Short straddle is one of the widely useful option trading strategies, especially amongst experienced traders and institutions. Short straddle option strategy is designed to profit during sideways or rangebound markets, allowing traders to benefit from time decay or falling volatility.

This strategy allows traders to capture the maximum profit during a sideways market where a trend trader struggles to make any profit. The winning probability of short straddle strategy is high but the profits are limited to the premium received, whereas the losses are theoretically unlimited. In this blog we will learn how to trade, and when to trade short straddle strategy safely.

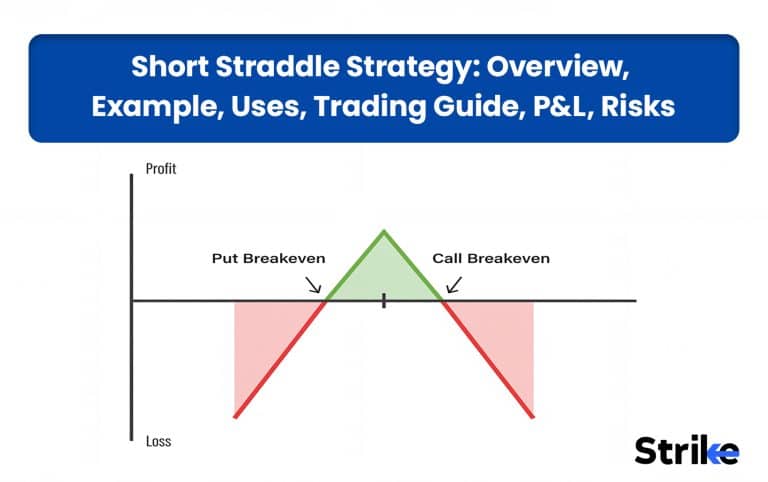

What is a Short Straddle?

Short straddle is an non-directional option selling trading strategy which involves selling of ATM (at the money) call and ATM (at the money) put options simultaneously of the same expiry. This strategy is used when traders expect the market to remain stable without moving significantly in either direction.

The structure of the short straddle payoff chart looks like an upside down “V”shape, where the peak represents ATM strike of call and put option. That is where the maximum premium is received as a profit. Once stock starts moving away from your select ATM strike, your profit shrinks linearly until you hit your break-even points, and it gradually starts reducing your premium or profit after reaching the break even point you enter the loss zone where the loss is unlimited.

How Does a Short Straddle Work?

The short straddle works by simultaneously selling a call and put option of same strike and same expiry to collect the premium upfront from both the options. Traders profit when the underlying asset stays near the sold strike until expiry and gradually loses its value due to time or theta decay.

Lets understand how a short straddle works using an example of stock XYZ. Suppose a stock XYZ is trading at ₹100 and as a trader, you expect the stock to remain stable without any significant move till expiry.

- Sell ₹100 strike call option for ₹5 premium

- Sell ₹100 strike put option for ₹5 premium

Both the above options have the same strike and same expiry and you receive a total premium of ₹10 (₹5 from each). This ₹10 is your maximum profit in this strategy.

Now there are two scenarios, either the stock will stay sideways as expected or it will move significantly in either of the directions.

- Scenario 1: If stock stays sideways and expires between ₹101 or ₹99, you keep the ₹10 premium as profit.

- Scenario 2: If the stock moves in upward direction to ₹130, the sold call option will incur heavy loss. However, the put option will give you profit but not more than ₹5. Hence the net position goes in loss due to limited profit from one side and unlimited profit from the other side. Similarly, if price moves downward to ₹70, the sold put option will incur heavy loss.

A short straddle involves selling both a Call Option and a Put Option at the same strike price, rewarding market stability but penalizing large price swings. By using this combination of a Call Option and a Put Option, the strategy becomes best suited for range-bound markets where price movement is expected to remain minimal.

What is an Example of Short Straddle?

Lets understand the short straddle using examples of Reliance Industries stock. Reliance Industries is currently trading at ₹1321.20. Now to create a straddle we will sell the call and put option of ATM strike ₹1330 of June expiry.

Above is the payoff chart we get after creating a short straddle. The peak represents ATM call and put strike ₹1330 of June expiry. ₹1257 and ₹1402 is breakeven level. If price moves beyond these levels, the trade will enter a loss zone.

Why Use a Short Straddle Strategy?

There are five main reasons to use the short straddle strategy. The reasons are briefly discussed below.

