The short iron butterfly is a limited profit and limited risk options trading strategy used when expecting low volatility in the underlying asset. The short iron butterfly involves selling a call spread and puts spread sharing the same center strike price.

The short iron butterfly benefits from neutral trading and a low volatility environment. The closer the asset remains to the center strike by expiration, the higher the profit. It aims to capture time decay, and IV crushes around the middle strike target.

This strategy is used to collect premium income from the rangebound movement forecast. It defines risk while profiting from stagnating price action. However, the short iron butterfly loses money from a significant breakout in either direction. Proper position sizing is key to managing the defined risk.

What is a Short Iron Butterfly?

A short iron butterfly, also known as an ironfly, is a limited risk, limited profit options trading strategy. It involves simultaneously selling a put option and a call option with the same expiration date and strike price while also buying a put with a lower strike and a call with a higher strike. This creates a rangebound strategy with defined maximum profit, maximum loss, and break-even points.

The short iron butterfly strategy aims to profit from the stock price staying between the lower and higher strike prices at expiration. The maximum profit is achieved if the stock price finishes right at the short strike. The maximum potential profit is equal to the net credit received when opening the iron butterfly. The maximum loss occurs if the stock price finishes outside the wings (below the lower put strike or above the higher call strike) at expiration. In this case, the maximum loss is equal to the difference between the wing strikes minus the initial credit received.

A short iron butterfly has a net credit position, meaning the trader collects a premium when opening the trade. The maximum profit at expiration is equal to this initial credit received if the stock price finishes between the lower and higher strike prices. The breakeven points occur at the wing strikes (X – Y and X + Z). Below the lower breakeven, the trader starts losing money until the maximum loss is reached. Above the higher breakeven, the trader also starts losing until the maximum loss.

While implementing a short iron butterfly strategy, the ideal situation is low volatility rangebound stock price. The maximum profit potential occurs if the stock finishes right at the sold strikes. Higher volatility or a strongly trending stock price puts more risk on the short options at the body. Monitoring volatility and price action is crucial to stay within the expected range.

A key risk lies in the unlimited downside beyond the sold strikes. Selling the naked puts and calls exposes the trader to potentially uncapped losses if the stock gaps up or down. Buying the out-of-the-money wings provides protection but also incurs a cost. The wings define and limit the maximum loss point.

Entering the short iron butterfly involves paying a net debit upfront, which is the maximum risk. This is where the trade gets to loss. However, the profit potential is defined and capped at the credit received for the body options. The reward is limited even as more risk is taken.

Time decay aids the short iron butterfly trader as the sold options lose extrinsic value approaching expiration. However, time decay also erodes the value of the long-wing options purchased. The ideal outcome is expiration with the stock finishing between the sold strikes.

While unlikely, early assignment is a possibility before expiration, especially on the short put. The traders have to close the position before realizing the full profit potential if exercised early. Avoiding early assignments is critical.

What is the importance of the Short Iron Butterfly in Options Trading?

The short iron butterfly is one of the most popular and versatile options trading strategies. Its importance stems from its well-defined risk-reward parameters, flexibility across any underlying asset, and ability to profit in rangebound or neutral markets. The short iron butterfly has stood the test of time and remains a foundational component of options spreads trading.

By clearly defining maximum profit, maximum loss, and break-even points, the short iron butterfly offers traders a high-probability strategy with quantifiable outcomes. The maximum profit is limited to the initial net credit received when opening the position. The maximum loss is defined as the difference between the wing strikes minus the initial credit. And the break-even occurs right at the wing strikes. This transparency of outcomes allows traders to precisely calculate potential risk-reward before entering a trade.

The short iron butterfly is viable for implementation on any underlying asset that offers options, including stocks, ETFs, indices, commodities, or currencies. This versatility across all liquid underlying gives it widespread applicability and utility in an options trader’s playbook. The strategy mechanics remain identical no matter the underlying asset. This allows traders to deploy the short iron butterfly in a portfolio approach across various asset classes.

Unlike other strategies like the short Straddle or short strangle, which rely on volatility expansion, the short iron butterfly aims to profit from neutral and rangebound markets. It performs optimally when the underlying trades within the wings at expiration. By selling options at the body and buying wings, the short iron butterfly has a positive theta, which means it benefits from time decay as expiration approaches. This strategic advantage makes it ideal for slow, directionless markets.

The short iron butterfly relies on precision strike selection to match the market forecast. Traders carefully choose strikes equidistant from the current price to match their outlook. This customizability provides flexibility to adapt the strategy across any market condition. Short iron butterflies are traded directionally with the body above or below the current price or neutrally at the money.

Defined risk profiles are critical for money management and capital preservation when trading options. Unlike naked short options, which have unlimited risk, the wings on the short iron butterfly strictly define loss. This helps prevent account blowups and allows position sizing using the exact maximum loss.

While the wings create a defined risk vertical spread, the short options at the body of the iron butterfly lower the cost basis. This means the position has a net credit, reducing margin requirements and tying up less capital. The reduced cost basis also boosts the potential return on investment.

For active options traders, managing winning trades is just as crucial as managing losing ones. The short iron butterfly offers clear technical signals for early exits to lock in profits or close out for a loss. It signals an optimal exit point if the underlying reaches either wing strike,

Any adjustments or early exits due to a change in forecast benefit from the clarity of the breakeven points. The trader knows precisely at what underlying price the position transitions between a gain or a loss.

While the short iron butterfly has no dividend risk since it is a net credit trade, early assignment on the short options remains a possibility. However, the likelihood is extremely low given the wings reduce extrinsic value and the position would most often be closed out well before expiration.

The probability of profit for a short iron butterfly is quite high when the strikes match the neutral forecast. This probabilistic edge gives the trade positive expectancy, especially after factoring in the credit received. A key analytical step is assessing the theoretical odds of success when trading any strategy.

As a credit spread, the short iron butterfly is useful for earning income from options premium decay. In slow, sideways markets with elevated implied volatility, traders repeatedly collect premiums using short iron butterflies. This income generation is consistent with strategies like covered calls.

The viability across all liquid options contracts makes the short iron butterfly a highly diversified trade. Traders implement the strategy on a variety of underlying rather than concentrating risk on just a single stock or ETF, like with a typical long vertical spread.

While the wings do incur an upfront debit cost, this defined risk mitigation is well worth the expense for prudent traders. The wings strictly cap the maximum loss, allowing traders to survive large adverse stock moves. For active portfolio managers, staying in power and managing drawdowns is essential.

How does Short Iron Butterfly work?

A short iron butterfly is a limited risk, limited reward options trading strategy. It involves the combination of a bear call spread and a bull put spread, with the spreads converging at a middle strike price. The mechanics involve selling an at-the-money call while buying an out-of-the-money call and putting it into creating wings.

To implement a short iron butterfly, a trader would execute four simultaneous legs as follows.

1. Sell a call option at strike X (the body strike).

2. Buy a further out-of-the-money call at strike X + Y (the wing strike).

3. Sell a put option at strike X (the body strike, same as call strike).

4. Buy a further out-of-the-money put at strike X – Z (the lower wing strike).

The distance between the body strike X and the wing strikes determines the width or risk parameters of the iron butterfly. A narrow wing spread indicates a smaller maximum loss but also caps the maximum profit potential.

