The short put butterfly is an options trading strategy that involves selling a put option at a middle strike price while also buying a put with a lower strike and another put with a higher strike. This creates a profit range between the lower and higher strikes while limiting risk.

The short-put butterfly benefits from neutral to bullish conditions. It aims to profit from a rise in implied volatility. This strategy has limited profit potential but also defined and limited risk. The maximum loss is incurred if the underlying asset finishes at either the lower or higher strikes at expiration.

What is a Short Put Butterfly?

A short put butterfly spread, also known as a short put butterfly, is an options trading strategy that involves selling a put option at a middle strike price while also buying two put options at a lower and higher strike price. The profit and loss graph of this strategy forms a symmetrical butterfly shape; hence the name butterfly spread.

The short put butterfly spread is constructed by selling one put option at a middle strike price and buying two puts, one with a lower strike price and one with a higher strike price. The lower and higher strike puts have the same expiration date as the short put at the middle strike.

This creates a range of strike prices that profit if the underlying asset closes within that range at expiration. Maximum profit is attained if the asset finishes at the short put strike at expiration. In contrast, the maximum loss occurs if the asset finishes below the lower strike put or above the higher strike put.

The short put butterfly spread has defined risk, meaning the maximum loss is limited, but the maximum profit is also capped. The maximum profit potential occurs when the underlying asset finishes right at the short put strike price at expiration. In this case, all the options expire worthless, and the trader pockets the net credit received when initiating the trade.

The maximum loss happens if the asset finishes below the lower strike put or above the higher strike put at expiration. In this scenario, the short put at the middle strike is in-the-money, and the lower and higher strike long puts expire worthless. The maximum loss is equal to the difference between the strike prices minus the initial credit received.

As a debit spread, the short put butterfly requires an initial credit to establish the trade, unlike a long butterfly spread, which requires a debit. The short puts butterfly profits if the underlying asset finishes anywhere between the lower and higher strike prices at expiration. This leads to the characteristic butterfly payoff diagram.

The breakeven points for the strategy are at the lower and higher strike prices. Any finish below the lower breakeven or above the higher breakeven results in a loss. The trader wants the asset price to finish as close as possible to the short put strike for maximum profit.

The short put butterfly is often used when the trader expects low volatility and does not anticipate a large move in either direction in the underlying asset. It profits from time decay as the options lose value into expiration. However, there is a risk if the asset price moves dramatically up or down outside the wings of the strikes.

As with any options strategy, proper position sizing and risk management are key. Traders should calculate the maximum risk and reward before placing the trade and be willing to withstand a loss up to the defined maximum risk. Using stops helps protect capital if the underlying makes a strong move against the position.

Selecting the proper strike prices and expiration dates allows the trader to fine-tune the risk-reward profile as desired. Wider wings represent higher risk but allow for a higher potential reward. Narrower wings have lower risk and lower reward. The trader sometimes adjusts based on their market outlook and risk tolerance.

Is Short Put Butterfly the same as 1-3-2 Butterfly Spread?

Yes, a short put butterfly spread is the same as a 1-3-2 butterfly spread.

The defining characteristic of a butterfly spread is that it combines options at three different strike prices in a specific ratio. For a put butterfly, this entails buying a put at a lower strike price, selling a put at a middle strike price, and buying a put at a higher strike price.

The ratios refer to the number of puts contracts involved at each strike price. So a 1-3-2 put butterfly means:

- Buy 1 put contract at the lower strike price.

- Sell 3 put contracts at the middle strike price.

- Buy 2 put contracts at the higher strike price.

This creates a ratio of 1:3:2 between the three strike prices. The 1-3-2 ratio is the most common configuration for butterfly spreads.

So when we talk about a “short put butterfly” or a “put butterfly spread,” it refers to a 1-3-2 configuration of buying puts at the wings (lower and higher strikes) and selling puts at the body (middle strike).

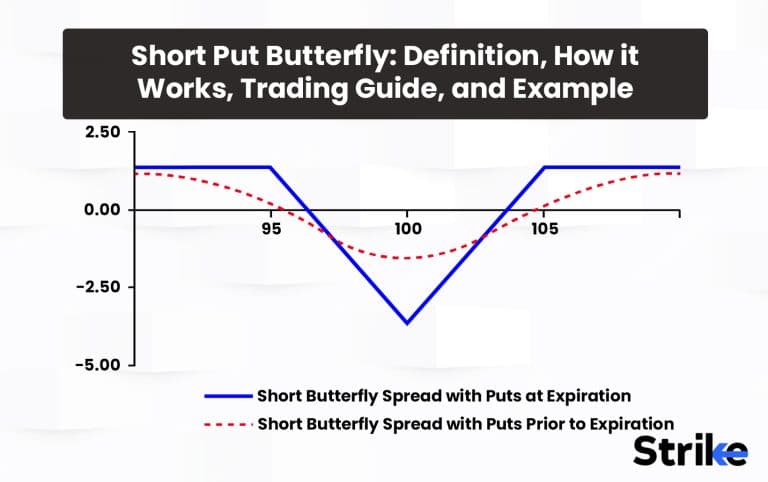

The short put butterfly has a payoff diagram that resembles a butterfly shape; hence the name butterfly spread. Maximum profit occurs at the middle strike price, while maximum loss happens below the lower strike or above the higher strike.

A short put butterfly spread has defined risk, meaning the maximum loss is capped while the maximum profit is also limited. The trader has short options at the middle strike and long options at the wings.

Being short options at the middle strike results in a net credit received for initiating the trade. This credit is the maximum profit potential if the underlying asset finishes at the middle strike price at expiration.

What is the importance of the Short Put Butterfly in Options Trading?

The short put butterfly spread is a significant options strategy that every trader should understand. Here are eleven of the key reasons why the short put butterfly is important for options trading.

Flexibility: The short-put butterfly is extremely adaptable in defining risk/reward. By selecting the strike prices and expiration, traders adjust the maximum profit, maximum loss, probability of profit, and breakeven points as desired. This flexibility allows the short put butterfly to match differing market outlooks and risk preferences.

Defined Risk: Unlike many multi-leg strategies, the short-put butterfly has defined limited risk. The maximum loss is strictly limited by the strikes chosen, allowing traders to exactly define their capital at risk. This is vital for proper risk management in options trading.