- Generate Premium Income: As we sell ATM call and ATM put options, the upfront premium received from both sides is higher, compared to selling a single option.

- Benefit from Time Decay: As we sell options in short straddles, time decay works in our favour. If the stock remains near the sold strike, both the options will lose the value due to theta decay, helping sellers to make profit.

- Profit in Sideways Markets: In sideways markets where normal trading or option buying struggles to give profits, short straddles tend to generate good profits in a sideways market.

- Benefit from Falling Volatility: If the short straddle was created during the period of high volatility, traders collect larger premiums or profits when the volatility drops.

- High Probability in Stable Conditions: When markets are calm and major events are absent, prices often stay within a limited range, which increases the chances of success for the strategy.

Overall, the short straddle is used to generate consistent premium income when a trader expects high Implied Volatility to decrease, resulting in limited price movement. By monitoring Implied Volatility, a trader can better anticipate the steady time decay required for the strategy to remain profitable until expiry.

When to Use a Short Straddle?

There are four ideal situations to use a short straddle strategy during low volatility expectation, sideways or range bound market after volatility spike or no major event expected.

- During Low Volatility Expectations: When you expect market volatility to remain low or decrease after entering the trade, make a short straddle, because during low volatility the market does not move much and remains sideways.

- Sideways or Range-Bound Market: When the market is expected to trade in a narrow range, a short straddle works best.

- After Volatility Spikes: Many traders prefer using short straddles after the sharp rise in volatility (more than 50%), because IV rises make option premium expensive. If later IV drops, option premium declines faster giving more profits.

- No Major Events Expected: The strategy is commonly used when there are no major events such as an earnings announcement, important economic data, policy decisions, or major news events. This reduces the chances of sudden large price movements.

In short, a short straddle is best used when you expect the market to remain calm and range-bound, a state frequently identified through Option Trading Indicators. When these Technical Analysis Indicators suggest the market is free from events that could trigger sharp price movements, the strategy has its highest probability of success.

How Option Greeks Affects Short Straddle?

Option greeks have direct effects on short straddle trading strategy because it involves selling of two ATM options. Let’s briefly discuss the effect of option greek on short straddle trading strategy.

- Theta (Time Decay): Theta is the most important greek for short straddle strategy and works positively for short straddle traders. As we sell ATM calls and put options, we earn a premium through theta decay. Option loses its premium due to theta decay everyday and you collect this decay as a profit. The process of theta decay is slower during initial days but accelerates as expiry approaches. Generally 30–45 DTE (days to expiration) options are considered optimal because they have a decent premium and good theta decay.

- Vega: Vega measures the change in option price with the change in implied volatility. Higher IV increases the option premium and allows traders to collect more profit, while lower IV reduces the premium income. IV Rank (IVR) above 30–50% is considered good to maximize premium collected.

- Delta: Initially the delta in short straddle strategy remains neutral (short call has a delta of roughly −0.5 and the short put +0.5) which means the strategy is Delta neutral strategy. However as soon as the stock starts moving, one leg Delta gains faster than others, creating a directional risk.

- Gamma: Short straddles have negative gamma, which means losses can increase rapidly if the stock makes a sharp move away from the strike price. Small price movements may not hurt much initially, but as expiry approaches, gamma increases sharply and delta changes faster, making the position highly risky during sudden market moves.

A short straddle benefits from positive theta and falling volatility, but traders must carefully manage delta and gamma risk, especially when the underlying makes a sharp move.”

How to Trade using Short Straddle?

There are five simple steps to trade using a short straddle strategy. The steps include, Stock selection, strike selection, execution, monitoring and risk management.

- Select a Suitable Stock: Choose a stock or index which is moving in a sideways range or has no clear direction. Such low-volatile stocks are suitable for short straddle strategy. Avoid selecting stock during the period of high uncertainty major news events or upcoming result announcements.

As we can see in the given above, I have selected Kotak Mahindra Bank stock because it is trading in a sideways range from the last two months.

- Choose the Strike Price: Go to the option chain and select the ATM call and put option. ATM options generally provide a high option premium and maximum time decay benefit.

- Sell Both Call and Put Options: Sell ATM call and put options to collect option premium upfront. Make sure that the options have the same strike price and same expiry date.

- Monitor Volatility and Price Movement: After entering the trade, keep monitoring implied volatility, price movement, option greeks, specially Gamma and theta.

