A put ratio backspread is an options trading strategy that involves selling multiple puts at a lower strike price and buying a smaller number of puts at a higher strike price, expiring at the same time. A put ratio backspread creates a net credit because the premium received from selling puts exceeds the premium paid for buying puts. It allows traders to benefit from a sideways or slightly downward movement in the underlying asset’s price.

However, the strategy also has limited upside potential and significant downside risk if the asset’s price falls below the break-even point. This strategy is appealing for traders looking to generate income from a neutral to moderately bearish market view over the short term. The key advantage is collecting premiums by putting more money at risk. The main disadvantage is unlimited risk if the asset price falls substantially.

What is Put Ratio Backspread?

A put ratio backspread is an options trading strategy that involves buying puts at a lower strike price and selling more puts at a higher strike price. A put ratio back spread is a bearish to neutral strategy that is used when the trader expects a moderate drop in the price of the underlying asset.

The put ratio backspread aims to profit from a decline in the underlying asset while limiting potential losses if the asset rises or doesn’t fall by the expected amount. The maximum profit is capped due to the short puts at the higher strike price, while the maximum loss is reduced due to the long puts at the lower strike price.

A put ratio backspread is constructed by buying X number of puts at a lower strike price and selling Y number of puts at a higher strike price, where Y is greater than X.

For example, a trader could buy 2 puts with a Rs. 50 strike price and sell 5 puts with a Rs. 55 strike price. Here, the put ratio is 2:5 – for every 2 puts bought at the lower strike, 5 puts are sold at the higher strike.

The puts that are bought have a lower break-even point and will generate profit if the underlying asset price falls below the lower strike price. However, the short puts at the higher strike price cap the maximum profit potential if the underlying price drops further.

At the same time, if the asset price rises and stays above the higher strike at expiration, the short puts expire worthless, while the long puts mitigate the losses.

The maximum profit on a put ratio backspread is achieved if the underlying asset price drops below the lower strike price of the long puts. The maximum profit is equal to the difference between the two strike prices minus the net premium paid to establish the position.

The maximum loss occurs if the underlying asset price rises above the higher strike by expiration. However, the long puts at the lower strike help reduce the loss compared to just being short puts alone at the higher strike. The maximum loss is limited to the net premium paid.

What is the importance of Put Ratio Backspread?

One of the main reasons why a put ratio backspread is important is because it provides a risk-defined way to profit from a downward move in the underlying asset. These are the top four advantages of risk management. It caps the maximum loss if the asset price remains stable or rises.

This is defined by the net debit paid to open the trade. The sell puts at the higher strike limit the profit potential from large downward moves past the lower strike. This also reduces risk. The precise risk-reward profile is sometimes tailored through the ratio of puts sold to puts purchased. A smaller ratio caps risk, while a larger ratio increases leverage.

Compared to just buying puts outright, the sold puts lower the cost basis significantly or even to a credit. This lowers capital requirements.

Put ratio back spreads allow traders to obtain leveraged bearish exposure while precisely defining maximum risk. This is important for managing capital and limiting losses on downward directional forecasts.

For traders who expect a modest drop in stock rather than a major bearish collapse, ratio back spreads are sometimes ideal. The following four factors explain why this method is effective for mildly pessimistic outlooks. The capped downside from the short puts optimizes gains in the target drop range. The strike prices are selected to match the expected decline.

The lower capital requirements allow trading opportunities even with smaller price moves. The defined risk lowers the break-even point. The negative delta exposure benefits from continued downward drift even after the short puts expire worthless. It avoids excessive time decay that comes with holding long puts through sideways Choppy markets.

Put ratio backspreads offer an efficient way to gain leveraged exposure to moderately bearish outlooks on an asset’s price.

How does Put Ratio Backspread work?

A put ratio backspread works by combining long puts at a lower strike and short puts at a higher strike in a ratio greater than 1:1. Take a look at the construction and operation of put ratio backspreads.

Position Construction

Traders will buy X number of puts at a chosen lower strike price. These are the long puts.

They will simultaneously sell Y number of puts at a higher strike price. These are the short puts.

The ratio is set where Y is greater than X. A common ratio is 1×2, buying 1 long put and selling 2 short puts.

