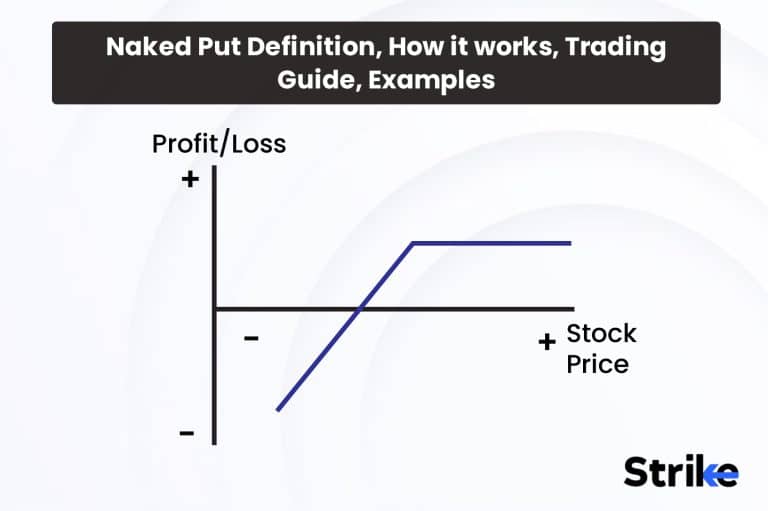

A naked put, or uncovered Put, is an options strategy where an investor sells put options without owning the underlying stock. When one sells a naked put, they take on the obligation to buy the shares at the strike price if the Put is exercised. However, the risk is unlimited as there is no upside limit to losses if the stock price moves significantly below the strike price.

Selling naked puts can be an attractive strategy for investors looking to generate income from premiums. However, it also exposes the seller to significant downside risk if the stock price moves against their position. For this reason, naked puts are considered a very risky, speculative options strategy. The maximum loss is equal to the strike price plus the premium received when the stock falls to zero.

What is Naked Put?

A naked put is an options strategy where an investor sells or writes a put option without holding a short position in the underlying asset. The naked put options strategy allows the investor to generate income by collecting the premium income but also exposes them to unlimited risk if the underlying asset’s price moves substantially lower.

Investors are obligated to buy 100 shares of the underlying stock at the strike price in case the put option is exercised by the counterparty when they engage in a naked put. However, the investor does not hold a short stock position to offset this obligation, unlike a covered put strategy. This leaves the investor with unlimited risk potential if the underlying stock price declines sharply below the strike price of the put option sold. The maximum loss from writing a naked put occurs when the underlying stock price falls to zero.

The investor would be obligated to buy 100 shares of the virtually worthless stock at the strike price in such a scenario. For example, an investor’s maximum risk would be Rs 5,000 (100 shares x Rs 50 strike price) if an investor wrote a naked Rs 50 put on a stock currently trading at Rs 60. The investor receives immediate cash inflow in the form of premium income in return for taking on this unlimited downside exposure from selling the put option.

It is considered a very risky strategy, while writing naked puts allows investors to generate income from options premiums. The key risk is that the investor is exposed to potentially large and unlimited losses if the underlying stock price declines below the strike price. The investor is left with an undesired long stock position that was not part of their original investment thesis if assigned shares at expiration. For this reason, naked puts are usually not recommended for conservative traders or investors with low-risk tolerance.

However, naked puts provide potential upside for more risk-tolerant traders under certain market conditions. An investor, for instance, sells a naked put on a stock that is statistically unlikely to decline substantially based on its historical trading range and volatility. The further out of the money the Put is, the lower the probability of the stock declining below the strike price by expiration. This allows the investor to collect premium income with a relatively low risk of assignment in the short term.

Another approach is to sell naked puts right before the company is expected to report strong quarterly earnings. It further reduces the chances of the stock declining below the put strike price by expiration if the earnings announcement causes an upside surprise. The premium collected on such “earnings naked puts” could potentially be large relative to the actual risk taken, given the informational catalyst. Some traders also opportunistically sell naked puts after a sharp one-day decline in a stock they see as oversold and likely to rebound.

