A long call condor is an options strategy that involves buying an at-the-money (ATM) call while simultaneously selling an out-of-the-money (OTM) call and an even further OTM call. A long call condor aims to profit from low volatility in the underlying stock price.

To construct the trade, a trader buys a call at the current market strike price. They then sell a higher OTM call and sell an even higher call. This creates a range between the two short call strikes, where the position makes money if the stock closes at expiration.

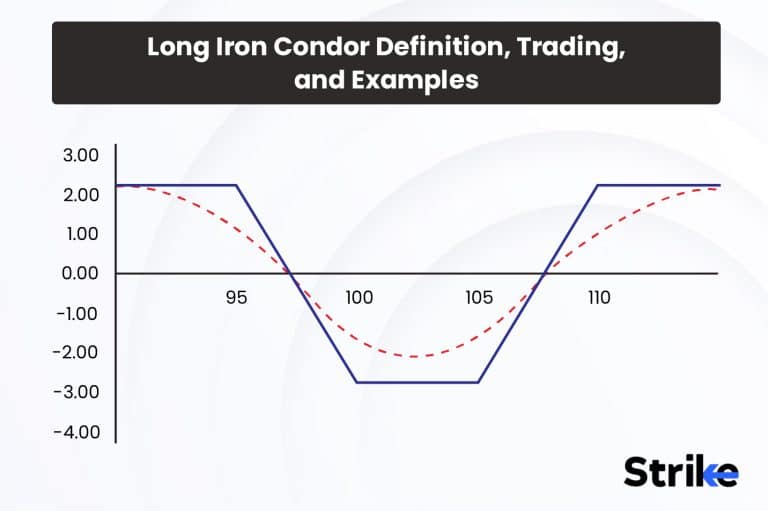

The maximum profit is achieved if XYZ closes at either the short call strikes of $105 or $110. The maximum risk is limited to the net debit paid to open the trade. A long condor is bullish below the short strikes but benefits most if the stock stays stable, allowing time decay to favor the position. It’s an effective strategy for capturing upside in a range-bound market.

What is a Long Call Condor?

A Long Call Condor is an options strategy that uses a combination of call options to generate income from an underlying security that is expected to be range-bound over the near term. A long call condor involves selling two out-of-the-money calls with the same expiration date while simultaneously buying a further out-of-the-money call and a call closer to being in-the-money.

The structure of this trade aims to profit from the underlying asset finishing between the call strikes at expiration. Establishing call spreads on both sides of the current price creates a range in which the net position remains profitable. The premium received from selling the further out calls helps offset the costs of the protective calls purchased. As long as the stock closes within this predefined range, the maximum profit potential is captured while the loss is limited.

More specifically, to establish a Long Call Condor, an investor could sell one call with a high strike price or sell one call with a lower strike price, or else buy one call with a strike below the lower sold call and buy one call with a strike above the higher sold call. All calls must have the same expiration date. This setup resembles the wingspan of a condor, hence the name.

Establishing call spreads above and below the current market price defines the acceptable range where the position remains in the money. The two sold calls generate a premium, which is used to purchase protection via the further-out calls. At expiration, all calls expire worthless except one long leg, which is exercised or sold for its intrinsic value if the underlying price ends within this range.

The maximum profit on a Long Call Condor is capped and occurs if the stock finishes precisely between the two bought call strikes at expiration. This captures the full credit received from selling the calls. The maximum loss is limited to the net debit paid to open the trade, which occurs if the stock moves violently above the upper call strike or below the lower call strike.

What is the overall goal of Long Call Condor?

The primary overall goal of implementing a Long Call Condor strategy is to generate profits from the inherent time decay that naturally occurs as options approach expiration. It allows traders to take a neutral, non-directional position on the underlying asset and benefit from price stability or a minor degree of upside movement over the term of the trade.

A key attribute of options is that they lose value simply due to the passage of time. As each day goes by, the likelihood of an option expiring in the money diminishes. This natural time decay is greatest for options that are near at-the-money and far from expiration. The Long Call Condor capitalizes on this time decay effect by selling (writing) call options that are closer to the current price of the underlying asset. These “short calls” will experience more rapid declines in premium value from theta erosion compared to further out-of-the-money calls.