Capped Profit Potential: While the short put butterfly profit is capped, some traders see this as beneficial since it sets clear expectations for the trade reward potential. Capped profits are preferable to undefined profit strategies for conservative traders.

Time Decay Benefits: As an option seller at the body strike, the short put butterfly inherently benefits from time decay as the options lose value heading into expiration. This allows the strategy to profit even if the stock remains stationary.

Credit Spread: Since the middle strike put is sold, the short put butterfly produces an initial credit. This credit lowers the breakeven points and provides potential profit even if the stock finishes slightly outside the strike.

Adjustment Potential: It is frequently possible to modify the short put butterfly to prevent a loss if the underlying stock moves sharply. For example, one side could be closed out to convert the position to an iron condor. This adjustment potential provides flexibility.

Stock Price Consolidation: The short put butterfly profits from sideways or moderately trending price action in the stock. It does not require a large directional move to be profitable. This suits many mid-term neutral outlooks.

Margin Advantages: Depending on broker rules, the short put butterfly has lower margin requirements than other multi-leg structures. This frees trader capital for additional positions.

Delta Neutral: A short put butterfly with at-the-money strikes has an initial delta close to zero. This removes directional bias, which some traders prefer.

Wide Availability: The short put butterfly is sometimes traded on most liquid optionable stocks and indexes. It does not require weekly options or highly unusual options chains.

Risk Parameter Tradeoffs: Traders customize the short put butterfly by adjusting the strikes to favor the probability of profit, credit received, breakeven width, and other risk metrics.

Each trading strategy has pros and cons. However, the short-put butterfly provides unique advantages that make it an indispensable tool for many options traders. The ability to precisely define and limit risk while retaining flexibility and benefitting from time decay leads to the ongoing popularity and importance of this spread.

While the short-put butterfly is not suitable for all market conditions or trading plans, it is an excellent strategy to understand. The customization, flexibility, defined risk, and directional adaptability empower traders to match specific outlooks and goals.

These characteristics demonstrate why the short-put butterfly persists as a foundational option spread after decades of evolving financial markets. The versatility to adapt to evolving trading needs will likely ensure the short put butterfly remains a critical instrument in any options trader’s repertoire for years to come.

Options traders who take the time to thoroughly learn the nuances of constructing, managing, and adjusting short-put butterflies often gain skills that enhance their long-term chances for options trading success. Due to the unique risk/reward profile, the short put butterfly offers value that other single-leg or spread trades cannot easily replicate.

How does Short Put Butterfly work?

A short put butterfly spread involves the simultaneous purchase and sale of put options at three different strike prices to create a range of possible profit and loss scenarios. Here is a detailed explanation of the short-put butterfly options strategy.

Construction

The short put butterfly is constructed by selling one put option at a middle strike price while also buying one put at a lower strike and another put at a higher strike. The lower and higher strike puts have the same expiration date as the short put at the middle strike price.

For example, a trader sometimes sells 1 put at a 50-strike price while also buying 1 put at a 45-strike and 1 put at a 55-strike, all with the same expiration date. This creates a range of 45-50-55.

The options must have the same expiration for this strategy. The distance between the strikes determines the profit/loss characteristics. Wider distances mean higher potential profit but also higher potential loss.

Max Profit

The maximum profit is achieved if the underlying asset closes right at the middle strike price of the short put at expiration. In this case, all the puts expire worthless, and the trader keeps the entire initial credit received when opening the position.

The initial credit is the maximum profit potential. This only occurs at the middle strike price at expiration. Otherwise, profit is lower but still possible within the wings.

Max Loss

The maximum loss happens if the underlying asset closes below the lower strike put or above the higher strike put at expiration. The short put at the middle strike is assigned, while the lower and higher puts expire worthless.

The maximum loss is equal to the difference between the strike prices minus the initial credit. Loss is minimized when the butterfly is established for a credit. Loss increases as the strikes widen.

Breakeven

The breakeven points are at the wings – the lower and higher strike prices, below the lower breakeven or above the higher breakeven, result in a loss. Between the breakevens produces a profit.

The initial credit lowers the breakeven points. Without the credit, the breakevens would be directly at the lower and higher strikes.

Profit Zones

The maximum profit zone is right at the middle strike price. Profit shrinks as the asset price moves away from the middle strike towards the wings. The zone of profit depends on the distance between the strikes and the credit received.

Loss occurs outside the wings below the lower strike or above the higher strike. Profit occurs between the wings. The resulting payoff diagram resembles a butterfly shape.

Greeks & Implied Volatility

The short-put butterfly has a near zero delta initially when established with at-the-money strikes. It benefits from time decay as options lose value heading into expiration.

The strategy has positive vega, meaning it profits from an increase in implied volatility. Higher IV expands the wings and breakevens, improving the risk/reward profile as long as the price holds within the wings at expiration.

Managing the Trade

The short put butterfly is often traded as a set-it-and-forget-it position held to expiration. However, traders sometimes choose to actively manage it if the underlying price makes a strong move either up or down outside the profit zone.

Depending on market conditions, the position could be closed out early for a profit or loss if desired. Alternatively, one side could be closed to adjust to other strategies like an iron condor. Active management gives flexibility to adjust to changing conditions.

Risks & Drawbacks

The short put butterfly risks loss if the underlying makes a strong move below the lower strike or above the higher strike at expiration. The trader has to withstand this maximum loss. The potential profit is also limited to the initial credit received.

Traders should calculate the maximum risk/reward prior to placing the trade. Precise strike selection and active management do help mitigate drawbacks if market conditions shift.

How commonly do traders use the Short Put Butterfly strategy?

The short-put butterfly options strategy is used by traders in certain situations, but overall, it is not an extremely common trading technique. The different traders who use the short put butterfly are listed here, along with the situations in which they are used.

Volatility Traders

Traders who specifically focus on volatility will use the short put butterfly when they forecast a low volatility environment in the near term. As a short options strategy, the put butterfly benefits from stable, non-trending markets where premiums decay over time. Volatility traders deploying this are expecting consolidation or a tight trading range developing, ideal for put butterfly spreads to earn income.

