A short box spread is an advanced options strategy combining a bear call and bull put spread with the same strikes and expiry, creating a synthetic way to lend money at the market’s implied interest rate. A short box spready involves receiving a net credit upfront and paying a fixed amount at expiry, with profit or loss locked in at entry.

A short box spread offers no directional risk and is used mainly by institutions for arbitrage or synthetic financing. Key risks include execution challenges, early assignment, and high margin requirements. Retail traders rarely benefit due to transaction costs and competitive institutional trading.

What Is a Short Box Spread?

A short box spread is an advanced options strategy made by selling a bear call spread and a bull put spread, using the same strike prices and expiration date. The short box spread is a synthetic way to lend money through the options market.

This strategy is not commonly used by retail traders in India or globally, due to high transaction costs and margin requirements. Instead, it is popular among institutional traders looking for arbitrage opportunities or a way to earn on market mispricings. The short box spread locks in a risk-free payoff if priced correctly, but perfect execution is required.

Since the trade is not sensitive to movements in the underlying asset, it is not a directional bet. It is used only when there are clear pricing discrepancies. In efficient markets, the profit potential disappears quickly as algorithms and large traders step in.

How Does the Short Box Strategy Work?

The short box strategy works by selling a bull put spread and a bear call spread at matching strikes and expiry, locking in a net credit and a fixed future payment. Here’s a step-by-step explanation.

- Sell a bull put spread: You sell a put at the higher strike (e.g., Rs. 110) and buy a put at the lower strike (e.g., Rs. 100), receiving a net credit.

- Sell a bear call spread: You sell a call at the lower strike (Rs. 100) and buy a call at the higher strike (Rs. 110), again for a net credit.

Both vertical spreads use the same strikes and expiry date, so the profit or loss is not affected by the underlying stock’s price. The total net credit you receive up front is your maximum possible profit. At expiry, you must pay the fixed difference between the strikes, which is Rs. 10 in this example.

The short box is a synthetic way to lend money at the options market’s implied interest rate. If there’s mispricing between the four legs, you lock in a profit. If options are efficiently priced, your profit is negligible after costs. This strategy is not a bet on direction, volatility, or trend—it is purely a capital markets trade.

This trade requires careful execution. Liquidity, tight bid-ask spreads, and advanced order entry tools are crucial for capturing arbitrage.

What Is an Example of a Short Box Trade?

Same stock, with the same strikes and expiry. Here’s a detailed example using a real Indian stock.

- Underlying: Reliance Industries (hypothetical prices for illustration)

- Strikes: Rs. 100 and Rs. 110, both expiring in one month

Construct the trade:

- Sell 1 Reliance Rs. 100 call, buy 1 Reliance Rs. 110 call (bear call spread)

- Sell 1 Reliance Rs. 110 put, buy 1 Reliance Rs. 100 put (bull put spread)

Suppose you receive a net credit of Rs. 9.50 per share for the entire box. At expiry, regardless of where Reliance trades, you will owe Rs. 10 per share, since the combined spread width is always Rs. 10.

Payoff at expiry

- If Reliance expires above Rs. 110, both call and put spreads are exercised, locking the fixed loss.

- If it expires below Rs. 100, you have the same result.

- If it expires between Rs. 100 and Rs. 110, option assignments offset, still resulting in the same payoff.

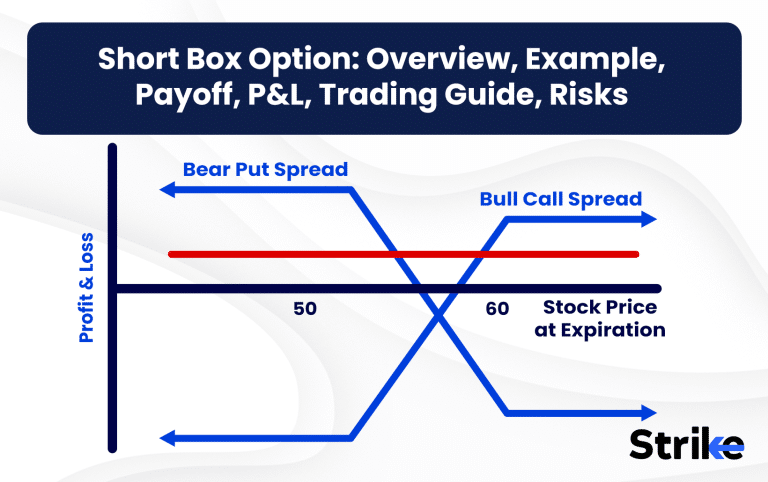

Payoff diagram

- The line is perfectly flat, showing a fixed loss of Rs. 0.50 per share (Rs. 10 owed minus Rs. 9.50 received).

