A fence option is a three-legged options trading strategy used to hedge a long stock position while controlling both upside and downside. A fence option combines a long stock holding, a long put, a short call, and a short put, creating a defined range for both profit and risk.

This structure is attractive for investors in India who seek to protect their equity exposure, especially when markets are expected to remain stable or moderately bullish. The main goal is to reduce hedging costs—often to zero or even a net credit—while still offering limited downside protection.

What Is a Fence Strategy in Options Trading?

A fence strategy in options trading is a structured, three-part hedge for a long stock position, often called a collar with a short put.

The fence strategy is achieved by holding the underlying stock, buying a put (to protect against minor falls), selling a call (to cap gains), and selling an additional, lower-strike put (to help pay for the hedge).

Unlike a regular collar, the extra short put in a fence means there is more downside risk if the stock price falls sharply.

This trade-off allows the investor to often set up the hedge at a net premium credit or zero cost, making it attractive during periods of low volatility. A fence strategy is particularly useful when you want to retain stock ownership and avoid paying high premiums for protection.

It is popular in the Indian market, especially among traders with large holdings in blue-chip stocks or indices. The strategy suits those who are comfortable with limited gains and controlled losses, in exchange for lower hedging expenses.

The fence is a flexible tool, but it comes with complex margin requirements and the potential for substantial loss if the stock falls below the lower short put strike.

How Does a Fence Work?

A fence works by combining a stock holding with a protective put, a short call, and an additional short put to create a cost-efficient hedge with capped gain and loss levels.

The objective is to provide downside protection for a long equity position, but at little or no cost—sometimes even generating a small net credit.

Trade Structure

- Own 100 shares (or 1 lot) of a stock trading at Rs. 2,000.

- Buy 1 put at a lower strike (e.g., Rs. 1,950) for Rs. 30.

- Sell 1 call at a higher strike (e.g., Rs. 2,100) for Rs. 25.

- Sell 1 put at a much lower strike (e.g., Rs. 1,850) for Rs. 10.

Net Premium

Rs. 30 (put bought) – Rs. 25 (call sold) – Rs. 10 (put sold) = Rs. 5 net credit.

Payoff Structure

- If the stock rises above Rs. 2,100, profit is capped at the call’s strike.

- If the stock falls below Rs. 1,950 but stays above Rs. 1,850, the loss is limited to the difference between the strikes.

- If the stock drops below Rs. 1,850, losses increase sharply due to the extra short put.

Tthe fence is often used to hedge large positions with an average cost reduction of 50-100% versus buying a protective put alone.

The fence’s payoff chart shows a flat gain above the call strike, a steady loss zone between the two puts, and an accelerated loss below the lowest put.

What Is an Example of a Fence Trade?

An example of a fence trade starts with owning a stock and layering three options to define the profit and loss range.

Suppose you own 1 lot (100 shares) of Reliance at Rs. 2,400.

- Buy 1 Reliance 2,350 put for Rs. 22.

- Sell 1 Reliance 2,500 call for Rs. 18.

- Sell 1 Reliance 2,250 put for Rs. 10.

Net premium

Rs. 22 (put bought) – Rs. 18 (call sold) – Rs. 10 (put sold) = Rs. 6 net credit per share.

Scenario 1

If Reliance rises above Rs. 2,500 at expiry, you are obligated to sell at Rs. 2,500, locking in a profit of Rs. 100 per share plus the net premium.

Your gain is capped, but you are protected against a sharp drop.

Scenario 2

If Reliance falls below Rs. 2,350 but stays above Rs. 2,250, your total loss is limited to Rs. 100 per share minus the net premium.

Scenario 3

If Reliance falls below Rs. 2,250, you start facing significant losses, as you must buy additional shares at Rs. 2,250 no matter how low the market price falls.

This example highlights how the fence offers capped profit, limited loss over a range, and significant risk only if the stock collapses far beyond the short put.

Why Use a Fence Strategy?

Investors use a fence strategy to hedge long equity positions at low or no net cost, while accepting limited upside in exchange for reduced hedging expenses.

This approach is especially useful for those who want to protect their portfolio against small-to-moderate declines without spending much on premiums. Here are the benefits.

- Hedge at minimal cost: By selling two options, you offset the cost of buying protection.

- Downside protection: Shields against moderate stock price drops, which is crucial in volatile markets.

