Volatility strategies in options trading allow traders to profit from both sharp price swings and calm market phases. Volatility strategies rely on how implied volatility affects option premiums, creating setups suited for bullish, bearish, or neutral views.

These strategies are widely used for speculation, hedging, and income generation. The key is selecting the right approach for the market’s expected movement and managing risk with proper adjustments.

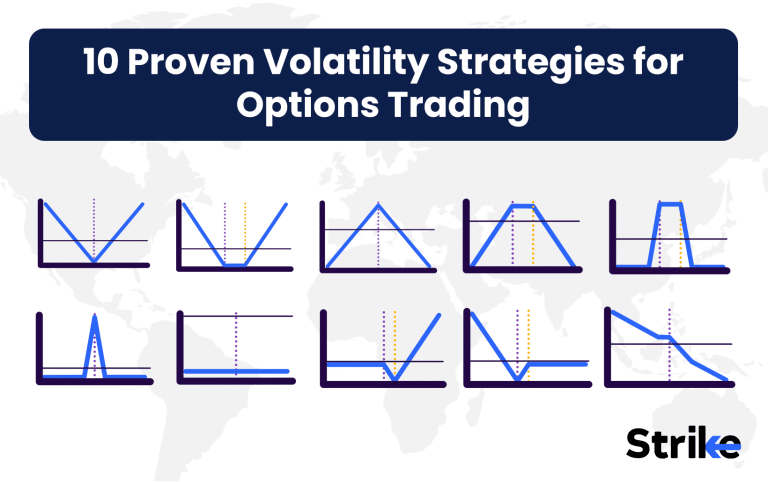

1. Long Straddle

A long straddle involves buying one call and one put option at the same strike price and expiry, typically at-the-money. This gives the trader a position that profits from large price moves in either direction, with risk limited to the total premium paid.

The strategy works best before high-impact events such as earnings, RBI decisions, or geopolitical announcements where volatility spikes are expected. Since direction is uncertain, the straddle covers both outcomes.

For instance, if NIFTY is at 25,000, buying a 25,000 Call at ₹200 and a 25,000 Put at ₹180 costs ₹380 in total. The breakeven points are 25,380 on the upside and 24,620 on the downside. A move beyond either level produces profits, while staying near 25,000 results in a maximum loss of ₹380.

Traders prefer straddles in volatile conditions because Vega benefits from rising implied volatility, while Theta decay is the main drawback. Studies show earnings straddles succeed in around 60–65% of cases where volatility expands by 10% or more.

| Pros | Cons |

| Unlimited profit potential | High upfront cost |

| Works in any direction | Requires strong move to break even |

| Simple to execute | Loses value quickly in flat markets |

A long straddle is a straightforward volatility play that rewards uncertainty, but only if the underlying makes a decisive move.

2. Long Strangle

A long strangle is built by buying an out-of-the-money call and an out-of-the-money put with the same expiry. It works similarly to a straddle but costs less because both strikes are away from the current price.

This setup is best used when traders expect extreme volatility but want lower initial premiums. Since the strikes are wider apart, the breakeven range is larger, meaning the underlying must move more significantly to generate profit.

For example, with NIFTY at 25,000, a trader could buy a 25,200 Call at ₹120 and a 24,800 Put at ₹100, paying ₹220 in total. The breakeven levels are 25,420 and 24,580. Maximum loss is limited to ₹220, while profits rise sharply once the index moves beyond either breakeven. I

Traders often deploy strangles ahead of major global events or during times of heightened uncertainty. They benefit from Vega when implied volatility rises but suffer from Theta erosion in quiet conditions. Backtests show success rates of 55–60% if volatility jumps more than 12%.

| Pros | Cons |

| Lower cost than straddle | Needs larger price move |

| Unlimited profit potential | Wider breakeven range |

| Suitable for extreme volatility | Loses in stable markets |

The long strangle is a cheaper alternative to the straddle but demands a stronger price move to deliver meaningful returns.

3. Short Straddle

A short straddle involves selling one call and one put at the same strike price and expiry. This strategy profits when the underlying stays close to the strike and option premiums decay over time.

It is most effective in calm markets with no major events ahead. Traders collect premium income but take on unlimited risk if the underlying moves too far in either direction.

