Exotic options are financial derivatives with more complex features than standard call or put options. Exotic options are designed to address specific investment, hedging, or risk management needs that ordinary options cannot solve efficiently.

Traders and institutions use exotic options to benefit from unique payoffs, custom exposure, or to reduce costs. These features make them popular in global markets, especially among sophisticated investors. The global market for exotic options is substantial, with research suggesting they account for over 25% of total OTC derivatives traded annually.

What Are Exotic Options?

Exotic options are customized derivatives with non-standard payout structures or conditions. Exotic options depend on variables such as the path of the underlying asset, time, or combinations of multiple assets.

These options are typically traded over-the-counter (OTC) between financial institutions and their clients. This allows for greater flexibility and customization, but also introduces additional risks, such as counterparty risk and lower liquidity.

Some exotic options are used for hedging highly specific exposures, while others offer speculative opportunities not available with vanilla options. Their complexity makes them less accessible to retail investors, but extremely useful for corporations and institutional traders with unique requirements.

Why Are They Called “Exotic”?

The term “exotic” highlights the options’ unusual and innovative features compared to standard (vanilla) contracts. The phrase originated in the 1980s, as banks and financial engineers developed new products to solve specific client problems.

Vanilla options refer to the most basic, traditional contracts, while exotic options break these molds. The “exotic” label quickly became industry shorthand for any non-standardized, custom-built option contract.

These options often require complex mathematical models for pricing, as their payouts depend on multiple factors or conditions. Their name also suggests a higher level of risk and sophistication, which appeals to certain market participants seeking advanced solutions.

How Do Exotic Options Work?

Exotic options work by introducing extra features or conditions into the basic option framework. These features might include barriers, averaging, or multi-asset dependencies, among others.

Some payoffs depend on whether the underlying asset hits a certain price (barrier options), while others use the average price over a period (Asian options) or the maximum/minimum price achieved (lookback options).

Pricing these options requires advanced quantitative techniques, often using Monte Carlo simulations or partial differential equations. Their workings are tailored to suit the needs of sophisticated clients, such as multinational corporations, hedge funds, and investment banks.

What Are the Types of Exotic Options?

There are 14 main types of exotic options, each catering to specific financial needs and market conditions. These include Barrier, Asian, Binary, Lookback, Quanto, Compound, Chooser, Bermuda, Basket, Extendible, Spread, Shout, and Range Options.

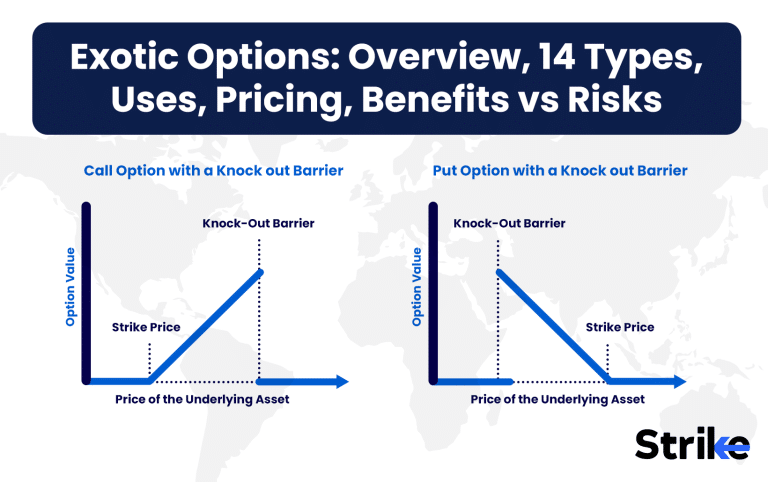

1. Barrier Options

Barrier options are derivatives whose payoff depends on whether the underlying asset crosses a pre-set barrier level. These options only become active (knock-in) or expire worthless (knock-out) if the asset price hits specific thresholds during the option’s life.

Payoff diagrams for barrier options look similar to standard options, but with an abrupt cut-off or activation point at the barrier. For example, if you buy a knock-out call on the Nifty with a strike at Rs. 20,000 and a barrier at Rs. 22,000, the option is nullified if Nifty touches Rs. 22,000 before expiry, regardless of where it ends up.