Risk management discipline is crucial when employing naked put strategies in all cases. An investor must have a clear plan for what level of stock decline they are comfortable accepting assignments should the Put be exercised. Strict profit targets and stop losses need to be defined from the outset. Position sizing is also important – naked puts should only represent a small percentage of the overall portfolio to limit exposure from any single trade going against expectations. Finally, rolling or closing output positions before expiration mitigates risk compared to staying in till expiry each time.

What is the importance of Naked Put?

Naked Put is important because it provides an excellent option strategy for generating income. A naked put, also known as an uncovered put, is when an investor sells a put option without shorting the obligated underlying asset. The seller collects the premium as profit if the put option expires worthless. However, if the option is exercised, the seller must purchase the underlying asset at the strike price.

Naked puts allow capitalizing on a neutral/bullish outlook to earn premium income. Selling naked puts is a popular income strategy as it provides steady cash flow. By selling puts on quality stocks you want to own anyway, the option premium received lowers the effective cost basis. Naked puts also help gain exposure to desired stocks without needing the full capital outlay. The key is to sell puts on stocks you are comfortable being assigned.

One of the biggest benefits of naked put selling is the ability to profit even when markets are trading sideways or experiencing a slight downturn. As long as the stock price remains above the put strike at expiration, the options seller gets to keep the premium. This provides an income stream during low volatility conditions when other directional strategies may struggle.

Naked puts allow leveraging existing cash holdings to generate additional returns. The cash secured from the put sale acts as collateral while also earning interest. This creates an advantage over just passively holding cash. The main risk is that the seller may be obligated to buy the underlying shares in case of exercise. However, this is acceptable on stocks you want to own for the long term.

The premiums earned from naked put selling can be utilized to offset any associated exercise costs. Even if exercised, the previously collected premium reduces the effective purchase price. Naked provides a disciplined framework for entering positions at favorable levels in an intended stock. Selling naked puts also allows profiting from high options premiums due to elevated implied volatility.

During such times, rich premiums can be collected, which potentially exceed the stock’s expected near-term downside. Volatility skew further boosts put option pricing, creating advantageous sale opportunities. A key benefit of naked put selling is the ability to profit from time decay. As options near expiration, time value erodes, which works to the advantage of the naked put seller who keeps the full premium. Maximizing time decay results in consistent income generation.

How does Naked Put work?

A naked put works when an investor who wants to employ this strategy will first analyze the underlying asset they want to write. Factors like historical volatility, support levels, and upcoming catalysts are examined. The trader selects a strike price for the put contract that is comfortably out of the money once an opportunity is identified. This lower strike improves the chance of retaining the premium received. The next step is to enter an order to “write” or “sell to open.” this puts a contract on the options exchange.

The trader’s brokerage will deposit the premium amount into their account immediately when the order is filled. This upfront cash is the main benefit, allowing the trader to potentially profit right away. However, in doing so, the trader takes on the obligation to buy 100 shares of the underlying per contract at the strike if assigned.

The trader has three potential outcomes from this point. They close the position for a gain, let it expire worthless, or get assigned the stock. The Put expires worthless, and the trader keeps the full premium as profit if the underlying asset stays above the strike price until expiration. Alternatively, the trader is able to close the position earlier for a gain if the underlying implied volatility declines, increasing the Put’s time value. Another strategy is to roll positions by selling a further out of the money put against an existing put holding to collect additional premiums.

However, the maximum risk occurs if the underlying asset closes below the strike price on expiration. In this scenario, the trader would be assigned 100 shares of the stock per put contract at the strike. They must then decide whether to hold the stock or sell it immediately. Proper risk management using stop-losses, trade size restrictions, and position adjustment is paramount for naked put traders. Unlimited downside exists, unlike covered puts, so disciplined practices around limiting loss exposure per trade are especially important. Successful traders employ these strategies opportunistically when the upside seems most likely.

