A long iron butterfly is a limited profit and limited risk options trading strategy used when an investor expects low volatility in the underlying asset. Long iron butterfly involves buying a call spread and putting a spread with the same strike prices while shorting a call and putting it with a strike price between the spreads.

The sold calls and puts at the middle strike price fund the long options, making the net debit small. The maximum profit is attained if the underlying is at the short strike at expiration. Profit is limited by the difference between strikes minus net debit paid. The maximum loss occurs if the underlying is outside the outer strikes.

A long iron butterfly benefits from low volatility expectations, as time decay erodes the short options faster than the longs. It risks losing the premium paid if volatility rises substantially. It is a defined risk strategy allowing advanced traders to profit from a rangebound forecast. Examples could include pre-earnings plays or rangebound indices. Overall, the long iron butterfly is best used when anticipating a period of low volatility.

What is the importance of the Long Iron Butterfly in Options Trading?

The Long Iron Butterfly is an important advanced options trading strategy that involves buying a call spread and putting a spread with the same strikes and expiration dates. It is one of the limited-risk, limited-profit option trading strategies that help limit the trader’s risk exposure while also capping the potential profit.

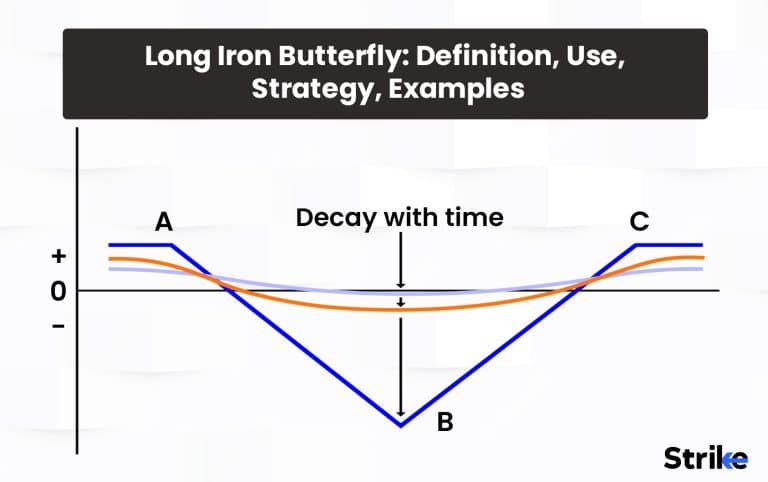

The Long Iron Butterfly gets its name from the shape it forms on the risk graph, resembling a butterfly. To initiate the strategy, the trader buys a lower strike out-of-the-money call option, sells an at-the-money call option, buys an at-the-money put option, and sells a lower strike out-of-the-money put option, all with the same expiration date.

The Long Iron Butterfly strategy aims to profit from the lack of movement in the underlying asset when the options expire. The maximum profit is attained when the underlying asset closes right at the short strike price at expiration. In this case, both the call spread and put spread expire worthless, allowing the trader to keep the entire initial credit received when putting on the trade.

The key advantage of the Long Iron Butterfly is that it offers a high probability of earning a small limited profit when the underlying stock is expected to have low volatility. The maximum loss is also limited and occurs when the stock closes below the lower strike put or above, the higher strike call at expiration. This defined risk-reward profile makes it appealing for traders looking to collect small premiums with a high probability of success.

While constructing the Long Iron Butterfly, it is important to choose options with adequate liquidity to ensure there is sufficient market interest on both the call and put side. The short strikes are typically chosen at-the-money or very close to the current price of the underlying. The wing spreads should also be equidistant from the short strikes to balance the position.

The trader wants the stock price to remain stable right around the short strike price for maximum profit potential. Any significant upside or downside move reduces the premium collected or leads to losses beyond the initial credit. Therefore, proper stock selection is key when using this strategy.

Ideal conditions for the Long Iron Butterfly include neutral sentiment on the stock, low implied volatility, and the expectation of stagnant price action. Earnings announcements, pending news events, and high-volatility stocks are best avoided when employing this strategy. Proper timing around events increases volatility is crucial.

The Long Iron Butterfly is often compared to the Long Iron Condor strategy, which also aims to profit from low volatility. The key difference is that while the Iron Condor involves wearing a wider wingspread for higher potential profit, the Iron Butterfly condenses the wingspread for a higher probability of profit. The condensed wingspread reduces potential reward in exchange for a higher likelihood of success.

How does a long iron butterfly work?

The long iron butterfly works when a trader buys a lower strike out-of-the-money call option, sells an at-the-money call option, buys an at-the-money put option, and sells a lower strike out-of-the-money put option. For example, with the stock trading at Rs.50, the trader could buy a 40-strike call, sell a 50-strike call, buy a 50-strike put, and sell a 40-strike put. All the options would have the same expiration date.