- Why use barrier options?

- Lower premiums than vanilla options due to conditional payouts.

- Useful in situations where you expect the underlying to remain within a certain range.

- Often used to hedge structured products or to bet on volatility without paying the full premium of a vanilla option.

Barrier options are common in currency and equity markets.

2. Asian Options

Asian options are those where the payoff is based on the average price of the underlying asset over a defined period, rather than the closing price at expiry. This feature reduces the impact of temporary price spikes or manipulation.

For example, an Asian call on TCS with a one-month averaging period pays out if the average price during the month exceeds the strike price. This can be useful for commodities or currencies that experience erratic daily movements.

- Why use Asian options?

- They offer protection against short-term volatility and end-of-period price manipulation.

- Lower premiums compared to vanilla options due to averaging effect.

- Often used by oil companies, airlines, and other firms exposed to average prices over time.

Asian options are especially popular in commodities and currency markets. In India, they help companies hedge against fluctuating average prices for key inputs, such as crude oil or foreign exchange rates.

3. Binary Options

Binary options are contracts that pay a fixed amount if a specific condition is met, and nothing otherwise. These options are also called “digital” or “all-or-nothing” options.

For example, a binary option on Reliance shares pays Rs. 1,000 if the price is above Rs. 2,500 at expiry, and zero otherwise. The payout is not related to how far the price moves above the strike—just whether the condition is met.

- Uses and risks:

- Attractive for traders seeking clear, simple bets on market moves.

- High risk of loss; binary options are often criticized for their resemblance to gambling.

- Banned or heavily regulated in many countries due to fraud and investor protection concerns.

Despite the controversy, binary options are still traded in some OTC markets and are occasionally used by professional traders to express short-term market views.

4. Lookback Options

Lookback options allow the holder to “look back” and choose the optimal price (minimum or maximum) of the underlying asset during the option’s life for payoff purposes. This feature maximizes the holder’s potential profit.

For instance, a lookback call on Infosys pays out based on the lowest price the stock traded during the option’s life, minus the strike price, providing the best possible outcome for the buyer.

- Why use lookback options?

- Extremely valuable in volatile markets, as they guarantee the best entry or exit price.

- Useful for hedging when the timing of peak or trough prices is uncertain.

- More expensive than standard options due to the favorable payout structure.

Lookback options are rare in retail markets but are sometimes used by institutional investors for hedging volatile exposures.

5. Quanto Options

Quanto options are those where the underlying asset is denominated in one currency, but the payoff is made in another currency at a fixed exchange rate. This eliminates the currency risk for the holder.

For example, an Indian investor buys a quanto call on the S&P 500, but the payoff is converted to Rs. at a pre-agreed USD/INR rate, avoiding uncertainty from forex fluctuations.

- Benefits and uses:

- Allows investors to take foreign market exposure without worrying about currency moves.

- Common with multinational firms managing international portfolios or global supply chains.

- Useful for hedging cross-currency risks in international contracts.

Quantos are often used in structured products and have become popular in Asian and European markets, especially for equity and commodity exposures.

6. Compound Options

Compound options are options that grant the right to buy or sell another option, rather than the underlying asset itself. They are, essentially, options on options.

A typical use case: a company may buy a call on a put option for crude oil, giving it the right to buy protection only if oil prices become volatile.

- Why use compound options?

- Useful when the timing of hedging needs is uncertain.

- Provides flexibility to secure options in the future, at pre-determined terms.

- Often used in interest rate and currency markets, especially for large corporate transactions.

Compound options are priced using complex models, as they involve multiple layers of optionality and risk.

7. Chooser Options

Chooser options give the holder the right to decide, after a certain period, whether the option will be a call or a put. This is valuable in unpredictable markets.

For example, an investor purchases a chooser option on HDFC Bank shares, deciding after three months whether to make it a call or put, depending on market direction.

- Why use chooser options?

- Maximum flexibility for hedging or speculation.

- Useful when the market view is unclear at the time of purchase.

- Higher premiums than standard options due to the choice feature.