Skilled traders potentially generate consistent profits from naked puts by balancing premium collection opportunities against downside risk tolerance. But speculating without due care makes the strategy dangerously risky. Traders must have conviction in their analysis to justify outright directional bets through this leveraged vehicle.

What is the equivalent amount in naked Put?

It is crucial for traders to thoughtfully determine the appropriate position size based on their risk tolerance and portfolio capital when employing the strategy of writing naked put options. Taking on naked put exposure without prudent position sizing exposes the trader to an undue amount of risk that could potentially wipe out their entire account.

Traders must first consider the downside liability they are taking on by writing the put contract to calculate the equivalent amount for a naked put position. The trader is on the hook to purchase 100 shares of the underlying stock at the strike price for every put option written if that Put is exercised.

For example, A trader’s liability would be equivalent to being short 100 shares of Stock A at Rs 50 per share, or Rs 5,000 total (100 shares x Rs 50 price) if they write a single naked put on Stock A with a Rs 50 strike price. Traders then compare this liability amount to their overall available trading capital to determine the appropriate position size for their account.

Conservative risk management suggests limiting total naked put liabilities to no more than 20-25% of an account’s risk capital. The position size equivalent would be around five put contracts (5 x Rs 5,000 liability = Rs 25,000 maximum risk) for an account with Rs 25,000 in capital dedicated to options trading strategies.

This allocation still allows for multiple contracts to take advantage of profits while reserving the majority of capital for potential losses. Traders adjust this ratio up or down based on their individual comfort with risk and volatility. It is also recommended to limit liabilities by delta levels rather than just the number of contracts. This caps downside exposure dollars rather than a number of shares and scales appropriately with underlying price changes.

Always maintain sufficient settled funds to withstand a worst-case assignment. Proper position sizing protects traders from a catastrophic loss wiping out their account due to one poorly timed trade. It preserves capital to allow for adjustments and future profit opportunities while naked puts are learned and mastered over time. Account management is key to the long-term success of any options strategy.

What is an example of Naked Put?

Let’s examine a hypothetical example of an opportunistic naked put trade on technology company Applied Widgets Inc. (AWI). The stock has pulled back 5% over the past week on broader market weakness, but fundamental strength remains intact.

An options trader analyzing AWI notices open interest and volume is high on the monthly expiration 50 strike puts. This strike sits 10% out of the money, with the stock trading hands at Rs 55 currently. Looking closer, the trader sees AWI is set to announce quarterly earnings in 5 days that analysts expect will beat forecasts, potentially driving the share price upwards.

The trader feels comfortable taking on the downside risk of a naked put due to the earnings catalyst and support at the Rs 50 level historically. They believe there is a low probability AWI dips below Rs 50 in the short time frame with an anticipated earnings pop. The 50-strike Put is, therefore, considered a high-probability sell. The trader enters an order to write a single AWI May 50 put, collecting Rs 275 of premium upon execution. They determine this one contract position equates to only 5.5% of their Rs 50,000 options account—within their risk threshold, considering the Rs 5,000 downside liability from a potential assignment at expiration.

AWI’s share price holds steady as the earnings announcement approaches over the next several days. The company beats expectations on the release date, fueling a 7% share price rally to Rs 58. Implied volatility declines sharply, with only two weeks until expiration, increasing the time decay on the Put. The trader is now able to repurchase the 50 put position for Rs 125 due to these favorable moves, realizing a Rs 150 profit over a short two-week holding period with minimal risk. They are glad to avoid potentially rocky final days if things turn against AWI before expiration. The trade demonstrates how timing opportune naked puts around catalysts generate alpha.

Of course, not all trades work out so cleanly. Consecutive losses could occur on naked puts even while risk was limited here through position sizing, management, and a near-term focus. Ongoing evaluation of strategies and markets is thus crucial for options traders to maximize winners and identify when conditions have shifted, requiring adjustments.

