Poor Man’s Covered Call represents a diagonal spread options strategy requiring less capital than traditional covered calls while maintaining similar profit potential. Poor Man’s Covered Call substitutes stock ownership with a deep in-the-money long-term call option, paired with selling short-term call options at higher strike prices. Emerging in the early 2000s, this strategy gained popularity among retail traders during the 2008 financial crisis when capital preservation became crucial.

Companies like Adani Enterprises and JSW Steel serve as excellent PMCC candidates due to their moderate volatility and strong uptrends. Traders typically achieve 2-3% monthly returns using this strategy in sideways markets.

What is a Poor Man’s Covered Call (PMCC)?

Poor Man’s Covered Call describes an options trading strategy that mimics a traditional covered call but requires significantly less capital investment. Poor Man’s Covered Call utilizes a diagonal spread consisting of buying a deep in-the-money, longer-term call option instead of purchasing the actual stock, then selling an out-of-the-money shorter-term call against it.

This strategy creates a synthetic position equivalent to owning shares while dramatically reducing capital requirements. Rather than purchasing 100 shares of stock at full price, traders buy a deeply in-the-money LEAPS call option (typically with 70%+ delta) that behaves similarly to stock ownership but costs substantially less.

Traders typically execute this strategy through monthly income cycles, repeatedly selling new short-term calls as previous ones expire or need adjustment.

How Does a Poor Man’s Covered Call Work?

Poor Man’s Covered Call operates by creating a diagonal spread that simulates owning stock and selling calls against it, but with much lower capital requirements. Poor Man’s Covered Call replaces direct stock ownership with a deep in-the-money long-term call option (often called LEAPS) while generating income by selling shorter-term out-of-the-money calls.

Execute this strategy through two key transactions. First, purchase a deep in-the-money call option with at least 6-12 months until expiration. Choose options with deltas exceeding 0.70 to closely mimic actual stock ownership. Second, sell a shorter-term call (typically 30-45 days until expiration) at a higher strike price than your long call.

The long call serves as your synthetic stock position. Deep ITM options move almost one-to-one with the underlying stock due to their high delta. This creates a position behaving similarly to owning actual shares but requiring only 20-40% of the capital.

The short call generates income through premium collection. Each time you sell a call against your long position, you collect a premium immediately. Ideally, these short calls expire worthless or get closed for profit before expiration.

Calculate your net debit (cost of long call minus premium received for short call) to determine your initial investment and break even points.

Why Use a Poor Man’s Covered Call Strategy?

Traders use a Poor Man’s Covered Call strategy primarily because it dramatically reduces capital requirements while providing similar returns to traditional covered calls.

The strategy enables access to expensive stocks with only 15-30% of the capital normally needed, opening participation to traders with smaller accounts. This capital efficiency proves particularly valuable, for Indian retail traders facing high-priced stocks like Asian Paints or Titan.

The strategy provides substantial downside protection compared to outright stock ownership. The maximum loss limits the initial debit paid (long call cost minus short call premium), typically representing 15-30% of the stock price. This defined risk profile protects traders from catastrophic losses during market corrections.

The strategy offers leveraged upside potential due to the options’ inherent leverage. The long call moves almost one-to-one with the stock (depending on delta) while requiring just a fraction of the investment, amplifying percentage returns.

PMCC maintains flexibility for adjustments throughout the position lifecycle. Traders roll short calls to capture additional premium or manage assignment risk. The position defends against moderate price declines through premium collection and allows adaptation to changing market conditions.

When to Use a Poor Man’s Covered Call?

Use a Poor Man’s Covered Call during moderately bullish market environments where stocks trade within defined ranges or show steady but limited upside momentum. Below is a similar situation.

The strategy performs optimally when you anticipate gradual price appreciation or sideways movement in the underlying asset, allowing you to benefit from time decay of the short calls while maintaining upside exposure through the long call.

Deploy PMCC positions when implied volatility sits at elevated levels for shorter-term options relative to longer-term options. This volatility skew enables selling expensive near-term options while buying relatively cheaper long-term options, creating favorable pricing dynamics.

Implement this strategy for stocks with moderate to high prices where traditional covered calls would require substantial capital. Companies like L&T, Bajaj Finance, or Dixon Technologies present ideal candidates in the Indian market due to their relatively stable price action and higher share prices.

Execute PMCCs after significant market corrections when stock prices have stabilized but remain below recent highs. This timing provides attractive entry points for the long call component while positioning for eventual recovery.