Chooser options are rare but can be found in OTC markets for specialized hedging needs.

8. Bermuda Options

Bermuda options permit exercise on specific dates (such as monthly or quarterly) during the life of the option, not just at expiry. They combine features of American and European options.

A Bermuda call on SBI shares, for example, is exercisable only on quarterly dates before expiry, offering flexibility at lower cost than an American option.

- Why use Bermuda options?

- Lower premiums than American options, but more flexibility than European options.

- Popular for structured products, callable bonds, and interest rate derivatives.

- Useful when aligning exercise dates with corporate events or financial reporting cycles.

Bermuda options are widely used by banks and corporates for managing structured risks.

10. Basket Options

Basket options are contracts based on the performance of a group (basket) of underlying assets, rather than just one. The payoff depends on the average or weighted return of the assets in the basket.

For example, a basket option on Nifty IT stocks pays based on the average return of companies like Infosys, TCS, and HCL Tech.

- Why use basket options?

- Diversifies risk across multiple assets.

- Useful for sectoral or thematic bets without buying multiple options.

- Common in equity, commodity, and currency markets.

According to industry data, basket options are used by over 40% of institutional investors for portfolio-level hedging.

11. Extendible Options

Extendible options allow the holder to extend the maturity of the option by paying an extra premium at a specified date. This feature is particularly useful when market trends are unclear as expiry nears.

For instance, if an investor holds an extendible call on Maruti shares and the stock is near the strike at expiry, they can extend the option for another month by paying a small fee.

- Why use extendible options?

- Offers time flexibility to benefit from ongoing trends.

- Useful for hedging exposures that might persist longer than expected.

- Higher premiums compared to standard options but valuable for uncertain markets.

Extendible options are commonly used by commodity traders and corporations managing long-term risk.

12. Spread Options

Spread options are contracts where the payoff is determined by the difference (spread) between the prices of two assets. These are popular in energy, commodity, and currency markets.

For example, a spread option on Brent and WTI crude oil pays based on the difference in their prices at expiry.

- Why use spread options?

- Hedge against price differentials between related assets.

- Useful for arbitrage and risk management strategies.

- Often used by refiners, airlines, and commodity traders.

Spread options allow sophisticated strategies and are a staple in the risk management toolkit of global firms.

13. Shout Options

Shout options let the holder “lock in” a profit at any one point before expiry and still benefit if the underlying moves further in their favor. The holder “shouts” once, fixing a minimum payoff.

For example, if you hold a shout call on Tata Motors and the price spikes mid-way, you can lock in the gain. If the stock rises further, you receive the higher payoff; if it falls, you still get the locked-in amount.

- Why use shout options?

- Provides certainty on minimum returns while allowing for upside.

- Useful in highly uncertain or volatile markets.

- Premiums are higher due to the embedded guarantee.

Shout options are rare in retail markets but are sometimes used by institutions for structured payouts.

14. Range Options

Range options pay out if the underlying asset remains within a predefined price range during a set period. If the price leaves the range, the option expires worthless or pays less.

For instance, a range option on the USD/INR pays a fixed amount if the exchange rate stays between Rs. 82 and Rs. 84 for one month.

- Why use range options?

- Useful for hedging or speculating on low volatility.

- Suitable for earning income in stable markets.

- Lower premiums than options betting on big moves.

Range options are commonly used in currency markets, especially when volatility is expected to remain low.

As with any advanced derivative, thorough due diligence, robust pricing models, and careful risk assessment are essential before using exotic options in any portfolio or hedging strategy.

Who Uses Exotic Options and Why?

Exotic options are primarily used by banks, financial institutions, exporters/importers, hedge funds, and large corporations to manage complex risks and achieve tailored investment goals. These market participants require more flexibility and customization than standard options provide.

Banks and financial institutions utilize exotic options to structure products for clients, hedge proprietary portfolios, or manage interest rate and currency risks. Exporters and importers employ them to protect against adverse currency movements, especially when revenues and expenses are denominated in different currencies.

Hedge funds execute structured strategies using exotic options to gain exposure to volatility, correlation, or specific market events that standard options do not address efficiently. Corporates lock in cash flows or optimize financing costs under certain conditions, such as using barrier options or range accruals to manage their balance sheets.