The short puts always have a higher strike price than the long puts. This defines the risk profile.

Net debt is usually paid to open the trade, but credit put ratio back spreads are also possible.

Payout Profile

Maximum profit is capped if the underlying drops below the long put strike at expiration. Profit is the difference between the strike prices minus net debit.

Maximum loss occurs if the underlying is above the short put strike at expiration. Loss is limited to the net debit paid.

The position is profitable between the strike prices. The short puts limit upside potential while long puts reduce downside risk.

Leverage from the additional short puts allows outsized returns from moderate downward moves between the strikes.

Factors Affecting Performance

The ratio of long puts to short puts impacts leverage and risk. A higher ratio increases leverage but also risk.

A wider distance between strike prices reduces cost but also caps upside potential. Closer strikes increase leverage.

Implied volatility affects option premiums. Higher IV helps position entry and management. Lower IV reduces the upside.

Time decay erodes extrinsic value, helping the short puts expire worthless. More time allows greater downward movement.

The timing of volatility and price movements affects P/L. Optimally, volatility rises, then underlying drops before expiration.

Managing Early

Take profits early if the underlying drops fast below the long put strike. Don’t get greedy, hoping for maximum profit.

Consider rolling position if modestly profitable and time remains. This allows benefiting from ongoing time decay.

Hedge or exit position if underlying rallies above the short put strike to avoid further losses.

Adjust strikes or ratios if the outlook changes. Provides flexibility to evolve position setup as conditions change.

Risk Management

Sizing position appropriately and limiting outright risk exposure is critical given the leverage involved.

Long puts mitigate downside risk from unforeseen large drops in underlying. Avoid over-leveraging.

Maximum loss should be an amount the trader is comfortable with losing. Capped and defined risk.

Spreading strikes widely to reduce cost also reduces the break-even range. Wider max profit zone but narrower profitability.

The put ratio backspread provides options leverage tied to bearish outlooks while using long puts to limit downside risk exposure simultaneously. Proper construction, management, and risk control allow benefiting from moderate declines in the underlying asset.

What are the components of Put Ratio Backspread?

The first component of a put ratio backspread is buying long puts at a lower strike price. Here are some important facts about long puts.

Involves purchasing puts at a strike below the current market price of the underlying asset. For example, long Rs. 45 puts when stock is trading at Rs. 50.

The number of long puts purchased exceeds the number of short puts sold, creating a net debit to enter the trade. Typically, a ratio of 2:5 is used.

The long puts create unlimited profit potential if the stock falls sharply below its strike price at expiration.

They also define the maximum loss if the stock remains above the short put strike at expiration. Loss is limited to the net debit paid.

The more out of the money the strike, the lower the premium cost but the smaller the leverage. Deeply, OTM strikes require bigger drops in profit.

Longer-dated puts provide more time value but also cost more. Short-dated puts are cheaper but need larger moves.

The goal is for the stock to drop below the long put strike so it gains intrinsic value at expiration.

The long puts create leverage and unlimited upside if the stock crashes. But they also define the fixed maximum loss if the stock fails to decline. Strike selection and expiration are key considerations.

The second component is selling short puts at a higher strike price. Here are some important facts about shortcuts.

Involves selling puts above the current market price. For example, a short Rs. 50 puts when stock trades at Rs. 50.

Fewer puts are sold than purchased at the lower strike, creating the net debit to establish the trade.

Selling the puts generates immediate income in the form of premium received. This lowers the cost basis.

The short puts create obligations to buy the stock if assigned at the higher strike price.

The ideal scenario is for the stock to drop below this strike so the short puts expire worthless and uncovered.

The short puts cap the maximum profit potential if the stock crashes below the long put strike.

The sold puts generate income to lower the trade cost while also capping gains in a sharp decline. Strike selection impacts risk and return.

How does a Put Ratio Backspread affect your initial investment?

A put ratio backspread either increase or decrease your initial investment depending on how the trade is structured and how the underlying asset price moves. There are four key ways a put ratio backspread impacts your initial capital outlay.