Apply PMCCs to stocks offering minimal or no dividends. The strategy performs better on growth-oriented securities where income comes primarily from price appreciation, since options holders receive no dividend payments, rather than distributions.

Consider this approach for blue-chip stocks demonstrating lower historical volatility but reliable growth trajectories, creating predictable trading ranges for optimal premium collection.

How Option Greeks Affect Poor Man’s Covered Call?

Option Greeks significantly impact Poor Man’s Covered Call profitability through their influence on both the long and short legs of the position.

Delta drives the fundamental relationship between your options and the underlying stock. Your long call typically carries 0.70-0.85 delta, meaning it captures 70-85% of stock movement, while your short call usually has 0.30-0.40 delta. This delta differential (0.40-0.55) represents your net exposure to directional moves.

Theta affects your position asymmetrically, creating profitable decay dynamics. Your short-term sold call decays more rapidly (higher negative theta) than your long-term purchased call. This theta differential generates daily profits as time passes, especially during the final 30-45 days of your short option’s life when decay accelerates exponentially.

Vega introduces volatility risk and opportunity. Your long-dated call contains greater vega sensitivity than your short-term call. Volatility increases generally benefit your position through disproportionate gains in the long call, while volatility decreases typically hurt more than help.

Gamma influences delta changes during price movements. The short-term call exhibits higher gamma than the long-term call, causing its delta to change more rapidly during price swings. Monitor this during strong directional moves to maintain appropriate hedge ratios.

Rho affects longer-term options more significantly. Your LEAPS call carries higher rho sensitivity, meaning interest rate increases typically benefit your long position more than they hurt your short call position.

How to Trade using Poor Man’s Covered Call?

Trading using Poor Man’s Covered Call requires selecting appropriate underlying assets with moderate to high price stability and sufficient options liquidity.

To trade with PMCC, first buy a far-month futures contract of the underlying stock or index. In this case, we are using Nifty, and the futures contract chosen is the 31st July expiry, bought at ₹24,711.2. Then, sell a current-month Out-of-the-Money (OTM) call option to generate income through premium collection.

This approach allows the trader to replicate a covered call position without actually holding the stock, hence the name “Poor Man’s Covered Call.”

This strategy benefits from the lower capital requirement of futures compared to buying the underlying stock. It works well when the outlook is moderately bullish, as the trader earns from the future’s price rise and the decay of the short call. In this setup, the call option sold is the 25,050 strike of the current expiry, priced at ₹25.75. The lot size is 75, resulting in a premium income of ₹25.75 × 75 = ₹1,931.25. This premium is your income from the short call, providing some cushion against downside risk.

Maximum profit is achieved if the spot price at the expiry of the call option is exactly ₹25,050. In this case, the future contract would gain (₹25,050 − ₹24,711.2) × 75 = ₹25,298. Adding the premium received from the short call, the total maximum profit comes to ₹25,298 + ₹1,931.25 = ₹27,229.25.

However, the strategy carries downside risk. If the underlying falls sharply below the futures entry price, losses start to accumulate. Since this is a long futures position, there is theoretically unlimited downside risk. The only cushion is the premium received from the short call, ₹1,931.25, which provides minor protection.

The breakeven point for this position is calculated as the futures buy price minus the premium per lot. That is, ₹24,711.2 − ₹25.75 = ₹24,685.45. So, if the spot price falls below ₹24,685.45, the position starts incurring losses.

How to Exit a Poor Man’s Covered Call?

Exiting a poor man’s covered call involves several strategic approaches based on your position’s performance and market conditions. Close the entire position simultaneously by selling your long call and buying back your short call in a single transaction. This complete exit works best when you’ve achieved your profit target or need to free capital for other opportunities.

Allow natural expiration for maximum efficiency when your short call remains out-of-the-money. Let it expire worthless, keeping the entire premium, then sell your long call for its remaining value. This approach maximizes the theta decay benefit of your short position.

Implement a rolling exit strategy during extended bullish runs. Buy back your short call before assignment, then sell your long call for its appreciated value. This captures upside movement while avoiding assignment complications.

Execute defensive exits during adverse price movements. Close both positions, if the underlying stock declines significantly, before your long call loses substantial value. This limits losses to a fraction of what you’d experience owning the actual stock.

Consider partial position closure by selling only a portion of your long call while maintaining short call writing on the remainder. This realizes some profits while continuing income generation.