- Manage Risk and Exit Position: If stock starts to rise sharply in either direction, immediately adjust the position of the trade or exit early to control the risk.

Many traders prefer booking profits on ATM strikes before expiry instead of holding till the last day because gamma risk becomes very high near expiration. Since ATM options are the most sensitive to price changes, closing the position early helps protect the collected premium from sudden market shifts.

What are the Maximum Profit & Loss on a Short Straddle?

The maximum profit in short straddles is limited to the total premium received from selling ATM call and ATM put options. This maximum profit only occurs when the market closes exactly at the strike price, causing both options to expire worthless.

Maximum Profit = Call Premium+Put Premium

A short straddle theoretically has unlimited loss if the stock sharply moves in an upward direction. If stock rises sharply in the upper direction the sold call option can give us unlimited loss because there is no upper limit to how high a stock can rise. Whereas, if stock falls sharply, the short put can give us a limited loss until stock reaches zero, which can still result in a very large loss.

What are the Risks of a Short Straddle?

There are five major risks involved in short straddles. The risks include unlimited loss, risk from volatility expansion, gamma risk, margin and MTM pressure, and an event risk.

- Unlimited Loss Potential: As we sell in short straddles, the losses can be huge or theoretically unlimited if the underlying makes a strong move in either direction.

- Volatility Expansion Risk: Increase in IV raises the option premium, which can cause losses even if the stock price has not moved significantly.

- Gamma Risk Near Expiry: As gamma measures the rate of change of delta, increase in gamma can increase the premium rapidly, causing losses. The gamma risk is higher during near expiry. Even a small movement can quickly turn into a large loss.

- Margin and MTM Pressure: Creating a short straddle requires a high margin and can face significant mark-to-market losses during volatile conditions, which requires a higher margin.

- Event Risk: Events like earnings announcements, economic data, or major news can lead to sharp price swings and heavily impact the strategy.

A short straddle is risky because it profits only when the market stays calm, but large price movements or rising volatility can create very large losses.

Is Short Straddle Strategy Profitable?

Yes, a short straddle strategy is profitable but only when traded in the right market context. The short straddle strategy is developed to trade sideways markets, hence it performs best in range bound markets.

However, the profitability of this strategy also depends on how you manage risk, because the payoff chart of this strategy is asymmetrical. Although you have a high winning probability and may win most of the time, one single loss is enough to wipe out the profits from many previous trades.

To manage such asymmetric risk traders follow the following risk management rules.

- Exit before expiry to avoid high gamma risk.

- Use stop-losses or predefined loss limits.

- Trade during periods of elevated implied volatility.

- Adjust or hedge the position if the stock moves significantly.

Overall, the short straddle strategy is profitable when used with the right market context and risk management. A SteadyOptions blog article by Kim Klaiman shows that if short straddles are executed properly, it can generate 18–25% annual return.

Is Short Straddle Bullish or Bearish?

A short straddle is neither bullish nor bearish. It is a non-directional options strategy. The strategy does not require the underlying asset to move up or down. Instead, it profits when the price remains close to the strike price and volatility stays low.

What are Alternatives to Short Straddle Strategy?

There are three alternatives to short straddle strategy which allows you to profit from the sideways market with a limited loss. These strategies are iron Condor short triangle and butterfly straight.

- Iron Fly: Iron fly is similar to short straddle strategy but with the hedge. Just like a short straddle, Iron fly also involves selling ATM put option and ATM call option but along with it, it also involves buying out of the money (OTM) call and put option as a hedge. In short an iron fly is nothing but a short straddle with the hedge.

- Short Strangle: Similar to short straddle, short strangle is also a rangebound market strategy, but unlike short straddle, short strangle involves selling of OTM (out of the money) call and put option instead of ATM (at the money) call and put option.

- Butterfly Spread: In Butterfly Spread we sell either 2 ATM call options or 2 ATM put options instead of one call and one put option and hedge by one ITM option and one OTM option. It is also a market neutral strategy with potential of limited risk and limited reward. This strategy is suitable when traders expect the market to remain near a specific price. In Butterfly Spread we sell either 2 ATM call options or 2 ATM put options instead of one call and one put option.

These alternatives allow traders to choose between limited risk, income generation, wider profit zones, or volatility-based opportunities, depending on their market outlook and risk tolerance.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 24")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 25")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 26")

: Overview, 10 Types of Indicators, Settings for Different Markets 28")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 30")

No Comments Yet.