The purchase of the lower strike call and put spreads forms the wings of the position. The short calls and puts at the middle strike form the body. This creates a risk graph shaped like a butterfly, hence the name Iron Butterfly.

The trader receives a net credit when entering the trade since the middle-at-the-money short options bring in more premium than the farther out-of-the-money long-wing options cost. The maximum profit is equal to this initial net credit received.

At expiration, if the stock closes exactly at the middle strike price of the short call and put options, then all the options expire worthless. The trader gets to keep the entire initial credit as profit. This is the maximum profit scenario.

Substantial losses occur with stock finishes below the lower put strike or above the higher call strike. Losses grow the further away the stock moves from the middle strike at expiration. However, the loss is capped due to the wings created by the long call and put spreads.

The trader wants the stock to finish as close to the middle strike as possible. Any significant price movement below the put wing or above the call wing will reduce profits or create losses.

The Long Iron Butterfly strategy aims to profit from neutral conditions and low volatility when the stock price finishes close to the middle strike at expiration.

Ideally, implied volatility is low, as that results in cheaper options pricing and more net credit when initiating the trade. Lower volatility also increases the likelihood of the stock finishing near the middle strike.

The trader wants neutral sentiment and a stagnant stock price. Any bullish or bearish bias creates directional risk and increases the chance of the stock finishing outside the wings. News events, earnings reports, and other catalysts that could increase volatility should be avoided.

Proper stock selection is crucial. Stable, low-beta stocks are ideal candidates for the Long Iron Butterfly strategy. The stock should have a history of making small moves around a predictable range rather than making explosive directional runs.

The Long Iron Butterfly has a clearly defined maximum loss, which is capped by the wings of the long call and put spreads. This helps contain the downside. The maximum loss occurs if the stock closes below the lower put strike or above the higher call strike at expiration.

The trader adjusts the width between the wings, the middle strikes, and the expiration date to define their comfort level with risk versus profit potential. Widening the wings helps reduce risk but also lowers the net credit. Moving the middle strikes further apart has a similar effect on defining risk parameters.

Actively monitoring the trade and closing early if the stock moves outside the wings is prudent risk management. The trader gives back some profit but avoids incurring large losses if volatility increases sharply. Portfolio diversification is crucial because losses will accumulate on multiple Iron Butterfly positions if a sudden market reversal occurs.

What is an example of a long iron butterfly?

Let’s assume ABC stock is currently trading at Rs.50 per share. An options trader believes ABC will remain relatively flat and trade within a narrow range until options expiration in 6 weeks. The trader decided to implement a Long Iron Butterfly strategy on ABC to profit from the expected low volatility. Here are the 6 steps to construct the trade.

The trader first buys 1 contract of the 40-strike call option that expires in 6 weeks. With ABC at Rs.50, this call option is out-of-the-money. The trader pays a premium of Rs.1 per contract for this long call. The 40-strike call acts as the lower wing of the Iron Butterfly and helps limit the trader’s risk if the stock drops below 40 at expiration. It also reduces the net cost of the overall trade.

The trader then sells 1 contract of the 50 strike call, which is at-the-money with the stock at Rs.50. They collect a premium of Rs.3 per contract for this short call.

The 50-strike call forms the body of the Iron Butterfly. The trader is betting that ABC will be very close to Rs.50 at expiration, so this call expires worthless.

Next, the trader buys 1 contract of the 50 strike put. This put is also at-the-money with the stock at Rs.50 and costs the trader a premium of Rs.3 per contract.

Buying this put completes the body of the Iron Butterfly and helps limit the downside risk. Having a long put and call at the same strike provides symmetry to the trade.

Finally, the trader sells 1 contract of the 40-strike put to form the lower risk-limiting wing on the put side. They collect a premium of Rs.1 per contract for the short put position.

The trader now has all the required legs of the Iron Butterfly in place – a 40/50 call spread and a 50/40 put spread sharing the same expiration date.

Adding up the premiums paid and collected, we have the below.

Paid Rs.1 x 1 contract for the long 40 call.

Collected Rs.3 x 1 contract for the short 50 call.

Paid Rs.3 x 1 contract for the long 50 put.

Collected Rs.1 x 1 contract for the short 40 put.

Results in a Net Credit of Rs.2 received by the trader.

This represents the maximum potential profit on the trade if ABC closes exactly at Rs.50 at expiration. The Rs.2 initial credit is retained.

The maximum risk is defined by the width of the wingspreads. Here, it is Rs.8 per contract (distance between strikes of 40 and 50).

As expiration approaches, the trader will monitor the price action of ABC closely. The Iron Butterfly strategy is on track to achieve maximum profit if ABC remains stable at around Rs.50.

The trader chooses to close the position early and take a smaller profit or reduced loss if ABC trends below 40 or above 50. The maximum loss of Rs.8 is incurred if ABC trends below 40 or above 50.

