A long call butterfly is a limited profit, limited risk options strategy used when an investor expects moderate upside movement in the underlying asset. A long call butterfly involves buying a call spread while selling a call between the spread strikes to finance the trade.

A long-call butterfly benefits from a moderate upside forecast in the underlying asset. As the short call decays faster than the long calls, profitability increases if the underlying rises slightly above the short call strike. It allows traders to profit from directional upside within a range. It can be used ahead of events with upside uncertainty, like product launches or earnings.

What is a Long Call Butterfly?

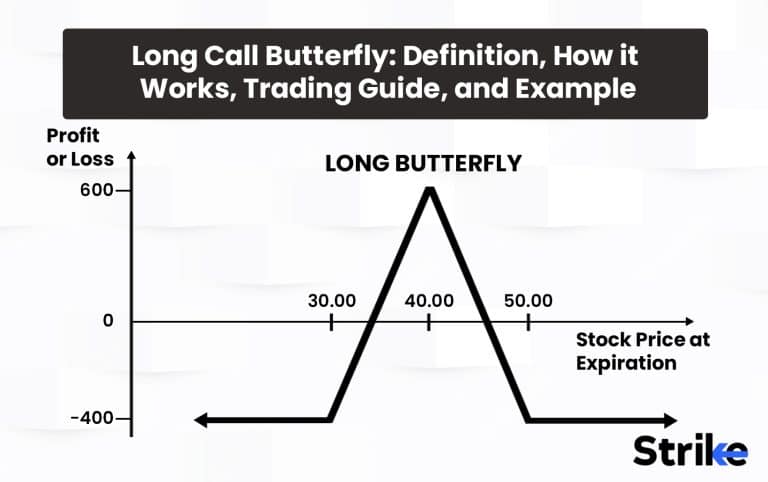

A long call butterfly, also known as a long butterfly spread, is an options trading strategy that involves buying two call options at different strike prices and selling two call options at a strike price between the two call options that were purchased. The goal is to profit from the stock price remaining near the middle strike price at expiration.

A long-call butterfly takes its name from the profit/loss diagram, which resembles the wings of a butterfly. It is constructed using three calls with the same expiration date but different strike prices. The strikes are equidistant from each other, and the middle strike is at the price where the trader expects the underlying stock to be at expiration.

Here is how a long-call butterfly is constructed.

- Buy 1 lower strike call option.

- Sell 2 middle strike call options.

- Buy 1 higher strike call option.

All the options must have the same expiration date. For example, a trader might buy 1 Rs. 90 call, sell 2 Rs. 100 calls, and buy 1 Rs. 110 call if they expect the stock price to be around Rs. 100 at expiration.

The long call butterfly limits profits but also reduces risk compared to just buying a call option. Maximum loss is limited to the net debit paid to construct the spread. The maximum gain is capped at the difference between the wing strikes (higher and lower strike calls) less the initial debit paid.

Profits are made when the stock price finishes near the short strikes at expiration. The further away the stock moves from the middle strike at expiration, the lower the profit or higher the loss up to the maximum loss.

The breakeven points are at the wing strikes less the initial debit paid. For example, if the lower wing strike is Rs. 90, the higher strike is Rs. 110, and debit paid is Rs. 5, breakeven is at Rs. 85 and Rs. 115.

Reasons to use a long call butterfly are mentioned below.

- Capped downside risk since the maximum loss is defined.

- Lower cost to establish than buying just calls or puts due to selling the middle strike options.

- Benefits from time decay as expiration approaches.

- Profits from moderate movement in stock price rather than large upside or downside moves.

The long call butterfly is essentially combining a bull call spread and a bear call spread. Buying the lower strike call and selling the middle strike call creates a bull call spread. Selling the higher strike call and buying the middle strike call creates a bear call spread. Combining them into a long butterfly reduces cost but also caps profits.

A trader might use this strategy when they expect low volatility and for the stock to remain close to the middle strike at expiration. It offers a lower-cost way to profit from small price moves versus just buying calls or puts. The well-defined risk-reward profile is attractive to many option traders.

Max loss occurs if the stock is below the lower strike or above the higher strike at expiration. Max profit occurs if the stock is at the middle strike at expiration. Anywhere between the wings results in variable profit/loss depending on how close to the middle strike the stock finishes.

Greeks behave differently for a long call butterfly spread in the following ways.

- Delta is positive when stock is below the lower wing, zero at the middle strike, and negative above the higher wing.

- Theta is positive – the passage of time helps call butterfly.

- Vega is low since volatility doesn’t help or hurt much within wings.

A long call butterfly benefits from time decay, so it is sometimes placed 30-60 days to expiration. Give enough time for a projected move to middle strike, but also have theta work.

The strategy is often used when a stock is expected to move from a high to a low volatility regime. For example, an earnings announcement may cause volatility expansion, but afterward, volatility could contract again. The long butterfly benefits from the stock stabilizing near the middle strike.

A trader might also use this strategy on an underlying stock that tends to trade in a price channel without much trend. A long butterfly sometimes profits from a price reversion to the mean between support and resistance levels identified by technical analysis.

The limited upside of a long call butterfly means it should only be used when expected price moves and volatility forecasts are fairly accurate. The long butterfly will perform worse than just purchasing calls or puts if the stock makes a greater up- or down-move. The trader gives up upside potential for lower cost and defined risk.

What is the importance of Long Butterfly Spread with Calls in options trading?