By selling the body call and put, the trader collects premium income in the form of credits on both legs. This establishes a net credit for the overall iron butterfly position. The maximum potential profit is capped at this initial net credit amount.

The wing call and put are purchased to define the risk on both sides of the body strikes. These debit spreads create an upper and lower breakeven point beyond which losses accumulate. The total loss between the wing strikes is reduced by the initial credit received.

An iron butterfly trader is anticipating the stock will remain between the wing strikes at expiration. Both body options expire worthless, and the trader keeps the full credit if the stock finishes within this price range. The wings expire at intrinsic value, offsetting each other.

The put spread starts losing money penny for penny with a further downside if the stock price moves below the put wing strike at expiration. But the call spread remains profitable by the initial credit amount, offsetting some losses. The total loss continues until the maximum is defined by the width of the wings.

On the upside above the call wing strike, the call spread starts accumulating, increasing losses. But the put spread retains its initial value, again offsetting some downside. Losses continue until they reach the fixed maximum loss point.

The breakeven points occur at the wing strikes. Below the put wing strike, total losses overcome the initial credit, and the position enters losing territory. Above the call wing strike, the same flip from profit to loss happens.

The trader should collect enough credit on the body strikes to pay for the wing debit spreads when establishing an iron butterfly. This ensures entering with a net credit, limiting capital requirements. The wings are typically placed equidistant from the body strike to create symmetry.

As expiration approaches, if it appears likely the stock will settle outside the wings, the trader exits the position early to lock in a smaller loss compared to holding until expiration day. An early exit around a breakeven point is prudent if the stock is trending toward a wing strike.

To close out a short iron butterfly, the trader would buy back the short calls and put them in the body. And they would sell the long wing call and put options. This reverses all the original transactions, flattening the position.

The maximum profit, maximum loss, and probabilistic edge rely heavily on getting the wing strike prices right relative to the body strikes. Careful position management is required to adjust the wings if the forecast changes. This involves rolling the position or converting it to another strategy.

The ideal conditions for profitability with a short iron butterfly include low implied volatility, neutral technicals, a range-bound stock price, and time decay working in your favor. Losses start accumulating if volatility rises or the stock trends are outside the wings.

How does Short Iron Butterfly differ from Butterfly Spread?

The short iron butterfly is a neutral options strategy constructed using both call and put credit spreads. It differs significantly from long butterfly spreads such as the long iron butterfly, long put butterfly, and reverse iron butterfly.

The key difference between long and short butterflies is the net debit versus net credit positions. A short iron butterfly involves selling options at the body to collect premium income upfront. This establishes a net credit position with a capped maximum profit potential. Long butterflies like the long iron butterfly require an initial net debit, limiting the maximum potential profit.

With a short iron butterfly, the maximum profit equals the initial net credit received from the body call and put sales. For long butterflies, the maximum profit is the difference between the wing strikes minus the initial debit. Short butterflies have a higher probability of profit but limited upside.

The short iron butterfly profits from time decay as the sold option premium declines ahead of expiration. Long Butterflies aim to profit from the expansion of the body options. These opposing Greeks mean their ideal trading environments also differ.

The short iron butterfly relies on low volatility and neutral technical sentiment to profit. The body options expire worthless in a range-bound market. Long butterflies perform better with increasing volatility as the body options become more valuable.

While both strategies exhibit limited risk, short butterflies have a clearly defined maximum loss. With long butterflies, early assignment of the short options poses risks. Short butterflies avoid any early assignment risk.

The breakeven points differ due to the net debit or credit positions. For short iron butterflies, the breakevens are right at the wing strikes. With long butterflies, the breakevens equate to the initial debit paid. This wider range makes short butterflies preferable.

Traders further customize short iron butterflies by adjusting the distance between the body and wing strikes when it comes to construction. This allows asymmetric risk profiles favoring a directional bias. Long butterflies tend to utilize evenly spaced strikes.

To close a short iron butterfly, the trader simply buys back the calls and puts sold at the body while selling the purchased wing options. Long butterflies require buying back the body options and selling the wings. The exit mechanics mirror the original entry.

The long put butterfly involves selling two puts at a middle strike while buying one lower strike put and one higher strike put. This long-put butterfly requires a net debit. The short iron butterfly sells a put and call at the same middle strike to create a net credit.

With the long-put butterfly, the maximum profit is capped between the wing strikes. The short iron butterfly’s maximum profit equals the initial credit. Both strategies exhibit limited risk, but the short iron butterfly has clearly defined max loss points.

While they share similar breakeven points, the short iron butterfly performs better in low-volatility environments. Long-put butterflies need rising volatility to profit from expanding body puts. Volatility contractions hurt long-put butterflies but aid short-iron butterflies.

The reverse iron butterfly contains a long iron butterfly paired with a short iron butterfly one strike higher. This further complicates the structure compared to a simple short iron butterfly.

The reverse iron butterfly requires establishing two separate iron butterflies at different strike prices. The short iron butterfly just needs one body and two wing strikes. This makes the short iron butterfly easier to analyze and manage.

With two iron butterflies, the reverse structure has twice the commission costs and margin requirements. The short iron butterfly allows taking in a net credit upfront with lower costs.

How commonly do traders use the Short Iron Butterfly strategy?

The short iron butterfly is a very commonly implemented options strategy among experienced retail and institutional traders. Its popularity stems from its well-defined risk-reward parameters, flexibility across any underlying asset, and ability to profit from neutral market conditions. Both long-term investors and short-term speculators regularly utilize the short-iron butterfly.

Among option traders, the short iron butterfly is considered one of the most basic strategies and is often one of the first credit spreads learned. It is frequently implemented by traders looking to generate consistent income from options premium decay. The initial net credit collected provides an income stream with capped downside risk.

One of the main advantages of the short iron butterfly is its viability across any liquid underlying. It is basically traded on stocks, ETFs, indices, commodities, forex and more. This makes it a widely diversified strategy. Traders implement short iron butterflies to speculate on everything from individual stocks to the S&P 500 index.

The clearly defined risk metrics allow even novice traders to understand the strategy and maximum loss. This transparency provides appeal to new traders as both an income and high probability play. More advanced traders take advantage of the versatility to adapt the strikes and customize as needed.

Trend traders implement short iron butterflies to capitalize on ranging, choppy markets. The strategy benefits from neutral price action and lacks momentum. Short iron butterflies become advantageous when the market enters consolidation after a prolonged trend.

Portfolio managers use short iron butterflies to hedge and generate incremental yield. They add short iron butterflies across multiple uncorrelated underlying to diversify risk. This provides a steady income analogous to covered call writing.

Institutional traders rely on short iron butterflies to exploit perceived mispricings in options. Short iron butterflies allow capturing yield if implied volatility offers rich premiums. Volatility compression benefits the strategy.

Some technical traders exclusively implement short iron butterflies in combination with chart patterns. For example, they will enter short iron butterflies when a stock breaks out of a Bollinger Band squeeze or triangle consolidation pattern, anticipating rangebound price action to follow.

Only advanced options traders utilize more complex strategies like the double short iron butterfly or short iron condor. The majority stick with basic single-leg short iron butterflies, which provide the best risk-defined parameters.