For instance, with NIFTY at 25,000, selling a 25,000 Call for ₹200 and a 25,000 Put for ₹180 gives a total premium of ₹380. The maximum profit is limited to ₹380 if NIFTY closes exactly at 25,000. Breakevens are 25,380 and 24,620, beyond which losses start to accumulate.

This strategy is popular with experienced traders because Theta decay works in their favor, but it carries high Vega risk during sudden volatility spikes. Historically, success rates are around 70% in stable, low-volatility phases.

| Pros | Cons |

| High probability of profit | Unlimited loss potential |

| Income from premium decay | Risky during breakouts |

| Simple to set up | Requires high margin |

A short straddle is powerful in calm markets but dangerous in trending conditions, making risk management critical.

4. Short Strangle

A short strangle is created by selling an out-of-the-money call and an out-of-the-money put. It resembles a short straddle but provides a wider profit zone since strikes are set further apart.

This setup works best when the trader expects the market to stay range-bound with low volatility. It yields smaller premium compared to a straddle but offers more breathing space before losses occur.

For example, with NIFTY at 25,000, selling a 25,200 Call for ₹120 and a 24,800 Put for ₹100 generates ₹220 in premium. Maximum profit is capped at ₹220, with breakeven levels at 25,420 and 24,580. Beyond these points, losses increase and are theoretically unlimited.

Short strangles are popular income strategies during dull market phases. Theta helps, but Vega risk is significant if volatility rises sharply. Success rates often reach 65–70% during quiet periods without news flow.

| Pros | Cons |

| Wider safety margin | Limited premium income |

| Lower risk than straddle | Unlimited risk on breakouts |

| Effective in calm phases | Needs adjustments in volatility spikes |

The short strangle is a balanced income strategy that rewards stability but leaves traders exposed to sharp unexpected moves.

5. Iron Condor

An iron condor is a four-leg strategy combining a short strangle with protective long wings. It profits in range-bound conditions while limiting potential losses.

The setup involves selling one OTM call and put, and buying a further OTM call and put for protection. This defines both risk and reward while reducing margin requirements.

For example, with NIFTY at 25,000, a trader sells a 25,200 Call for ₹120 and buys a 25,400 Call for ₹60, then sells a 24,800 Put for ₹100 and buys a 24,600 Put for ₹50. The net premium is ₹110. Maximum profit is ₹110, and maximum loss is ₹90, which is the difference between strikes minus premium.

Iron condors are widely used by professional traders because of their high win probability in sideways markets. Success rates are typically 70–75% in stable conditions, with Theta working positively and risk strictly capped.

| Pros | Cons |

| Defined risk and reward | Profit is limited |

| High probability of success | Requires four trades to execute |

| Lower margin requirement | Prone to adjustments if volatility rises |

The iron condor is a favored choice for consistent income in neutral markets, offering safety and clarity in risk management.

6. Iron Butterfly

An iron butterfly is a limited-risk, limited-reward options strategy designed to profit from low volatility when the underlying stays near a central strike. The structure involves selling one ATM call and one ATM put, while buying an OTM call and an OTM put for protection. The result is a tent-shaped payoff with a narrow profit zone.

The setup works best when traders expect minimal movement around a key price level. Since the sold options are at-the-money, the premium collected is higher than in an iron condor, making the potential reward larger if the underlying remains flat.

For example, with NIFTY at 25,000, a trader sells a 25,000 Call at ₹200 and a 25,000 Put at ₹180, while buying a 25,200 Call at ₹100 and a 24,800 Put at ₹90. The net credit is ₹190. Maximum profit is capped at ₹190 if NIFTY closes exactly at 25,000, while the maximum loss is limited to ₹110, which is the difference between strikes minus net premium.

This strategy is attractive due to defined risk and a higher reward-to-risk ratio compared to an iron condor. Success rates in calm market phases hover around 70%. Theta decay is favorable, while Vega risk is moderate.

| Pros | Cons |

| Higher reward potential than iron condor | Very narrow profit zone |

| Defined risk on both sides | Loses quickly if market trends |

| Works well in flat markets | Execution involves four legs |

The iron butterfly is powerful for traders confident that the underlying will remain range-bound near a central level.