By establishing positions both above and below the short calls through simultaneously buying calls at lower and higher strikes, the trader creates a range within which time decay of the sold options generates profits. The long calls act as hedges to limit downside risk if the underlying moves dramatically. The ideal scenario that realizes maximum gains occurs if the price finishes precisely at the strike of the short calls on expiration. In this outcome, the short calls expire worthless, but the trader retains the full premium collected from writing them. The long calls have no intrinsic value.

What is the importance of the Long Condor?

The Long Call Condor strategy is important because of its risk-managed flexibility, adaptability across market environments, analytical underpinnings, controlled payoff profiles, and the maturing options ecosystem supporting nimbler trade construction. Its popularity endures due to dependable profit potentials from sustained neutral market conditions.

One major reason for its rising popularity was the emergence of higher volatility environments that made basic long calls or put riskier plays. The condor’s bounded outcomes created by multiple option positions on both sides of the market provided a measure of downside security lacking in single-legged spreads. By establishing floors and ceilings to potential profits and losses, the condor offered a means to participate in directional views on an asset without taking on undefined risks from major short-term swings. This gave it greater stability and dependability than directional naked trades as volatility increased.

Its adaptability also proved advantageous. Traders could establish wider or narrower ranges by manipulating the short strikes to suit their precision in predicting a probability distribution rather than pinpointing an absolute closing price. Minor impacts from breaching defined thresholds were contained. Additionally, the condor allowed hedging core portfolio positions through synthetic short strategies, complementing long-term bullishness with protection from current price swings. Its structure offered delta neutrality and vega benefit during sharp volatility fluctuations, boosting risk management attributes.

Another key reason for rising interest was the availability of sophisticated analytical tools for assessing its Greeks and simulating profit/loss outcomes under various scenarios. Options analytics platforms provided advanced modeling capabilities not previously accessible to retail traders. Highly customizable risk profiles could now be precisely engineered.

Realizing the condor’s mathematical boundaries and sensitivities gave participants confidence in its controlled approach, which is absent from discretionary strategies reliant solely on market intuition or directional biases alone. Rising options liquidity also contributed. As optionable assets multiplied and contract sizes decreased on indexes and individual equities, market makers accommodated ever more granular strikes to implement ultra-tailored condor structures on any timescale. Spreads tightened.

How does Long Condor work?

A long-call condor strategy works by buying an out-of-the-money call while also selling calls and putting above and below the long call to limit upside and downside risks for a net credit, with the goal of profiting if the underlying asset closes between the short strikes at expiration. The Long Call Condor strategy generates profits by establishing a defined range between short strikes through purchasing wings, where short calls experience greater time decay than long calls if the underlying closes within this zone at expiration due to their proximity to the current price. Otherwise, losses ensue.

Long condor creates a structural position with four distinct “wings” consisting of two long calls (purchased calls) on the outer edges and two short calls (sold calls) in the middle. The central wing strikes represent the maximum gain targets. To implement a long call condor trade, a trader would take four positions. They would buy one call representing the bottom wing with a relatively low strike price. Then, they would sell two calls with higher strike prices above the current market level, representing the top and bottom inner wings. Finally, they would buy a final call with the highest strike to cap their liability at the top.

How effective is Long Condor?

Based on analytical modeling and trading evidence, the Long Call Condor is an effective strategy for achieving success rates over 50% and annual double-digit returns in subdued markets particularly suited to extracting time decay of premium through a predefined range framework while maintaining a mathematically structured risk profile competitive versus many passive alternatives through adjusted implementation calibrated to adjust to changing environments. Determining the precise effectiveness or success rate of any options strategy requires testing it across large, backtested datasets that include different market conditions.

The long call condor targets neutral, low volatility zones where option premiums tend to erode most rapidly due to time decay alone. These contained, non-trending periods are favorable for extracting such premium decay profits. The stable environments with minimized big moves allow the premium to naturally deteriorate over time in a contained manner.

What is the breakeven of Long Call Condor?

The breakeven points are defined price levels at which the trader would neither make a profit nor incur a loss when establishing a Long Call Condor position. The breakeven prices for a long call condor indicate the upper and lower price levels at expiration where the intrinsic value offset from penetrated strikes is exactly balanced by the initial net credit or debit, clearly outlining the range required for break-even results versus losses as an important reference for traders to assess the accuracy of their range assumptions intra-period based on market movements relative to the predetermined risk thresholds.