- Income generation: The net premium credit from the options sold can add to your returns.

- Defined risk zone: You know exactly how much you stand to gain or lose within a given range.

A fence is often used during earnings season or before major policy events, when stock volatility can spike. The fence strategy is ideal for investors willing to accept capped gains in exchange for cost savings and a clear profit/loss range.

When to Use a Fence Strategy?

A fence strategy suits investors with a moderately bullish or neutral outlook, who are willing to accept limited upside in exchange for lower hedging costs.

It is especially effective when you want to reduce the premium cost of a regular collar and are comfortable holding stock through a specific price range. Let us look at some ideal situations.

- Neutral to mildly bullish markets: When you don’t expect a sharp rally but want to keep some upside.

- Cost-conscious hedging: When buying a plain put is too expensive, fences provide a budget-friendly solution.

- Stock ownership with a target exit: If you plan to sell a stock if it rises above a certain level, a fence can capture gains up to that price.

- Defined loss acceptance: Willing to take on more risk if the stock price falls drastically below the short put.

Fences are common for large-cap stocks before quarterly results, where volatility is high and hedging costs spike. Investors use this Option trading strategy to lock in gains or protect capital temporarily, often rolling the position as the outlook changes.

How to Structure a Fence Trade

To structure a fence trade, follow these steps to combine stock ownership with three strategic options positions.

- Own or buy the underlying stock.

You must have the stock in your portfolio, as the strategy is designed to hedge existing equity exposure. - Buy a protective put (lower strike).

Purchase a protective put option at a strike slightly below the current market price to limit downside risk. - Sell a covered call (higher strike).

Sell a covered call option at a strike above the current price to generate premium and cap your upside. - Sell a lower strike put (below the long put).

Sell an additional, further out-of-the-money put to bring in more premium and reduce or eliminate the net cost.

Example:

- Stock: Rs. 2,000

- Buy 1 Rs. 1,950 put (pay Rs. 30)

- Sell 1 Rs. 2,100 call (receive Rs. 25)

- Sell 1 Rs. 1,850 put (receive Rs. 10)

The net premium is often zero or slightly positive, resulting in a low-cost hedge with defined risk and reward bands.

Ensure you monitor margin requirements, especially for the extra short put, as significant losses can occur if the stock falls sharply.

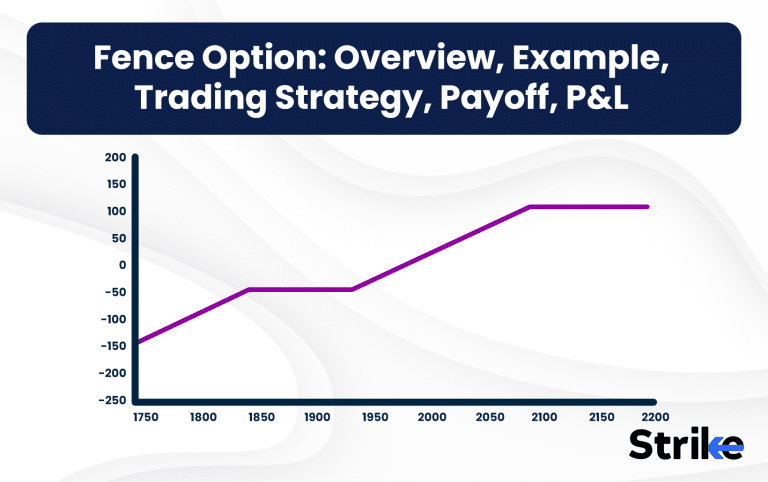

What Is the Payoff Structure of a Fence?

The payoff structure of a fence features limited maximum gain, a small loss zone, and potentially large loss if the stock falls below the short put.

This unique combination creates a payoff graph that is flat at the top, dips slightly in the middle, and drops steeply at the bottom.

Payoff zones

- Maximum gain: Achieved if the stock rises above the short call’s strike. The profit is capped at the difference between the stock price and the call strike, plus collected premiums.

- Small loss zone: If the stock finishes between the long put and the short put at expiry, you incur a minor loss (the “fence” zone).

- Maximum loss: If the stock falls below the short put strike, you face large and theoretically unlimited losses, as you are obligated to buy more stock at the lower strike.

Example:

- If the stock closes above the call strike, gains are capped (e.g., Rs. 100 per share).