The Long Iron Butterfly provides a way to potentially profit from ABC trading in a range while defining risk. The wings help contain losses while the body positions aim to expire worthless for maximum profit.

What are the advantages of the Long Iron Butterfly?

The Long Iron Butterfly is an advanced neutral options strategy that offers traders 8 key advantages, including limited risk, high-profit chance, defined profit potential, etc.

1. Defined and Limited Risk

One of the main benefits of the Long Iron Butterfly is that it has a defined and capped risk profile. Maximum loss is limited and occurs if the underlying stock closes below the lower strike put or above, the higher strike call at expiration.

The wings created by the long out-of-the-money call and put spreads contain the loss to a fixed amount compared to short options strategies that have an uncapped downside. Knowing the maximum loss in advance helps traders carefully size positions and manage risk in the trade.

2. High Probability of Profit

The Long Iron Butterfly offers a high statistical probability of earning a profit when constructed properly. The maximum profit is achieved if the stock finishes right at the short strike. The condensed wingspreads boost the likelihood of expiration occurring within the wings.

Probability is further enhanced when volatility is low, and the stock is expected to remain range bound. The high probability of a small profit makes Iron Butterflies popular for consistent income generation.

3. Capped and Defined Profit Potential

The Long Iron Butterfly also defines max profit, which is equal to the initial net credit received when opening the trade. The short options decaying over time combined with the long options offset each other’s cap profit at a set level.

Knowing the maximum gain in advance allows traders to assess their risk-reward ratio. The capped profit is small, but it comes with a high probability of being retained at expiration.

4. Leverage from Credit Received

The Long Iron Butterfly generates income in the form of credit received from the short options expiring worthless. The time decay benefits received from the body of the trade are greater than the cost paid for the wings.

This nets an overall credit, providing leveraged profit potential relative to the minimum margin requirement. Gaining exposure with a smaller outlay is an inherent advantage of credit-based strategies.

5. Low Capital Requirements

Speaking of margin requirements, the Long Iron Butterfly carries modest capital requirements relative to the total contracts traded. Only the wings have an outlay, while the body brings in credit.

The ability to efficiently utilize capital and margin allows traders to implement multiple Iron Butterfly positions on a variety of stocks and broaden their diversification.

6. Wide Range of Implementation Methods

The Iron Butterfly is highly customizable, providing the flexibility to modify key components like the strikes, expiration, and width between the wings.

Traders get adjusted to this strategy based on their market outlook, risk tolerance, and desired probability of profit. The availability of weekly options contracts further expands implementation possibilities.

7. Benefits from Any Market Conditions

Iron Butterflies are structured to profit from rangebound, neutral, volatile, or directional markets when properly constructed. Traders modify the strikes and wingspreads to match their forecast.

The versatility allows Iron Butterflies to generate income opportunities across diverse sectors and various market environments. Traders capitalize regardless of the overarching conditions.

8. Trading Volatility and Time Decay

Since the Long Iron Butterfly benefits from low volatility and time decay, it allows traders to implement views on implied volatility rather than just direction. Profiting from vega and theta expands the number of exploitable opportunities.

With defined risk, a high probability of profit, modest capital requirements, and broad customization potential, the Long Iron Butterfly is an adaptable options strategy. Its flexibility to structure the wingspreads and profit from time decay in any market conditions makes it a versatile tool for income generation. The Long Iron Butterfly provides experienced options traders with an advantageous strategy when crafted properly.

What are the disadvantages of Long Iron Butterfly?

The 8 potential disadvantages and limitations of using the Long Iron Butterfly options trading strategy are mentioned here. This includes capped potential, narrow profit zone, expiration risks, etc.

1. Capped Profit Potential

The maximum profit on the Long Iron Butterfly is limited to the initial net credit received. Even if the underlying stock moves favourably, the structure of the trade prevents any additional gains beyond the credit.

The capped upside is more disadvantageous compared to strategies like the Long Call that have unlimited profit potential during a bull run. Traders sacrifice further profits for downside protection.

2. Narrow Profit Zone

For maximum profit, the stock must close precisely at the short strikes. Any significant movement above or below that zone erodes profits quickly. This makes the range of profitability very narrow.

A sudden price swing in either direction could turn a winning trade into a loser. The condor structure does not provide much leeway outside the short strikes.

3. Expiration Risk

All profits or losses are realized at expiration per the structure of the Long Iron Butterfly. This makes proper timing and execution vital. Early assignment or exercise could force traders out of positions at suboptimal prices.

The time decay that boosts profits also works against the position closer to expiration. Traders might have to accept less than maximum profit if they close the trade prior to expiration.

4. Requires Low Implied Volatility

The Iron Butterfly works best when volatility is low, and the stock is expected to move sideways in a range. In volatile markets with expanding price swings, losses exceed the wings quickly as the stock trends away from the short strikes.

Timing the trades around upcoming events that increase volatility is crucial to avoid uncontrolled losses.