The prevalence of the short iron butterfly on public options exchanges provides ample liquidity when entering and exiting positions. The volume and open interest on the individual options legs ensure easy order fills.

While defined risk strategies like short iron butterflies limit profit upside compared to speculation, most prudent traders favor downside protection over unlimited reward propositions. This helps explain the popularity of short iron butterflies.

How to Create a Short Iron Butterfly?

The short iron butterfly is a limited-risk, neutral options strategy that aims to profit from low volatility and a range-bound stock price. To properly construct a short iron butterfly, these 12 steps are followed.

Define Outlook: Determine your market outlook and suitable underlying asset. The short iron butterfly performs best when you expect the stock to trade within a defined price range until options expiration.

Pick Expiration: Choose a suitable option expiration date. Shorter expirations take advantage of faster time decay but require tighter wings. Longer expirations allow wider wings.

Select Strikes: Identify the strike prices to use for the body and wings. The body strikes should be as close to at-the-money as possible. The wing strikes equidistant from the body strike create symmetry. Adjust wing width based on risk tolerance.

Analyse Credits: Sell the body call and put options, then buy the wing options. Compare potential credit received to the width of the wings to ensure adequate compensation for the defined risk taken. Wider wings and greater time value yield more income.

Evaluate Risks: Calculate maximum profit (equal to initial credit) and maximum loss (difference between wing strikes minus credit). Assess upside and downside breakevens where the trade transitions between profit and loss. Measure the probability of profit based on wing width.

Place Trades: Execute the four legs simultaneously to open the short iron butterfly, which sells body call, buys wing call, sells body put, and buys wing put. Use a net credit order to ensure entering at an optimal price. Adjust wing prices as needed to get filled.

Monitor Position: Once filled, actively manage the short iron butterfly through expiration. Track the stock price relative to the breakevens. Make adjustments if the forecast changes. Exit early if max loss is likely.

Manage Risk: Defined wing risk, low correlations across underlying, position sizing, and avoiding overcrowded trades. Use stops at breakevens or technical levels. Hedge directional bias with additional options.

Address Assignment: Though unlikely, early assignment occurs on short options. Understand brokerage rules for exercise and dividends. Close positions before ex-dividend dates.

Time the Exit: As expiration approaches, prepare to exit. Let position expire for full profit if stock settles right at body striker. Exit early to avoid max loss if finishing beyond breakevens. Leg out judiciously.

Close Positions: Buyback short body call and put options, selling the long wing options to flatten the trade. Net profit or loss equals the maximum credit received less debit paid to close position early.

Review Results: Analyze P&L relative to objectives, adjust position sizing, and risk parameters going forward. Optimise strike selection, expiration dates, wing width, underlying assets, and sector allocation.

When to enter a Short Iron Butterfly strategy?

The short iron butterfly options strategy is a limited profit, limited risk options trading strategy. It is used when the options trader expects low volatility in the underlying asset during the life of the options contracts. The ideal circumstance to implement a short iron butterfly is when the underlying asset is trading in a tight trading range, and volatility is expected to remain low through options expiration.

The short iron butterfly strategy involves selling a lower strike out-of-the-money put, buying an at-the-money put, selling an at-the-money call, and buying a higher strike out-of-the-money call. The distance between the sold put strike and sold call strike is the same. Credit is taken in to enter the trade, which represents the maximum potential profit if the underlying stock closes right at the short strike at expiration.

The 5 signals to look for to implement a short iron butterfly strategy are as follows.

- The underlying stock is consolidating in a tight trading range and has been for some time. This indicates a period of low volatility as the stock oscillates in a range rather than exhibiting a strong trend.

- Implied volatility is low relative to historical levels. Low IV suggests options are relatively cheap, allowing the short options sold to collect more premium.

- Upcoming events like earnings announcements that could increase volatility are not on the horizon before options expiration. Avoid times when volatility could spike higher.

- Minimal news or events could send the stock strongly in either direction in the near term. The tighter the recent trading range, the better.

- Technical indicators like Bollinger Bands and Average True Range show that the stock is not making large moves, and volatility is contracted.

The underlying stock breaks out of its trading range, and declines below the sold put strike or rises above the sold call strike prior to expiration if the short iron butterfly is entered too early when volatility remains relatively high. This could result in losses on the short options. Alternatively, if both short strikes are tested, resulting in assignment of stock, the trader is then exposed to overnight gap risk.

Entering the trade too late after the stock has settled into very low volatility trading will reduce the credit received. With less premium collected, the reward relative to risk becomes less attractive. The trader generally wants to implement the short iron butterfly after volatility has contracted, but the premium remains fairly high.

When to exit a Short Iron Butterfly strategy?

Timing the exit is crucial when trading short iron butterflies to maximize gains or minimize losses.

Critical short iron butterfly exit signals include the stock price breaching the wings indicating max loss risk, rapid IV contractions presenting early profit capture opportunities, sentiment shifts negating the neutral outlook and requiring position adaptation, upcoming binary events creating volatility risks warranting closure, breakouts above resistance or below support signaling trend start threats, minimal remaining time value limiting further gains, achieving 50-75% of max profit allowing prudent early exits, and the stock approaching upper or lower break-even points acting as clear profit take or stop loss trigger levels.

Consequences of early exits

Exiting a short iron butterfly prematurely caps realized gains if the stock ultimately finishes within the wings at expiration. Holding the position through maturity could have extracted maximum time decay gains. Prematurely closing the trade forfeits additional profit potential.

Early exits also require paying the bid/ask spread to close out the position. The transaction costs incurred from the spread increase overall costs compared to holding the short iron butterfly through expiration, where time decay expires the options.

Additionally, misreading temporary price movements or overreacting to normal volatility fluctuations runs the risk of warrantlessly closing out a short iron butterfly trade that reverses direction favorably later. With patience, what appears to be a losing position still expires profitably if the stock settles between the wings.

Consequences of late exits

Delaying the exit or holding a challenged short iron butterfly too long risks incurring substantial losses from the stock moving well beyond either wing strike before finally closing the position. The slow response allows the maximum loss to be fully realized.

Late exits also force the trader to chase unfavorable exit prices in a rushed panic to liquidate the position as expiration nears. The urgency leads to hasty trading decisions that magnify slippage impact costs.

Additionally, holding short iron butterflies into the final days before expiration significantly increases assignment risk if the short call or put options are in-the-money. Taking assignments early results in unwanted stock positions.

What is the maximum loss for Short Iron Butterflies?

With a short iron butterfly, maximum loss occurs when the underlying stock price closes below the lower put wing strike or above the higher call wing strike at expiration. The maximum loss is quantified and strictly defined based on the strikes chosen when constructing the iron butterfly.

The maximum loss is calculated as stated below.

Max Loss = Strike Price of Long Put – Strike Price of Short Put – Net Premium Received

Or

Max Loss = Strike Price of Long Call – Strike Price of Short Call – Net Premium Received

Where,

Long put = The out-of-the-money put option purchased for the lower wing

Short put = The at-the-money put option sold for the body position

Long call = The out-of-the-money call option purchased for the higher wing

Short call = The at-the-money call option sold for the body position

The further apart the wing strike prices are from the body strikes, the greater the maximum loss. The net credit received from the body call and put sales reduces the total maximum loss. But this credit income is capped.