Most put ratio backspreads are opened for a net debit – you pay a premium to establish the trade. This net debit is your maximum risk and reduces your initial investment. However, inverted put ratio backspreads are opened for a net credit. This net credit is added to your account and increases your initial investment. Wider strike distances and a higher ratio of short to long puts make net credit put ratio backspreads more likely. The maximum risk is still capped at the net debit/credit even though it impacts initial capital differently.

The short puts in a put ratio backspread allows controlling a larger dollar amount of the underlying asset compared to just buying puts outright. This leveraged notional exposure sometimes increases the upside potential without requiring a proportional increase in capital outlay. Effectively, the strategy sometimes provides greater upside with limited invested capital through the power of leverage. However, the caveat is that leverage also compounds losses if the trade moves against you, resulting in an amplified downside from over-leveraging.

The maximum loss on the trade is defined and capped at the net debit paid upfront. This cap on risk limits capital exposure. Knowing the exact amount of capital at risk allows appropriate position sizing relative to account size and risk tolerance. Compared to buying puts alone, the put ratio back spread has a lower break-even point and thus reduces the capital exposed to losses. The defined and capped risk profile keeps the asset allocated to the trade fixed and controlled.

Put ratio backspreads provide similar risk/reward profiles to long puts at lower capital requirements. Selling additional short puts lowers net cost and capital outlay needed to establish the position. The lower capital requirements make the strategy accessible to smaller accounts. Achieving exposure with limited invested capital frees up capital for other opportunities.

What are the advantages of using Put Ratio Backspread?

Put ratio backspreads are advantageous options trading strategies when used in the right situations. Here are five of the major benefits.

Defined and Capped Risk Profile

One major advantage of put ratio backspreads is the defined and capped risk profile. Maximum potential loss is limited and known upfront before entering the trade. Maximum loss occurs if the stock remains above the short put strike at expiration. Loss is defined as the net debit paid to establish the position. The trade has a built-in stop loss at the amount debited. Risk is capped no matter how far the stock sometimes falls. Knowing maximum loss in advance provides strategic risk management compared to outright long puts.

Lower Cost Structure

Put ratio backspreads sometimes achieve leveraged exposure for a lower upfront cost. Selling the short puts generates instant premium income. This lowers the net debit required to establish the position. The short puts subsidize the cost of the long puts. Requires less capital than buying long puts outright. Achieves greater leverage per dollar invested. The defined risk reduces the break-even relative to the capital invested.

Benefits from Increasing Volatility

Another advantage is positive vega exposure that benefits from rising volatility. Volatility increase boosts long put values faster than short puts. So, a volatility spike sometimes significantly increases the position value. Helps widen the edge compared to straight, long put positions. Provides volatility asymmetry not seen in simple option trades. The structure profits from volatility expansion, unlike most basic options strategies.

Optimised for Moderate Downtrends

The ratio structure is optimized for profiting from moderate downtrends. Performs best if the stock drops between the long and short strikes. Short puts expire worthless, while long puts gain value. The strikes are sometimes selected to match the expected downtrend. It is more efficient than outright puts if targeting a limited decline. The sweet spot hit rate is sometimes quite high when forecasted accurately.

Access to Unlimited Profit Potential

Despite the short puts limiting gains from a crash, profit potential remains uncapped. Further profits result if the stock declines below the long put strike. Allows participating in sharp downtrends beyond the short strike. Remaining long puts continue benefiting if the decline extends. There is no upside limit like a vertical credit spread.

The defined risk parameters, low-cost structure, vega asymmetry, optimized moderate decline targeting, and uncapped profit potential give put ratio back spreads a unique strategic advantage worth leveraging. They offer an asymmetric options strategy with benefits above and beyond those of straightforward long puts when used carefully based on trade outlook.

What are the disadvantages of using Put Ratio Backspread?

While ratio backspreads are advantageous under certain circumstances, there are also inherent disadvantages or risks to consider.

Requires Substantial Downward Move

The main drawback is a put ratio backspread requires a significant downward move in the underlying stock to become profitable. The Break-even is at the short put strike minus the debit paid. Often requires the stock to drop 5-10% to reach break-even. The deal sometimes loses money if the fall is smaller than expected. Has a negative theta, so time decay works against the position without a move downward. The opportunity cost of capital if the stock trades flat or upward. The high break-even relative to the stock price means profitability is dependent on a sizable selloff.