7. Calendar Spread

A calendar spread is built by selling a short-term option and buying a longer-term option at the same strike. The strategy profits from time decay differences and rising implied volatility in the long-dated option.

It is best used when the trader expects the underlying to remain near a specific level in the near term, while anticipating volatility to increase over time. This setup balances short-term decay against long-term protection.

For instance, with NIFTY at 25,000, a trader sells a 25,000 Call with one-month expiry at ₹200 and buys a 25,000 Call with two-month expiry at ₹300. The net debit is ₹100. Maximum profit occurs if NIFTY finishes close to 25,000 at the short expiry, as the short leg decays faster than the long leg. Loss is limited to the net debit.

The appeal lies in exploiting time decay (theta differential) and rising implied volatility. Studies show calendar spreads deliver around 60% success when IV expands in the back-month option.

| Pros | Cons |

| Takes advantage of time decay | Requires stable underlying price |

| Limited risk exposure | Limited profit if volatility falls |

| Works well with rising IV | More complex to manage |

A calendar spread is a sophisticated strategy for traders expecting stability in the short term with potential volatility ahead.

8. Call Ratio Backspread

A call ratio backspread is a bullish volatility strategy that profits from strong upward movement. The structure involves selling fewer lower-strike calls and buying more higher-strike calls, typically in a 1:2 ratio.

This setup is ideal when the trader expects a sharp rally and wants unlimited upside potential with limited downside risk. Losses are capped, while gains increase exponentially with price surges.

For example, with NIFTY at 25,000, a trader sells one 25,000 Call at ₹200 and buys two 25,200 Calls at ₹120 each. The net debit is ₹40. Maximum loss is ₹40 if NIFTY stays below 25,000, while profits are unlimited if NIFTY rises significantly above 25,200.

The strategy benefits from Vega, as rising volatility increases option value. Backtests suggest 65% success when used before bullish events like budget announcements or positive earnings seasons.

| Pros | Cons |

| Unlimited upside profits | Requires strong rally |

| Limited downside loss | Wider breakeven points |

| Gains from volatility spikes | Slightly complex to set up |

A call ratio backspread is ideal for traders looking for leveraged bullish exposure while keeping downside risk contained.

9. Put Ratio Backspread

A put ratio backspread is a bearish volatility strategy structured by selling fewer higher-strike puts and buying more lower-strike puts, often in a 1:2 ratio. The position profits from large downward moves.

It is best deployed when the trader expects a sharp fall in the underlying. Losses are capped if the market does not drop, while profits grow rapidly with deeper declines.

For example, with NIFTY at 25,000, a trader sells one 25,000 Put at ₹200 and buys two 24,800 Puts at ₹120 each. The net debit is ₹40. Maximum loss is limited to ₹40 if NIFTY closes above 25,000, while profits are unlimited if the index crashes well below 24,800.

The strategy gains from Vega, making it useful during bearish volatility surges. Data shows around 65% success when used before negative earnings or economic shocks.

| Pros | Cons |

| Unlimited downside profits | Needs a sharp decline |

| Limited upside loss | Wider breakeven levels |

| Good hedge for long portfolios | Slightly complex management |

A put ratio backspread is a high-reward bearish strategy suited for traders expecting heavy downside volatility.

10. Broken Wing Butterfly

A broken wing butterfly is a modified butterfly spread where strike distances are unevenly adjusted to reduce cost or skew risk. The strategy profits from stable markets but carries a tilted risk-reward profile.

It works best when traders expect range-bound movement but want to reduce downside risk or entry cost compared to a regular butterfly. By shifting one wing further out, traders lower debit while keeping controlled risk.

For example, with NIFTY at 25,000, a trader sells two 25,000 Calls at ₹200 each, buys one 24,800 Put at ₹120, and buys one 25,400 Call at ₹60. The payoff creates limited profit potential with reduced downside loss. Maximum risk is capped, but reward is concentrated around the middle strike.

This strategy balances theta gains with limited Vega risk. Success rates are around 65% when volatility remains stable.

| Pros | Cons |

| Lower cost than standard butterfly | Uneven risk distribution |

| Defined risk and reward | Profit limited to narrow zone |

| Flexible to adjust | More complex to execute |

The broken wing butterfly is a creative variation that reduces entry cost while retaining the key benefits of defined risk trading.