For example, consider a short iron butterfly constructed as follows.

Long 100 Put at strike Rs.45

Short 100 Put at strike Rs.50

Short 100 Call at strike Rs.50

Long 100 Call at strike Rs.55

Let this be a position entered for a net credit of Rs.2 per contract.

The maximum loss on the put side is as follows.

Strike of Long Put: Rs.45

Minus Strike of Short Put: Rs.50

Minus Net Premium: Rs.2 credit

Equals Max Loss: Rs.3 loss per contract

The maximum loss on the call side is as follows.

Strike of Long Call: Rs.55

Minus Strike of Short Call: Rs.50

Minus Net Premium: Rs.2 credit

Equals Max Loss: Rs.3 loss per contract

So, the total maximum loss is Rs.3 per contract, incurred if the stock finishes below Rs.45 or above Rs.55 at expiration.

The maximum loss occurs because the long-wing options expire worthless while the short-body options are exercised or assigned at a loss. The wings expire worthless and provide no protection outside of their strikes.

In this example, the maximum loss represents the distance between the wing strikes of Rs.5, reduced by the Rs.2 credit income collected when initiating the trade. Wider wing spreads lead to larger potential losses but also allow more premium income.

It is important to carefully calculate maximum loss when constructing the short iron butterfly, so you know the full risk being taken before entering the trade. The maximum loss calculation quantifies the exact downside and helps determine appropriate trade sizing and risk management parameters.

What is the maximum profit for Short Iron Butterflies?

With a short iron butterfly, the maximum profit is achieved when the underlying stock price closes right at the body strike prices of the sold call and put options on the expiration date. The maximum profit is strictly limited to the initial net credit received when opening the short iron butterfly trade.

The maximum profit is calculated as stated below.

Max Profit = Net Premium Received

Where,

Net Premium Received = Credit from Short Call – Debit from Long Call + Credit from Short Put – Debit from Long Put

This net credit amount represents the maximum potential profit on the short iron butterfly because the body call and put options will expire completely worthless if the stock finishes precisely at their strike price at expiration.

For example, consider a short iron butterfly set up as follows.

Short 1 Call at Rs.50 strike

Long 1 Call at Rs.55 strike for Rs.2 debit

Short 1 Put at Rs.50 strike

Long 1 Put at Rs.45 strike for Rs.1 debit

Let the initial net credit received is Rs.3 per contract. Then, the maximum profit would simply be as stated below.

Max Profit = Net Premium Received

= Rs.3 credit

The Rs.3 credit consists of the following.

– Rs.2 credit from the Rs.50 short call

– Rs.2 debit paid for the Rs.55 long call

– Rs.1 credit from the Rs.50 shot put

– Rs.1 debit paid for the Rs.45 long put

Both the short Rs.50 call and put expire worthless, while the Rs.55 and Rs.45 wing options expire with no intrinsic value if, at expiration, the stock is exactly at Rs.50. This results in the maximum profit being realized of Rs.3 per contract.

The five key things to remember are as follows.

- Maximum profit is always capped at the net credit received upfront when initiating the short iron butterfly.

- It is achieved when the stock closes precisely at the strike price of the short call and puts it at expiration.

- No further profit is possible beyond the initial credit amount.

- The wing spreads pay for themselves and does not add to potential profit.

- Time decay and volatility contraction cannot increase profits above this limit.

Carefully calculating the maximum profit when constructing the short iron butterfly allows traders to quantify the capped upside. By collecting credits upfront, potential gains are strictly limited. The wings serve only to define risk, not amplify returns. Understanding the maximum profit mechanics is vital to successfully trading short iron butterflies.

What is the most Appropriate market forecast for Short Iron Butterfly?

The most appropriate market forecast for successfully implementing a short iron butterfly strategy is a neutral outlook expecting minimal volatility, stability, and an underlying stock price that remains range-bound through options expiration. This forecast maximizes the probability of profit for the short iron butterfly structure and provides the ideal conditions for reaching maximum gain.

A neutral, range-bound forecast is optimal for short-iron butterflies because of 5 reasons.

Firstly, with the stock expected to trade between the wings, both the short call and short put positions will expire completely worthless at maturity. This allows the trader to retain the full premium income collected when initiating the call and put credit spreads. The out-of-the-money long wings will hold little to no intrinsic value.

Secondly, low volatility during the trade duration keeps extrinsic time value elevated in the options. This increases the premium income generated from the short call and put sales. More credit directly enhances the potential return.

Thirdly, minimal price movement allows the wings to maintain their full hedging value without being tested or breached prior to expiration. The wings will not need to buffer downside risk if volatility remains muted.

Fourthly, time decay accelerates into expiration, rapidly eroding the short options’ extrinsic value. This constant erosion amplifies gains for short iron butterflies as the trader pockets the credits upfront.

Finally, neutral or slightly bearish conditions keep early exercise risk negligible on the short call, with the stock finishing comfortably below the strike at maturity.

Suppose a neutral, stable forecast appears; traders will capitalize in different ways.

First, sell short-term out-of-the-money calls and puts to generate income, anticipating they will expire worthless. Also, purchase longer-term, farther out-of-the-money calls and puts to construct protective wings that limit maximum loss if the range breaks. Next, actively manage the overall iron butterfly as expiration nears, including early exits if the stock price threatens the wings. Additionally, consider legging into more iron butterflies at different strikes to increase income exposure to the stagnating outlook. Furthermore, be ready to swiftly adapt the structure if the forecast changes by exiting shorts or adjusting wings accordingly. Finally, focus trading on high implied volatility underlying where elevated extrinsic value provides ripe conditions for decay into expiration.

How does implied volatility affect the Short Iron Butterfly?

Implied volatility is a key factor affecting short-iron butterfly pricing, risk metrics, and profitability. Implied volatility represents the market’s expectations for future volatility priced into an option’s premium. Understanding IV behavior is crucial for successfully trading short iron butterflies.

Higher implied volatility is beneficial when initiating new short-iron butterfly positions. Elevated IV increases the premium value of the short call and puts options sold at the body strikes, boosting the net credit received for the trade. Higher premium income also allows wider separation of the wing strikes for the same credit, reducing cost basis while widening the profitable trading range. Additionally, the greater the IV, the larger the potential profits if the IV mean reverts lower by expiration as expected. Finally, increased IV raises the “cushion,” protecting the overall position from adverse price swings.

However, there are also risks from high IV levels. The wider wings increase the maximum loss if the stock price moves beyond the breakevens. The short strikes lose value slower if IV continues rising rather than falling as projected. Also, wider wings cost more capital to establish initially.

In contrast, lower implied volatility hurts new short iron butterflies by diminishing potential profit from smaller credits on the short call and put sales. With lower credits, the wing strikes must be set closer to the money, which narrows the profitable trading range. The wings also have less buffer before being tested, raising the odds of hitting maximum loss. Finally, lower IV offers less cushion for volatility expansion.

Yet lower IV also carries advantages, including reducing maximum loss by allowing cheaper wing options. Additionally, minimal extrinsic premium enables faster time decay. Finally, any increase in IV going forward benefits the short-body positions.