Income Traders

Traders focused on generating consistent income, like the short put butterfly for its defined and limited risk parameters. The maximum profit is capped at the credit received, but some profit is earned as long as the stock finishes between the wings. This fits income traders looking for steady returns through options premium without taking on excessive risk. The short-put butterfly is not a home-run strategy but sometimes produces regular profits.

Smaller Accounts

The defined and lower margin requirements of the put butterfly make it appealing to smaller traders with less capital. Unlike naked short puts, which require large cash reserves, the put butterfly offers leveraged income potential with a lower cash outlay required. Newer traders utilize it to generate premium income with less risk than undefined short-put selling.

Algorithms/Automated Traders

The rules-based nature of the short put butterfly makes it well-suited for algorithmic and automated trading systems. The max profit, max loss, breakevens, and exit rules can all be programmed to execute the strategy automatically based on quantitative signals. Traders running algo strategies employ the put butterfly for its formulaic implementation.

How to Construct a Short Put Butterfly?

An explanation of how to build a short put butterfly options spread is provided below.

1. Identify Market Outlook

The first step is identifying your market outlook. The short put butterfly is ideal for neutral to moderately bearish outlooks, expecting the underlying stock to trade sideways or make a small bearish move. It benefits from low-volatility environments. The short put butterfly is appropriate if you anticipate continuous price activity inside a range.

2. Choose Expiration Date

Next, choose the expiration date for the options contracts. Short-put butterflies work best with at least 30-60 days to expiration to allow time decay to occur. Avoid using weekly options or options expiring in less than 30 days. Give yourself enough time to be right about the market direction.

3. Select Strikes

Now, determine the strike prices for each leg of the spread. Typically, the body strike is at-the-money or near the current stock price. The wings are equidistant away from the body and strike at a distance that defines your risk tolerance. For example, a stock at Rs. 50 could have strikes at 45-50-55.

4. Sell Body Puts

Once the strikes are defined, you will sell to open the put options at the body strike price. This is usually at least 2-3 contracts to match the wings. In a 1-3-2 ratio, you would sell 3 puts at the 50 strikes in the above example.

5. Buy Wing Puts

Next, buy to open the put options at the lower and higher wing strikes. You want 1 contract in each wing for a 1-3-2 ratio. In our example, buy 1 put at the 45 strike and 1 put at the 55 strike.

6. Create Net Credit

Sell the body puts for a higher premium than the wings cost to create a net credit. This lowers your break-even points and increases profit potential. The credit received is the maximum potential profit if the stock closes at the body strike.

7. Evaluate Risks

Review the risks involved before placing the trade. Calculate your maximum loss, which is the width of the strikes minus the initial credit. Set a stop loss if the stock approaches the wing strikes to contain losses. Define your profit target ahead of time as well.

8. Place Butterfly Order

As soon as you’re ready, place the short put butterfly order by selling the body put strike and concurrently purchasing the lower and upper wing put strikes for a net credit. Many brokers allow you to place this as a multi-leg combo order for ease of execution.

9. Actively Manage

Once the position is open, actively monitor and adjust if needed. You can close one side early to convert to an iron condor if the stock trends outside the wings. Manage the position to optimize returns for the market conditions.

10. Close at Expiration

Allow the options contracts to expire if all goes as planned. The trade generates the highest profit if the stock is at the body strike at expiry. You make a lower profit if you are in the wings. Let the put options expire worthless.

Precise construction and active management are vital for maximizing potential profit while limiting losses with this options trading strategy.

When to enter a Short Put Butterfly strategy?

Determining the optimal timing for entering a short-put butterfly spread requires analyzing five key factors. Traders should look for specific signals to identify advantageous entry points and avoid mispricing the trade. Here are five guidelines on when to enter a short put butterfly.

Low Implied Volatility

This is the most crucial element for effective put butterfly positioning. Implied volatility reflects the expected volatility priced into options. Lower IV makes options relatively expensive, perfect for a short-put butterfly sale. Check the IV Rank/Percentile for readings below 30-40, signaling depressed volatility expectations. Entering when IV is already elevated adds risk.

Range-Bound Stock Price

View technical charts to confirm the stock price is moving sideways within a range between clear support and resistance boundaries. Ideal conditions show a balance between bulls and bears. The stock doesn’t need to be in the exact middle of the range but should exhibit equilibrium without a directional bias.

Sideways Price Action

Analyse recent daily price action to identify non-trending behavior. The stock should demonstrate balance through alternating up and down days with relatively equal candle size and range. This choppy back-and-forth movement indicates no momentum in either direction.

Upcoming Known Events

Selling a short put butterfly around known volatility events like earnings or product releases allows maximizing high IV. Capture inflated premiums just prior to the announcement when uncertainty peaks. IV will decline post-event once the uncertainty is resolved.

Technical Support/Resistance

Identify key support or resistance levels the stock is approaching, such as moving averages, previous swing highs/lows, or Fibonacci retracements. These areas represent floors or ceilings that sometimes contain price movement. Target range-bound stocks near these zones.

The consequences of mistimed entry are listed below.

- Too early risks volatility expansion leading to early max loss.

- Too late reduces credit received and the probability of profit if the trend resumes.

When to exit a Short Put Butterfly strategy?

Knowing when to exit a short put butterfly spread is critical for locking in potential profits and avoiding unnecessary losses. Here are five key signals for butterfly exits and the consequences of exiting early or late.

Volatility Expansion

A spike in implied volatility indicates options are becoming relatively cheap again. This cuts into the value of short options positions. Exiting the put butterfly as IV rises allows for capturing existing premiums before they erode further.

Approaching Upper or Lower Strikes

Look to exit the put butterfly if the underlying stock moves in the direction of either the upper or lower strikes before expiration. The max loss point is reached if it breaches the wings. Take profits as it nears the wings while the spread still holds value.

Major Fundamental Changes

News that sometimes causes a big move in the stock, like an earnings surprise, merger, or CEO departure, should trigger an exit. The put butterfly relies on range-bound conditions that are disrupted by significant events. Close positions before the announcement.

Time Decay Acceleration

As expiration approaches, time decay tends to accelerate. This ramps up the erosion of the short option premium. Consider closing the put butterfly spread 2-3 weeks before expiration to realize the premium income as theta declines start compounding.

