The Broken Wing Butterfly (BWB) is an options spread that adjusts the traditional butterfly to shift risk and reward, offering strategic flexibility for traders seeking asymmetric payoffs. The BWB modifies the standard butterfly by widening one “wing,” which removes risk on one side and shifts the breakeven point, often allowing for a zero-cost or even credit entry.

The history of the Broken Wing Butterfly traces back to advanced options traders looking for ways to benefit from range-bound or moderately trending markets without the risk of large losses on both sides.

What is a Broken Wing Butterfly?

A Broken Wing Butterfly is an options strategy where one wing of a traditional butterfly spread is widened, creating an asymmetric risk/reward profile with limited risk on only one side. Broken Wing Butterfly modification is achieved by either moving the upper or lower long option further away from the body, breaking the perfect symmetry of a classic butterfly.

In a typical butterfly, the trader buys one in-the-money (ITM) option, sells two at-the-money (ATM) options, and buys one out-of-the-money (OTM) option, with equal distances between strikes. The Broken Wing Butterfly alters this by increasing the distance on one side, resulting in the “broken” wing.

This transformation shifts the breakeven point, often reducing or eliminating the cost of entry, and alters the payoff shape so that risk exists only on the side with the wider wing.

How Does a Broken Wing Butterfly Work?

A Broken Wing Butterfly works by creating an options spread with one wing wider than the other, shifting the risk and reward so that a trader profits if the underlying closes near the short strikes and faces limited risk only on the broken side.

The payoff profile is unbalanced, with the potential for a net credit or zero-cost entry.

The dynamics are straightforward: the trader buys one ITM/OTM option, sells two ATM options, and buys one further OTM/ITM option at a different distance from the body, creating the broken wing. This setup allows the trader to profit if the price lands near the short strikes, while only risking loss if the market moves sharply past the broken wing.

For instance, NIFTY is at ₹22,000, a trader may buy one ₹21,700 put, sell two ₹22,000 puts, and buy one ₹21,500 put. Here, the lower wing is “broken” by making it 200 points wide instead of 150, which can result in a net credit at entry.

The maximum profit is realized if NIFTY expires at ₹22,000, while the maximum risk is only if it drops below ₹21,700, and is limited to the distance between the short and far long strike, minus any collected credit.

The unbalanced structure means the reward-to-risk ratio is skewed, often favoring the trader with higher probability of a small win and only a slim chance of a larger, but known, loss. Some traders use this edge to repeatedly collect small credits, accepting the occasional capped loss.

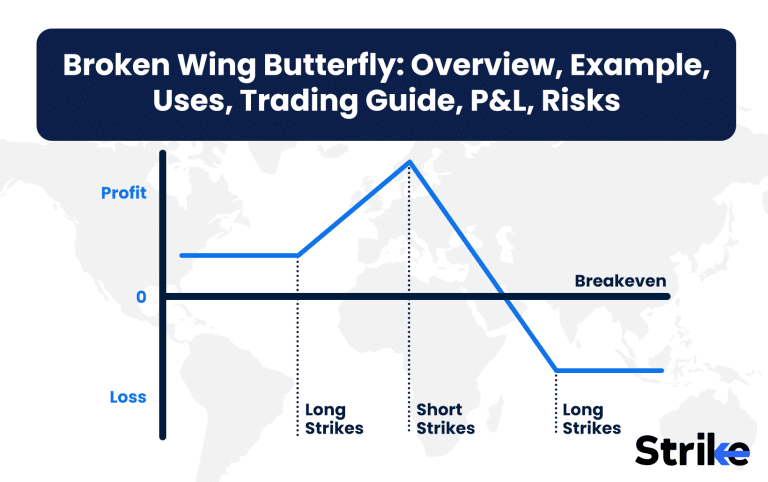

Below is a simple payoff diagram to show the structure.

This visual makes it clear: profit is highest at the short strikes, risk is only on the broken wing, and the rest is flat or slightly profitable.

Why Use a Broken Wing Butterfly Strategy?

The Broken Wing Butterfly is used for its lower maximum loss compared to traditional butterflies, improved breakeven potential, cost-efficient directional bias, and higher probability of profit.

Traders are attracted to this strategy because it shifts risk to just one side, allowing for a more favorable risk/reward dynamic. See the image below.

One of the primary advantages is that the BWB can often be entered for a net credit or at zero cost, especially when implied volatility is favorable.

This means the trader does not need the underlying to move much to realize a gain, and sometimes even a move against the position does not result in a loss. The defined risk on one side allows traders to hold positions with greater confidence, knowing that a catastrophic loss is not possible.

The breakeven point for a BWB is usually more favorable than a standard butterfly, thanks to the shifted wing.