Capped Profit from Large Drops

The structure also caps the profit potential from a large, sharp selloff in the stock. The short puts limit gains if the stock crashes below the long strike. For very bearish outlooks, long puts are sometimes more optimal. The maximum profit is constrained between the two strikes. Other bearish strategies like put spreads allow greater gains. While gains continue mildly after the short put cap, extreme crashes are not maximized.

Time Decay Sometimes Hurt Without Volatility

Since a put ratio back spread has negative theta, time decay sometimes hurts the position. As expiration approaches, the puts lose value from time decay. This erosion hurts without stabilization or a decline in the stock. Theta acceleration into expiration also impacts the position. Needs volatility expansion or a downward move to outpace time decay. Sustained sideways or upward drift in the stock will steadily drain profits.

Assignment Risk on Short Puts

The short put component creates stock assignment risk if the stock drops below the short put strike, risk of put assignment. Requires proactive management and monitoring. Sometimes, it results in unwanted stock ownership if not closed out timely. Exercising the long puts to cover is not preferable either. The short puts introduce additional risks to manage around the assignment.

Bid/Ask Spread Impact on Upfront Costs

Wide bid-ask spreads on the options sometimes negatively impact the put ratio structure. The net debit price includes crossing wide bid-ask spreads. This increases the initial cost and lowers break-even. Sometimes, it impacts the attractive theoretical price and risk levels. Liquidity and spread impact should factor into position sizing. Poor options liquidity undermines the edge created on paper.

The complex structure of put ratio backspreads requires expertise to trade properly. The constraints on profit potential, time decay exposure, assignment risks, and wide bid-ask spreads need to be incorporated into trading plan decisions. The disadvantages require active management and prudent position sizing to minimize.

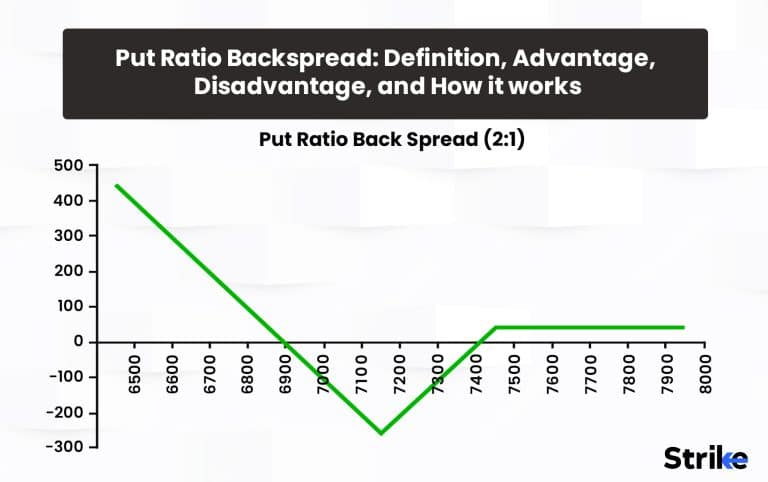

What is an example of Put Ratio Backspread?

A put ratio backspread involves being long puts at a lower strike and short puts at a higher strike, in a ratio greater than 1:1. For example, a trader could establish a 1×2 put ratio back spread by buying 1 put with a Rs. 50 strike and selling 2 puts with a Rs. 55 strike on the same underlying asset and expiration date.

This is a bearish strategy that profits if the asset declines moderately by expiration. However, profits are capped due to the short puts at the higher strike. The long put mitigates losses if the asset rallies sharply beyond the short put strike.

Assume Stock XYZ is now trading at Rs. 60. The following is how a trader starts a 1×2 put ratio back spread for September expiration.

Buy 1 put contract with a Rs. 50 strike at Rs. 2.50 premium.

Sell 2 put contracts with a Rs. 55 strike at Rs. 1.00 premium each.

The net debit to open the trade is as follows.

Long Put Cost: Rs. 250 (1 contract x Rs. 2.50 premium x 100 shares/contract)

Short Put Credit: Rs. 200 (2 contracts x Rs. 1.00 premium x 100 shares/contract)

Net Debit: Rs. 50

The maximum risk on the trade is Rs. 50 net debit paid upfront. This is the trader’s maximum loss.