The breakeven prices provide important reference levels that indicate how close the underlying asset needs to finish at expiration for the position to realize modest gains compared to taking the maximum possible loss. They help define the exact range where profits are captured. To calculate the breakeven prices of a long call condor, we consider the individual strike prices and premiums/credits of all the options that make up the trade structure. For instance, suppose a trader enters a condor composed of the following positions: they buy 1 call at a strike of 100 for a Rs.1 premium. Additionally, they sell 2 calls at a strike of 110, collecting Rs.0.50 in premium per call for a total of Rs.1. Finally, they buy 1 call at a strike of 120 for an Rs.0.25 premium.

Net credit = Rs.1 – Rs.1 + Rs.0.25 = Rs.0.25

The upper breakeven = highest strike – net credit

Upper Breakeven = 120 strike – Rs.0.25 net credit = 119.75

The lower breakeven = lowest strike + the net credit

Lower Breakeven = 100 strike + Rs.0.25 net credit = 100.25

Intuitively, this makes sense. At the lower breakeven, the in-the-money amount of the long call exactly offsets the net debit. At the upper breakeven, the intrinsic value lost from additional ITM-ness on the short calls is precisely balanced by the net credit received initially.

So, in this example, a price between 100.25 and 119.75 at expiration results in neither profit nor loss. Below/above yields losses expanding as the strikes are penetrated. Determining the precise breakevens ahead of time provides transparency into risk exposures and profit zones. Traders know exactly how close the market needs to perform to their range assumptions to realize successful trades. This is valuable information when managing positions intra-period before expiration extinguishes variance.

In general, the Long Call Condor targets a narrow range between strikes defined by high-probability scenarios. The breakeven calculations objectively reveal if these assumptions fit underlying volatility tendencies or require adjustments on evolving markets.

What are the advantages of using Long Condor?

A long call condor provides a limited risk trade structure by establishing a range between call option strikes. Its main benefits stem from incorporating factors like premium time decay, customizable risk profiles, and analytical transparency, etc. These eight advantages are given below.

Risk Management

One of the main advantages of a Long Call Condor is its strictly limited downside risk profile. The maximum possible loss is always finite and known with precision prior to entering the trade. Unlike naked options positions, there is no unbounded risk potential for the market to move in adverse directions. Traders have clarity on their worst-case outcomes upfront.

Upside Participation

Another major advantage is the strategy provides participation on the upside while guarding against major downswings. The position captures gains from mild price increases through one of the purchased calls becoming profitable. Yet the additional long and short calls create virtual ceilings and floors that mitigate losses in more extreme scenarios. This delivers an asymmetrical return profile.

Time Decay Edge

The time decay factor inherent to options presents an edge for long condors. So long as the market remains between the short strikes close to expiration, time value erosion provides opportunities to profit. Even neutral conditions suffice rather than stringent directional bets. This enhances effectiveness in range-bound environments where capturing small premiums reliably is challenging.

Probability Dependence

Relatedly, long condors leverage one of the surest aspects of options – their statistical tendency to decline in price as expiration nears. This allows capturing positive carry from a spread position based on a mathematical tendency rather than uncertain forecasts. Outcomes depend more on probability than market opinion or volatility assumptions.

Capital Efficiency

Transactions involve limited cash outlay thanks to the premiums collected from writing calls. This enhances capital efficiency by permitting participation on larger underlying position sizes using less buying power. Proceeds from short calls partly or completely offset costs to establish each leg.

Customization

Their complexity translates to diverse adjustable trade structures. Investors are able to fine-tune risk/return profiles by altering strike prices, expiration dates, and option amounts to target desired probability ranges precisely. Custom outcomes on any stock or market index are engineered methodically.

Advanced Analytics

Analytical backtesting and risk metrics give advanced transparency into profit/loss breakeven points and sensitivities to market fluctuations. A strong understanding of boundary conditions and scientific underpinnings improves odds versus arbitrary speculation. Statistical validity enhances measurable discipline and viability.

Dynamic Management

Option adjustments like rolling short calls or closing long wings dynamically in response to price levels add flexibility missing from static positions. Active management facilitates optimizing trades in changing market environments throughout the lifespan.