How to perform Naked Put?

Careful planning and preparation are crucial steps when performing a naked put trade. Traders must thoughtfully analyze both the underlying asset and market environment to perform this strategy effectively. Rushing into trades without conducting adequate fundamental and technical study of the stock or ETF increases the likelihood of taking losses. A loose approach to selection and timing leads the position to move against the trader from the start.

Traders must pay close attention to selecting an appropriate expiration date and strike price in addition to studying the underlying. They also limit profit potential even while shorter durations and further out-of-the-money strikes reduce risk. Conversely, options that are too long-term or close to the current price carry higher risks of assignment. Balancing these factors based on the market assessment is important to define a high-probability trade setup. Choosing poorly without considering how expiration and strike interact with the view easily turns even well-researched trades unprofitable.

Proper position sizing is another vital component that should not be overlooked. Naked options intrinsically expose traders to high leverage, so account allocation must reflect personal risk tolerance. Not establishing position size limits in accordance with total portfolio value invites the very real chance of a single adverse move significantly impairing or even zeroing the account. Failure to plan for worst-case scenarios through prudent capital allocation all but guarantees eventual damaging losses will materialize over many trades.

Ongoing trade management practices like setting protective stops, adjusting positions as conditions evolve, and taking profits in a timely manner are equally imperative elements. Not actively monitoring trades and addressing changes risks, allowing trades to run their full deleterious course unchecked. Proper defense and optimization keep traders on the right side of the markets.

What are the requirements to perform Naked Put?

One of the primary requirements for employing naked put strategies is sufficient capital and trading experience. Naked puts should generally only be utilized by traders with robust portfolios that withstand periods of drawdown due to the potentially large risks involved. Those just starting out in options are best avoiding this advanced strategy until more experience is gained. Significant practice with less risky trades is warranted first to hone skills.

A necessary requirement, in addition to robust capitalization, is access to margin trading. Brokers mandate investors maintain adequate margin capacity to purchase shares if assigned since naked puts lack underlying stock ownership to offset assignment. Often, a minimum of 50% of the stock value per contract is required within the account as a maintenance margin. Failure to meet margin requirements risks facing force-liquidation of positions. Thorough knowledge of options pricing fundamentals like volatility, time decay, and the Greeks is another crucial requirement.

These concepts underpin how the probabilities and risks of naked puts fluctuate over time. Comprehending implied volatility surfaces’ impact on premiums and analyzing gamma risk around strikes is especially important. Traders leave themselves vulnerable to unfavorable trade dynamics without competence here.

Mental fortitude is an essential yet often under-appreciated requirement as well. Naked puts rely on market views being correct. Setbacks are inevitable, testing traders’ capability to objectively evaluate mistakes and tolerance for adversity. Those lacking the proper mindset risk compounded emotional mistakes. Strong discipline in both money management and psychology helps withstand inevitable drawdowns.

When to enter the market using Naked Put strategy?

One scenario where a trader finds a strategic opportunity to enter the market employing a naked put would be after a stock pulls back sharply, but strong fundamentals remain intact.

For example, consider a leading technology company that reports solid quarterly earnings yet sees its share price decline suddenly by 10% in the following session on broader sector weakness. The trader, upon further examination, notices the selloff was primarily driven by macroeconomic fears instead of any issues specific to the company itself. Factors like strong order backlogs, profit margins at multi-year highs, and upbeat management guidance suggest the recent results are sustainable.

However, the market has seemingly disproportionately punished the stock in the short term. The trader hypothesizes the price overcorrected, and a bounce could materialize within the next few weeks as sentiment adjusts. The trader sees an asymmetric risk-reward setup formed based on these observations. A tight band of strikes just below this price point is selected, with the share price currently sitting near a long-term support level. The upcoming 30-45 days hold the potential for implied volatility to decrease as traders’ fears recede.