P/L Scenarios

The following happens if XYZ is less than Rs. 50 at its September expiry.

The long Rs. 50 put is in the money and has Rs. 50 of intrinsic value.

The short Rs. 55 puts expire worthless.

Total profit is Rs. 50 strike difference less Rs. 50 net debit = Rs. 0

The following happens if XYZ is Rs. 53 at September expiry.

The long Rs. 50 put has Rs. 3 of intrinsic value.

The short Rs. 55 puts expire worthless.

Total profit is Rs. 300 – Rs. 50 net debit = Rs. 250

The following happens if XYZ is greater than Rs. 55 at September expiry.

The long Rs. 50 put expires worthless.

The short Rs. 55 puts are in the money, creating a loss of 2 x (Rs. 55 – XYZ price).

The maximum loss if XYZ is above Rs. 55 is the Rs. 50 net debit.

Between the Rs. 50 and Rs. 55 strikes are the profitable zone by expiration. The trader makes the maximum profit if XYZ is below Rs. 50 at expiration.

The upper break-even point is the short put strike + net debit = Rs. 55 + Rs. 50 = Rs. 105

The lower break-even point is the long put strike – (short put strike – long put strike – net debit) = Rs. 50 – (Rs. 5 – Rs. 50 – Rs. 50) = Rs. 45

The transaction is profitable if XYZ is between Rs. 45 and Rs. 105 when it expires in September. Outside of this, the trade loses money. The maximum profit is Rs. 500, and the maximum loss is Rs. 50.

This example demonstrates how a 1×2 put ratio backspread provides leveraged bearish exposure between the strikes while capping losses if the underlying rallies beyond the short put strike. Appropriate position sizing and risk management are key to successfully utilizing this options strategy.

When do you start the Put Ratio Backspread?

The most suitable situation to start putting a ratio backspread is when moderately bearish on a stock’s short-term outlook. Reasons ratio spreads work well in this case are listed below.

The structure is optimized for profiting from limited, moderate price declines.

Provides leveraged exposure without requiring a major crash.

Strike prices are sometimes set to match the expected drop target.

It is more efficient than long puts if only expecting a 5-10% pullback.

Entering when forecasting a modest selloff yields the highest probability of success.

Initiating put ratio backspreads when a stock is pushing up into technical overhead resistance is sometimes advantageous.

Resistance often leads to temporary pullbacks in an uptrend.

Ratio spreads offer a risk-defined way to play the resistance bounce.

The short strike sometimes aligns with support levels below resistance.

Sometimes, the leg into the position as the stock approaches the ceiling.

The defined risk works well for short-term mean reversion setups.

Another good entry point is when a stock is overbought on the relative strength index (RSI) and shows bearish divergence.

RSI above 70 signals overbought conditions ripe for a pullback.

Divergence with price forming lower highs signals waning momentum.

Ratio spreads offer a low-cost way to benefit from the anticipated pullback.

Helps confirm the RSI signal aligns with a tradable options strategy.

RSI and momentum indicators help time countertrend entries.

Entering put ratio spreads after a strong upside move and period of gains also makes sense.

Large runs higher often lead to slight pullbacks or consolidation.

The short put strike sometimes aligns with support levels below.

Caps risk if the stock resumes the uptrend after consolidating.

Predefined risk helps to play mean reversion at swing highs.

It offers a risk-controlled way to benefit from temporary topping patterns.

Implementing a put ratio back spread on an index ETF provides a way to hedge portfolio risk tactically.

Sometimes, scale the position to hedge specific downside risks.

Defines maximum loss while allowing participation in further declines

Resets after expiration, allowing adjusting the hedge as needed

It is more efficient than holding long puts as a constant hedge.

Downside protection is gained around known risks like elections, inflation data, or FOMC meetings.

Optimal timing centers around moderately bearish scenarios for a limited decline. The defined-risk parameters match well with short-term contrarian opportunities.

How to perform Put Ratio Backspread?