These advantageous attributes make long condors scientifically compelling limited risk vehicles for hedging purposes or methodically capturing quarters profits in stable exchanges. Their analytical foundation and customizable profiles provide sound alternatives to fixed outright plays reliant exclusively on prognostication abilities.

What are the disadvantages of using Long Condor?

While long-call condors provide risk management benefits, challenges must be addressed. Capped profits, narrow ranges, expiration timing, commissions, volatility changes, and breaching limits impact performance if not mitigated properly. Seven disadvantages are given below.

Capped profits

Since gains are limited to the premium collected from writing calls, the strategy fails to realize larger returns from strongly bullish periods. However, limited profit is by design for risk management. Retail traders use multiples of condors or focus on high-premium stocks to boost probabilities.

Narrow profit zone

The range between short strikes allowing gains is constrained. Significant moves beyond this spectrum incur losses quickly. However, establishing wider acceptable parameter distributions preserves downside protection while enlarging the beneficial area. Dynamic leg adjustments also keep positions alive.

Expiration timing

Time decay advantages lessen, and volatility changes pose greater risks if executed too far from expiry. Targeting 30-45 days often ensures sufficient theta erosion to achieve targeted returns within a suitable window. Rolling to later dates is favorable to decay.

Commission burden

Frequent adjustments like rolling short strikes incur dealing costs that reduce performance. However, advanced platforms provide low-cost futures-style trading, minimizing hurdles. Selective changes focused on optimal extending dates and husband commissions.

Changes in volatility

Sudden, sharp movements in implied volatility alter option pricing in ways detrimental to long condors. However, their delta-neutral nature means directionally-linked vega swings are minimized. Positions are closed pre-expiration or re-established further out to benefit from reversion tendencies.

Breaching limits

Losses exceed maximum theoretical levels and wipe out earlier gains if the market penetrates above or below the protective call strikes. However, setting conservative, wide ranges reduces breaching probabilities to very low levels, according to analytics. Losses are still strictly finite.

Complex mechanics

Their multiplicity of legs over complicated matters for less experienced traders lacking full comprehension. Paper trading, simulation tools, and demo accounts offer risk-free education on the position’s nuances before committing real funds based on thorough comprehension.

These potential disadvantages either fail to seriously materialize or are effectively circumvented through conservative practices, technical adjustments, and diligent ongoing management tuned to specific market conditions. Overall, positive attributes outweigh isolated downsides.

What are the things to consider before using the Long Condor Strategy?

Before using a long condor strategy, traders should consider the implied volatility environment, liquidity of the underlying options, optimal time to expiration, available strike prices, capital requirements, the underlying historical volatility tendencies, personal risk tolerance, time horizon and goals, potential tax implications, platform capabilities, any necessary disclosures, and upcoming news events. Twelve important factors to consider before using the long condor strategy are given below.

Market Volatility

Condors work best when implied volatility is moderately low to high. In very low volatility environments, time decay proceeds slowly, and sufficient premium is difficult to harvest. Evaluate VIX levels and recent price action.

Liquidity

Ensure the underlying asset and specific option contract expiries and strikes chosen have adequate liquidity. Illiquid contracts hamper managing trades and achieving optimal entry/exit prices.

Time to Expiry

Target 30-45 days are generally optimal but should be adjusted based on how levels are changing. Further dates reduce decay advantages, while weekly will complicate its risk/reward.

Available Strikes

Check sufficient strike price granularity exists to design the desired tight risk range. Wider spreads consume profits unnecessarily.

Capital Requirements

Understand initial and maintenance margin levels. Condors tie up with considerable buying power, so position sizing is critical for portfolio allocation.

Historical Volatility

Analyse standard deviations and probable ranges. Align short strikes and wings appropriately based on tendencies, not just current ATM levels.

Risk Tolerance

Condors fit certain profiles better than others. Understand potential profit/loss scenarios and be psychologically prepared for drawdowns from general market moves.

Goals and Time Horizon

Consider whether capital will be deployed long enough to realize full trade cycles if adjustments become necessary due to fluctuations.

Taxes

Understand tax implications of options profits versus netted premium collected. Bracket changes sting profits unexpectedly if unprepared.

Platform Capabilities

Verify your broker accommodates multi-leg options orders natively in one transaction versus multiple steps. Simultaneous fills impact pricing.