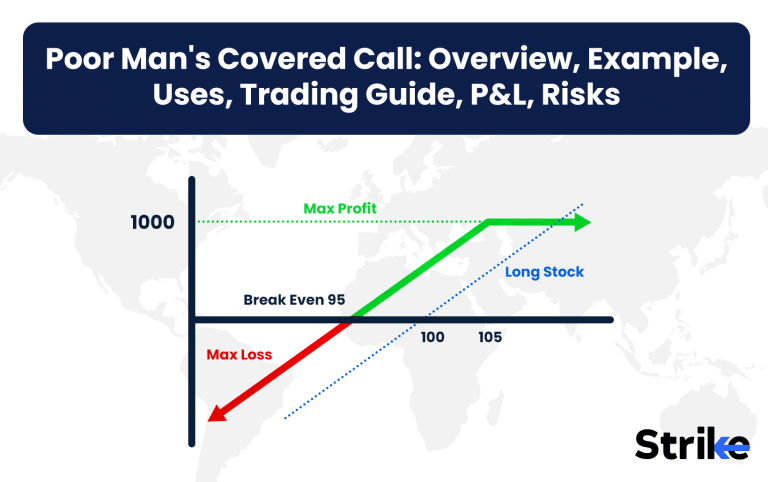

What is the Maximum Profit & Loss, Breakeven on a Poor Man’s Covered Call?

Maximum profit on a Poor Man’s Covered Call equals the difference between short call strike and long call strike plus net premium received when establishing the position.

This profit ceiling occurs when the underlying stock price reaches or exceeds the short call strike at expiration. For example, with a ₹400 long call, ₹450 short call, and ₹15 net debit, maximum profit equals ₹35 per share (₹450 – ₹400 + ₹15).

Maximum loss limits to the net debit paid when establishing the position (cost of long call minus premium received for short call). This worst-case scenario happens if the stock price falls dramatically before expiration, rendering both options worthless. Using the previous example, maximum loss equals ₹15 per share, significantly less than owning 100 shares outright.

Breakeven price calculates as the long call strike plus net debit paid. Continuing our example, breakeven equals ₹415 (₹400 + ₹15). At this price, the long call’s intrinsic value offsets the initial debit, resulting in neither profit nor loss.

These profit/loss parameters improve with each successful short call cycle. Every time you sell a new short call after the previous one expires worthless, you collect an additional premium that reduces your cost basis. After multiple cycles, your effective breakeven drops substantially.

Time decay impacts profitability throughout the position lifecycle. The short call’s faster decay relative to the long call creates positive theta, benefiting the position as expiration approaches.

What Happens if a Poor Man’s Covered Call Expires in the Money?

Your short call faces automatic exercise, when a Poor Man’s Covered Call expires in-the-money, triggering assignment obligations. The options exchange assigns 100 shares per contract to your account, requiring delivery of these shares to fulfill your obligation. You must take specific actions to manage this situation, since you don’t own actual shares in a PMCC.

Your broker typically handles this through an automatic exercise of your long call position. They exercise your long call to acquire shares at its strike price, then immediately deliver these shares to satisfy the assignment of your short call. This results in realizing the maximum profit for your position—the difference between strikes plus any net credit received.

Exercise and assignment involve transaction costs that reduce your overall profitability. Most brokers charge per-contract fees for exercise/assignment ranging from ₹15-50, cutting into your returns especially on smaller positions.

The timing difference between exercise and assignment creates temporary margin requirements. Your broker might require sufficient funds to purchase shares at the long call strike before delivering them for the short call assignment, potentially causing a margin call.

What Happens if PMCC Gets Assigned?

Assignment on your Poor Man’s Covered Call occurs when the short call holder exercises their option, requiring you to deliver 100 shares of the underlying stock per contract. Your broker immediately notifies you of this assignment through your trading platform or email, typically the morning after exercise.

The broker initiates an automatic response to protect your account. They exercise your long call to acquire shares at its strike price, then deliver these shares to fulfill your assignment obligation. This completes the position cycle and realizes your maximum defined profit—the difference between strike prices plus any net credit received at position entry.

Additional fees apply during this process. Assignment incurs a special handling fee (typically ₹15-50 per contract in India), reducing your net profitability. Your broker charges both exercise and assignment fees in this scenario.

Assignment destroys remaining time value in your long call position. Even though your long call might have significant time remaining until expiration, early assignment forces liquidation, eliminating potential future gains from continued appreciation.

What are the Risks of Poor Man’s Covered Call?