Technical Breakouts

A clear breach above resistance or breakdown below support warns of a momentum shift. Exit put butterflies if technical patterns show trend continuation or chart patterns like triangles complete with directional breakouts.

The consequences of mistimed exits are mentioned below.

- Exiting early sometimes leaves profit potential on the table if the stock remains stable.

- Exiting late risks turning winning trades into losses if a swing develops.

What is the maximum loss for Short Put Butterfly?

The maximum loss occurs if the underlying stock finishes below the lower strike or above the higher strike at expiration. This results in the short put at the middle strike being assigned while the long wing puts expire worthless.

To calculate the maximum loss amount, take the following steps.

First, determine the width between the strike prices. For example, if the strikes are 25-50-75, the total width between the outer strikes is 50 points (75 – 25).

Next, factor in the initial net credit or debit when entering the trade. Typically, a short put butterfly is placed for a small credit, which reduces maximum loss exposure.

This would decrease the loss by Rs. 1 * the number of traded contracts if it were set for a Rs. 1 credit. For a 1-3-2 ratio spread, a Rs. 1 credit would reduce max loss by Rs. 3 (3 contracts sold at middle strike).

Therefore, the calculation for maximum loss is as stated below.

Total width between outer strike prices – Initial credit received

Using the example above with strikes 25-50-75 and a Rs. 1 credit, the following will be the max loss.

Max loss = 75 – 25 – Rs. 3 credit = Rs. 47

The Rs. 3 credit received for selling 3 puts at the 50 strike lowers the loss by Rs. 3. So the maximum loss comes out to Rs. 47 per 1-3-2 ratio traded.

Without the credit, the maximum loss would simply be the full width between the strikes, or Rs. 50 in this case.

What is the maximum profit for Short Put Butterfly?

The maximum profit potential is an important consideration when analyzing a short put butterfly spread. Here is an overview of how to calculate the maximum possible profit.

The maximum profit on a short put butterfly spread occurs if the underlying stock finishes right at the short strike price at expiration.

In this scenario, the short put expires worthless, allowing the trader to keep the entire initial credit received when the position was opened.

The key determinants of maximum profit are the following.

- The initial credit is collected when establishing the spread position. This credit is the maximum profit possible.

- The number of contracts sold at the short strike. Each short-put contract contributes to the total credit.

For example, consider a short put butterfly with strikes at 40-50-60, established for a Rs. 1.00 credit.

Following the 1-3-2 ratio, 3 puts are sold at the 50 short strike in the middle. So, the total initial credit would be as stated below.

Rs. 1.00 credit x 3 contracts sold = Rs. 3.00 total initial credit

Therefore, the maximum profit for this particular short-put butterfly is the full Rs. 3.00 credit received.

This Rs. 3.00 profit occurs if the underlying stock finishes precisely at Rs. 50 (the short strike) at expiration. Any finish below 40 or above 60 would result in the maximum loss.

Five key considerations for maximum profit are the following.

- Realized only at body strike: Stock must be at short strike at expiration.

- Initial credit amount: Larger credit means higher profit potential.

- Number of body contracts: More short puts means greater credit received.

- Profit is capped: Maximum gain limited, unlike naked short options.

- Expiration dependent: Requires holding until expiry to capture full profit.

The initial credit collected when opening the short put butterfly represents the maximum profit possibility. The number of short puts at the body strike determines the total credit. Calculating the maximum gain ahead of time is crucial for assessing the risk/reward profile of the trade.

How does implied volatility affect the Short Put Butterfly?

Implied volatility has a significant impact on short-put butterfly spreads. Generally, low IV is beneficial, while high IV poses risks. Here is an overview of how implied volatility affects short-put butterflies.

Low IV at Entry

This is the ideal condition for initiating short-put butterfly spreads. Low implied volatility results in options being relatively expensive. As IV decreases, options premiums decline. This allows the short put butterfly trader to sell overpriced puts and benefit from ongoing IV contractions after entry.

Decay of Premiums

With the passage of time, implied volatility tends to revert lower. This erosion of extrinsic value profits short options positions like the put butterfly. The declining IV leads to decay in the short put premiums, enabling the trader to close the spread at a lower net debit or let it expire for maximum profit.

Compression Post-Earnings

Selling put butterfly spreads prior to earnings announcements allows benefiting from inflated IV ahead of the event. Once the uncertainty of the announcement passes, IV tends to decompress, resulting in short option premium deterioration.

Unlimited Risk if IV Spikes

While low IV is preferred, a sudden increase in volatility harms short-put butterflies. The short puts could need to be terminated at substantially higher prices if IV climbs further. In extreme cases, volatility expansion leads to unlimited losses beyond the maximum loss point.

Adjusting Strikes

The trader is able to tweak the put butterfly to tighter strikes if IV significantly drops after entrance. This allows for collecting more premiums at the new strikes. Strikes sometimes spread to lower danger if IV increases.

Implied volatility is a key consideration when trading short-put butterfly spreads. Low, stable IV after entry helps maximize profits. However, volatility spikes negatively impact the strategy. Traders should monitor IV closely when managing short-put butterfly positions.

How do traders break even with a Short Put Butterfly?

A Short Put Butterfly is an options trading strategy involving three puts with the same expiration date but different strike prices. The strategy is constructed by selling one put option at a middle strike price and buying two put options, one with a lower strike price and one with a higher strike price.

The short put butterfly strategy aims to profit from a stock trading in a narrow range near the short strike price at expiration. Potential profits are limited, but the maximum potential loss is also defined. Here are the key details on how the strategy works.

Strike Prices

The Short Put Butterfly involves three put option contracts with the same expiration but different strikes.

For example:

- Sell 1 Put at Middle Strike of Rs. 50.

- Buy 1 Put at a Lower Strike of Rs. 45.

- Buy 1 Put at a Higher Strike of Rs. 55.

To implement the short put butterfly, the trader collects a premium credit by selling the middle strike put. This is offset by paying premiums to purchase the outer strike puts. The goal is for all puts to expire worthless, allowing the trader to keep the initial credit received.

Maximum Potential Profit

The maximum potential profit on a short put butterfly is equal to the net credit received from the option premiums. This occurs if the underlying stock price is at the short strike at expiration.