How do traders break even with Short Iron Butterflies?

With a short iron butterfly, there are two breakeven points that determine where the trade transitions between profit and loss. The breakevens occur at the strike prices of the out-of-the-money call and put options purchased as downside protection wings.

The breakeven points are calculated as stated below.

Lower Breakeven = Strike of Long Put

Higher Breakeven = Strike of Long Call

Where,

Long put = The out-of-the-money put bought as the lower wing

Long call = The out-of-the-money call bought as the higher wing

For example, consider a short iron butterfly constructed as the following.

Long 1 Put at Rs.45 strike

Short 1 Put at Rs.50 strike

Short 1 Call at Rs.50 strike

Long 1 Call at Rs.55 strike

Here, the breakevens would be as mentioned below.

Lower Breakeven = Rs.45 (the long put wing strike)

Higher Breakeven = Rs.55 (the long call wing strike)

At the breakeven points, the intrinsic value of the wings exactly offsets the premium income collected from the body short call and put sales. Below the put breakeven or above the call breakeven is where losses begin accruing.

The trader reaches the breakeven points in two scenarios.

Firstly, if the underlying is precisely at either wing, strike at expiration. The wings expire with an intrinsic value equal to the initial credit income, flattening the trade.

Secondly, if the position is closed out early when the underlying is at the wing strikes, buying back the shorts and selling the wings net zero profit or loss.

The breakevens create clear exit signals for the short iron butterfly position. Exiting is advised to avoid incurring maximum loss beyond those points if the stock price trends toward or reaches either breakeven before expiration.

The distance between the breakevens determines the range where the short iron butterfly retains the initial credit profit. This width depends on the strikes chosen for the wings when establishing the position. Wider wings increase the profitable range but also increase risk.

It is crucial to proactively manage the short iron butterfly around the breakeven points. The stock price must finish between the breakevens to earn the maximum profit if holding to expiration. The breakevens quantify where profits turn into losses on the trade.

How does Short Iron Butterfly strategy assignment risk occur?

With short iron butterflies, there is the risk of early assignment on the short call and options sold to collect premium income. Assignment causes the shorts to exercise early, forcing the trader to deliver or receive stock. This closes the options position before expiration.

Assignment risk mainly arises when the underlying goes deep in the money relative to the short strikes. The probability increases if the stock price rallies well above the call or declines far below the strike.

However, assignment risk is relatively minimal on short iron butterflies because the wings reduce extrinsic time value, discouraging early exercise. Also, the traders often close positions before expiration, avoiding final week assignment risks. The at-the-money body strikes require a significant price move for high early exercise odds. Utilizing an index or ETF underlying minimizes dividend-related assignment risks. And brokerage exercise thresholds minimize undue assignment.

Early assignment is generally neither good nor bad for short iron butterfly traders. The trader loses the remaining time value but nets the same intrinsic value regardless. The assignment only accelerates the closing part of the trade. The lost time value offsets reduced erosion on the long wings.

What is the impact of Time Decay on Short Iron Butterflies?

Time decay, or theta, has an overall positive impact on short iron butterfly positions. As time to expiration decreases, the time value priced into the short call and put options erodes, benefiting the short iron butterfly. However, time decay also gradually diminishes the value of the long-wing options.

Time decay has positive effects on short iron butterfly positions. As expiration approaches, the extrinsic premium of the short call and put decreases, lowering the cost to close the trade and increasing potential profit. Less time value also makes it more likely the shorts expire worthless for maximum profit. Rapid decay in the closing weeks accelerates gains since the collected premiums benefit from erosion.

However, time decay also has negative impacts. The extrinsic value of the long-wing options decreases, eroding their downside protection and hedging ability. Less time premium on the wings means smaller offsets to losses if the shorts go in the money. Time erosion lowers the range of profitable stock prices as breakevens converge. Rapid decay late in the trade reduces opportunities to adjust wings if the stock price moves against the position.

While time decay positively impacts the short call and put credits collected, it also deteriorates the value of the long-wing options. Traders must balance these dynamics and manage short iron butterflies more proactively as expiration approaches. The key is closing positions before time value erosion eliminates opportunities or exacerbates losses.

How does expiration risk affect the Short Iron Butterfly strategy’s gains and losses?

Expiration risk refers to the uncertainty of where the underlying stock price will be at the options expiration date relative to the short iron butterfly strikes. This directly impacts the realized profit or loss. Managing trades into expiration exposes short iron butterflies to adverse volatility and price moves.

The short iron butterfly has three distinct expiration risk scenarios traders must consider. First is the max profit zone, where both short calls and puts expire worthless if the stock finishes at the body strike price. This is the optimal outcome.

Second, are the max loss zones below the put wing strike or above the call wing strike? Here, the shorts get exercised while the wings provide no protection outside their strikes, incurring maximum loss. Avoiding these areas is key.

Third are the breakeven points, where the position reaches neutral if the stock lands precisely on either wing strike. Beyond the breakevens, losses accumulate as the stock price distances further from the body strikes.

As expiration nears, any sharp price swings or volatility expansion push the stock outside the profitable range between the breakevens, exposing short iron butterflies to sudden losses.

Holding positions into the final trading days also increases risks from reduced liquidity, volatility spikes, wider spreads, heightened assignment odds, and lack of reaction time to overnight gaps.

To mitigate expiration risks, prudent traders look to close short iron butterfly positions at least 2-3 weeks prior to final expiry rather than relying on arbitrary expiration prices. This buffer period allows seeking optimal early exits to lock in profits or minimize losses based on the risk-reward scenarios. Careful management of expiration is crucial for short-iron butterflies.

What is the importance of adjusting Short Iron Butterfly

The short iron butterfly options strategy is adjusted to defend against losses or lock in profits as market conditions change. Here are 10 effective adjustment techniques.

Rolling the Position: As expiration approaches, traders roll the entire iron butterfly outward in time to a later expiration date. This retains the structure while capturing additional credit from the new short options to offset losses or improve cost basis. Rolling defends the position longer.

Modifying Wing Strikes: The traders roll the wings further out of the money if the underlying price threatens to breach the wings. This widens the distance between the breakevens, delaying the max loss point. More room to withstand volatility is created.

Closing One Side: The trader closes that side of the iron butterfly, flattening the threatened body-wing pairing if the stock breaks through either wing. The other side is kept open. This isolates the directional risk while allowing the untested body-wing to potentially profit.

Resizing Contracts: Increasing or decreasing the number of contracts on either body-wing pairing reshapes the position to capitalize on directional bias. It weights exposure based on which side has greater profit potential from the stock’s movement.

Legging into Spreads: The trader closes one body-wing pairing and leaves the other side as a credit call or puts a vertical spread. This capitalizes fully on directional views instead of purely range-bound expectations.

Collaring With Protection: Purchasing additional out-of-the-money calls and putting around the wings collars against a breach while retaining range-bound profits. The long calls/puts hedge upside/downside exposure.

Synthesizing New Positions: Closing the challenged position and simultaneously establishing a new iron butterfly at improved strikes rolls risk out in time. It synthesizes a fresh position with a higher probability of profit.

Pricing the Adjustments: Monitoring time remaining is critical for judging effective adjustments. Changes require comparing debit or credit costs to optimize pricing.