Risks of Poor Man’s Covered Call include significant downside exposure despite the reduced capital requirement compared to traditional covered calls. Sharp declines in the underlying stock diminish the long call’s value quickly, potentially erasing most of your investment. Percentage losses often exceed those of covered calls due to the leveraged nature of options.

Assignment risk threatens position management, especially during volatile markets. Early assignment of your short call forces position liquidation, sacrificing time value in your long call. This typically occurs near ex-dividend dates when holders exercise calls to capture dividends.

Time decay damages your long call’s value continuously. Both positions lose time value as expiration approaches, despite the positive theta differential between short and long options. Your long call experiences accelerating decay in its final 30-60 days, requiring careful management of position duration.

Volatility changes impact both legs of your position asymmetrically. Volatility increases generally benefit your long call more than hurting your short call, while volatility decreases typically harm more than help. Sudden volatility spikes during market corrections temporarily increase position value even during price declines.

Is Poor Man’s Covered Call Strategy Profitable?

Yes, Poor Man’s Covered Call strategy generates consistent profits under appropriate market conditions and proper execution. The strategy creates three revenue streams: premium income from short calls, capital appreciation in the long call, and positive theta differential between options. Studies show PMCCs delivering 2-4% monthly returns during sideways or moderately bullish markets.

Repeated short call cycles reduce effective cost basis over time. Traders often reach “free” long call positions after 3-4 successful cycles, where accumulated premium exceeds initial debit paid.

Is Poor Man’s Covered Call Bullish or Bearish?

Poor Man’s Covered Call displays moderately bullish characteristics with defined profit limitations and some downside protection. The strategy profits most when the underlying stock price rises gradually toward the short call strike price without exceeding it significantly. This bullish directional bias stems from the positive delta exposure maintained throughout the position lifecycle.

The position consists of a higher delta long call creating synthetic stock ownership (typically 0.70+ delta) partially offset by a lower delta short call (typically 0.30-0.40 delta). This structure creates net positive delta exposure around 0.30-0.50, confirming the bullish outlook. The position differs from strongly bullish strategies by capping upside potential at the short call strike in exchange for immediate premium income.

What are Alternatives to Poor Man’s Covered Call Strategy?

Alternatives to Poor Man’s Covered Call Strategy include calendar spreads offering similar capital efficiency with different risk profiles. Below are some other alternatives.

| Strategy | Structure | Capital Efficiency | Risk Profile | Income Potential | Market Bias |

| Calendar Spread | Buy and sell options with same strike, different expiries | High | Limited risk, benefits from time decay | Moderate (from time decay) | Neutral to slightly bullish |

| Vertical Bull Call Spread | Buy lower strike call, sell higher strike call (same expiry) | High | Defined risk and reward | Moderate | Bullish |

| Iron Condor | Sell OTM call and put, buy farther OTM call and put (4 legs) | High | Limited risk, wide breakeven range, lower max profit | Limited | Neutral |

| Cash-Secured Put | Sell put with cash set aside for stock purchase | Medium to Low | Similar to covered call risk; potential stock assignment | Moderate (premium income) | Bullish to neutral |

| Naked Put Selling | Sell put without owning underlying or collateral | High (Leveraged) | High downside risk if stock falls below strike | High | Bullish |

| Ratio Spread | Sell more calls than long calls (e.g., 2 short, 1 long) | Moderate | Asymmetric risk; can incur large losses if move is too directional | High (if move is controlled) | Moderately bullish or volatile |

| Synthetic Covered Call | Long put + short call (mimics covered call without owning stock) | High | Similar to covered call; depends on put-call parity | Moderate | Neutral to bullish |

The wheel options strategy is another income-focused alternative where traders sell cash-secured puts first and then sell covered calls after stock assignment.

Is PMCC better than Covered call?

Yes, Poor Man’s Covered Call offers significant advantages over traditional covered calls for most retail traders. PMCCs require substantially less capital—typically 15-30% of the investment needed for regular covered calls—while generating similar returns. This capital efficiency enables traders to diversify across more positions or trade higher-priced stocks otherwise inaccessible.

PMCCs provide superior leverage, amplifying percentage returns on invested capital. A 5% stock move might generate 15-25% returns on a PMCC position versus 5% on a covered call. This leverage creates greater profit potential during favorable market conditions.

The strategy offers enhanced flexibility for adjustments across multiple dimensions including strikes, expirations, and position sizing.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 31")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 37")

No Comments Yet.