In the example above, if the trader collects a net credit of Rs. 2.00 by executing the short put butterfly, Rs. 2.00 is the maximum profit potential. This is achieved if the stock is right at Rs. 50 at expiration, causing all the puts to expire worthless.

Maximum Potential Loss

The maximum potential loss is defined on a short-put butterfly. The maximum loss occurs if the stock price is below the lower strike or above the higher strike at expiration.

In the example, the maximum loss is the difference between the middle strike and the outer strikes, less the initial credit. So with strikes of 45/50/55, the maximum loss would be Rs. 5 – Rs. 2 credit = Rs. 3.

This loss happens if the stock is below Rs. 45 or above Rs. 55 at expiration. In either case, the bought puts would be in-the-money while the sold Rs. 50 put would have little or no value.

Breakeven Points

There are two breakeven points on a short-put butterfly strategy. The breakeven is calculated as stated below.

- Lower Breakeven = Middle strike – net credit received

- Higher Breakeven = Middle strike + net credit received

In the example with a Rs. 50 middle strike and Rs. 2 credit, the breakevens are the following.

- Lower breakeven = Rs. 50 – Rs. 2 = Rs. 48

- Higher Breakeven = Rs. 50 + Rs. 2 = Rs. 52

At expiry, the transaction does not turn a profit or a loss if the stock price is between these breakeven thresholds. Below Rs. 48 or above Rs. 52, a loss is incurred.

Risk Profile

A short put butterfly has a risk profile with two breakeven points surrounding the short strike price. There is a maximum loss defined if the stock moves below the lower strike or above the higher strike. The profit potential is limited to the net credit received.

The trader aims for the stock to be anywhere between the breakevens at expiration. As long as it remains in that range, the short-put butterfly produces a profit.

Margin Requirements

Margin requirements on a short put butterfly are usually less than other strategies since the maximum loss is defined. The initial margin requirement is typically around 20% of the maximum loss amount.

For the example strategy, with a maximum Rs. 300 loss, the initial margin requirement would be around Rs. 60. This is because the maximum risk is known and capped. Maintenance margin requirements are also lower for short-put butterflies than many other strategies.

ROI Analysis

Return on investment for a short put butterfly is assessed by comparing the maximum potential profit amount to the margin requirements.

In the example, the maximum profit is Rs. 200 on a Rs. 60 margin requirement. This represents a potential return on investment of 333% (Rs. 200 profit / Rs. 60 margin). However, this assumes the trader captures the maximum profit at expiration.

A trader breaks even on a short put butterfly by having the stock price between the breakeven points at expiration after the trade is executed. The probability of profit depends on the strike prices chosen and volatility conditions. Careful position management is required to maximize the ROI.

How does Short Put Butterfly strategy assignment risk occur?

A Short Put Butterfly involves writing or selling a put option at the middle strike price. This short put carries assignment risk, meaning there is a chance the trader is assigned to the put and obligated to buy the underlying stock. Here is an overview of how and when assignment risk occurs on a short put butterfly and whether it is ultimately good or bad for the trader.

How Assignment Risk Happens

With a short put butterfly, assignment risk primarily comes into play if the stock price drops below the middle strike price where the put was sold.

For example, consider a short put butterfly executed with the following strikes.

- Long 45 Put

- Short 50 Put

- Long 55 Put

The 50 put that was sold goes from being out-of-the-money to being in-the-money if the price falls below Rs. 50. The further below Rs. 50 the stock goes, the higher the intrinsic value becomes on this short put.

Once a put option is deep enough in-the-money, the holder sometimes chooses to exercise their right to sell shares at the strike price. This results in the short put seller being assigned – they must buy shares at Rs. 50 to fulfill their obligation.

The key point is that assignment typically only happens on a short put when it is in-the-money. This occurs if the stock drops below the middle strike at some point prior to expiration.

Is Assignment Good or Bad?

There are both pros and cons to early assignment on a short put butterfly.

Potential Downsides:

- Assignment triggers commissions/fees to buy shares.

- Impacts cash/buying power until stock is sold.

- Prevents further time decay benefit if close to expiration.

Potential Benefits:

- Exits option position at a favorable price.

- Opportunity to sell shares for profit if rebound occurs.

- Eliminates assignment uncertainty at expiration.

Assignment is generally neither inherently good nor bad. The net outcome depends on how the trader manages the shares after assignment.

The primary downside is assignment causes 100 shares per contract to be purchased. This sometimes ties up cash and buying power until the shares are sold. It also prevents taking advantage of remaining time decay as expiration approaches.

However, if assigned the stock at a lower price, the trader has the opportunity to sell the shares at a higher price if a rebound occurs. The trader is able to book a profit on the stock while keeping the net credit from the short put butterfly.

Timing of Assignment

Assignment risk increases as expiration approaches since the time premium component of the option declines. However, early assignments sometimes happen anytime the short put transitions into an in-the-money position.

Once a put is approximately 0.10 or more in-the-money, the chance of early assignment rises substantially. This generally corresponds to the underlying stock trading 0.10 lower than the put strike price.

For example, if short 50 put, stock at Rs. 49.90 could see a higher probability of assignment. The intrinsic value is high enough that a holder sometimes exercises the put instead of waiting.

Preventing Early Assignment

A trader takes four steps to reduce the chances of early assignment on a short put butterfly.

- Close out position before expiration if threatened.

- Avoid holding to expiration week.

- Buy back short put if deep in-the-money.

- Use European style options, which only allow assignment at expiration.

While not guaranteeing the prevention of early assignment, traders proactively monitor and manage positions with these tactics to reduce assignment risk at unfavorable times.

What is the impact of Time Decay on Short Put Butterfly?

Time decay, or theta, has a significant positive impact on short-put butterfly spreads. As expiration approaches, the erosion of time value benefits short options positions like the put butterfly. Here are the key effects of time decay listed below.

Premium Erosion

As time to expiration decreases, the extrinsic value or time premium priced into options declines. This erosion of time value profits short options traders like put butterfly investors. The declining premium boosts the mark-to-market profitability of the short puts.

Higher Probability of Profit

With the passage of time, the probability of the stock finishing between the wings by expiration increases. This rising probability benefits the short put butterfly, where maximum profit occurs if the stock holds the trading range. Time decay makes the forecast range more likely.