The trader judges their probability of profit as substantially higher than the risk of falling deeply into the money by selling puts at a strike comfortably below support for this short duration. Retaining the premium seems likely without taking an assignment should the bearish scenario prove unfounded. There is minimal downside, yet reasonable income could potentially be generated from the prudently sized naked put position should the trade work out as envisioned. Some short-term market overreactions birth limited risk opportunities for options income strategies like this. Careful evaluation is required to selectively deploy capital.

When to exit the market using Naked Put strategy?

One scenario warranting closure would be if the underlying stock begins to approach the strike price from above within the option’s remaining lifetime. For example, say an investor had sold a naked put on technology firm Acme Inc. with a Rs 50 strike price expiring in 30 days. Acme was trading at Rs 55 per share at the time of the trade initiation. The stock drifted lower but remained above Rs 52 over the next couple of weeks.

However, negative technical signals started to flash as Acme bounced off its 50-day moving average support for the third time as expiration neared. Daily price momentum also crossed below key levels, indicating a loss of upside vigor. The trader judged the risk of a break below Rs 50 had risen meaningfully with under a week to go. The trader decided to simply close the position for a small profit rather than testing this view, taking the remaining time premium into account. This preserved capital to redeploy into a new opportunity with a more comfortable margin of safety.

Had the Put been allowed to expire in the money, the assignment would have inflicted an undesirable long stock position absent the trader’s original analysis and intent. The risk was prudently mitigated versus gambling on an uncertain outcome by exiting proactively based on shifting market conditions. It’s generally wiser for naked put sellers to depart trades early once favorability fades versus cutting losses deeply if assigned. Optimal times often coincide with technical warning signs or macro surprises dissolving prior edge assumptions. Disciplined traders respect such changes in risk/reward promptly.

What is the maximum gain for Naked Put strategy?

The maximum theoretical gain is capped at the initial premium received upon entering the position when employing naked put trades. For example, Rs 250 would represent their maximum possible profit on that particular trade if an options seller writes a put contract and collects Rs 250 in premium from the buyer.

This ceiling is reached if the underlying stock closes above the put strike price on the expiration date, resulting in the option expiring worthless. The premium collected in this scenario is unattainable to exceed since it has already been fully realized upfront as profit.

Some traders attempt to enhance gains through other techniques like rolling positions. However, this also introduces additional risk. Rolling involves simultaneously buying back the original Put sold and using those proceeds plus extra funds to write a new put with a later expiration date. It increases the cost basis and extends the risk window while also allowing the collection of multiple premiums over time. Each roll amplifies liabilities versus simply accepting the original maximum ceiling. Rolls morph into larger losing trades counter to their intent unless executed carefully.

What is the maximum loss for Naked Put strategy?

Naked puts carry theoretically unlimited risk given appropriate market conditions, unlike covered put writing, where the short stock position limits the downside. The maximum possible loss is only reached in the most severe of scenarios where the underlying asset’s stock price plunges fully to zero. Consider an options trader who writes a naked put with a Rs 50 strike price to understand how this occurs.

The stock is trading hands around Rs 60 per share when entered. The trader would face assignment at Rs 50 per share despite the actual worthlessness of the security should a cataclysm later drive the stock beneath any conceivable support to negligible valuations.

Short-term plunges remain possible, while bankruptcy or similar market crashes resulting in total loss are thankfully rare. For example, the options writer stands to lose Rs 4,500 on that single contract after keeping the initial premium if compelled to purchase 100 shares of a Rs 60 stock depressed to just Rs 5 upon expiration.

Of course, most trades are closed or expire prior to such doomsday scenarios playing out in full. But the open-ended downside is why naked puts demands stringent risk management. Position sizing to a small percentage of total capital helps cap worst-case obligatory stock purchase exposure. Ongoing technical analysis also aids in timely reassessment and position adjustment or closure when bearish setups form.

How does volatility affect Naked Put strategy?