- If it closes between the long put and the short put, losses are minor (e.g., Rs. 50 per share).

- If it drops below the short put, the loss grows rapidly (e.g., every rupee drop below the strike adds to your loss).

This structure suits investors who want capped profits, shallow risk in a defined range, but are willing to accept deep risk only in extreme scenarios.

What Is the Profit/Loss & Breakeven in a Fence?

Profit, loss, and breakeven in a fence strategy are determined by the option strikes, premiums, and the movement of the underlying stock.

The maximum profit is capped, losses are limited within a range, and breakeven points are wider than in a collar due to the extra premium collected from the short put.

Key profit/loss points

- Maximum Profit: Achieved if the stock closes at or above the short call’s strike.

Profit = (Call strike – Stock purchase price) + Net premium received. - Maximum Loss: Occurs if the stock falls below the short put strike.

Loss = (Long put strike – Short put strike) – Net premium received + (Stock purchase price – Short put strike) for every share below the short put. - Breakeven Points:

- Upside breakeven = Stock purchase price + Net premium received.

- Downside breakeven = Short put strike – Net premium received.

Fences often have wider breakeven bands than collars, reflecting the extra income from the sold put.

This makes them attractive for cost-conscious investors but requires careful monitoring if the stock price approaches the short put.

Is the Fence Strategy Profitable?

Yes, a fence strategy is profitable in stable or slightly bullish markets, offering small upside potential and controlled loss.

This approach works best when the premium collected from selling options offsets the cost of buying protection.

The risk-reward profile is asymmetric: you risk large losses only in a market crash, but most of the time, profits are steady and predictable.

The strategy is less profitable than aggressive bullish strategies but provides more stability.

What Are the Risks of the Fence Strategy?

The main risks of a fence strategy are large losses if the stock price falls below the short put, capped profit from the covered call, and complex margin requirements.

- Downside breach: If the stock drops below the short put strike, losses can be unlimited, as you must buy more shares well below the market price.

- Profit cap: Gains are limited to the call strike, reducing potential upside in strong bull markets.

- Margin requirements: Selling an extra put increases margin needs, especially if not cash-secured.

- Assignment risk: Early exercise of the short options can occur, particularly close to expiry.

- Monitoring: Fences require careful management, especially if the underlying approaches the short put or call strike.

Always assess your willingness to buy more stock at much lower prices and ensure you have the margin to cover potential losses.

Not managing these risks can result in large, unexpected losses, especially during market crashes.

What Is the Difference Between a Fence and a Collar?

The main difference between a fence and a collar is that a fence adds a short put to the collar structure, increasing risk in exchange for a wider breakeven and more premium.

Both strategies use a long stock, a long put, and a short call, but only the fence includes an extra short put.

| Feature | Collar | Fence |

| Components | Stock, Long Put, Short Call | Stock, Long Put, Short Call, Short Put |

| Downside Risk | Limited | Unlimited below short put |

| Premium Cost | Usually debit | Usually credit or zero |

| Breakeven Band | Narrow | Wider |

| Profit Cap | Yes | Yes |

The fence is more aggressive, offering more premium income but exposing the trader to higher risk if the stock falls sharply.

Choose a collar for more conservative risk management, and a fence if you desire a larger breakeven band and are comfortable with higher downside risk.

What Are the Alternatives to the Fence Strategy?

Alternatives to the fence strategy include the collar, protective put, covered call, put spread, and iron condor, each offering different risk-reward profiles.

The choice depends on your outlook, risk tolerance, and cost considerations.

| Strategy | Components | Risk Profile | Cost/Net Premium |

| Collar | Long Stock, Long Put, Short Call | Limited downside, capped upside | Usually small debit |

| Protective Put | Long Stock, Long Put | Pure downside hedge, unlimited upside | High debit |

| Covered Call | Long Stock, Short Call | Capped upside, no protection | Credit |

| Put Spread | Long Put, Short Put | Limited risk, bearish | Debit |

| Iron Condor | 2 Calls + 2 Puts, 4 strikes | Range-bound returns, limited risk | Credit |

Choose a strategy aligned with your market view, capital, and risk appetite.

Different approaches work better at different times; always weigh cost, risk, and reward before deciding.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 32")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 33")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 34")

: Overview, 10 Types of Indicators, Settings for Different Markets 36")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 38")

No Comments Yet.