The long call butterfly spread is an important multi-leg options strategy that offers defined risk management, low-cost structure, and unique profit potential. Its importance stems from the flexibility and advantages it provides options traders in certain situations.

A long call butterfly involves buying a lower strike call, selling two at-the-money calls, and buying a higher strike call. It creates a payoff diagram shaped like a butterfly, with the wings representing profit potential.

The importance of the long call butterfly includes the ones listed below.

Defined Risk

The maximum loss on a long call butterfly is the net premium paid to establish the position. Unlike naked call writing, the wings limit upside risk. The trader knows the most they can lose at entry. This defined and capped risk is vital for prudent options trading.

Limited Profit Potential

A long-call butterfly has limited profit potential equal to the difference between the wing strikes minus the net cost. While not offering unlimited upside like long calls, the strategy allows reasonable profits from a range-bound outcome.

Lower Cost Structure

Since a long call butterfly only involves buying options, the lower premium outlays create a more affordable multi-leg spread. Compared to positions that sell options for income, like a short iron condor, the lower cost makes it accessible to smaller accounts.

Benefits from Low Volatility

Time decay hurts the long calls but also helps offset the short calls. An ideal scenario is a decline in implied volatility that erodes premium across all the options equally. This allows the position to retain value better than solely long options.

Flexibility in Adjusting or Closing

The three-legged structure offers flexibility to adjust or close at opportune times. For example, the short calls could be closed first if the stock drops below the lower wing to remove downside exposure.

Profit Potential with Range Bound Trading

A long-call butterfly achieves maximum profit if the stock price finishes right at the short strikes. This optimized outcome occurs if the underlying trades are in a range. The strategy allows benefiting from range-bound behavior.

Neutral to Moderately Bullish Bias

While market neutral, a long call butterfly exhibits a slightly bullish bias since the lower wing strike is closer to the stock price than the higher wing. A moderate move up is acceptable, just not a large rally above the upper breakeven.

Hedging or Volatility Positioning

The characteristics make it suitable as a hedging position or to take advantage of a volatility view. For example, it could hedge a long stock position or benefit from an expected volatility compression.

Higher Probability Outcomes

Relative to the cost incurred, the maximum profit potential occurs at a higher probability middle range rather than requiring substantial stock movement like a long condor.

The following are mentioned when considering their practical significance in the deployment of a long-call butterfly.

It allows benefiting from a stock previously trading directionally when expecting a shift to non-directional trading.

It is sometimes used to leg into a long iron butterfly if the stock moves above the upper strike to further limit risk.

It provides a better risk-return profile than buying expensive out-of-the-money calls to benefit from the upside.

It offers a way to reduce cost over a long call vertical while still maintaining upside potential.

It functions as a volatility hedge around events like earnings when expecting a surge in implied volatility.

While complex spreads, once understood, a long call butterfly provides important advantages not replicated by other basic strategies. The limited risk nature, centered maximum profit area, and versatility make it an important tool for seasoned options traders.

How do Long Call Butterflies work?

A long call butterfly spread is constructed by buying a lower strike call option, selling two at-the-money call options, and buying a higher strike call option. It is named as such because the payoff diagram resembles the shape of a butterfly. The mechanisms behind a long call butterfly are rooted in the interaction between the long and short calls..

Buying Calls

A long call butterfly involves going long, a lower strike call, and a higher strike call. These provide the potential for unlimited upside profit if the stock appreciates. The purchased calls have defined limited risk equal to the premium paid.

Selling Calls

Short calls are sold at the body strikes to bring in premium income and offset the cost of the wings. The short calls face unlimited risk beyond the strike price. But the wings help limit this risk within a range.

Defined Profit Zone

Maximum profit occurs if the stock settles right at the middle short strikes where both the long and short calls expire worthless. This creates a defined zone where the net original premium creates maximum gains.

Capped Downside Risk

Losses are capped at the cost of opening the position if the stock falls below the lower long call strike at expiration. The short calls expire worthless to offset the lower wing call premium paid.

Capped Upside Risk

On the upside, if the stock surges above the higher long call strike at expiration, the higher call offsets the loss from the lower wing and short calls expiring in the money. Upside risk is defined.

Offsetting Greeks

The long calls have a positive delta and are hurt by time decay. But the negative delta short calls see gains as time passes. This creates a more stable position around the body strikes.

Volatility Dynamics

While volatility crushes long option premiums across all strikes, the impact is muted in a long butterfly. Lower volatility is ideal as the position decays over time.

Adjustment Flexibility

The legs are sometimes managed independently to defend or adjust. For example, closing the body short calls if the stock drops below the lower strike to eliminate downside exposure.

In terms of execution, a long call butterfly is sometimes traded as the following.

- A single net debit multi-leg order.

- Legging in by buying wings first, then shorting calls.

- As separate debit spreads by buying lower call vertical and higher call vertical.

To maximize chances of profitability, a long call butterfly is best initiated for the following.

- Low implied volatility stocks with options exhibiting cheaper premiums.

- Range-bound stocks trading directionless within a channel.

- Times of low upcoming uncertainty, like before an earnings gap.

- Near-term expiration for faster time decay of premium.

The mechanics behind a long call butterfly center around defined risk management. The wings combine with the short calls to create a tent-like payoff diagram. This exhibits a single maximum profit price point.

Understanding the interplay of the long and short calls is key to deploying long call butterflies successfully. The evidence demonstrates this multi-leg strategy relies on leveraging option Greeks dynamically across the strikes. The long call butterfly is a great risk-defined options trading technique when implemented properly.