Disclosures

Review any restrictions, approvals, or alerts needed before trading complicated strategies. Brokers also limit order types available for condors.

News Events

Be aware of economic reports, earnings, and other market-moving events that could inject short-term volatility regardless of prevailing conditions.

These factors all merit assessment prior to entering long condors to structure optimal positions aligned with individual objectives, risk tolerance, available tools, and prevailing market character. Proper prep lays the foundation for success.

Why do traders prefer Long Call Condor over other strategies?

The major reason many traders favor Long Call Condors compared to alternative strategies is their clearly defined risk profile. With a condor, the maximum possible loss is finite and known with precision before entering any trade. This is in contrast to naked option positions where risk is theoretically unlimited. The structural boundary conditions provide a major psychological advantage.

Another key differentiator is that condors allow participation in upside price movements while still offering substantial downside protection. The long calls capture gains if the underlying moves favorably through one strike, but short calls above and below create virtual price floors and ceilings. This provides an asymmetrical, controlled, risk-defined return structure.

Compared to basic long calls or puts, condors reduce overall sensitivity to volatility. While Implied Volatility Affects all options prices uniformly, changes have a smaller impact on balanced positions. This mitigates detrimental vega effects that could whipsaw directional plays disproportionately.

The time decay properties of options present an inherent trading edge for condors. As long as the market remains inside the range, gradual premium losses provide systematic profit opportunities. Neutral conditions suffice rather than stringent directional market forecasts, enhancing reliability, especially in sideways phases. Condor transactions require limited capital outlay compared to naked bets. Proceeds from writing calls partly or completely offset costs, allowing traders to establish larger notional positions using less margin. This capital efficiency is appealing for portfolio applications.

Their analytical risk metrics provide transparency to break-evens and sensitivities that simple directional strategies lack. Understanding boundary outcomes affords clearer rational management versus arbitrary guessing. This enhances discipline and viability long-term. Adjustable trade structures enable customizing risk-return profiles to narrow or wider target ranges for varying views. This methodical construction appeals to traders seeking probabilistic evidence over ambiguous forecasting alone.

Is Long Call Condor good for long term use?

No, the Long Call Condor strategy is generally not the most appropriate approach for extended long term use, although certain aspects of it are incorporated successfully into a longer-term options trading approach. The Long Call Condor is designed to profit from the natural time decay of options as they approach expiration in a narrowly range-bound market. This makes it most effective when each trade is held for a relatively short duration of 4-8 weeks at most.

Over longer periods of time, there are challenges for maintaining a pure Long Call Condor approach. Volatility assumptions become less reliable as the strategy relies on stable volatility for time decay to work as the main driver of profits. Extended bull or bear trends tend to increase volatility in unpredictable ways. This makes time decay a less consistent edge.

Additionally, capital efficiency is reduced when tying up margin in multiple positions for months at a time. This hinders the ability to adapt positions or take advantage of other opportunities in a changing market. Transaction costs also mount up as rolling positions to extend their duration incur additional fees. These fees eat into returns over many years of active management.

What is the maximum profit in using the Long Condor Strategy?

The maximum possible profit from a Long Call Condor trade is strictly limited and defined by the amount of premium collected from writing (selling) the calls. This finite upside is one of the main attributes that makes it a limited-risk strategy.

A sample long call condor trade consists of buying one call at a Rs.100 strike price for a Rs.1 premium, selling two calls at a Rs.110 strike price for Rs.0.50 each (collecting Rs.1 total), and buying one more call at a Rs.120 strike for Rs.0.25 premium.

Net credit received = Rs.1 – Rs.1 + Rs.0.25 = Rs.0.25

For this trade, the maximum possible profit would be equal to the net credit of Rs.0.25.

This would be achieved if the underlying asset closes precisely at the short strike price of Rs.110 at expiration.

In the ideal scenario where the maximum profit is achieved, the underlying asset would close precisely at the Rs.110 strike price at expiration. In this scenario, the calls sold at Rs.110 would expire worthless, allowing the trader to keep the full Rs.1 credit received for selling them. Additionally, the long Rs.100 and Rs.120 calls would have no intrinsic value at expiration. With the Rs.110 calls expiring worthless but their full credit retained and no amount owed on the long calls, the trader would lock in a profit equal to the Rs.0.25 net premium credit collected when entering the position.