This gives the position a better chance of being profitable, even if the underlying does not settle exactly at the body strike. For traders with a moderate directional view, the BWB offers a way to express that view with lower risk and higher reward-to-risk ratios than many other option spreads.

When to Use a Broken Wing Butterfly?

A Broken Wing Butterfly is most effective when you expect moderate directional movement, have a neutral-to-bullish or neutral-to-bearish bias, and want to benefit from time decay in low volatility environments.

The setup thrives in markets where large, unexpected moves are unlikely.

Ideal scenarios for deploying a BWB include periods before earnings announcements, major economic data releases, or central bank decisions, when implied volatility is elevated but a controlled move is anticipated.

The structure allows traders to profit from both time decay and a move toward the short strikes, while limiting risk if the market surprises in one direction.

BWBs are also popular when traders want to avoid the high capital outlay and risk of traditional spreads but still desire a meaningful profit opportunity. The strategy’s design is well-suited for sideways markets with a slight tilt, where theta decay steadily erodes option value and the underlying is unlikely to breach the broken wing.

This approach is less effective in highly volatile or trending markets, where the risk of a large, adverse move is greater. By carefully choosing the direction and width of the broken wing, traders can tailor the position to their specific market view and risk appetite.

How Option Greeks Affects Broken Wing Butterfly?

The Greeks play a key role in the Broken Wing Butterfly, with the strategy showing small directional delta, positive theta, slightly negative vega, and low gamma except when price nears the short strike at expiration. Each Greek impacts the trade differently at entry versus near expiry.

Delta is modestly positive for bullish BWBs and slightly negative for bearish setups, reflecting the directional tilt. The position earns positive theta, benefiting from time decay, as the value of the short options erodes faster than the long options, especially when the market stays near the short strikes.

Vega is usually slightly negative, so the BWB profits if implied volatility drops after entry. Gamma is low for most of the trade’s life but increases sharply if the underlying nears the short strikes at expiry, making the P&L more sensitive to small price changes in the final days.

Below table shows the Greek impact at entry and near expiry.

| Greek | At Entry | Near Expiry (Near Short Strike) |

| Delta | Small (±) | Increases in direction of bias |

| Theta | Positive | Highest near short strikes |

| Vega | Slightly negative | Insensitive near expiry |

| Gamma | Low | Spikes if near short strike |

This helps traders manage risk and optimize adjustments as expiry approaches.

How Implied Volatility Affects Broken Wing Butterfly?

Broken Wing Butterflies are best opened when implied volatility is low, as lower IV makes option premiums cheaper and reduces the cost of setting up the spread. If IV drops after opening, the position typically benefits.

Ahead of major events like earnings, implied volatility often spikes, inflating option prices. Entering a BWB just before such events, when premiums are rich, is less attractive. However, after the event, an IV crush can make the position profitable, even if the underlying doesn’t move much.

Unlike Iron Condors, which suffer during volatility expansions, or Straddles, which require big moves to profit, the BWB’s risk is isolated to one side, making it more forgiving. The BWB profits from both time decay and a drop in IV, but is less sensitive than naked short premium strategies.

How to Trade using Broken Wing Butterfly?

Let us look at how to trade using a broken wing butterfly through an example.

This strategy involves a broken wing butterfly spread created using Nifty options. The position comprises selling two call options at the 24650 strike for ₹60.9 each, buying one lower strike call at 24600 for ₹79.2, and one higher strike call at 24800 for ₹28.0. The lot size is 75.

To calculate the net premium, we add the premiums paid for the two long calls and subtract the premium received from the two short calls. This gives us: ₹79.2 + ₹28.0 − (2 × ₹60.9) = ₹107.2 − ₹121.8 = −₹14.6. Since the result is negative, the strategy is initiated for a net credit of ₹14.6 per lot.

The maximum profit for this setup occurs when the underlying closes exactly at the short strike price of 24650. At that point, the 24600 call will be worth 50 points, and the other options will expire worthless. The max profit is calculated as the difference between the short and lower long strike multiplied by the lot size, plus the net credit received. That is, (24650 − 24600) × 75 + 14.6 × 75 = ₹3,750 + ₹1,095 = ₹4,845.

The maximum loss happens when the underlying closes at or above 24800. In this case, both short calls and the higher long call become in-the-money, but the short position outweighs the protection from the long 24800 call. The loss is determined by subtracting the net credit from the width between the short and higher strike, and multiplying by the lot size: (24800 − 24650 − 14.6) × 75 = (135.4) × 75 = ₹10,155.

The breakeven point is where the strategy neither gains nor loses. For a net credit broken wing butterfly, this typically occurs at the short strike plus the credit received. So, the breakeven is 24650 + 14.6 = ₹24714.6, which can be rounded to ₹24714.