How effective is Long Call Butterfly?

The long call butterfly is an effective options trading strategy when used properly and under the right market conditions. The construction of buying a lower strike call, selling two middle strike calls, and buying a higher strike call creates a unique risk-reward profile with efficiency benefits compared to other approaches.

A primary reason the long call butterfly is effective is that it offers defined risk. The maximum loss is limited to the net debit paid upfront to create the spread. This gives the trader an efficient use of capital since the risk is known on entry.

The maximum gain is also well-defined. It is capped at the difference between the wing strikes minus the initial debit. While profits are limited, it is an efficient use of capital to earn the maximum return.

The long call butterfly is constructed at a lower cost than buying calls outright since the sold calls help offset the price. This means capital is used more efficiently to establish the trading position.

Looking at hypothetical examples sometimes quantifies the potential efficiency rate.

- Stock at Rs. 50

- Buy 40 strike calls for Rs. 2

- Sell two 50-strike calls at Rs. 1 each

- Buy 60 strike calls for Rs. 2

- Net debit Rs. 2

In this case, the max loss spending of Rs. 2 means only Rs. 2 of capital is at risk. A Rs. 10 potential profit represents a 5:1 reward-to-risk ratio on capital used.

The maximum profit would be Rs. 10 if the stock closes at Rs. 50 at expiry. This represents a 500% return on the capital risked.

- Stock at Rs. 80

- Buy 70 calls for Rs. 5

- Sell two 80 calls at Rs. 3 each

- Buy 90 calls for Rs. 5

- Net debit Rs. 4

Here, the maximum risk is Rs. 4, but the maximum profit is Rs. 10 for an efficiency rate of 2.5:1 reward-to-risk. The potential profit of Rs. 10 represents a 250% return on capital at risk.

As the examples show, the long call butterfly offers efficient capital usage measured by the reward-to-risk ratio and return on investment metrics. Properly executed, positive efficiency rates are common.

The breakeven points also demonstrate efficiency. With defined maximum profit at the middle strike, breakevens at the wings mean only a moderate price move is required for profits. This contrasts with buying options outright, which need larger moves.

The reason long-call butterflies sometimes offer strong efficiency is because of the following combined characteristics.

- Lower cost exposure than outright option purchases.

- Defined and limited risk level.

- Favorable reward-to-risk ratios.

- Capped but good return on capital at risk.

- Breakevens only require moderate stock movement.

In terms of an efficiency rate, prospective long-call butterfly traders should look for opportunities with at least 2:1 reward-to-risk. A potential return on capital at risk of 100% or greater also indicates a favorable setup.

The main caveat is that if the stock moves well beyond the wings at expiration, the efficiency rate will decline. But used properly around events like an earnings announcement, the efficiency metrics are sometimes quite strong.

How do traders breakeven using Long Call Butterfly?

A long call butterfly spread has two breakeven points traders aim to reach in order to generate a profit on the strategy. The breakevens are determined by the wings of the butterfly – the bought lower strike call and higher strike call.

The lower breakeven is at the strike of the purchased lower wing call minus the net debit paid to establish the position. The higher breakeven is at the strike of the purchased higher wing call minus the net debit.

For example, a trader sets up a long call butterfly as follows.

- Buy 1 Rs. 90 call

- Sell 2 Rs. 100 calls

- Buy 1 Rs. 110 call

- Net debt paid is Rs. 2

The lower breakeven point would be Rs. 90 – Rs. 2 = Rs. 88

The higher breakeven point would be Rs. 110 – Rs. 2 = Rs. 108

The Rs. 2 debit is the maximum loss that may be incurred if the stock price is less than Rs. 88 at expiration. The maximum loss is also incurred if the stock is higher than Rs. 108 when the option expires.

To break even or make a profit, the stock needs to be between the two breakeven points at expiration. The maximum profit occurs if the stock settles exactly at the middle strike price of Rs. 100.

As the stock price moves away from the middle strike toward the wings, the potential profit decreases. Right at the breakeven points, the profit/loss on the long call butterfly is zero.

Six key points about how breakeven is achieved are listed below.

- Requires stock to be between the breakeven points at expiration.

- Lower breakeven is lower wing strike minus debit.

- Higher breakeven is higher wing strike minus debit.

- Maximum profit attained at middle strike price.

- Profit declines as the stock moves away from the middle strike.

- At breakeven, profit/loss is zero on the position.

In addition to the stock settling between the breakevens at expiration, breakeven sometimes occurs earlier if volatility declines enough during the life of the trade.

As time passes and expiration approaches, the time value portion of the option premium decays. This time decay benefits a long call butterfly. The short calls at the middle strike have the most time value baked into the premium.

The middle strike short calls depreciate more quickly than the lower and higher strike long call wings if implied volatility drops significantly before expiry. This sometimes pushes the position to breakeven or a small profit prior to expiration.

For example, if a long call butterfly is established for a net debit of Rs. 200, and the short calls subsequently decline by Rs. 100 in premium, the mark-to-market value of the position could be near Rs. 100 profit. This could allow the trade to be closed early at breakeven or better.

How to construct a Long Call Butterfly strategy?

The long call butterfly is a flexible strategy that is used as often as opportunities arise in alignment with a trader’s approach and risk tolerance. While there is no perfect frequency, some guidelines do help determine appropriate timing between trades.