Accelerated Decay Near Expiration

Time value decay tends to accelerate in the last few weeks before expiration. This nonlinear compression is beneficial for short-put butterflies, as premium income sometimes grows rapidly late in the trade.

Allows Closing Spreads at Lower Cost

Declining time value enables traders to buy back short put butterflies at a lower net debit as expiration approaches. Traders realize profits without holding to expiration as premiums erode.

Maximizes Return for Accurate Forecast

Time decay maximizes earnings on the short options when volatility and price movement follow the predicted patterns. The trader’s forecast is rewarded through greater premium income from theta.

Time value erosion has a very positive effect for short-put butterfly traders. It enables capturing increasing profits as expiration nears. With volatility and price stable, decaying time premiums maximize income within the trade’s defined risk parameters. Monitoring time decay is essential for managing short-option spreads.

How does expiration risk affect the Short Put Butterfly strategy’s gains and losses?

A short put butterfly involves significant expiration risk because the maximum profit is only achievable if the underlying asset closes right at the middle strike price of the three legs on the expiration date. Any deviation above or below this price at expiration dramatically reduces profits or leads to losses.

The ideal scenario for a short put butterfly is for the underlying asset price to be at the middle strike price when the options expire. In this case, the middle long put expires worthless while the trader keeps the full premium collected from shorting the lower and higher strike puts. This allows the trader to realize the maximum potential profit built into the position. However, if the asset price is above or below the middle strike at expiration, some additional loss on the long put and reduced profit on the shorts occurs.

For example, if the asset price declines below the middle strike by expiration, the long put finishes in-the-money and has intrinsic value. This means the trader loses money on the long put while also making less profit on the lower-strike short put. The same dynamics apply in reverse if the asset price rises above the middle strike. Here the higher strike short put finishes in-the-money while the long middle put loses value. In both cases, the traversal of the middle strike price severely cuts into the maximum income potential.

This expiration risk is greater the wider the distance between the wing strikes. The larger the gap, the greater the asset price sometimes moves before a loss is generated. However, the wider the strike distance, the smaller the initial premium income collected. This results in a trade-off between maximizing credit received upfront and minimizing expiration risk.

Expiration risk also increases the closer the asset price is to one of the wing strikes as expiration approaches. An early assignment on the short put is conceivable if it is significantly in the money. This removes the short put premium while exposing the trader to an exercised option assignment. To avoid this, the position must be closed before expiration if the asset price approaches either wing strike by maturity.

One way traders aim to reduce expiration risk is by using shorter-term options, such as monthly over weekly expirations. The accelerated time decay of shorter-term options raises the probability of the asset finishing close to the middle strike target price at maturity. However, shorter expirations still carry a risk if a substantial price move up or down develops.

How to adjust Short Put Butterfly?

There are five effective adjustment techniques to salvage challenged short-put butterfly spreads.

Roll the Options Out in Time

Rolling out the options on a monthly or quarterly cycle might lower the risk if the underlying stock goes in a different direction than the wings. This pushes the expiration date further out to give more time for the stock to revert into a profitable range. Be aware of transaction costs on multi-leg rolls.

Leg Out of One Side

Traders define risk on only one side by closing a wing at a loss if the stock breaches it. For example, if a 45/50/55 put butterfly rises above 55, close the 55 put to remove upside risk. Hold the 45/50 puts as a modified butterfly.

Convert to an Iron Butterfly

Sell puts at the higher strike as well to turn the put butterfly into an iron butterfly if the stock is trading between the middle strikes as expiry draws closer. This monetizes the body risk at credit to offset the maximum loss.

Expand the Wings

The put butterfly wings are sold at closer strikes to earn more premium if implied volatility significantly drops. This adjustment is feasible if the forecast range compresses.

Transition to a Condor

Put condors increase the range of profitability if the stock goes outside the profit zone, but volatility is still modest. Sell further OTM puts to finance converting a losing butterfly to a condor.

Adjustment decisions depend on factors like time to expiration, volatility, and transaction costs. The goal is to reduce risk and increase the probability of profit through timely adjustments.

What is an example of a Short Put Butterfly?

An example of a short put butterfly strategy would be buying 1 XYZ 50 put, selling 1 XYZ 45 put, and selling 1 XYZ 55 put, all with the same expiration date. This creates a short put butterfly spread with the wings at a 45/55 strike and the body at 50.

In this example, the trader would receive a net credit when opening the short put butterfly spread, as the premium collected from selling the 45 and 55 puts would be greater than the premium paid to purchase the 50 puts. For example, if the trader collected Rs. 2 per contract selling each wing and paid Rs. 1 to buy the body, that would equate to a Rs. 3 net credit per butterfly spread.

The maximum potential profit on this short-put butterfly is equal to the initial net credit received. In this example, the maximum gain would be Rs. 3 per spread. Profit is realized if XYZ stock closes precisely at the body strike price of Rs. 50 when the options expire. In this case, all the options in the spread expire worthless, and the trader keeps the full Rs. 3 credit per spread.

The maximum potential loss is equal to the difference between the wing strikes, less the initial credit. Here, the wing strikes are 45/55 for a 10-point spread. With a Rs. 3 initial credit, the max loss comes to Rs. 7 per spread (10 – 3 = 7). A loss occurs if XYZ closes below Rs. 45 or above Rs. 55 at expiration. Between the wings, losses shrink as XYZ approaches Rs. 50 at expiration.

The short put butterfly profits from time decay as the short 45 and 55 puts lose value faster than the long 50 put. The position benefits if XYZ remains stable or slowly trends up/down over time. Large, quick moves beyond the wings incur losses. Adjustments are required if XYZ trends are strongly bearish or bullish before expiration.

An example profit scenario would be if XYZ is trading for Rs. 48 when the position is opened, then gradually trends up to Rs. 50 by expiration. In this case, the short put butterfly expires with XYZ at the ideal Rs. 50 body strikes to achieve the maximum Rs. 3 profit. A loss scenario would be if XYZ declines below Rs. 45 rapidly, causing early exercise and losses on the lower wing before expiration.

What are the advantages of Short Put Butterfly?

A short put butterfly, also known as a short put condor, is a multi-leg option spread strategy with defined risk and profit potential. The advantages of a short put butterfly are the following.