Weighing Bidding: Buying back the bodies and selling new ones is one creative adjustment. The goal is to improve the risk-reward profile by customizing the structure.

Maintaining Discipline: Disciplined traders have pre-planned adjustment rules ready for different scenarios. Reacting methodically based on strategy helps remove emotion.

Why is Hedging a Short Iron Butterfly crucial in managing potential risks and losses

Hedging a short iron butterfly involves utilizing additional long or short options positions to help mitigate defined downside risk. Hedging allows traders to reduce maximum loss exposure and improve risk-adjusted returns.

Hedging short iron butterflies with additional long calls or puts protects against adverse price moves that threaten to breach the wings. The added options act as buffers to delay incurring maximum loss. This allows more time for the short strikes to expire worthless.

Incorporating hedges helps manage event risk around earnings reports or economic data by reducing volatility exposure on the short options. Unexpected news quickly erases short premium value, so hedges limit this downside.

Adding hedges allows utilizing wider wing spreads for the same amount of risk taken. This broadens the profitable trading range for the underlying asset. Wider wings also collect more premium income.

Hedging creates additional opportunities to adjust the overall trade structure by rolling, widening, or legging in and out of positions. The extra calls or puts provide structural flexibility.

It diversifies the risk beyond just the strict short iron butterfly P&L profile. Different combinations of options create non-correlated returns.

Hedged butterflies require less frequent monitoring and active management. The protection buffers allow holding through some adverse moves rather than overreacting.

Traders balance the cost of hedges versus the risk mitigation provided. Cheaper hedges reduce losses at lower costs but allow some risk. More expensive hedges provide insurance by eliminating most risks.

Hedging accommodates directional bias based on market outlook. Bears add more puts, while bulls incorporate additional calls to align with views and improve odds.

It prevents emotions-based trading around volatile events. Hedges enable adhering to trading plans and risk limits in turbulent times.

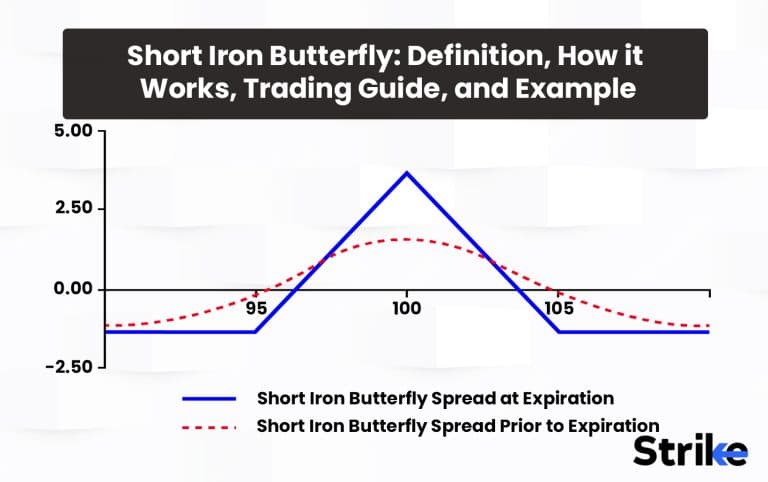

What is an example of a Short Iron Butterfly?

Let’s walk through an example short iron butterfly constructed on stock XYZ currently trading at Rs.50 per share with 30 days until options expiration.

To initiate the short iron butterfly, we first sell 1 XYZ 50 strike put contract, collecting a premium of Rs.2.

This represents the body put option position that will profit from the put expiring worthless if XYZ remains above Rs.50 at expiration.

Next, we buy 1 XYZ 45 strike put contract, paying a debit of Rs.1 to open the long put wing.

The 45 put provides downside protection in case XYZ drops below Rs.50. It defines our maximum loss.

We then sell 1 XYZ 50 call contract, collecting another Rs.2 premium to open the call body position.

This call benefits like the short put if XYZ is still at Rs.50 on the expiration date.

Finally, we buy 1 XYZ 55 strike call, paying Rs.1 debit to complete the long call wing.

This 55 call protects the upside if XYZ rallies past Rs.50 by expiration.

In total, we collect Rs.4 in premium income from the short 50 puts and calls while paying Rs.2 in debits for the long 45 put and 55 call wings.

This nets an overall credit of Rs.2 for initiating the short iron butterfly. Rs.2 represents the maximum potential profit if XYZ closes precisely at Rs.50 on the expiration date.

The maximum loss on the trade is capped at Rs.3, calculated as the difference between the wing strike prices of 55 and 45 minus the Rs.2 credit. This would occur if XYZ finishes below 45 or above 55.

The breakeven points are right at the 45 put and 55 call wing strikes. Below 45 and above 55 is where losses start accruing on the short iron butterfly.

We will now actively manage the short iron butterfly as expiration approaches, closing out the position early if XYZ threatens to breach either wing and incur maximum loss.

The short put and call options will expire worthless for the maximum Rs.2 profit target if XYZ remains between 45 and 55 through expiration. The long wings expire with no intrinsic value.

How successful is the Short Iron Butterfly?

The short iron butterfly has a relatively high probability of profit compared to many options strategies when implemented correctly. Precise statistics on success rates are limited, but various studies and probability models have estimated typical short iron butterfly profitability between 50-70% when incorporating sound risk management rules.

Academic research analyzing short iron butterflies held to expiration has calculated the probability of profit between 50% and over 60%, assuming a range-bound underlying price. The defined risk wings boost win rates substantially compared to naked short options selling.

Proprietary analytics conducted by leading derivatives desks have measured realistic short iron butterfly win rates around 45-55% when excluding wider low probability wings. Careful strike selection optimizes the probability of finishing in the money.

Historical backtesting of short iron butterflies on index ETFs like SPY shows profitable expiration outcomes roughly 60-65% of the time based on over 20 years of price data. These real-world results highlight the edge short iron butterflies carry.

Statistical models estimating the probability of the underlying finishing between the wings based on current volatility forecasts compute short iron butterfly POPs frequently over 50%, and optimal constructions over 65%.

Anecdotal estimates from experienced options traders often cite short iron butterfly win rates between 50-70% when actively managing trades incorporating sound risk management rules for early exits.

The key factors supporting favorable probability outcomes include selling overpriced implied volatility, careful strike selection, active management, early exits to retain profits, and utilizing hedging tactics.

While no strategy wins 100% of the time, favorable win rates in the 50-70% range highlight the probabilistic edge short iron butterflies carry when combining advantageous construction with optimization of trade management across the portfolio.

Is Short Iron Butterfly better than Straddle?

No, short iron butterflies are not necessarily better than long straddles overall. Each strategy has advantages and disadvantages depending on the market outlook and trader’s goals.

The long Straddle involves buying an at-the-money call and putting on the same underlying asset. It benefits from substantial volatility in either direction.

In contrast, the short iron butterfly sells an at-the-money call and put while buying farther out-of-the-money calls and puts as protection wings. It aims to profit from low volatility and a range-bound stock price.

The long Straddle has unlimited profit potential if the underlying makes a sharp move up or down. However, both options expire worthless for maximum loss if the stock finishes close to the strike price at expiration.