The market conditions and technical setup required for a high probability long call butterfly only emerge occasionally for a given underlying stock. Traders should patiently watch for the right circumstance rather than trying to force frequent butterfly trades.

Some traders use the strategy around scheduled events like an earnings release when the market is pricing in a potential move followed by mean reversion. This sometimes only allows one or two trades per quarter on a particular stock.

However, across a diversified portfolio of equities, setting up butterflies on different names whenever the ideal conditions appear for each stock provides more frequent usage overall. Monitoring markets across sectors, industries, and indexes expands potential opportunities.

Some active option traders implement long-call butterflies when they have a directional forecast but want a defined risk. This systematic approach sometimes results in trades every few weeks or monthly, depending on the volatility of the underlying. The key is objectively defining when the criteria are met rather than randomly trading.

Swing traders utilize butterflies to capture moves over one to four weeks. For stocks in consistent uptrend or downtrend channels, butterflies are generated at a frequent pace. The challenge is avoiding complacency about continually meeting the criteria.

Traders should be wary of overusing long-call butterflies or forcing frequency. Each trade should be taken independently on the merit of its structure and conditions rather than chasing premiums or shooting for a target number of trades.

It’s better to be patient and wait for a few quality setups per month or quarter than to make butterfly trades every week out of habit. Frequent trading also racks up more commissions compared to taking fewer but higher conviction trades.

The ideal frequency depends on factors like the following.

- Active universe of underlying stocks monitored.

- Volatility levels across different sectors.

- Risk tolerance and butterfly sizing.

- Combined with other strategies in the playbook.

- Time committed to actively seeking opportunities.

A part-time retail trader sometimes only employs a couple of butterflies per quarter on stocks they follow closely. A professional volatility arbitrage trader sometimes utilizes butterflies multiple times per week across a diverse set of tradable securities.

The frequency could also vary over time based on macro conditions. Periods of higher volatility or churning markets present more chances to capitalize on butterfly opportunities.

How often can I perform Long Call Butterfly?

The long call butterfly is a flexible strategy that is used as often as opportunities arise in alignment with a trader’s approach and risk tolerance. While there is no perfect frequency, some guidelines do help determine appropriate timing between trades.

The market conditions and technical setup required for a high probability long call butterfly sometimes only emerge occasionally for a given underlying stock. Traders should patiently watch for the right circumstance rather than trying to force frequent butterfly trades.

Some traders use the strategy around scheduled events like an earnings release when the market is pricing in a potential move followed by mean reversion. This sometimes only allows one or two trades per quarter on a particular stock.

However, across a diversified portfolio of equities, setting up butterflies on different names whenever the ideal conditions appear for each stock provides more frequent usage overall. Monitoring markets across sectors, industries, and indexes expands potential opportunities.

Some active option traders implement long-call butterflies when they have a directional forecast but want a defined risk. This systematic approach sometimes results in trades every few weeks or monthly, depending on the volatility of the underlying. The key is objectively defining when the criteria are met rather than randomly trading.

Swing traders utilize butterflies to capture moves over one to four weeks. For stocks in consistent uptrend or downtrend channels, butterflies are generated at a frequent pace. The challenge is avoiding complacency about continually meeting the criteria.

In general, traders should be wary of overusing long call butterflies or forcing frequency. Each trade should be taken independently on the merit of its structure and conditions rather than chasing premiums or shooting for a target number of trades.

It’s better to be patient and wait for a few quality setups per month or quarter than to make butterfly trades every week out of habit. Frequent trading also racks up more commissions compared to taking fewer but higher conviction trades.

The ideal frequency depends on factors like the ones mentioned below.

- Active universe of underlying stocks monitored.

- Volatility levels across different sectors.

- Risk tolerance and butterfly sizing.

- Combined with other strategies in the playbook.

- Time committed to actively seeking opportunities.

A part-time retail trader only employs a couple of butterflies per quarter on stocks they follow closely. A professional volatility arbitrage trader sometimes utilizes butterflies multiple times per week across a diverse set of tradable securities.

The frequency could also vary over time based on macro conditions. Periods of higher volatility or churning markets present more chances to capitalize on butterfly opportunities.

When should I enter using the Long Call Butterfly strategy?

Determining the ideal entry points is crucial for long-call butterfly trading success. Traders aim to initiate butterflies when market conditions offer the highest probability of the stock finishing within the wings at expiration.

Prime times to enter long call butterflies include the following.

Pre-Earnings Announcements

Volatility typically rises in earnings as the market prices are uncertain. Initiating a butterfly just before earnings allows for benefiting from the volatility surge. Post-earnings implied volatility will contract rapidly, accelerating time decay to potential profit.

Range Bound Price Action

A stock that oscillates between obvious support and resistance levels while trading sideways denotes uncertainty and a bias in neither direction. Entering a butterfly when the stock is range bound maximizes the chance of remaining within the wings at expiry.

Elevated but Declining IV

Richer premiums are offered when creating the wings and body when implied volatility is expanded to the upside. A lengthy butterfly scenario is useful if IV is predicted to decrease after entrance.

Legging In From Debit Spreads

Legging in by initially buying a call debit spread allows benefiting from some upside momentum. The extra wing is sometimes sold to convert the option into a long call butterfly if the stock approaches the higher strike.

Fed Announcements

Indecisive markets ahead of Fed decisions offer uncertainty in direction but expectation of a sizable move. Initiating long butterflies heading into the announcement provides a low-cost means to capture the unknown move.