This example highlights the short box’s use for arbitrage, not speculation, in option trading, where the strike price plays a critical role in determining the strategy’s profitability.

What Is the Payoff of a Short Box?

The payoff of a short box spread is a fixed, known payout at expiry, regardless of where the underlying asset trades. This makes it unique among options strategies because it has zero exposure to the price of the underlying security.

At expiry, you owe the spread width (Rs. 10, using the example above), no matter how far the stock has moved up or down. This fixed payment is offset by the net credit you received when the trade was opened. As a result, your profit or loss is predetermined at the time of entry.

This structure means there is no volatility, delta, or trend exposure. The payoff is shown as a flat line on a chart, with no changes regardless of where the stock finishes. This makes it appealing to traders seeking arbitrage or synthetic financing.

The only variables that affect the payoff are mispricing at entry, transaction costs, and execution quality. If the market is efficient, the box will price close to the present value of the spread width, leaving little room for profit.

What Is the Profit/Loss & Breakven in a Short Box?

Maximum profit in a short box is the net credit received at entry, while maximum loss equals the sprMaximum profit in a short box is the net credit received at entry, while maximum loss equals the spread width minus the net credit. There is no breakeven price, as the profit or loss is locked in when the position is opened.

- Max profit: If you receive a credit greater than the present value of the spread width, that extra amount is your profit. For instance, if the spread width is Rs. 10 and you receive Rs. 10.20, your profit is Rs. 0.20 per share.

- Max loss: If you receive a credit less than the spread width, the shortfall is your loss. For example, if you receive Rs. 9.80, your loss is Rs. 0.20 per share.

- No breakeven: Since the box is not directional, there is no breakeven based on stock price.

The only factors influencing P&L are transaction costs, margin interest, time decay, and time-value. Interest rate differences between now and expiry can create or eliminate profit opportunities. For retail traders, costs and execution risks often wipe out potential gains.

Institutional traders use the short box to lock in synthetic interest rates. In India, margin and liquidity requirements are high, limiting this trade to the most sophisticated participants.

How to Execute a Short Box Spread?

To execute a short box spread, you must sell both a bear call spread and a bull put spread at the same strikes and expiry. Here’s a step-by-step process.

- Choose a liquid underlying: Pick a stock or index with high options liquidity and tight bid-ask spreads. Liquidity is critical for execution.

- Select strike prices: Decide on two strikes, such as Rs. 100 and Rs. 110, that are available for both calls and puts.

- Sell both spreads: Enter four orders—sell Rs. 100 call, buy Rs. 110 call, sell Rs. 110 put, buy Rs. 100 put.

- Verify net credit: Ensure the premium received is close to the spread width minus the time value of money. Any mispricing here is your opportunity for profit.

- Check margin requirements: This strategy requires high margin, as you are exposed to maximum loss if not executed properly.

- Use advanced trading platforms: Multi-leg order entry is recommended to reduce legging risk. Some Indian brokers offer spread entry tools.

Professional traders use algorithms to execute all four legs of strategies like the Bear Call and Bull Put simultaneously. For retail traders, achieving perfect execution is difficult, and partial fills can introduce risk.

When to Use a Short Box Strategy?

ThThe short box strategy is best used for arbitrage when pricing inefficiencies exist, or for synthetic financing needs. It is not intended for making bets on direction, volatility, or trends.

- Arbitrage: If the market misprices the four options legs, you can lock in a risk-free profit by executing the box. This is rare but possible, especially during periods of market stress or low liquidity.

- Synthetic financing: Institutions use the short box to lend cash at the implied market interest rate, earning a return from the net credit received.

- Flat market view: The short box has no risk from stock price movement, so it’s suitable when you expect low volatility and want to avoid directional exposure.

- Non-directional trading: Traders who want to profit from market inefficiencies without taking on price risk use this strategy.

Retail traders rarely use the short box due to high margin requirements and transaction costs. Most arbitrage profits are quickly eliminated by professional traders with faster access and lower costs.