The short iron butterfly has capped profits limited to the net credit received but also strictly defined maximum loss. The wings create an upper and lower breakeven where the trade transitions between profit and loss.

Long straddles are ideal when expecting a breakout ahead of a major catalyst event like an earnings report. Short iron butterflies fit neutral, range-bound forecasts.

Holding long straddles into expiration exposes the trader to binary outcomes and time decay. Short iron butterflies benefit from time decay eroding the short strikes.

A long straddle buyer must pay double the premium upfront for the call and put. The short iron butterfly seller collects premium income.

What are the Advantages of Short Iron Butterflies?

The short iron butterfly is an options trading strategy with both limited profit potential and limited risk. It involves a combination of selling out-of-the-money puts and calls to collect premiums while also buying further out-of-the-money puts and calls to hedge risk. There are 8 key advantages to using a short iron butterfly strategy as follows.

Low Capital Requirements

The short iron butterfly has lower capital requirements than many other options strategies. Only the difference between the credit received from the short options and the cost of the long options has to be outlaid. This defined risk strategy does not require large capital reserves to manage potential losses like naked short options selling. The required capital is known upfront.

Defined and Limited Risk

The simultaneous sale and purchase of the put and call options creates a defined max loss. Most of the short iron butterfly loses the difference between the credit collected for the short options and the cost paid for the long options. The range where the maximum loss occurs is known when entering the trade. Risk is capped no matter how much the underlying stock will move.

Profit Potential in a Range-Bound Market

The short iron butterfly benefits from a stock trading in a horizontal channel with no discernible trend. As long as the stock remains between the short strikes at expiration, the trader keeps the entire credit collected. This strategy excels when volatility contracts and the stock oscillates in a range.

Higher Probability of Profit

By selling options and collecting premiums, there is a higher probability of earning a credit than simply buying options. The odds favor the options seller, which is the role taken with the short iron butterfly. The maximum profit is attainable as long as the stock finishes within the sold strikes.

Versatility in Selecting Strikes

The trader customizes the short iron butterfly by choosing the ideal strike prices based on the stock’s current trading range. Wider spreads mean higher credits but a lower probability of profit. Narrower spreads have a lower risk but smaller potential rewards. Flexibility in setting the strikes to match the stock’s expected range.

Defined Profit Zone

The maximum profit is known at the outset before trade entry. It is simply the net credit received. As long as the stock closes within the narrow range defined by the short strikes at expiration, this profit target is achieved. The profit potential is clear.

No Need to Predict Direction

Unlike many options strategies, the short iron butterfly does not rely on predicting the direction of the underlying stock. As long as volatility remains low and the stock settles within the sold strikes at expiration, the direction does not matter. No complicated timing of market tops or bottoms is needed.

Leverage with Minimal Costs

Selling options provide leverage on the capital committed. Each contract controls 100 shares of the underlying stock, magnifying returns on the initial investment. The long options hedge the shorts but have minimal cost due to being farther out-of-the-money. Leverage is created while limiting costs.

What are the Disadvantages of Short Iron Butterflies?

The short iron butterfly involves selling an at-the-money put and call while buying an out-of-the-money put and call to create a range with limited profit potential and defined risk. While this options strategy has advantages, there are also 10 potential disadvantages to consider.

Requires Low Implied Volatility

The short iron butterfly thrives when implied volatility on the options contracts is low. This allows the trader to collect more premium on the short options positions. It becomes more expensive to close out the short options if implied volatility rises. High IV environments are not suitable.

Limited Profit Potential

The maximum possible gain is capped at the net credit received when opening the trade. Even if the underlying stock ends up finishing substantially higher or lower at expiration, no additional profits are made beyond the initial credit. The short iron butterfly lacks upside potential beyond the solid strikes.

Bid/Ask Spread Risk

There are four legs to the short iron butterfly, which exposes the trader to more bid/ask spread risk than simple single-option trades. The cost of entering and exiting the trade is higher relative to other strategies with fewer components. More slippage on each leg adds up.

High Commission Costs

With four separate options contracts involved in most short iron butterflies, the commissions paid to brokers are typically higher than many other options strategies. More contracts mean more commissions if the broker charges on a per-contract basis. Costs eat into the maximum profit potential.

Early Assignment Risk

Selling the at-the-money options exposes the short iron butterfly trader to early assignment risk before expiration, especially on the short put leg. While not always optimal for the buyer, early assignment occurs and needs to be prepared for by the trader.

Loss of Stock Exits Range

Losses will begin accruing above the maximum risk point if the stock breaks out above the sold call strike or drops below the sold put strike at expiration. Whereas many options strategies have unlimited profit potential, the short iron butterfly faces unlimited risk if the stock exits the range.

Need for High Margin Reserves

Brokers require margin reserves to cover the maximum loss on short iron butterflies in case the stock breaks out above or below the sold strikes. Due to the undefined risk beyond the sold strikes, the margin requirements are onerous for the potential profits involved.

Complex Structure

The short iron butterfly has four separate legs involved, requiring diligent tracking and monitoring. Unwary traders do not fully comprehend the interwoven risks and components. The complexity makes it unsuitable for beginner options traders.

Wide Markets May Invalidate

In fast-moving, trending markets that gap up or down, the short strikes of the iron butterfly are breached, invalidating the strategy. Whereas defined risk is a key advantage in range-bound markets, fast markets heighten the risk of losses beyond the sold strike prices.

Difficult to Adjust or Roll

Short iron butterflies are difficult to adjust or roll to avoid losses if threatened early. The multiple legs and precise structure make modifying the strategy mid-trade problematic compared to simpler structures with fewer moving parts.

How risky is a Short Iron Butterfly?

The short iron butterfly does carry a defined and quantifiable maximum risk. However, with proper construction, monitoring, and management, the risks are mitigated compared to other options strategies.

The maximum loss on a short iron butterfly is known and strictly limited based on the strikes chosen for the wings. This loss is incurred if the underlying stock price closes below the lower wing put strike or above the higher wing call strike at expiration.

For example, if the put wing is at Rs.45 and the call wing is at Rs.55, the maximum loss would be the difference between the strikes minus any net credit received. This loss is realized if the stock finishes below Rs.45 or above Rs.55.

While potentially substantial in absolute dollar terms, the maximum loss represents the complete 100% risk amount. Short iron butterflies do not carry the theoretical unlimited loss potential of other short options strategies like naked calls or puts.

Appropriately sizing positions is crucial so that the defined maximum loss represents only a small percentage of the overall portfolio value. Concentrating too heavily on a single short iron butterfly trade exposes the trader to excessive downside versus total assets.

Actively tracking the stock price relative to the upper and lower break-even points allows managing winners and losers proactively. Monitoring the proximity to break-even signals when to take profits or cut losses early.

Hedging the wings using additional long calls and puts is an effective tactic to delay incurring maximum loss. The hedges provide buffers, allowing the short strikes more time to expire worthless if challenged.

Closing positions at 50% of the maximum profit potential locks in gains and minimizes risks into expiration. Letting profits run risks overnight volatility erasing short premium values.

Selecting highly liquid options on stable broad market ETFs minimizes the chance of excessive volatility jumps outside the wings. Less liquid options have large bid/ask spreads and gaps.

Implementing disciplined trade planning, execution, and management avoids emotional decisions that deviate from the strategy. Following rules and processes maintains rational reactions.