Peak Fear or Greed

At excessive bearish or bullish sentiment extremes, the high emotion makes a reversal more likely. Entering a butterfly near peak fear or greed improves the odds of directionless trading.

Unclear Directional Bias

It is desirable to deploy butterflies when the dominant trend is waning and momentum indicators show ambiguity in direction since this indicates a probable transition to range-bound behavior.

In contrast, situations to generally avoid initiating long call butterflies include the ones listed below.

Strong Trending Markets

Sustained directional trends with little pullback increase the odds a stock finishes outside the wings. It is prudent to wait for range-bound conditions to emerge.

High Implied Volatility

Rich premium from elevated IV hurts the cost of establishing the wings. Waiting for IV to cool off first optimizes entry timing.

Pre-Market Moving Events

Butterflies are vulnerable to substantial adverse moves around binary events like clinical trial results or merger news. It is wise to avoid deployment into such uncertainties.

Earnings Misses or Beats

The expanded move after a significant earnings surprise exceeds the wings, resulting in maximum loss. Allow the heightened volatility to subside before utilizing a butterfly.

Leg In at Higher Wing

Entering the upper wing leg after a large upside run takes the stock outside the profitable range. It’s better to leg in closer to the lower wing strike.

The ideal entry is when volatility has crested and is expected to contract according to probabilities and quantitative analysis. Developing the discipline and analysis skills to identify these opportunities is crucial for successfully trading long-call butterflies.

When should I exit using the Long Call Butterfly strategy?

Determining opportune exit points is essential for long-call butterfly success. Traders aim to close butterflies when the probabilities shift against the ideal range-bound outcome between the wings at expiration.

Prime times to exit long call butterflies include the following.

50% Maximum Profit Taken

Closing the entire position after capturing 50% or more of the maximum profit allows benefiting while the trade has extrinsic time value remaining.

Breaking Out of Range

The range-bound argument is refuted if the stock aggressively breaks out above resistance or breaks down below support. Exiting at the breakdown point mitigates further losses.

Rising Implied Volatility

Surging IV increases the premium value across the strikes, hurting P/L. It is prudent to unwind the position if volatility expands rapidly after entry.

Pre-Catalyst Events

The increased uncertainty justifies quitting butterflies early to escape the unknowable conclusion if a significant binary event, such as an FDA decision or court judgment, is approaching.

Double Maximum Loss

Letting losses accumulate beyond 100% of the maximum loss is throwing good money after bad. Close the trade if the loss exceeds 2x the original max loss amount.

Legging Out

Legging out by buying back the profitable short calls first locks in gains from that portion while additional time value remains on the wings.

Rolling

Rolling out the position in time preserves the structure while reaping the benefits of extra time decay if the stock stays range-bound, but expiry is drawing near.

In contrast, situations to avoid early butterfly exits include the ones listed below.

Chasing Performance

Exiting simply because the position is briefly unprofitable fails to allow the intrinsic value to be realized by expiration. Avoid overtrading.

Premature Close

Closing a butterfly with weeks remaining ahead of a known volatility event like earnings forfeits extrinsic value yet to decay.

Spikes Beyond Wings

Normal moves briefly outside the wings typically revert back unless there is a breakout. Avoid overreacting to temporary price action.

Max Profit Achieved

Exiting at the maximum profit center still forfeits unrealized time value. Keeping the position through expiry optimizes the trade.

While long call butterflies have defined exit at expiration, early and active trade management often improves results. The evidence demonstrates informed volatility and technical analysis optimizes timely butterfly exits.

How can I get out of Long Call Butterfly?

Getting out of a long-call butterfly spread involves methodically legging out of the position, closing the entire spread at once, or rolling the trade forward to avoid a loss. The optimal exit approach depends on factors like time remaining, transaction costs, and risk management preferences.

Legging Out

Legging out closes each option leg at different times to aim for an optimal exit price on each piece.

For example:

- Close lower strike long call when it reaches the 80% profit target.

- Close higher strike long call if stock rally exceeds upside breakeven.

- Let short calls expire worthless for maximum gain.

The goals are to lock in profits on winning legs, cut losses on losing legs, and avoid the bid/ask spread on closing the complete position at once.

Closing the Spread

This exits the entire long butterfly spread simultaneously by placing a closing order for the spread. The net credit or debit is calculated automatically based on the current bid/ask prices.

Benefits include taking advantage of remaining time value and avoiding legging out over multiple transactions. Drawbacks include bid/ask spread slippage and less control over each component.

Rolling the Position

The spread could be rolled out in expiry if the long call butterfly is at or close to its maximum loss with time left. This extends the trade at a net credit to avoid realizing the full loss.

For example, if the current long butterfly is Rs. 50 wide and a Rs. 100 loss, rolling it out one month for a Rs. 150 credit turns it into a Rs. 50 gain and avoiding loss.

Considerations for getting out of a long call butterfly are as follows.

- Leg out of Wings vs Body separately.

- Use daily volume patterns to optimize exit liquidity.

- Set conditional orders to automatically capture gains.

- Roll untested wings into new butterflies for a second chance.

- Close body if the stock moves outside the profit zone.

- Offset with other positions to hedge risks.

How much can I profit using Long Call Butterfly?

The maximum potential profit on a long call butterfly spread is limited but still provides an attractive return. The key factors that determine profitability are the wingspan between the strike prices, the net debit paid to enter the trade, and where the stock finishes at expiration.