The short box is not suitable if you expect significant volatility, as early assignment or dividend events can disrupt the trade and introduce risk.

What Are the Risks of a Short Box?

The main risks of a short box are execution risk, assignment risk, and interest rate changes. Here’s a detailed look at each.

- Execution risk: All four legs must be filled at optimal prices. Any slippage or partial fill can turn a risk-free trade into a loss.

- Assignment risk: If options are American-style, you could be assigned early on one or more legs. This breaks the box and introduces unwanted stock exposure.

- Early exercise and dividends: If a dividend event occurs before expiry, puts or calls might be exercised early, impacting the trade outcome.

- Interest rate risk: Changes in risk-free rates can alter the value of the box, creating or eliminating arbitrage opportunities.

- Margin requirement: Short boxes require significant margin, as exchanges demand collateral for the fixed payout at expiry.

- Mispricing risk: If volatility skews or liquidity issues cause mispricing, you might lock in a loss instead of a profit.

Retail traders face a higher risk due to wider bid-ask spreads, slower execution, and higher commissions. Institutional traders have better access and tools, allowing them to manage these risks more effectively.

Is the Short Box Strategy a True Arbitrage?

Yes, the short box is a true arbitrage in theory, but practical trading frictions often reduce or eliminate Yes, the short box is a true arbitrage in theory, but practical trading frictions often reduce or eliminate profits. If all four legs are executed at fair value, you lock in a risk-free profit that is independent of market direction.

- In theory: No market risk, no volatility exposure, and fixed profit/loss.

- In practice: Execution frictions are significant. You face:

- Slippage from imperfect fills

- Commissions and taxes

- Bid-ask spreads, especially on less liquid options

- Potential early assignment if American-style options are used

- Institutional advantage: Large traders and institutions with direct market access exploit most arbitrage opportunities. They use algorithms for fast execution.

Retail traders rarely access true arbitrage due to costs and execution delays. Statistics show that less than 1% of retail box spreads succeed in capturing true arbitrage after fees, compared to 10% or more for institutions.

This makes the short box a professional’s strategy, not a retail one.

How Are Box Spreads Priced in the Market?

Box spreads are priced near the present value of the spread width, determined by risk-free interest rate parity. This means the price of a box reflects the implied interest rate in the options market for the time to expBox spreads are priced near the present value of the spread width, determined by risk-free interest rate parity. This means the price of a box reflects the implied interest rate in the options market for the time to expiry.

- Interest rate parity: The fair value of a Rs. 10 box expiring in three months is the present value of Rs. 10, discounted at the prevailing risk-free rate.

- Typical market pricing: If the annual interest rate is 6%, a three-month box would trade at approximately Rs. 9.85 (Rs. 10 discounted for 0.25 years).

- Time to expiry: The longer the time to expiry, the lower the present value of the box.

- Retail profit margin: Typical transaction costs in India for a four-leg trade (including taxes and commissions) are about Rs. 0.20–0.30 per share, wiping out most arbitrage gains for small traders.

As a result, box spreads rarely offer profits for retail traders after costs. Institutional traders, with lower fees and better execution, capture most opportunities. Box spread pricing, driven by option pricing models, is a key indicator of interest rate expectations in the options market.

Short Box vs Long Box: What’s the Difference?

The short box spread involves selling both a call and put spread to synthetically lend money, while the long box spread involves buying both spreads to synthetically borrow money, with both strategies locking in a fixed payoff regardless of stock direction.

| Feature | Short Box Spread | Long Box Spread |

| Construction | Sell call + sell put spread | Buy call + buy put spread |

| Net Cash Flow | Receive premium (credit) at entry | Pay premium (debit) at entry |

| Synthetic Action | Synthetic lender (you lend cash) | Synthetic borrower (you borrow cash) |

| Payoff | Pay spread width at expiry | Collect spread width at expiry |

| Directional Risk | None | None |

| Use Case | Arbitrage, synthetic lending | Arbitrage, synthetic borrowing |

| Margin | High | High |

| Retail Use | Low | Low |

| Institutional Use | High | High |

The short box is used to lend money at the options market’s implied rate, while the long box is used to borrow money. Both are non-directional, market-neutral strategies requiring significant capital and expertise.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 16")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 17")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 18")

: Overview, 10 Types of Indicators, Settings for Different Markets 21")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 22")

No Comments Yet.