Defined and limited risk

A short-put butterfly has a clearly defined maximum loss, which is limited to the difference between the wing strikes minus the initial credit received. For example, if the wing strikes are 30 and 40, with a 10-point spread, and the initial credit is Rs. 2, the maximum loss is Rs. 8 (Rs. 10 – Rs. 2 credit = Rs. 8 loss). The loss is capped at the wing strike distances regardless of how far the underlying asset price moves.

Lower margin requirements

Compared to positions with undefined or unlimited risk, like short naked puts, the defined risk aspect of a short put butterfly lowers the margin requirement. Less capital is tied up in the trade. The cash freed up is used to open other positions or provide a buffer against losses.

Benefits from time decay

As an options seller strategy, a short put butterfly profits from time decay as the overall position loses value into expiration. The short puts at the wings decay at an accelerated rate compared to the long put at the middle strike. This erosion of time value translates into potential profit if held to expiration.

Profits from stable or directionally trading markets

Markets trending sideways or experiencing low volatility create ideal conditions for this strategy. The passage of time enables capturing profit as the short options’ premium decays. Small downward or upward drift also allows for reaching maximum profit potential.

Leveraged returns on capital

The initial credit received provides leveraged returns since the capital outlay is only the margin requirement, not the full position size. For the risk taken, the percentage return on required capital is sometimes quite high if the trader reaches the maximum gain.

Flexible adjustment capabilities

The short put butterfly provides for altering both wings, the body, or the entire risk profile if the price of the underlying asset moves against the position. Repair strategies help defend against losses in many market scenarios.

Higher probability of profit

Structuring the put butterfly as a credit spread boosts the probability of a profitable trade. The parameters are set up to achieve a probability of 80% or greater, especially if aiming to capture just a portion of the maximum gain.

The advantages of short-put butterflies include defined risk, lower capital needs, leveraged returns, time decay benefits, and flexibility. This trading approach has the ability to provide steady revenue when used with good position management.

What are the disadvantages of Short Put Butterfly?

A short put butterfly involves selling a put at a lower strike, buying a put at a middle strike, and selling a put at a higher strike for a net credit. The disadvantages of a short-put butterfly are listed below.

Large moves can lead to maximum loss

A large, rapid rise or fall in the underlying asset price sometimes results in the maximum loss on a short put butterfly. Significant losses occur if the price goes below the lower strike or above the higher strike by expiry. The wider the wing strikes are set, the greater the maximum loss.

Substantial margin requirements for wide spreads

A short-put butterfly has specified risk, but occasionally, it is still necessary to use a substantial amount of margin money due to the possibility of loss. Butterflies with wider wings have greater loss risk and margin needs. The cash tied up in margin sometimes negatively impacts available trading capital.

Challenging to achieve maximum profit

Realizing the maximum profit potential requires the underlying asset to close precisely at the middle strike price at expiration. Any deviation above or below reduces profit. Hitting the exact center price is unlikely, making full profits hard to capture.

Vulnerable to volatility increases

Rising implied volatility hurts short options positions since higher volatility raises options prices. An increase in volatility sometimes reduces profits or creates losses on a short put butterfly, especially in the last 30 days until expiration.

Early assignment risk on short options

Early assignment risk on the short put exists if the asset price drops below the lower strike. Early exercise could force purchase of the underlying at an undesirable price. Preventing early assignment requires closing the position prior to expiration.

Complex structure with multiple legs

A short put butterfly involves at least three, often four, total options contracts. The multi-leg structure makes it more complex to analyze, establish, and adjust compared to basic strategies like long puts or calls.

Significant transaction costs to open and adjust

The number of contracts traded leads to higher commissions paid to open and close a short put butterfly. Legging in or out also increases costs. Rollovers or adjustments add further transaction fees.

Short-put butterflies carry defined but substantial risk, margin needs, and transaction costs. The specialized structure and exposure to volatility also require active management. These disadvantages must be accounted for when utilizing this strategy.

Is Short Put Butterfly risky?

No, a short-put butterfly options strategy is not inherently risky when implemented properly.

While a short-put butterfly does carry some defined risk, it is structured as a limited loss strategy. The maximum loss is capped at the difference between the wing strike prices minus any initial credit received. For example, if the wing strikes are 30 and 40, the max loss is Rs. 10. The loss cannot be greater than Rs. 8 if the account was started for a Rs. 2 credit.

The defined and capped risk makes short put butterflies less risky than undefined risk short selling strategies like naked puts or calls. The use of multiple options contracts also spreads the risk across the strikes to localize losses.

However, the loss is still substantial sometimes on a short put butterfly if the underlying stock makes a very large move outside the wings before expiry. So, proper position sizing relative to account size is key to limiting the risk. Wider strike distances also increase the loss potential.

In addition, short-put butterflies benefit from time decay, allowing profits to be made even if the stock moves somewhat against the position before expiration. The initially collected credit provides a buffer against losses in many scenarios.

Is Short Put Butterfly a good options strategy?

Yes, a short put butterfly is sometimes an effective options trading strategy in certain market environments and when utilized properly. Here’s a more detailed explanation.

The main benefits of a short-put butterfly are the defined and limited risk profile along with the ability to profit from time decay. By shorting the wings and buying the body, the position profits as the overall spread loses value into expiration. This makes it a suitable strategy for range-bound markets.

The short put butterfly offers leveraged returns on the initial credit received while requiring lower capital outlay than undefined risk short put positions. The spread structure also localizes losses to the wings, reducing risk.

However, the short put butterfly does have downsides. It sometimes does experience substantial losses if the underlying stock breaks out of the wings before expiration. And transaction costs are higher due to the multiple-leg structure.

Achieving the maximum profit also requires the stock to close right at the middle strike price at expiry, which is challenging. So, profits are often less than the theoretical maximum. Any large, rapid price move violates the ideal stable trading range.

Is Short Put Butterfly hard to use?

No, a short put butterfly options strategy does not have to be overly complex or challenging to implement and manage. Here is a more in-depth explanation.

While the short-put butterfly involves multiple legs and parameters to analyze, the structure itself is straightforward. Traders simply sell a put at a lower strike, buy a put at a middle strike, and sell a put at a higher strike, ideally for a net credit.