5. Requires Neutral Outlook of Stock

Since the Iron Butterfly benefits from rangebound conditions, it does not perform well if the stock exhibits a pronounced bullish or bearish bias. Directional movement outside the wings leads to losses.

Traders should avoid stocks with clear uptrend or downtrend patterns. The strategy is better suited to stable, low-beta stocks.

6. Erosion Due to Time Decay

While the passage of time boosts profits on the short options, time decay also erodes the value of the long-wing options. This factor makes holding till expiration problematic if the stock remains stationary.

Managing the trade before expiration often becomes necessary to lock in profits and avoid time decay eroding the wings’ protection. This requires active monitoring.

7. Assignment Risk on Short Options

The dual short options at the middle strike carry early assignment risk. Traders face losses well in exceeding the maximum loss at expiration if assigned early on a large upward or downward swing.

Rarely does this event devastate an Iron Butterfly position and lead to margin calls. Defined risk goes out the window if assigned prematurely.

8. Requires Collateral/Margin to Construct

Unlike credit spreads, the Iron Butterfly requires margin and collateral to construct since the wings have an outlay. The locked-up capital could otherwise be deployed elsewhere for better returns.

The economics of the trade must justify tying up capital that could be utilized to put on additional positions instead. This impacts opportunity costs.

With its narrow profit zone, expiration risks, time decay erosion, and margin requirements, the Long Iron Butterfly has notable limitations. Proper construction, timing, and active management are essential to overcome its capped upside potential, early assignment risks, and vulnerability to volatility. The drawbacks outweigh the advantages of this strategy when not implemented judiciously.

How risky is Long Iron Butterfly?

The Long Iron Butterfly is generally considered a limited-risk options trading strategy. It has a clearly defined maximum loss, capped profit potential, and breakeven points that are calculated prior to entering the trade. However, there are some risks associated with the Long Iron Butterfly that traders should be aware of.

One of the benefits of the Long Iron Butterfly is that maximum loss is well-defined and capped. The maximum loss occurs if the underlying stock closes below the lower strike put or above the higher strike call at expiration.

The maximum loss equals the difference between the strike prices of the long and short options minus the initial credit received for selling the short options.

For example, if the strikes are 40, 50, and 60, the maximum loss would be 60 strikes minus 40 strikes or 20 points, minus the original credit collected. The width between the wingspreads caps the loss on the trade.

However, it is possible for assignments to occur on the short options prior to expiration. This could lead to greater losses beyond the defined risk based on where the underlying is trading at that point.

The Long Iron Butterfly has a well-defined profit zone with breakeven points above and below the short-strike prices. The maximum profit, which equals the initial credit received, occurs if the stock expires precisely at the short strikes.

The upside breakeven point is equal to the higher strike call minus the credit received. The downside breakeven is the lower strike put plus the credit. A profit is retained if the stock closes within these breakeven points.

Beyond the breakevens, incremental losses start occurring. While the breakeven points help quantify risk, the stock quickly swings outside the profit zone. A sudden price move beyond the breakeven point turns an intended profit into a loss in a short period of time.

While time decay works in favour of the short options, the passing of time also erodes the extrinsic value of the long-wing options. Time decay crushes the value of the wings and leaves the position unprotected if volatility remains low and the stock doesn’t move much,

Any increase in volatility also expands the expected range of stock movement, raising the probability of closing beyond the breakeven points. Reduced time value and higher volatility both work against the success of the position.

Early assignment, while rare, remains a possibility on the short options, especially when dividends are involved. Substantial losses occur well beyond the maximum loss at expiration. If assigned early, exercise on the long options could also force liquidation before ideal points are reached. Additionally, exercise and assignment risk increases exponentially as expiration approaches. The accelerated time decay near expiration provides very little protection if the stock makes an unexpected move.

Proper position sizing, portfolio diversification, and avoiding overconcentration are key to managing the downside risks. Outsized exposure to one stock or sector spells troubles if a sudden downturn in volatility or prices occurs. The losses accumulate quickly.

What are the things to consider before applying for the Long Iron Butterfly?

There are 10 key considerations when evaluating whether to apply the Long Iron Butterfly options trading strategy.

1. Neutral Outlook on the Underlying

The Long Iron Butterfly profits from a stagnant stock price and low volatility environment. It performs best when the trader has a neutral bias and expects a relatively tight trading range. Any pronounced bullish or bearish outlook that could cause a directional bias increases risk.

2. Implied Volatility Levels

Implied volatility directly impacts options pricing. Lower IV results in cheaper options prices, increasing the credit received when initiating the trade. Traders want to deploy Iron Butterflies when the IV rank is low relative to its past range. High IV environments expand the expected range of stock movement and the probability of breakeven points being hit.