Volatility is one of the most significant factors impacting the profitability of naked put trades. Higher implied volatility embedded in option prices generally benefits sellers, while declining volatility favors buyers. Understanding these dynamics is crucial for traders employing this strategy. Put options will trade at inflated premiums compared to intrinsic value when implied volatility is high.

This provides an advantageous environment for writing puts, as prices have been bid up beyond theoretical worth. The elevated premium collected acts as a bigger buffer against adverse stock movement. However, as turbulence subsides, the market’s “fear premium” embedded in options fades accordingly. Time decay accelerates as volatility falls and prices regress toward their genuine valuation.

This decreases the value of short puts more rapidly, allowing well-timed traders to repurchase contracts at a profit even if the stock price is unchanged. Selling puts during high implied volatility environments, therefore, capitalizes on relatively cheap option insurance being sold to panic-driven buyers. The duration mismatch between collection and potential assignment is optimized for time value decay by targeting contracts set to expire before any macro uncertainty has fully resolved.

How does time decay affect Naked Put strategy?

Time decay, also known as theta decay, is one of the major factors benefiting those who employ naked put strategies. The natural erosion of time value inherent to all contracts is a trader’s ally when expirations approach as an options seller. Put options derive a portion of their premium from the length of time until expiration. The longer the duration, the greater their time component. But this time, the premium proportionally shrinks as the ta burn sets in as each day passes.

Options sellers profit off this steady withering away of value through Vega volatility selloff and declining day count. Time decay exerts an outsized influence on naked puts in particular. It serves as a buffer protecting against adverse short-term stock movements, which correct prior to monthly or weekly expiries. Daily theta burn chips away additional downside, improving the positional break even should the underlying slip modestly below the strike.

Traders, therefore, benefit by targeting options with 30 days or less until expiry. The high and accelerating decay rate compresses premiums rapidly, allowing well-positioned sellers to repurchase contracts for less than originally sold to lock in the time premium spread. Nearing expiration also diminishes tail risk exposure from any unanticipated volatility spikes, disrupting the maintenance of strike price buffers.

Pinning to the deliverable range curtails erratic swings once weekly options reach their last few sessions. Carefully selecting short puts offering a sizable time premium component enhances how close traders can operate to expiration before facing assignment threats. This maximizes the decay harvesting period’s influence on position results over many trades.

What are the things to consider before applying the Naked Put strategy?

There are 5 important factors to consider carefully before employing a naked put strategy. They are given below.

- One of the primary things to evaluate is thorough research into the underlying asset. A trader should conduct both fundamental and technical analysis of the stock or ETF. They need to understand the company’s industry, historical price behavior, upcoming earnings dates, or other catalysts. Reviewing past levels of implied and realized volatility is also crucial. This upfront investigation helps identify high-probability trades.

- Traders must thoughtfully determine position sizing. Naked puts introduce substantial leverage, so guidelines are required. One approach is allocating no more than 20-25% of total portfolio capital to any single trade. Another is placing a limit on the total position delta. Maintaining settled funds to potentially cover any assignments is also prudent. Proper sizing aims to cap risks.

- Choosing appropriate option contracts that match the market view is another key thing to assess. The ideal expiration should correspond to that outlook’s time horizon. Targeting out-of-the-money strikes with high probabilities of expiring worthless also fits risk profiles. Considering open interest and volume helps ensure potential liquidity needs at later dates.

- Defining robust risk management practices beforehand is equally important. This includes setting a maximum acceptable loss on each position. Placing a stop loss or trailing stop order protects against further downsides. Remaining vigilant by monitoring trades continuously also enables quick action to change. Preparation here guards against surprises.

- The current environment’s macro factors must be evaluated, too. Implied volatility trends impact premium levels and probabilities. Any recent news stories affecting relevant market sectors should be noted. Watching support and resistance zones aids in timely exits. Hedging naked puts with offsetting positions sometimes warrants consideration as well.

Careful consideration of all these elements through comprehensive planning decreases risk when shorting options. Naked puts, though providing income opportunities, demand experienced handlers cognizant of their inherent leverage. Solid research and preparation are requirements for consistent long-term application.