A long call butterfly involves buying a lower strike call, selling two at-the-money calls, and buying a higher strike call. The maximum gain occurs if the stock finishes right at the middle strike price at expiration.

For example, Let’s take a stock at Rs. 50.

- Buy 1 Rs. 40 call

- Sell 2 Rs. 50 calls

- Buy 1 Rs. 60 call

The highest gain would be the spread between the wings of Rs. 20 – the initial Rs. 2 debit = Rs. 18 potential profit if established for a net debit of Rs. 2, and the stock ends at Rs. 50.

On a Rs. 2 investment, an Rs. 18 gain represents a 900% return on capital deployed for the trade. This demonstrates how long call butterflies generate sizable percentage returns from relatively small debit amounts.

The wider the spread between the wing strikes, the greater the potential profit. However, wider spreads also have higher debits, reducing the return multiple.

The highest gain on a Rs. 30 widespread would be Rs. 25 for a 500% return if the lower strike had been Rs. 30 instead of Rs. 40 in the case above.

So maximizing total profit potential involves balancing the wingspan versus the initial debit amount paid. Larger wing widths are not always optimal.

Factors impacting potential butterfly profits are the following.

- The width between wing strike prices.

- Net debit amount paid to establish trade.

- Where stock price finishes relative to the middle strike.

- Time remaining until expiration when trade is entered.

- Future volatility level compared to forecast.

A Rs. 100 wide butterfly entered for Rs. 10 debit would yield a maximum of Rs. 90 profit if the criteria are met. On a Rs. 10 risk, that is a 900% return, demonstrating the power of long-call butterflies.

It’s possible for profits to exceed the maximum if volatility declines substantially, enabling an early exit with remaining time value.

The key considerations for profiting from long-call butterflies are mentioned below.

- Balancing width of strikes vs initial debit amount.

- Targeting a return of at least 100% on capital at risk.

- Managing trade based on projected volatility path.

- Planning early exit if max profit target hit.

- Sizing butterfly position appropriately for risk tolerance.

With the defined risk-reward payoff, a long call butterfly implemented properly sometimes realistically achieves profits in the 100-1000% return range on capital deployed if stock settles near the middle strike at expiration. The limited but substantial profit potential makes it an attractive options trade.

How profitable is the Long Call Butterfly strategy in the long term?

Over the long run, properly constructed long call butterflies are a reasonably profitable options trading strategy. However, as with any trading approach, profits are not guaranteed, and maximum losses do sometimes occur. The limited risk nature provides an edge for prudent traders.

Expected Profitability

Historically, the probability of profit on a typical long call butterfly falls between 50-65% based on backtesting and trade studies when moderately favorable conditions are present.

This assumes butterflies are established with proper spread width fitting the expected move, 45-60 days to expiration, on range-bound stocks, and managed actively based on technical analysis rules.

With ideal construction, the win rate reaches 70%+ in bullish volatility environments. Conversely, poorly timed butterflies in choppy markets sometimes only achieve 40-45% success.

An average win rate of 55-60% on risk-defined butterflies represents satisfactory performance over time, provided winners exceed the size of losers.

Maximum Profit Potential

The maximum profit on a long call butterfly is equal to the formula stated below.

Strike Price of Short Calls – Strike Price of Lower Wing Call – Net Premium Paid

For example, a butterfly with short 100 strike calls, long 95 and 105 wing calls, and Rs. 2 net debit paid would have max profit as stated below.

Max Profit = Rs. 100 – Rs. 95 – Rs. 2 = Rs. 3

Maximum profits are achieved if the stock finishes precisely at the short strike price at expiration. Any finish outside the wings results in the maximum loss.

Maximum Loss Potential

The maximum loss on a long call butterfly is simply equal to the net premium paid to establish the position.

Using the example above, the maximum loss would be the Rs. 2 net debit, realized if the stock finishes below Rs. 95 or above Rs. 105 at expiry.

Over the long run, the capped risk limits butterfly losses. Profits sometimes substantially outweigh losers when properly leveraged and risk-managed.

How profitable is the Long Call Butterfly strategy in the short term?

In the short term, the profitability of the long call butterfly is mostly determined by the prevailing volatility environment and the trader’s skill in trade management. While maximum profits are limited, the maximum loss is defined, allowing for favorable short-term risk-reward.

The maximum possible profit on a long call butterfly in the short term is capped at the difference between the wing strike prices minus the net debit paid to enter the trade.

For example, if a 50-strike long call butterfly is established for a Rs. 2 debit with 40-50-60 strike legs, the maximum profit potential is Rs. 20 – Rs. 2 = Rs. 18.

This Rs. 18 max gain represents a 900% return on the Rs. 2 capital at risk on the trade. Short-term butterfly profits sometimes reach this maximum return if the underlying stock finishes very close to the middle strike price at expiration per the forecast.

More realistically, to consistently achieve strong short-term profitability on each butterfly trade, typical profit targets sometimes aim for 50-100% or more on capital deployed.

For a butterfly with a Rs. 100 max risk, reasonable short-term profit goals would be Rs. 50-150 or more. This equates to a 50-150% return on the capital allocated to the trade.

The maximum loss on a long call butterfly is simply the net debit paid when opening the position. This defined risk parameter allows prudent position sizing to limit short-term loss.

For example, if the trader keeps each butterfly trade to a 1% or less portfolio risk, then losses on any single trade are contained to that 1% allotment.