3. Upcoming Events or News

Earnings reports, FDA decisions, analyst days, and other potential catalysts that could increase volatility should be avoided when implementing Iron Butterflies. The unknowns around market-moving events boost uncertainty leading into the announcements. Traders should steer clear of stocks with major pending events.

4. Technical Factors

Technicians should evaluate trends, support/resistance levels, moving averages, volume patterns, and chart formations to assess expectations of rangebound conditions. Stocks exhibiting solid uptrends or downtrends are not ideal candidates for Iron Butterflies, which benefit from sideways consolidations.

5. Fundamental Factors

The company’s financial health, growth metrics, valuation, competitive advantages, market position, debt levels, and other fundamental factors provide insights into the stability of the business. Heavily indebted, unprofitable, struggling companies are more prone to making explosive directional moves versus quality stable large-caps.

6. Sector and Industry Conditions

The broader sector and industry trends also impact the likelihood of stocks making sizable moves in either direction. Sectors prone to volatility, like biotech or cyclical industries dependent on economic cycles, carry additional risks versus defensive non-cyclical sectors.

7. Liquidity of the Options

Illiquid options with wide bid-ask spreads should be avoided, especially for short strikes. Thin markets increase the difficulty of entering and exiting trades at preferable prices. Traders want high liquidity and tight spreads to smoothly manage the multiple-leg structure.

8. Dividend Risks

Stocks paying dividends around the expiration date increase early assignment risks on short options positions. The carrying cost is transferred to the option holder before the ex-dividend date. Dividend capture strategies adversely impact Iron Butterfly trades.

9. Earnings Around Expiration

Similarly, earnings announcements near expiration tend to increase volatility and uncertainty over a company’s near-term direction right as the options expire. The unknowns make managing the strategy at expiration more difficult.

10. Portfolio Diversification

Maintaining a diversified portfolio is key to managing Iron Butterfly risks across multiple stocks and sectors. Overconcentration into any single name increases correlation risks if a stock or sector decline emerges. Avoiding correlated positions is prudent.

When weighing the Long Iron Butterfly, traders should analyze the stock’s volatility, technical and fundamental factors, upcoming events, sector trends, options liquidity, dividend risk, earnings timing, and diversification needs. Proper situation analysis and prudent position sizing are key to overcoming its limitations. Careful implementation allows for managing its risks and generating consistent income.

When to enter using Long Iron Butterfly?

The ideal time to enter a Long Iron Butterfly centres around neutral sentiment, low implied volatility, and expectations for stagnant trading in the underlying stock over the duration of the trade. As such, traders will look to deploy the Long Iron Butterfly when they get aligned with the following conditions.

Low implied volatility is one of the key components for successfully implementing a Long Iron Butterfly. Options premiums tend to be cheaper when IV levels on options are relatively low. This allows traders to collect more credit when initiating the Long Iron Butterfly trade. Lower IV also indicates expectations for more subdued, rangebound trading rather than explosive directional moves. Traders want to deploy the Long Iron Butterfly when the IV rank or percentile is at the lower end of its historical range.

The sector and industry trends provide insights into expectations for volatility and potential price trends. Stable sector and industry conditions without major fundamental catalysts on the horizon suggest an environment conducive to a Long Iron Butterfly strategy. Monitoring relative strength and momentum across sectors and industries helps identify rangebound opportunities suitable for a Long Iron Butterfly.

Technical analysis metrics such as Bollinger Bands, moving averages, support & resistance levels, and chart patterns are useful for assessing expectations of directional bias versus rangebound consolidation. The Long Iron Butterfly performs optimally when the stock is trading sideways within a well-defined range, oscillating between technical support and resistance levels. Periods of consolidation after a strong uptrend or downtrend are ideal entry points.

It is prudent to avoid initiating Long Iron Butterfly positions on stocks that have major earnings reports or other volatility events scheduled for release during the intended trade duration. The unknowns and uncertainty surrounding such events tend to increase implied volatility ahead of the announcements. Traders should scan the events calendar and look to deploy the Long Iron Butterfly only when no major announcements are imminent.

The Long Iron Butterfly benefits from time decay as the short options expire worthless. However, traders need to ensure sufficient time remains until options expire to allow for the time decay to play out. Initiating Long Iron Butterfly positions with 6-8 weeks until expiration provides more wiggle room. The effects of time decay accelerate in the last 30 days before expiration, so the remaining duration is key.

The Long Iron Butterfly is structured around short strikes equidistant from the current market price, with wings spread out at farther out-of-the-money strikes. Traders seek to find beneficial entry positions with low implied volatility and the best credit spreads in relation to strike distances. This optimizes the trade structure and probability of profit.

When to exit using the Long Combo Strategy?

The Long Iron Butterfly has defined maximum profit and loss levels based on the strikes and wingspreads. However, traders look to exit the positions early under certain conditions before expiration to capture profits or limit losses.