Is Naked Put a good strategy?

Yes, naked put selling is a good options strategy when used properly. By selling puts on quality stocks you want to own, you can earn premium income while lowering the effective cost basis if exercised.

Is Naked Put suitable for beginner traders?

No, naked put strategies are generally not suitable for traders just starting out in the markets upon careful consideration. They introduce elevated risks that inexperienced handlers tend to be ill-equipped for while these options trades generate income when employed skillfully.

Is Naked Put best for the long term?

No, naked put strategies are generally not considered the optimal approach for long-term investing and wealth generation. Several factors diminish their appropriateness as a core portfolio allocation strategy for the long haul, while skilled traders employ them profitably over the years.

How efficient is the Naked Put strategy?

The naked put strategy is not considered particularly efficient in the context of portfolio management. Several factors diminish its overall efficiency relative to other options, while skillful traders generate steady premium income deploying it.

Is Naked Put better than Diagonal Call in terms of long-term profit?

No, the diagonal call strategy would likely prove more conducive to generating consistent long-term profits compared to naked puts. Factors tilt the scales in favor of diagonal calls for buy-and-hold portfolios, while experienced traders deploy both capably. One advantage is the reduced risk profile.

Diagonal calls involve limited downside via long calls held as a hedge. Naked puts carry an unlimited risk if markets plummet unexpectedly. Over decades, extreme moves emerge that could overwhelm even optimized put strategies. Limited risk aids in compounding gains steadily.

Is Naked Put better than Covered Short Strangle in terms of long-term profit?

The covered short strangle strategy holds some advantages over naked put writing when assessing long-term profitability. The strangle approach provides a more balanced risk-return profile better suited for buy-and-hold investors though both generate premium income.

A key benefit of strangles is their defined risk characteristics. Maximum loss on strangles is known with short strikes acting as ceilings, unlike naked puts, which carry an unlimited downside. Over decades, unpredictable events will surface, testing portfolio resilience – limited risk protects accumulated gains.

Capital efficiency is also stronger with strangles. Larger sizing is deployed within the same margin requirements since positions are covered with an underlying stock holding. This magnifies income generation on a dollar-for-dollar basis compared to the restrictive leverage of naked puts. Compounding works more powerfully.

Is Naked Put better than Long Iron Condor in terms of short-term profit?

Yes, for traders primarily focused on generating profits within brief trading periods, the naked put strategy arguably holds an edge over long iron condors. Both offer premium income when markets remain steady. However, several factors pertaining to risk exposures and position mechanics make naked puts a more advantageous short-term play.

What is the difference between Naked Put to other Income strategies?

Naked puts differ meaningfully from alternative approaches in several key ways, while many options strategies aim to generate premium income. One such tactic is covered calls, where the underlying stock is owned prior to writing calls. This caps the downside, trading the upside for regular smaller payouts.

Naked puts lack this balance, carrying unbounded risk below strikes to amplify profits but demand stringent risk management. Leverage magnifies both wins and losses, so placement and sizing require expertise calls. Protection also reduces probabilities for optimal returns long-term versus dynamically positioned naked plays.

Another income vehicle is cash-secured puts, like covered calls limiting exposure with dedicated funds. The upside is sacrificed to consistently collect premiums, whereas naked puts carry flexible upside participation when trades work out. However, unlimited downside demands trader skill, as puts obligate stock purchases outright.

Naked puts actively aim to benefit from short-term underperformance or choppiness rebounding to protective strikes, while long-term strategies often deploy diagonal spreads or covered strangles. These sell premium out and purchase longer-dated cover, structuring steady renewal of limited risk positions with less dependence on precise technical or sentiment views.

Even condors, which take advantage of stasis with little directional opinion, remain on for extended periods passively depreciating. Naked puts necessitate ongoing judgment adjusting or closing flawed setups before harm escalates. Other options ease costs and management demands long-term investors’ value.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.