What Is Volatility in Options Trading?

Volatility in options trading refers to the degree of price fluctuation expected in the underlying asset. It is the most important factor in option pricing after the underlying price itself.

Implied volatility (IV) measures market expectations of future movement, while historical volatility measures past price changes. Higher volatility raises option premiums, while lower volatility reduces them.

Traders use volatility to decide whether to buy or sell options. Buying strategies like straddles and strangles benefit from rising volatility, while selling strategies like condors and straddles work best in falling volatility.

Volatility is also linked with the Greeks. Vega shows sensitivity to IV changes, while Theta tracks time decay. Understanding these dynamics helps traders choose the right volatility strategy. In essence, volatility drives opportunity, and mastering it is key to consistent options profits.

When Should You Use Volatility Strategies?

Volatility strategies are used when traders anticipate sharp moves or prolonged stability in markets. The timing depends on market events and volatility levels.

Use long volatility strategies like straddles, strangles, and ratio backspreads before major events such as earnings, budgets, or policy changes. These setups benefit from expanding implied volatility and strong directional moves.

Use short volatility strategies like iron condors, butterflies, and short strangles during quiet phases. These strategies earn from time decay and premium erosion when prices stay within a range.

The choice depends on market outlook. Traders with event-driven expectations choose long setups, while those expecting calm conditions favor short premium structures. Matching the strategy with volatility conditions improves success probability and reduces risk.

Which Volatility Strategy Is Suitable for You?

The best volatility strategy depends on your risk appetite, capital, and market outlook. No single setup fits all traders.

Aggressive traders expecting sharp moves prefer straddles, strangles, or ratio backspreads. Conservative traders seeking steady income in stable markets use iron condors or butterflies. Intermediate strategies like calendar spreads balance time decay and volatility shifts.

The table below compares 10 strategies across key parameters.

| Strategy | Structure | Market Outlook | Profit Potential | Loss Potential | Breakevens | Vega Impact | Theta Impact | Margin Needed | Complexity | Success Rate | Best for |

| Long Straddle | Buy ATM Call + Put | High volatility expected | Unlimited | Limited to premium | Narrow | Positive | Negative | Low | Simple | 60–65% | Uncertain direction |

| Long Strangle | Buy OTM Call + Put | Extreme volatility | Unlimited | Limited to premium | Wide | Positive | Negative | Low | Simple | 55–60% | Big events |

| Short Straddle | Sell ATM Call + Put | Low volatility | Limited to premium | Unlimited | Narrow | Negative | Positive | High | Simple | 70% | Calm phases |

| Short Strangle | Sell OTM Call + Put | Stable markets | Limited to premium | Unlimited | Wide | Negative | Positive | High | Simple | 65–70% | Neutral outlook |

| Iron Condor | Sell OTM Call + Put + Buy wings | Range-bound | Limited | Limited | Defined | Neutral | Positive | Moderate | Medium | 70–75% | Income traders |

| Iron Butterfly | Sell ATM Call + Put + Buy wings | Flat markets | Limited | Limited | Narrow | Neutral | Positive | Moderate | Medium | 70% | Precise range |

| Calendar Spread | Sell short-term + Buy long-term | Stable with rising IV | Limited | Limited to debit | At strike | Positive | Mixed | Moderate | Medium | 60% | Volatility shifts |

| Call Ratio Backspread | Sell 1 Call + Buy 2 higher Calls | Bullish volatility | Unlimited | Limited | Wide | Positive | Negative | Medium | Medium | 65% | Strong rallies |

| Put Ratio Backspread | Sell 1 Put + Buy 2 lower Puts | Bearish volatility | Unlimited | Limited | Wide | Positive | Negative | Medium | Medium | 65% | Sharp declines |

| Broken Wing Butterfly | Uneven Butterfly spread | Range-bound | Limited | Limited | Defined | Neutral | Positive | Moderate | Complex | 65% | Income with skew |

Each strategy fits a unique purpose, and traders succeed by aligning the right setup with expected market conditions.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 44")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 45")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 46")

: Overview, 10 Types of Indicators, Settings for Different Markets 48")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 50")

No Comments Yet.