The keys to maximizing short-term butterfly profits are the ones listed below.

- Appropriate trade sizing and risk management.

- Discipline in taking quick losses when the forecast is incorrect.

- Letting profits run when volatility behaves as expected.

- Adjusting dynamically to changing market conditions.

- Optimizing the timing of entry and exit points.

- Scaling out of winning trades at target prices.

What are the advantages of using Long Call Butterfly?

The long call butterfly spread offers traders six important advantages that make it an attractive instrument under the right market conditions.

Defined and Limited Risk

The maximum loss on a long call butterfly is capped at the net debit paid upfront when establishing the spread position. This defined and limited risk allows traders to size positions accurately without exposure to uncapped losses. The ability to define risk in a volatile market environment is a key advantage.

Lower Cost Exposure

Long-call butterflies provide exposure to upside or downside stock moves at a lower cost than simply buying calls or puts outright. The short calls sold at the body of the butterfly help offset the cost of the wings. The lower capital outlay sometimes allows participation in a greater number of opportunities.

Profit Zone Flexibility

Traders have flexibility in customizing the upside and downside profit zones through strike selection when constructing the long call butterfly. The wings are sometimes made wider or narrower depending on the expected range of stock movement. This tuning of the risk-reward profile provides an advantage over single-option strategies.

Capital Efficiency

The limited risk and lower cost exposure of long call butterflies provide efficient use of account capital. Less capital is tied up for each position compared to other strategies, given the defined and capped risk parameters. The remaining capital is sometimes deployed elsewhere while the long butterfly trades.

Built-In Exit Strategy

The maximum gain is achieved if the stock settles precisely at the short strikes in the body of the butterfly at expiration. This defined outcome provides a natural profit target and exit strategy. No guesswork is required for ideal timing and taking profits.

Favourable Time Decay

Time decay tends to work in favor of a long-call butterfly position, given the short options sold in the body. The passage of time allows the trader to capture additional gains if the forecast proves accurate. This differs from options buying strategies.

The structure of long-call butterflies strategically utilizes options to provide exposure to stock movements while reducing and defining risks. Once implemented carefully, this technique offers a desirable risk-reward profile with a number of benefits over alternative methods.

What are the disadvantages of using Long Call Butterfly?

While the long call butterfly offers advantages, there are also seven important challenges and disadvantages traders should understand before implementation.

Capped Profit Potential

The maximum gain on a long call butterfly is limited to the wingspan width less the initial debit paid. Even if the underlying stock makes a hugely favorable move, the butterfly trader only earns the defined maximum profit. The inability to capture unlimited upside profits is a disadvantage.

Narrow Profit Zone

The stock price must finish very close to the short strike prices at expiration to achieve the maximum profit. Profits decrease if the price closes much above or below the short strikes. The narrow profit range leaves little room for error in forecasting the price movement.

Loss of Time Value

The loss of the remaining time value will have a negative effect on the P/L if the trader needs to close the position before expiry. Earlier exits do not capture the full-time decay benefit of the position. This sometimes cuts into potential gains.

Uncapped Downside Between Strikes

While the maximum loss is defined at the debit amount, if the stock price settles between the wings at expiration, uncapped losses occur below the initial capital outlay. This risk of uncapped downside between strikes is a disadvantage.

Wide Bid/Ask Spreads

Depending on option liquidity and volatility, the bid/ask spreads on long call butterflies are sometimes wide. Higher transaction costs must be overcome to generate a profit and limit the frequency of trading.

Inability to Participate in Reversals

A long butterfly is unable to profit if the stock reverses course while the transaction is open since it is in a net negative position. This limits profit potential in whipsaw markets.

Trade Timing Difficulty

It is sometimes challenging to properly time entry points, recognize early exit signals, and optimize expiration management. Mistimed butterfly trades are prone to losses.

While defined and limited risk helps mitigate disadvantages, traders should incorporate prudent position sizing, risk management, stop losses, and be selective with trade entry points. An understanding of both advantages and disadvantages leads to a more informed use of this strategy.

Is using Long Call Butterfly risky?

The long-call butterfly options strategy carries a defined and capped risk profile, making it less risky than many other option strategies. However, there are still important risks to consider, especially for beginner traders.

The maximum loss on a long call butterfly is limited to the initial net debit paid to establish the spread position. This defines and quantifies the worst-case downside scenario. The risk is known upfront before entering the trade.

However, the probability of achieving the maximum profit is low, given the requirement for the stock to finish precisely at the short strike price at expiration. More commonly, the trade sometimes loses some portion of the initial debit amount.

While the dollar risk is defined, beginners should be cautious of over-leveraging and risking too large a percentage of capital on any single butterfly trade. Picking the wrong stocks or mismanaging the trade timing sometimes leads to the maximum loss being realized.

There are also challenges around execution costs, given the multi-leg structure of the strategy. The bid/ask spreads on the options sometimes eat into potential profits, especially if trades have to be exited early. This makes profitability more difficult.

Is it hard to use Long Call Butterfly?

The long call butterfly spread has some inherent complexities that sometimes make it a more challenging options strategy, especially for beginner traders. However, with education and practice, it is an accessible strategy.

Constructing the multi-leg butterfly spread requires precision in both strike prices and timing of entry/exit. Small mistakes sometimes turn a potential winning trade into a loser. This demands more focus and skill than buying a call or putting it alone.

Beginners also struggle with visualizing the risk-reward payoff diagram and probability of profit analysis. Understanding where and when the trade gains or loses requires foundational options knowledge.