The first step to performing a put ratio back spread is to determine if there is a moderately bearish market outlook throughout the options expiration cycle. Assess expected volatility direction – ideally, IV rises, then underlying drops. Evaluate the risk-reward ratio given a modest bearish forecast. Choose a lower strike for long puts below the current underlying price. Select a higher strike for short puts above the current underlying price. Consider the distance between strikes – wider reduces cost but narrows potential profit range. Balance upside profit potential if underlying drops and loss potential if rallies.

Assess the ideal ratio of long puts to short puts based on risk tolerance. Typical 1×2. A higher ratio increases leverage but also risk. A lower ratio reduces cost and risk. Model payoff diagrams at different ratios to visualize the risk-reward profile.

Verify long put and short put strikes, ratio, expiry date, and order type selected. Confirm net debit or credit to open position matches maximum risk tolerance. Double-check all order specifics before submission to avoid errors.

Place buy order for long puts at chosen lower strike. Simultaneously (or in rapid succession), place a sell order for short puts at a higher strike in the desired ratio. Use contingent or bracket orders if available to ensure simultaneous execution.

Monitor price action relative to break-even points. Prepare to close the position if necessary. Consider taking profits early if a move happens quickly in your favor. Roll, adjust strikes, or hedge if the outlook changes. Adapt position to new conditions. Let us allow the position to expire if it is profitable to realize full gains. No action is needed if at a max loss. Act in advance of expiration to handle any exercise/assignment risk on the remaining legs.

How are break-even points calculated in a Put Ratio Backspread?

A put ratio backspread points are calculated based on the strike prices chosen and net debit or credit taken when entering the trade.

The lower break-even point is the level where the total position begins to gain value. It is calculated as stated below.

Lower Break-even = Short Put Strike – Net Debit

The position will only turn a profit if the stock is trading exactly at this lower break-even price at expiration. Below this level is where profits start accruing.

This first break-even level is important for determining the minimum downward move needed before the trade becomes profitable. A higher break-even means requiring a larger selloff.

The upper break-even point is where the maximum potential profit is achieved. This level is calculated as stated below.

Upper Break-even = Long Put Strike + Net Debit

The biggest gain is obtained if the stock is precisely at this break-even at expiration. Any price below the upper break-even does not increase profits further due to the short puts capping the upside.

This second break-even indicates the optimal target price for the maximum risk-reward profile.

Let’s say a put ratio backspread is constructed on stock XYZ.

Sell 2 XYZ 50P for Rs. 2 credit each

Buy 5 XYZ 45P for Rs. 1 debit each

Net Debit = 2 x Rs. 2 – 5 x Rs. 1 = Rs. 3

The break-even would be the following.

Lower Break-even = Rs. 50 – Rs. 3 = Rs. 47

Upper Breakeven = Rs. 45 + Rs. 3 = Rs. 48

So XYZ needs to fall to at least Rs. 47 for gains to start. But the maximum profit is achieved if XYZ drops to Rs. 48 at expiration.

Knowing these two break-even points guides trade management and helps evaluate the probability of success. The break-evens quantitatively define the risk-reward parameters.

Calculating the lower and upper break-even levels on a put ratio backspread provides important insight into the trade structure. Comparing the break-evens to the current stock price indicates the required move and profit potential. This informs decisions around trade management, adjustments, and rolling to continue benefiting from the position’s advantages.

How do you handle risk in a put ratio backspread?

To handle risk in a put ratio backspread, the most important step is defining the maximum loss upfront when entering the trade. The net debit or credit paid to establish the position is the capped and predetermined risk. This strict risk limitation allows appropriate position sizing relative to account size and risk tolerance. During the trade, if the underlying stock price rises above the short put strike at expiration, the maximum loss is incurred as the short puts expire worthless while the long puts also lose value.

To mitigate this risk, the trader should close out the position before expiration if it moves close to max loss by buying back the short puts and selling the long puts. The upside profit potential remains uncapped, so the trader may choose to stay in the trade if the stock declines sharply.

However, they should monitor for opportunities to take profits or adjust the position if the forecast changes. The short puts introduce assignment risk if the stock drops below that strike. Careful monitoring and proactively closing the shorts before expiration reduces this risk. Overall, the defined and capped risk structure allows for managing overall risk, but active adjustment may still be required if the price action unfolds unfavorably.