Where Are Exotic Options Traded?

Exotic options are traded mainly in the over-the-counter (OTC) markets, rather than on formal exchanges. This OTC environment allows for the high degree of customization that these instruments require.

Financial institutions, corporations, and hedge funds negotiate these contracts directly with counterparties, often through large banks or brokers. Most exotic options are not standardized enough for exchange trading, which limits their liquidity but provides flexibility on terms, settlement, and underlying variables.

Listed exotic options exist but are rare, as exchanges focus on standard, high-volume products. The OTC market for exotics is substantial: According to the Bank for International Settlements, OTC derivatives notional outstanding exceeded $600 trillion globally in 2023, with exotics a significant subset.

How Are Exotic Options Priced?

Pricing exotic options requires advanced mathematical models, such as Monte Carlo simulations, binomial trees, or finite difference methods. These tools handle path-dependent payoffs and multiple underlying assets more effectively than the traditional Black-Scholes formula.

Monte Carlo simulations model thousands of potential future price paths, making them suitable for options with complex features like averaging or barriers. Binomial tree methods offer flexibility for early exercise and multiple event scenarios by constructing a lattice of possible asset prices and option values.

Finite difference methods solve partial differential equations that describe the option’s value evolution. These approaches accommodate the intricate boundary conditions of exotic contracts. Implied volatility and correlation between assets are also crucial inputs, as small changes significantly impact the calculated price.

What Are the Benefits of Exotic Options?

Exotic options offer bespoke risk management and investment solutions, enabling users to precisely match their hedging or speculative needs. Their flexibility allows for innovative payout structures and exposures not possible with vanilla options.

Some exotics provide lower premiums than similar vanilla options, especially those with knock-in or range-limited features. For example, a knock-in option costs less because it only becomes active under certain market conditions, reducing upfront costs.

Exotic options are efficient tools for hedging non-standard exposures, such as foreign currency revenues, commodity baskets, or path-dependent risks. They allow users to target outcomes, manage volatility, or optimize returns in ways tailored to their financial situation.

Customization also means that companies and institutions can design options to fit regulatory, accounting, or operational constraints. As a result, exotics are essential in sectors like banking, energy, and global trade, where standard contracts do not suffice.

What Are the Risks of Exotic Options?

Exotic options expose users to significant risks, including complex payoff structures, lower liquidity, and pricing difficulties. Their complexity makes it harder for investors to fully understand how the option will behave in different market scenarios.

Lower liquidity is a common problem, as most exotics are traded OTC and not on exchanges. This limits the ability to unwind positions easily and can result in wider bid-ask spreads or unfavorable exit prices.

Valuing exotics demands advanced quantitative models, and incorrect assumptions or inputs may lead to mispricing and unexpected losses. Counterparty risk is also higher, as settlement depends on the financial health of the OTC dealer rather than a central clearinghouse.

Transparency is reduced compared to exchange-traded options, making it difficult to benchmark pricing or assess fair value. In summary, these risks require sophisticated monitoring, robust internal controls, and expert oversight.

What Is the Difference Between Exotic and Vanilla Options?

Exotic options differ from vanilla options in structure, customization, risk, and market use. The table below summarizes the key differences.

| Feature | Vanilla Options | Exotic Options |

| Structure | Standard calls and puts | Customized, complex payoffs |

| Trading Venue | Mostly on exchanges | Primarily OTC |

| Liquidity | High | Low to moderate |

| Pricing Model | Black-Scholes and variants | Advanced models (Monte Carlo, etc.) |

| Transparency | High | Lower |

| Use Case | Simple hedging/speculation | Tailored risk management/strategies |

| Counterparty Risk | Low (cleared) | Higher (OTC bilateral contracts) |

| Accessibility | Suitable for all investors | Mainly for institutions/corporates |

Vanilla options suit most retail investors and straightforward hedging. Exotic options address complex exposures and are mainly used by sophisticated market participants.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 48")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 49")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 50")

: Overview, 10 Types of Indicators, Settings for Different Markets 53")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 54")

No Comments Yet.