Managing the position over time as market conditions change adds further complexity. Decisions around early exits, rolling untested wings, and extracting maximum value require experience.

In addition, finding ideal trading opportunities has its challenges. Butterfly contracts themselves tend to be less liquid. Pinpointing the right entry and foreseeable volatility contraction takes practice.

However, while the long call butterfly is more advanced than buying calls or puts, it is manageable for intermediate traders willing to learn through small positions.

The key concepts of defined risk, favorable time decay, and volatility mean reversion are grasped with the study. Gaining experience in assessing conditions and managing trades further builds competency.

Is Long Call Butterfly the most effective Butterfly spread strategy?

The long-call butterfly is an effective strategy but not necessarily the universally best butterfly spread in all market conditions. Other butterfly techniques sometimes are more effective depending on the trader’s forecast and risk preferences.

The long call butterfly has defined limited risks and achieves maximum profit if the underlying expires at the short strike price. This makes it attractive for high-probability scenarios predicting consolidation or range-bound prices.

However, the long-call butterfly lacks unlimited profit potential. The maximum gain is capped at the difference between wing strikes less the debit paid. Other butterflies sometimes provide a greater upside if the trader has a forecast beyond the wings.

For instance, a long condor butterfly involves wider wing strikes, allowing for unlimited gains if the underlying price moves outside the outer wings. This comes at a higher net debit cost but sometimes does warrant it.

The short iron butterfly has a lower cost of entry and achieves maximum profit if the stock finishes outside the wing strikes at expiration. This is sometimes more effective for directional breakout forecasts.

A short-call butterfly gains profit from a move lower or sideways drift. For bearish outlooks, it is sometimes superior to a long-call butterfly.

Overall, the most effective butterfly spread depends greatly on the factors listed below.

- Directional or range-bound forecast.

- Risk tolerance and capital considerations.

- Skew in put/call volatilities impacting pricing.

- Liquidity differences across option contracts.

The long call butterfly is quite versatile for moderately bullish outlooks and is effective with proper construction. But insisting on only this type of butterfly in all cases sometimes leaves profit opportunities on the table or risks losses.

What is the difference between Long Call Butterfly and Short Call Butterfly?

Long and short-call butterflies have distinct risk-reward profiles and are used in different market environments based on the trader’s forecast. The key differences include the following.

Long-call butterflies have a net debit cost paid upfront to enter the trade. Short-call butterflies take in a net credit when opened for no upfront cost. The long structure risks the debit amount, while the short risks the credit received.

The maximum gain on a long butterfly is capped at the difference between the wing strike prices and the debit amount paid. The maximum profit on a short butterfly is limited to the initial credit received. The short often has a lower upside.

The long butterfly’s maximum loss is defined as the initial debit amount. But the short butterfly has unlimited loss beyond the credit received if the stock finishes outside the wings. The long butterfly benefits from defined risk.

A long butterfly has two breakeven points at the wing strike prices. The short butterfly has one breakeven – the body strike price. This wider breakeven range makes the long butterfly less sensitive to price moves.

Long butterflies are anticipating low volatility or a move toward the body strike price. Short butterflies are positioned for high volatility or a drift outside the wings. Different directional biases are required.

Long butterflies perform better in range-bound, flat, or downward-trending markets. Short butterflies favor strongly trending or volatile markets. The environment impacts strategy selection.

Time decay benefits the long butterfly through expiration as the short strikes decay faster. Time decay hurts the short butterfly as the body value erodes. The passage of time has opposite effects.

The defined and limited risk long butterfly allows easier loss quantification and position sizing. The short butterfly’s uncapped downside requires strict loss management.

The key differences come down to cost, risk parameters, breakeven points, market environment fit, and assumptions on future volatility. Selecting the appropriate structure for each forecast is crucial to success.

What is the difference between Long Call Butterfly and Short Put Butterfly?

Long-call butterflies and short-put butterflies have differing risk-reward profiles and are used in various market conditions based on the trader’s outlook. The main differences include the following.

The long call butterfly buys a lower strike call, sells two at-the-money calls, and buys a higher strike call. The short put butterfly sells a higher strike put, buys two at-the-money puts, and sells a lower strike put. Different legs are bought/sold.

Long call butterflies require a net debit paid upfront to establish the spread position. Short-put butterflies take in a net credit when opened for zero upfront cost. The long risks the debt, while the short risks the credit.

The max gain on the long call butterfly is capped at the difference between the wing strikes less the debit amount. The max profit on the short put butterfly is limited to the initial credit received. The short often has lower upside potential.

The long call butterfly has defined limited risk up to the initial debit paid. But the short put butterfly has uncapped loss beyond the credit if the stock drops below the lower wing. The long structure benefits from limited downside.

The long call butterfly has two breakeven points at the wing strike prices. The short-put butterfly has one breakeven – the body strike. This tighter range makes the short more sensitive to price moves.

Long-call butterflies match range-bound or moderately bullish outlooks. Short-put butterflies favor bearish scenarios anticipating downside moves. Each strategy has different ideal conditions.

The defined risk long call butterfly is generally simpler to manage with quantifiable loss limits. The uncapped risk short-put butterfly requires strict, disciplined loss management to prevent runaway losses.

Differences in construction, cost, risk parameters, breakeven points, environment fit, and complexity management make proper strategy selection essential based on market forecasts and risk tolerance.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 32")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.