The defined risk parameters and profit/loss diagrams are also easier to grasp compared to strategies with unlimited risks, like short naked options. The maximum gain occurs at expiration if the underlying is at the mid-strike, while the maximum loss is limited by the wings.

In addition, many trading platforms have pre-built templates or automated tools for establishing short-put butterfly spreads with a few clicks. This makes opening the position seamless. Charting platforms also often include profit/loss modeling capabilities.

During the life of the trade, monitoring is relatively simple – traders mainly have to watch if the asset price trends too far above the higher or below the lower wing strikes. As long as it remains between the wings, no action is required.

Adjustments sometimes get more complex if repair strategies are needed, such as rolling the position. But these adjustments are not inherently difficult, just something traders get better at implementing with practice over time.

Is Short Put Butterfly a bullish strategy?

No, a short put butterfly is generally not considered an inherently bullish options trading strategy.

A short put butterfly is structured by selling a lower strike put, buying a middle strike put, and selling a higher strike put. This spread profits from time decay as the overall position loses value into expiration.

The strategy aims for the asset price to be close to the middle strike at expiry. Maximum profit occurs if the price finishes precisely at the middle strike at expiration. This means the position sometimes profits from the asset trading in a sideways or moderately bullish fashion over time.

However, unlike solely long bullish trades like long calls, a short put butterfly actually benefits from somewhat bearish activity initially after opening the trade. Some downward movement allows the short puts to expire worthless while the middle put loses less value.

In addition, increased volatility, which accompanies bear moves, sometimes raises the value of the short puts and provides additional early profits. So, the position does not need a strongly bullish trend to profit, just low volatility and a neutral to modestly bullish outlook.

While substantial downward moves below the lower wing strike sometimes generate losses, small bearish moves are beneficial. As long as the asset remains between the wings at expiry, bearish price action does not negatively impact the strategy.

Is Short Put Butterfly the most effective Butterfly spread strategy?

No, the short-put butterfly is not necessarily the most effective butterfly spread strategy in all market conditions.

A butterfly spread combines a bull spread and a bear spread with the center strike in common. It uses three strikes to form the “wings” and “body” of the butterfly. There are four basic types – call butterflies, put butterflies, iron butterflies, and iron condors.

The short put butterfly specifically involves selling a lower strike put, buying a middle strike put, and selling a higher strike put. It aims for the underlying asset to be at the body strike at expiration to profit.

However, short calls and iron butterflies are more effective in certain situations. For stocks expected to rise, a call butterfly targets upside moves more precisely. Iron butterflies are more flexible, with both call and put credit spreads, and have a higher probability of profit.

The relative effectiveness depends on factors like directional bias, volatility, time to expiry, and risk management preference. Short-put butterflies excel when moderately bearish to neutral activity is expected. But they are not universally better across all market environments.

In general, traders select the butterfly strategy that best matches their outlook on the underlying asset while accounting for risk preferences. Each butterfly spread has advantages in certain situations depending on strike selection, cost, and directional assumption.

What is the difference between Short Put Butterfly and Long Put Butterfly?

A long put butterfly involves buying a put at a lower strike, selling two puts at a middle strike, and buying a put at a higher strike. A short put butterfly entails the reverse – selling a lower strike put, buying two at the middle, and selling a higher strike put.

The long put butterfly is a debit spread, meaning the trader pays a net debit to open the position. The short put butterfly is a credit spread, with the trader collecting a net credit upfront when opening the trade.

The maximum profit on a long butterfly is attained if the asset expires between the wing strikes. The maximum profit on the short butterfly occurs at expiration if the asset price is right at the middle strike.

The long put butterfly profits if the asset closes inside the wings at expiry after making a large move lower or higher. The short butterfly benefits from time decay and low volatility, seeking to profit from a small move or neutral trading into expiration.

The long butterfly has defined maximum risk, limited to the initial debit paid. The short butterfly also has defined risk, capped at the wing strike width less the initial credit.

For the long-put butterfly, higher volatility expanding the width of the wings raises the probability of profit. For the short put butterfly, lower volatility and a narrower trading range boost the odds of success.

The long-put butterfly is anticipating and benefiting from a sizable directional move and swing in volatility. The short butterfly has negative vega, so profits from stable, low volatility conditions into expiry.

Adjustments for the long butterfly involve rolling up/down the wings or closing early to avoid max loss. Short butterfly adjustments aim to defend credits, such as closing early to take profits or rolling untested wings.

Margin requirements differ, with the defined risk long put butterfly having a higher margin. The defined risk short butterfly has a lower margin requirement.

Both defined risk strategies are useful for different neutral strategies or moderately bullish/bearish outlooks. Their distinct risk/reward profiles cater to varied expectations on volatility, price action, and time decay over the life of the options.

What is the difference between Short Put Butterfly and Short Call Butterfly?

A short put butterfly involves selling a lower strike put, buying a middle strike put, and selling a higher strike put. A short call butterfly entails selling a lower strike call, buying a middle strike call, and selling a higher strike call.

The short put butterfly achieves maximum profit if the underlying expires at the middle strike price. The short call butterfly reaches max profit if the underlying finishes right at the middle strike at expiration as well.

The short put butterfly benefits from mildly bearish price action initially, allowing the short puts to expire worthless while the long put retains value. The short-call butterfly profits from mildly bullish action initially instead.

With the short put butterfly, the trader collects a premium upfront if the asset price is above the higher strike put sold. The short call butterfly collects a premium if the asset is below the higher strike call sold.

The short-put butterfly wants volatility to decline over the life of the trade. The short call butterfly profits from falling volatility as well, enabling the short calls to expire worthless.

Rising volatility hurts the short put butterfly as put prices increase, potentially causing losses. But rising volatility benefits the short-call butterfly as call prices increase.

An early exercise risk on a short put butterfly arises if the asset declines below the lower strike put sold. For the short call butterfly, early exercise risk emerges if the asset rises above the higher strike.

Adjustments for the short put butterfly involve repairing the untested side by rolling or modifying the losing tested side. Short call adjustments are the mirror image – adjusting the tested side and leaving the untested side.

The short-put butterfly has a negative delta, benefiting from falling prices. The short call butterfly has a positive delta, gaining from rising prices.

Previous Article

Previous Article

14")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 16")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 17")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 18")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 22")

No Comments Yet.