No matter how far or close the price moves within the range defined by the protective calls, the maximum the trader earns is always capped at the net premium collected upfront.

This clearly defined upside limit is a deliberate part of the risk management approach. In exchange for taking a capped-profit position, the trade has maximum loss potential that is also finite and known in advance.

What is the maximum loss in using the Long Condor Strategy?

Along with the finite maximum profit, another defining aspect of the Long Call Condor is that it carries a strictly limited maximum potential loss. The maximum possible loss is calculated using a long call condor strategy, which is equal to the net debit paid to enter the position. This is because it involves both buying and selling options to structure multiple option positions simultaneously. To determine the maximum possible loss, we examine the same sample long call condor position. This trade involved buying one call at a Rs.100 strike price for Rs.1, selling two calls at a Rs.110 strike for Rs.0.50 each (collecting Rs.1 total), and buying an additional call at a Rs.120 strike for Rs.0.25.

Net debit = Rs.1 – Rs.1 + Rs.0.25 = Rs.0.25

For this trade, the maximum possible loss would be equal to the net Rs.0.25 debit paid to open the position.

This would occur if the underlying closed far outside the protective call strikes at expiration, resulting in one of the long calls expiring deep in the money to offset losses from the short calls. The maximum loss is always known with precision upfront since it is simply equal to the cost of entering the position. Unlike naked options, there is no potential for theoretically unlimited risks.

What is the perfect time to execute a Long Condor Strategy?

The long condor options strategy works best when the underlying asset is trading within a tight, well-established range with low implied volatility, as these conditions allow profits to be made from the natural time decay of the shorts options as expiration approaches. Entering a long condor spread when the market has recently consolidated without major price moves, and volatility is low provides optimal opportunities for the time-centric strategy. The implied volatility level is important to consider when entering a long condor position. Very low volatility makes it difficult to capture sufficient time decay in the options used, while high volatility increases the random and unpredictable movement of the underlying asset. Ideally, implied volatility should be in the middle or lower range based on its recent readings for the asset.

It is also best to implement the long condor when the underlying market has recently exhibited a period of sideways consolidation without any sudden or large price moves outside of an established tight trading band. This type of price action lends itself well to the strategy as natural theta decay in the options is captured as they approach expiration if the market remains range-bound. Examining technical indicators helps to identify the support and resistance zones where the asset has found a balance or equilibrium, such as the middle of a recent trading channel or range. This provides logical strike prices for the short calls or puts in the condor spreads.

What is the perfect time to exit the Long Condor Strategy?

The optimal time to exit a long condor strategy is before expiration if the underlying asset breaks out of its consolidated range, volatility rises substantially, profit targets are met, or technical indicators forecast that consolidating conditions are changing to avoid having the positions move further against the trade assumptions.

Ideally, traders aim to hold long condors until expiration to benefit fully from time decay, eating away at the premium of the short options. However, there are other factors to monitor as expiration approaches. It is best to hold out for maximum time value decay if the underlying remains inside the strike range for two weeks until expiration.

As the expiration date nears, it’s important to closely watch the price action of the underlying asset. A sustained break above or below the call or put strikes indicates it’s better to exit the position earlier to cut potential losses rather than see the short strikes move deeper in the money against the spread.

What is an example of Long Call Condor?

Let’s say it’s August 1st, and SPY is trading at Rs.410 per share. The 30-day implied volatility is 15%, which is toward the lower end of its recent range. SPY has been oscillating between support at Rs.405 and resistance at Rs.415 for the past few weeks.

Looking at the options chain, we see there is liquidity for options expiring in 30 days (August 30th expiration). We decided to target this expiration date to take advantage of time decay over the next month. To implement a long call condor trade, an options trader could do any of the following.

First, buy one call option with a strike price of Rs.400 and pay a premium of Rs.5 per contract. This serves as the bottom of the strategy. Additionally, the trader would buy one call option with a strike of Rs.420 but only pay Rs.3 in premium since this functions as the top of the position.

Secondly, to generate credits, the trader would then sell one call option at the Rs.412.50 strike price, receiving Rs.4 in premium per contract. They would also sell one more call at the Rs.407.50 strike, collecting another Rs.4 in premium per contract.

