monitored, meaning it is suitable to generate income passively and on a long-term basis.

Which Options Income Strategy is the Safest?

Covered call is considered to be the safest option income strategy because it is backed by the underlying stock, which significantly reduces the risk of unlimited loss.

The maximum loss in this strategy is limited to downside risk of stock itself, while the option premium provides partial downside protection and regular income. This strategy works best in sideways to a slightly bullish market, suitable for conservative traders.

How Do Option Sellers Earn Money Every Month?

The option sellers earn money every month through theta decay, where sellers collect premium upfront that erodes over time if the option expires worthless. Option sellers typically target a range bound market to sell the options which expires after 20-45 days.

Option sellers can earn consistent profit with a high win rate (70–80%) through proper strike selection and risk-defined setups—this is the core idea behind Option Selling.

Is Options Income Sustainable in the Long Term?

Yes, options income is sustainable in the long term, but only when traded with proper risk management and realistic return expectations.

A disciplined option income trader typically targets 1-3% per month on their total capital, which makes around 12–30% annually. These returns are achievable by following a conservative option strategies without taking excessive risk. Most professional traders exit trades when they get 50% or 70% of the premium, minimizing risk on market volatility.

What is the Principle of Time(Theta) Decay in Income Trading?

The principle of time (Theta) decay in income trading says that the option premium decays with time even when the market is doing nothing. This principle works in favour of option sellers since every day the extrinsic value of the option decreases and enables one to generate income without huge fluctuations in price.

Income traders sell options (like covered calls, iron condors, or credit spreads) and benefit from this decay. The rate of theta decay increases during the last days before expiry, that is why short-term options are preferred. In case the price remains in range, the option will expire out of the money and the seller will retain the premium, time is actually the ultimate advantage in trading income.

How Do Income Strategies Differ from Other Options Strategies?

Income strategies are designed to earn regular, repeatable premiums, while other option strategies focus more on directional moves or big price swings. The difference is mainly in objective, risk profile, and trade management.

| Aspect | Income Strategies | Other Option Strategies |

| Goal | Regular income | Big directional profit |

| Market Type | Sideways / Mild trend | Strong trend / Breakout |

| Time Decay | Beneficial | Harmful |

| Risk | Usually defined | Often higher |

| Win Rate | Higher | Lower |

| Profit Size | Smaller, consistent | Larger but irregular |

Income strategy focuses on steady, repeatable profits using time decay, whereas other option strategies chase larger gains with less consistency.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 280")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 281")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 282")

: Overview, 10 Types of Indicators, Settings for Different Markets 284")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 286")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 290")

No Comments Yet.