Is Put Ratio Backspread a bearish strategy?

Yes, a put ratio backspread is considered a bearish options trading strategy. The put ratio backspread aims to profit from a moderate decline in the underlying asset price. Buying long puts provides direct bearish exposure that increases in value as the price drops. The short puts add leveraged downside exposure compared to simply buying puts alone.

The ideal scenario is for the asset price to fall below the long put strike at expiration so the maximum profit is achieved. This accrues gains in a bearish outcome.

While the short puts limit the profit from substantial declines, the overall positioning benefits from drops in the underlying. The maximum loss is also defined if the asset rises.

A put ratio backspread is initiated for a net debit, reducing the upfront cost of implementing this bearish market view. The sweet spot is a moderate fall, not a crash. It provides a way to trade bearish while limiting risks.

So, while the strategy has a more nuanced risk profile than outright bearish trades, the overall bias profits from and is geared towards drops in the underlying.

How efficient is Put Ratio Backspread?

A put ratio backspread is an efficient structure for bearish options trades. The short puts provide leveraged exposure to the underlying for a lower capital outlay compared to simply buying puts outright. This substantially increases returns on the invested capital. Furthermore, selling the additional short puts lowers the net debit required to open the trade compared to long puts alone.

The premium collected from the shorts helps subsidize the cost of the long puts. This cost reduction means the position has a lower break-even point. At the same time, the long puts cap the maximum loss strictly to the net debit, so risk is defined. The leverage and lower cost structure allow efficient access to strategic exposures with limited impact on capital. When used prudently, a put ratio backspread delivers bearish options exposure and defined risk with an efficient use of capital.

When to enter using Put Ratio Backspread?

The best time to enter using a Put Ratio Backspread is when you have a moderately bearish forecast on the underlying stock. Specifically, you expect the stock to decline modestly by an amount larger than the net debit paid to initiate the position. This decline should target the zone between the short put strike and the long put strike to maximize profits.

Entering when implied volatility is high can reduce the net debit cost and break-even point. The elevated IV also means volatility has room to expand, benefiting the long puts. You want to optimize initiating the position for an upcoming period of stabilized or increasing IV followed by a downward drift in the stock price. Always assess the risk-reward payoff diagram at initiation to confirm acceptable profit potential relative to maximum loss.

Be sure to use proper position sizing so the defined risk fits your account size and risk tolerance. Executing the long and short legs simultaneously with contingent orders ensures you get the intended net debit price. In summary, the ideal time to enter a put ratio backspread is when forecasting moderate downside coupled with expanding volatility in the near term that allows an efficiently structured risk-reward payoff.

When to exit using Put Ratio Backspread?

The best time to exit using a Put Ratio Backspread is when you have realized your desired profit target or the trade has reached maximum loss. If the forecasted moderate decline occurs swiftly, you may look to take profits by buying back the short puts and selling the profitable long puts.

This allows capturing the gains prior to expiration. If the stock stabilizes or drifts higher, you can close the position before the maximum loss is reached to limit the damage. Actively manage the position as the outlook changes by rolling, adjusting strikes, or hedging. You want to exit before expiration to avoid assignment risk on the short puts if the stock drops below that strike.

Monitor time decay as expiration approaches and evaluate whether volatility expansion still warrants holding the position. If the negative theta decay outpaces volatility benefits, close the position. The maximum loss is reached if the stock expires above the short put strike. No action is required at max loss since the position expires worthless.

What is the maximum profit in using Put Ratio Backspread?

The maximum profit in using a Put Ratio Backspread occurs when the underlying stock price declines below the strike price of the long puts at expiration. The maximum profit is capped between the strike price of the short puts and the strike price of the long puts. Here’s an example to illustrate.

Say a trader initiates a 1×2 put ratio backspread on XYZ stock with the following structure.

Sell 2 XYZ 50 Puts

Buy 1 XYZ 40 Put

XYZ falls to Rs.35 at expiration, and the maximum profit potential is realized. The short 50 puts expire worthless for no loss. The long 40 put is deep in the money and has an intrinsic value of 50 – 40 = Rs.10. With the 1×2 ratio, the maximum profit is 2 * Rs.10 = Rs.20.