Utilizing stops at the breakeven points or other technical indicators provides clear triggers for early exits to preserve capital. Stops create automatic sell signals when reached.

Avoiding holding short iron butterfly positions into the final expiration week is wise since risks increase exponentially from gaps, volatility, low liquidity, and assignment.

Maintaining a balanced portfolio prevents overconcentration in any single short iron butterfly trade. Correlated losses will accumulate quickly without proper diversification.

Is Short Iron Butterfly a good option strategy?

Yes, the short iron butterfly is an effective options strategy in the right situations and when properly constructed and managed. It offers advantages over many other option techniques.

The short iron butterfly provides clearly defined, quantified risk parameters. Maximum loss is strictly limited to the difference between the wing strike prices minus any initial credit received. This contrasts with undefined risks of naked calls or puts.

Selling the call and putting credit spreads generates upfront premium income, enhancing potential returns. The probability of profit is favorable at around 50-70% for well-structured short iron butterflies held to expiration.

The wings create upper and lower break-even points that determine where losses begin accruing. This signals clear exit levels to preserve profits and minimize losses.

Short iron butterflies carry less risk than other short premium strategies like naked calls or puts which lack protection wings. The wings cap the total loss.

The cash flow from short premium sales contributes steady income to portfolios while waiting for neutral forecasted moves to play out.

Short iron butterflies profit from stable, range-bound markets and sideways trading stocks. This occurs frequently across lengthy time horizons.

However, the strategy does require market forecasts to be precise for maximum profit at expiration. Sharp volatility breaks across wings quickly, leading to maximum loss.

Is Short Iron Butterfly hard to use?

No, short iron butterflies are not inherently hard to use for experienced options traders familiar with basic vertical spreads. However, proper implementation does require learning key considerations.

Constructing a short iron butterfly only requires selling a call credit spread and putting credit spread sharing the same body strike and maturity date. This establishes the defined risk wings and body credit positions.

The potential profit, maximum loss, and break-even points are clearly calculated when entering the trade to quantify risk-reward scenarios.

Unlike more complex strategies like iron condors or butterflies, short iron butterflies contain just four total legs, allowing straightforward position management.

As the underlying price fluctuates, only the relative position to the breakeven points requires monitoring. Early closure or adjustment is warranted if either wing is threatened,

The mechanics of rolling, defending, or modifying short iron butterflies are relatively simple for seasoned options traders used to spread and verticals.

However, utilizing short iron butterflies effectively does require experience in 5 areas.

- Selecting appropriate strike widths based on volatility forecasts.

- Legging into positions efficiently at advantageous prices.

- Avoiding overpaying for wings while maximizing credit from shorts.

- Managing early if the body shorts become challenged.

- Understanding the impact of time decay on both wings and body options.

In addition, applying prudent risk management through defined trade plans, disciplined position sizing, and active monitoring is essential to managing potential drawdowns.

Is Short Iron Butterfly a bearish strategy?

No, the short iron butterfly is generally considered a neutral strategy and not inherently bullish or bearish in directional outlook. It aims to profit from low volatility rather than upward or downward forecasted price moves.

A short iron butterfly involves selling an at-the-money put credit spread and call credit spread sharing the same body strike and expiration. The wings create defined risk parameters.

The short call and put will expire worthless for maximum profit, if the underlying remains relatively stable with minimal volatility into expiration. The strategy benefits from non-directional trading.

The ideal forecast is for the stock to finish very close to the short strike at expiration. Whether it is slightly higher or lower does not matter since the key is settling between the breakeven points.

While traditionally neutral, short iron butterflies take on bullish or bearish tilts based on 3 positioning. Firstly, having a tighter put-than-call wing to benefit more from downward moves. Secondly, initiating the body put credit spread first if forecasting bearishness. Finally, it will widen the call wing more on rallying stocks to collect greater call premiums.

However, these directional tilts represent slight tactical shifts. The overall structure remains market-neutral, seeking to avoid substantial volatility in either bullish or bearish directions.

Unlike naked calls or protective puts, short iron butterflies are not inherently bullish or bearish in bias. Their goal is minimizing price movement, not choosing a forecasted direction.

Is Short Iron Butterfly the Most Effective Iron Butterfly Spread?

No, the short iron butterfly is not necessarily the most effective version of the iron butterfly options strategy. The long iron butterfly has its own set of advantages and disadvantages to consider.

The long iron butterfly involves buying an out-of-the-money put, selling at-the-money puts and calls, and buying an out-of-the-money call. It profits from low volatility, with the stock finishing near the short strikes.

In contrast, the short iron butterfly sells the at-the-money put and call spreads to collect premium income while buying the wings for protection. It, too, benefits from neutral sideways trading.

The long iron butterfly requires paying debit upfront and has limited but defined maximum profit potential capped by the distance between the wing strikes and body strikes. It risks total debit paid if it finishes outside Wings.

The short iron butterfly collects credit upfront and has maximum profit limited to that initial credit received. Maximum loss is also defined based on wing strike width minus initial credit.

The long iron butterfly then has a lower but also less risky max profit scenario. The short iron butterfly offers greater but capped return potential.

The long iron butterfly benefits more from time decay on the short options. The short iron butterfly’s wings also experience erosion over time.

In general, the short iron butterfly aligns better with neutral forecasts, expecting minimal volatility into expiration. The long butterfly fits small temporary price swings.

There are also iron condor variations combining call and put credit spreads. Ultimately, the proper structure depends on projected market conditions and risk preferences.

What is the difference between Short Iron Butterfly and Long Iron Butterfly?

The short iron butterfly involves selling an at-the-money put and call vertical spread to collect premium income upfront. In contrast, the long iron butterfly entails buying an out-of-the-money put and call vertical spread, paying a net debit to enter the trade.

The short structure has potential but capped maximum profit limited solely to the net credit received from the short call and put sales. The long structure has a lower but also defined maximum profit potential determined by the width between the wing and body strike prices.

The short iron butterfly’s maximum loss is strictly limited by the difference between the wing strike prices minus the initial credit collected. The long butterfly’s maximum loss is simply the total amount paid upfront to establish the body-wing vertical spreads.

In terms of Greeks, the short butterfly benefits from time decay eroding the value of the short call and putting premiums. However, the long wings also deteriorate in value over time. The long butterfly profits more purely from time decay on just the short options.

The short structure requires putting up margin collateral to support the naked short call and put verticals. The long butterfly trades define risk through the wings and need no margin.

The short iron butterfly collects credit upfront, boosting potential returns compared to the long butterfly which must pay a net debit out of pocket, lowering profit upside.

The short aims for both the call and put verticals expiring completely worthless at maturity. The long butterfly wants intrinsic value retained between the differences in wing and body strike prices.

There are assignment risks on the short call and put positions before expiration if they finish deep in the money. The long butterfly has no exposure to early assignment.

The short structure profits most from the stock price ending right at the sold strikes. The long butterfly aims for the stock to finish right between the wings and short strikes.

Short iron butterflies carry higher risk but offer greater return potential through short premium collection. Long iron butterflies cost less to initiate but have lower capped profits due to their defined risk-long positions.

Previous Article

Previous Article

26")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.