In total, this long call condor strategy would generate a net cash inflow of Rs.1 per contract since the Rs.4 and Rs.4 collected from the short calls exceeds the Rs.5 and Rs.3 paid for the long calls, defining the risk and maximum profit potential of the position.

Net credit received = Rs.8 – Rs.5 – Rs.3 = Rs.0

Our maximum risk is the net Rs.0 paid to open the position. Our maximum profit potential is Rs.8, which would be achieved if SPY settles between the short strikes of Rs.407.50-412.50 at expiration.

Leaving 30 days for volatility contraction and time decay to potentially drive the short strikes worthless, capturing their premiums for profit. This trade sets up an asymmetrical, risk-defined potential return profile targeting a defined sideways zone on SPY.

How does Long Condor differ from Butterfly Spread?

While long call condors and butterfly spreads both establish multiple option positions to profit from projected price action, there are important differences in their risk-reward structures and suitability for different market conditions.

A long condor involves combining long and short calls or puts at varying strike prices to create an area of protection between the short strikes. This defines a narrow range where time decay generates profits so long as the underlying closes within this band. Maximum risk is finite due to capping long positions, whereas reward is limited to the premium collected on entry.

A butterfly also uses multiple strikes but employs only long or short positions of the same option type, establishing wide protection zones above and below while maintaining neutrality at the middle strike. It carries an unlimited risk to pricing surprises yet likewise presents limitless upside potential if perfectly positioned.

Due to condors’ short positions offsetting longs, they assume limited risk suitable for range-bound trading, seeking consistent smaller gains. Butterflies’ asymmetric payoff profile necessitates precise directional forecasting, lacking a “defined failure” point if wrong. Their big, one-time windfalls necessitate more timing accuracy.

Condors’ short strikes define a tighter expected range compared to butterflies’ wider zones. This allows condors’ probabilistic edge from premium contraction to accrue over many trades, while butterflies require successful binary upstairs/downstairs bets in each individual position.

Traders dynamically adjust condors through rolls or adjustments to react as underlying prices shift, preserving the limited risk structure. Alterations breaking a butterfly’s equilibrium change its risk-reward dynamics entirely, demanding perfection from the start.

While both strategies involve multi-leg structures, condors’ ability to offset gains and losses from opposing positions makes them better suited for neutral periods. Conversely, butterfly payoffs rely entirely on directional assumptions, magnifying uncertainty.

For these reasons, condors tend to offer more reliable outcomes adaptively across varied markets by capitalizing on two-sided opportunities and preserving downside protection. Butterflies demand correct directional projection for success in their singular attempts. Overall strategy emphasis differs significantly due to these important contrasts.

How does Long Call Condor differ from Short Call Condor?

While long and short call condor strategies both employ multiple call options positions, they have distinctly different directional assumptions and risk-reward profiles suited for divergent market conditions.

A long call condor constructs a neutral, non-directional trade aiming to profit from a range-bound underlying through offsetting long and short call positions. Its strikes define a narrow expected range where time decay generates a steady income. Maximum gain equals net premium collected on entry, while precise maximum loss equals this amount.

In contrast, a short call condor structures an outright bearish bet that the underlying asset price will decline below all strikes by expiration. It relies solely on naked short calls at various downside intervals to capture full intrinsic value declines as the market falls. Profit potential grows exponentially unlimited as prices approach infinity to the downside. However, risk likewise reaches unconstrained extremes if the outlook proves wrong.

With its limited gains but explicitly defined boundaries, a long condor involves controlled probabilistic wagering utilizing the statistical edge of volatility contraction, favoring strikes over the long run. Short condors take a speculative “all-or-nothing” approach reliant on the accuracy of a monolithic directional projection.

Traders employ long condors when neutral to slightly bullish or bearish, seeking consistent smaller victories from two-sided opportunities across range-bound phases. Short condors demand powerful conviction as security faces precipitous timely drops to compensate for potential uncapped downside exposure.

Active management is common for long positions, using adjustments like rolling calls forward to adapt. Short condors remain static bets, necessitating precision initially without flexibility. Wider strike spacings offer room for breaks to be lower but eliminate mitigation of any contravening moves.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 16")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 17")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 18")

: Overview, 10 Types of Indicators, Settings for Different Markets 20")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 22")

No Comments Yet.