What are the Maximum Profit & Loss on a Broken Wing Butterfly?

Maximum profit on a Broken Wing Butterfly is the difference between the middle and long strike minus the net debit (or the full credit if opened for a credit), while maximum loss is the distance between the short and broken wing minus any received credit. Let’s use an example for clarity.

Suppose you set up a call BWB on NIFTY: buy 1 lot ₹22,000 call (pay ₹95), sell 2 lots ₹22,500 call (receive ₹60 each), buy 1 lot ₹23,200 call (pay ₹10). The net premium paid is ₹95 + ₹10 – (₹60 + ₹60) = -₹15, so you receive a ₹15 credit.

Maximum Profit:

Middle strike (₹22,500) – long strike (₹22,000) – net debit

= ₹500 – (–₹15) = ₹515 (or simply the full credit, if the wings are set to allow only credit as max profit).

Maximum Loss:

Broken wing distance (₹22,500–₹23,200 = ₹700) – net credit

= ₹700 – ₹15 = ₹685

This structure means you have a capped loss on one side and a higher chance of a smaller profit if the underlying settles near the short strikes.

What are the Risks of Broken Wing Butterfly?

The main risks of a Broken Wing Butterfly are exposure on the broken wing side, the need for precise strike selection, poor performance in volatile or trending markets, and liquidity risks when options are thinly traded. The structure protects you on one side, but if the underlying moves sharply through the broken wing, losses occur.

Losses are limited but real if the underlying moves sharply through the broken wing. This risk is the primary trade-off for the strategy’s favorable risk/reward profile.

Picking the wrong strikes reduces profit potential or increases the chance of loss. Effective strike placement is crucial to maximize edge.

Unexpected large moves in the underlying can breach the broken wing, quickly turning a high-probability trade into a maximum loss. The BWB works best in stable or moderately directional environments.

Wide bid-ask spreads or low open interest increase transaction costs and slippage. Exiting or adjusting the position might be difficult in illiquid contracts.

Short options might be assigned before expiration, leading to unwanted long or short positions. This is especially likely near ex-dividend dates or expiry.

Making repairs or rolling the position is harder if the market moves quickly against the trade. Complex adjustments may increase risk or transaction costs.

Brokers can raise margin unexpectedly, forcing early closure or additional capital. This is more likely during periods of market stress.

Earnings, policy decisions, or geopolitical shocks can cause rapid price moves beyond the broken wing. The strategy’s risk protection does not cover such extreme events.

Watching the position closely might tempt traders to over-manage or exit too early. Emotional responses can erode the strategy’s statistical edge.

Is Broken Wing Butterfly Strategy Profitable?

Yes, the Broken Wing Butterfly is often profitable when the underlying price finishes near the short strikes and the setup is entered for a credit or minimal debit. Its high probability of profit comes from the forgiving payoff structure, though large losses can occur if the broken wing is breached.

Profitability depends on market selection, timing, and proper management. Consistent use in stable markets with good premium yields steady results for experienced traders.

Is Broken Wing Butterfly Bullish or Bearish?

A Broken Wing Butterfly is either bullish or bearish depending on which options you use and how you structure the strikes. Bullish BWBs use calls with the broken wing above the market; bearish BWBs use puts with the broken wing below.

This flexibility allows you to express a directional bias while keeping risk defined and reward asymmetric.

What are Alternatives to Broken Wing Butterfly Strategy?

Alternatives to the Broken Wing Butterfly include the standard butterfly, iron condor, ratio spread, and credit spreads, each offering a different risk/reward and complexity profile. The standard butterfly features equal wings and a centered payout, while iron condors provide a wider range with similar risk.

Ratio spreads are more aggressive and directional, offering larger potential profits at the cost of higher risk. Credit spreads are simpler and easier to manage but offer lower reward-to-risk ratios. Here’s a comparison table.

| Strategy | Max Profit | Max Loss | Greeks | Cost | Complexity |

| Broken Wing Bfly | Moderate | One side | Pos. theta | Zero/credit | Moderate |

| Standard Butterfly | Moderate | Both sides | Pos. theta | Debit | Moderate |

| Iron Condor | Low | Both sides | Pos. theta | Credit | Moderate |

| Ratio Spread | High | Unlimited | Directional | Credit/Debit | High |

| Credit Spread | Low | One side | Pos. theta | Credit | Low |

Each alternative suits different market views, risk profiles, and experience levels, so it’s important to match your strategy with your objectives and comfort with risk.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 16")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 17")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 18")

: Overview, 10 Types of Indicators, Settings for Different Markets 19")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 22")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 25")

No Comments Yet.