The Iron Butterfly captures 80-90% or more of the maximum profit if the underlying stock is trading very close to the short strikes well before expiration. Traders elect to exit early and realize these sizable gains rather than holding out for the last incremental profit near expiration. The risk of reversals is high near expiration, while most profits are already attained.

The underlying stock approaching key support or resistance levels, especially coupled with increasing volatility, signals a potential breakout outside the profit zone. Technicians will monitor price action around key levels and opt to proactively close out all or a portion of the position to lock in profits before a breakdown.

A significant swell in IV indicates greater expectations for wider price swings and directional move potential. This expands the chances of the stock closing beyond the breakeven points. Traders exit early to avoid vega risk impacting the position’s profitability if IV spikes before expiration.

A major announcement like an earnings report or FDA drug approval decision was not accounted for when initiating the trade, and traders need to close positions early before the unknown event risk. Holding Long Iron Butterfly positions over major events tends to be very risky.

Upon the stock exhibits a definitive breakout and establishes a directional bias violating support or resistance levels, technicians will likely close Long Iron Butterfly positions early. Continuing to hold onto the trade when the rangebound premise fails to hold true results in the maximum loss being realized.

In the last 30 days before expiration, time decay tends to accelerate, which erodes extrinsic value very rapidly. The accelerated time decay overwhelms any remaining profits if the stock isn’t trading near the ideal short strikes. Traders exit around 30 days out.

While early assignment is rare on index options, the risk increases when trading weekly options contracts. Traders look to close out the positions proactively before expiration week to avoid being assigned early at adverse prices on the short options.

The key is to maintain discipline based on the initial assumptions and avoid giving back profits. Traders utilize technicals, volatility analysis, upcoming events, and time decay considerations to close Long Iron Butterfly positions before the maximum loss point is reached. The goal is to capture the majority of profits and mitigate risks ahead of expiration.

How efficient is the Long Iron Butterfly Strategy?

The Iron Butterfly is generally considered an efficient options strategy when implemented correctly under the right market conditions. The 9 main factors impacting the efficiency of the Iron Butterfly strategy include the following.

Defined Risk-Reward Profile

The Iron Butterfly has a defined maximum gain capped at the initial net credit received. It also has a defined maximum loss limited by the width between the long and short strikes. This defined risk-reward profile allows traders to precisely calculate potential outcomes before entering the trade. The ability to pre-determine the risk-reward parameters makes it an efficient strategy.

High Probability of Profit

The Iron Butterfly often provides a probability of profit estimated around 80-90% based on the width between strikes when constructed properly using options pricing models. This high statistical probability of earning a profit up to the maximum gain is enabled by the condensed wingspreads and optimal strike selection. The probability edge contributes to its efficiency.

Capital Efficiency

The Iron Butterfly provides leveraged exposure to the underlying with lower capital outlay than buying the stock outright. It earns positive net credit upfront and requires margin only on the wingspread portion. This allows traders to put on multiple positions and diversify across various underlying in a capital-efficient manner.

Clearly Defined Loss Points

The maximum loss on the Iron Butterfly is very well defined, allowing traders to know the exact loss they are exposed to on the trade if the stock closes below the put strike or above the call strike at expiration. The breakeven points are also clearly defined. This helps efficiently manage risk.

Built-In Contingency Plan

The wingspreads on the Iron Butterfly act as a built-in contingency plan for adverse price moves. The wings cap the loss, so no additional hedging is required. The defined risk parameters make it an efficient trading vehicle that does not require additional adjustments.

Efficient Use of Time Decay

The Iron Butterfly benefits from time decay as the extrinsic value of the short options erodes leading up to expiration. Short options across multiple strike prices efficiently monetize theta decay.

However, the Iron Butterfly does have inefficiencies to consider.

Capped Profit Potential

The maximum profit is strictly limited to the initial credit received, capping any gains from large favourable price moves. Other strategies, like the long call, have unlimited profit potential. This capped upside reduces efficiency in strong trending markets.

Wide Bid-Ask Spreads

Illiquid options with wide bid-ask spreads increase slippage costs when entering and exiting. This erodes efficiency and the probability of earning the maximum profit. Liquid options are required.

Complex Structure

The Iron Butterfly involves multiple legs across various strikes, requiring more precise execution versus simplistic strategies. There are more variables at play, making it less efficient from a structural perspective.

What is the maximum loss for a Long Iron Butterfly?

The Long Iron Butterfly has a clearly defined maximum loss that is determined at the outset when constructing the trade. The maximum loss occurs if the underlying stock closes below the lower strike put or above the higher strike call at expiration.

Four steps are followed to calculate the maximum loss on a Long Iron Butterfly.

1. Identify the Strikes

First, identify the following four strike prices used in the Long Iron Butterfly.