Although the stock could fall further below 35, the maximum profit is capped between the strikes at 40 – 50 = Rs.10 per spread unit. Essentially, the short 50 puts limit the profit on the long 40 puts to the distance between the strikes. The ultimate maximum profit depends on the number of units traded.

What is the maximum loss in using Put Ratio Backspread?

The maximum loss in using a Put Ratio Backspread is limited to the net debit paid when opening the position. Here’s an example to illustrate: Say a trader initiates a 1×2 put ratio backspread on XYZ stock for a net debit of Rs.200 per unit. This means

– Paid Rs.200 x 1 unit = Rs.200 to buy 1 XYZ 40 Put

– Received Rs.100 x 2 units = Rs.200 to sell 2 XYZ 50 Puts

Net Debit = Rs.200 – Rs.200 = Rs.200

The maximum loss occurs if XYZ stock expires above the short 50 strike at expiration in this scenario.

– The long 40 put expires worthless for a Rs.200 loss

– The short 50 puts expire worthless for no loss

Since the trader paid Rs.200 to open the position, the maximum loss is capped at Rs.200 if XYZ remains above 50 at expiration. This Rs.200 was the defined and maximum risk when establishing the trade. The maximum loss is predefined as the net debit paid when initiating the put ratio backspread. The short puts cap and define risk, while the long puts provide upside potential.

How often is Put Ratio Backspread used by traders?

Put Ratio Backspread used by traders is a more advanced options strategy that requires some specialized knowledge and active position management. As a result, it tends to be used less frequently than more basic strategies like buying calls or puts outright.

The strategy is most often employed by sophisticated options traders and active investors who understand the nuances and have skills in actively managing the position. The structure is less accessible to casual options traders.

Initiating the trade requires accurately forecasting both the magnitude and timing of an expected downward move in the underlying stock. This directional outlook and price target forecasting limits usage frequency.

Managing the timing of the entry, closing out legs, adjusting to changing conditions, and avoiding risks like assignments requires expertise. This active management component curbs widespread adoption.

The defined risk parameters appeal to prudent traders looking to mitigate risk exposure on a bearish forecast efficiently. But, learning the strategy is still required.

Is the put ratio backspread an effective strategy?

Put ratio backspread is an effective options strategy in certain situations for traders who use it properly. It provides leveraged exposure for a lower cost compared to simply buying puts outright. The structure is capital efficient and maximizes bearish exposure per dollar invested. This leverage boosts returns when the forecast is correct.

The defined and capped risk parameters allow for mitigating the downside. The maximum loss is strictly limited to the net debit paid upfront. This helps control overall risk in the trade.

Implied volatility skews are present, and the shot put and the sold at high implied volatility for an edge. The long puts benefit if volatility then expands. This volatility asymmetry improves effectiveness.

However, the strategy is complex and requires specialized expertise. Forecasting ability and active management of the moving parts are critical to utilize it effectively. It also lacks robustness to varying market conditions.

So, in the right situation, traders with sufficient knowledge can use a put ratio backspread effectively. However, it is not an effective strategy across all market environments and trader skill levels.

What is the difference between Put Ratio Backspread and Call Ratio Backspread?

The main difference between Put Ratio Backspread and Call Ratio Backspread lies in the opposite risk profiles created by the put versus call legs.

A put ratio backspread combines long puts and short puts. The long puts have limited risk and uncapped upside potential if the stock declines. The short puts create defined and capped risk if the stock rallies. This structure creates leveraged exposure to downside moves.

In contrast, a call ratio backspread combines long calls and short calls. Now, the long calls create capped risk but unlimited profit potential if the stock rises. The short calls introduce defined and limited risk if the stock declines. This structure provides leveraged exposure to the upside.

While both strategies use a ratio spread to enhance leverage compared to outright long positions, the put ratio targets bearish moves, whereas the call ratio targets bullish moves.

The put structure benefits from volatility expansion and downside. The call structure benefits from volatility rises coupled with upside.

Both require forecasting ability, active management, and risk mitigation knowledge to trade effectively. The primary difference lies in whether seeking leveraged exposure to upside or downside based on market outlook.

Previous Article

Previous Article

38")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 40")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 41")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 42")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 46")

No Comments Yet.