– Lower Strike Put

– Higher Strike Call

– Short Strike Put

– Short Strike Call

For example:

– Lower Strike Put: Rs.45

– Higher Strike Call: Rs.55

– Short Strike Put: Rs.50

– Short Strike Call: Rs.50

2. Calculate Strike Width

Subtract the Lower Strike Put from the Higher Strike Call to determine the width between strikes.

In this example:

Higher Strike Call (Rs.55) – Lower Strike Put (Rs.45) = Rs.10

The Rs.10 width between the higher and lower strikes represents the maximum loss without the credit received.

3. Determine Initial Credit

While initiating the Long Iron Butterfly, a net credit is typically received from the short options expiring worthless. This credit amount reduces the maximum loss.

For example, if the initial credit received is Rs.2 per share, this would lower the maximum loss.

4. Subtract Initial Credit from Strike Width

To calculate maximum loss, subtract the initial credit received from the width between the higher and lower strikes.

In this example:

Strike Width Rs.10 – Initial Credit Rs.2 = Maximum Loss Rs.8

Therefore, the maximum loss on this Long Iron Butterfly would be Rs.8 per share if the stock finished below Rs.45 or above Rs.55 at expiration.

The short strikes at Rs.50 expire worthless to offset each other in the loss calculation. So, only the lower and higher strikes impact the maximum loss, which is then offset by the initial credit amount.

This clearly defined and capped maximum loss is the key risk metric for the Long Iron Butterfly. Understanding how to accurately calculate it informs the trader’s potential downside and helps size positions appropriately.

The maximum loss sets the threshold where downside protection kicks in. Careful construction of the wingspreads and strike selection allows traders to custom-tailor the parameters based on their risk tolerance. Wider wingspreads widen the maximum loss point.

What is the maximum profit for Long Iron Butterfly?

The maximum profit on a Long Iron Butterfly is capped and defined upfront when first initiating the trade. It is one of the key attributes of the strategy.

Five steps are followed to calculate and understand the maximum profit potential.

1. Sell the Short Options

A Long Iron Butterfly involves being short an at-the-money call option and an at-the-money put option with the same strikes and expiration.

For example, with the stock at Rs.50, the trader would sell the following.:

– 1 ATM 50 Strike Call

– 1 ATM 50 Strike Put

These short options bring in premium income in the form of credits.

2. Buy the Long Options

The next component is buying farther out-of-the-money calls and putting options to create the wingspreads.

For example, the trader could buy the following.:

– 1 OTM 45 Strike Put

– 1 OTM 55 Strike Call

Buying these long options results in a debit or cash outlay.

3. Calculate Net Credit or Debit

To determine maximum profit, add up the credits received from the short options and the debits paid out for the long options.

In this example:

– Credit received from short 50 Calls: Rs.3.

– Credit received from short 50 Put: Rs.3

– Debit paid for long 45 Put: Rs.1

– Debit paid for long 55 Call: Rs.1

Total Net Credit = Rs.4

The total net credit or net income received when opening the trade represents the maximum profit potential.

4. Max Profit Achieved at Expiration

This Rs.4 net credit is the maximum profit that is made using the Long Iron Butterfly if the underlying stock expires precisely at the short 50 strike at expiration.

In this case, all the options expire worthless, allowing the trader to capture full profit.

5. Capped Upside

Importantly, even if the stock moves favourably, no additional profit is made. The maximum gain is capped at the initial net credit regardless of how high or low the stock moves.

Is the Long Iron Butterfly good at bullish trends?

No, the Long Iron Butterfly options strategy does not perform well in a strong bullish trending market environment. The capped upside profit potential and directional risk make it a suboptimal choice when bullish momentum is dominant.

The maximum profit on the Long Iron Butterfly is limited to the initial net credit received when opening the position. Even if the underlying stock rallies sharply, no additional profits are made. The wingspread structure caps the upside. This makes the strategy inefficient for capitalizing on a prolonged bull run.

The ideal conditions for the Long Iron Butterfly are neutral sentiment and rangebound trading. A strong bullish bias increases the odds of the stock rallying beyond the higher strike call wing, incurring incremental losses. The directional momentum works against the neutral outlook needed.

In strongly trending bull markets, time decay tends to accelerate, which erodes the value of the long call wing much faster. This diminishes protection on the upside. The long call wing is crucial for capping losses in the event of a bull run.

Bullish momentum inflates the chances of early assignment on the short-call leg. Significant losses are incurred if assigned before expiration. The maximum loss protecting the downside assumes holding till expiration. Premature assignment eliminates this protection.

Bull trends are often coupled with higher implied volatility as prices trend higher. This inflates options premiums across all strike prices, reducing the net credit at entry and widening the maximum loss point. Volatility expansion hurts the probability of profit.

In uptrends, previously broken resistance levels start acting as support on any pullbacks. This increases the chances of the stock consolidating around these technical levels rather than dropping to the lower strike put. Resistance shifting to support is a headwind.

Strong bullish momentum expands the probability of breaching the higher call strike wing and incurring the maximum loss. While the probability of profit remains high in the 60-80% range, the 20-40% loss probability becomes more likely.

Is the Long Iron Butterfly good at bearish trends?

No, the Long Iron Butterfly options strategy does not perform well in a strong, bearish, trending market environment. The capped upside profit potential and directional risk make it a suboptimal choice when bearish momentum is dominant.

The maximum profit on the Long Iron Butterfly is limited to the initial net credit received when opening the position. Even if the underlying stock declines sharply, no additional profits are made. The wingspread structure caps the upside. This makes the strategy inefficient for capitalizing on a prolonged bear run.

The ideal conditions for the Long Iron Butterfly are neutral sentiment and rangebound trading. A strong bearish bias increases the odds of the stock dropping below the lower strike put wing, incurring incremental losses beyond the maximum loss point. The directional momentum works against the neutral outlook needed.

In strongly trending bear markets, time decay tends to accelerate, which erodes the value of the long put wing much faster. This diminishes protection on the downside. The long put wing is crucial for capping losses in the event of a bear run.

Bearish momentum inflates the chances of early assignment on the short put leg. Significant losses are incurred if assigned before expiration. The maximum loss protecting the downside assumes holding till expiration. Premature assignment eliminates this protection.

Bear trends are often coupled with higher implied volatility as prices trend lower. This inflates options premiums across all strike prices, reducing the net credit at entry and widening the maximum loss point. Volatility expansion hurts the probability of profit.

In downtrends, previously broken support levels start acting as resistance on any bounces. This increases the chances of the stock consolidating around these technical levels rather than surging to the higher strike call. Support shifting to resistance is a headwind.

Strong bearish momentum expands the probability of breaching the lower put strike wing and incurring the maximum loss. While the probability of profit remains high in the 60-80% range, the 20-40% loss probability becomes more likely.

Is Long Iron Butterfly good at neutral trend?

Yes, the Long Iron Butterfly options strategy performs best in a neutral trending market environment where the underlying stock is trading range bound. The defined risk-reward profile and high probability of profit align well with stagnant price action.

The Long Iron Butterfly offers a clearly defined profit zone between the breakeven points surrounding the short-strike prices. This zone widens in range-bound, trendless markets as volatility declines. The probability of finishing within the profit zone increases when directional momentum is absent.

With the underlying stock oscillating in a horizontal channel, the probability of breaching the wings on either side and incurring maximum loss diminishes. The wings provide protection against directional breakouts while allowing profits to be captured within the expected range.

Low and stable implied volatility is ideal for the Long Iron Butterfly as it reduces options premiums and narrows the distance between strikes. A lower IV environment indicates reduced expectations of outsized bullish or bearish trends emerging.

The passage of time and accelerated time decay in the last 30 days before expiration have a less adverse impact on the wings when the stock is range-bound. The extrinsic value erosion is muted, with the stock stabilized near the ideal middle strike prices.

Range-bound trading is often defined by clear support and resistance boundaries that contain price action for extended periods. Oscillating between technical levels reinforces a neutral bias and widens the expected trading range.

Neutral trends significantly reduce the chances of early assignment on the short legs before expiration. With less directional momentum, holders are less inclined to exercise options to capture dividends or directional profits pre-expiry.

Estimates for the probability of profit on the Long Iron Butterfly are typically 60-80% or greater under neutral conditions given the narrow wingspreads. In trending markets, the probability of loss rises as directional risks increase.

How does Long Iron Butterfly differ from other strategies?

The Long Iron Butterfly has limited, capped profit potential, whereas Long Call and Put offers unlimited profit if the stock makes a big directional move. However, the maximum loss is clearly defined on the Iron Butterfly, while long calls/puts face theoretically uncapped losses if the stock moves against the directional bias.

Additionally, the Iron Butterfly benefits from time decay and low volatility, unlike long calls/puts, which rely on continued directional momentum and increasing volatility. The Iron Butterfly requires a neutral outlook on the stock, while long calls/puts need a pronounced bullish or bearish bias to yield profits.

The Long Iron Butterfly provides a higher probability of earning a small profit, but gains are capped. Naked short calls and puts face unlimited risk for comparatively tiny potential gains. Maximum loss is a known quantity with the Iron Butterfly due to the wingspreads, whereas short options carry unlimited risk if the trade moves against the trader. Also, margin requirements are lower for the Iron Butterfly versus uncovered short positions. Assignment risk before expiration is largely mitigated by the Iron Butterfly structure, unlike naked shorts.

The Long Iron Butterfly benefits from time decay across multiple short options, while vertical spreads have just a single short leg. The probability of profit is higher on the Iron Butterfly, but the maximum profit potential is lower due to the condensed wingspread structure. The Iron Butterfly generally requires a larger net debit upfront than credit spreads, increasing maximum loss. However, the maximum loss is clearly defined in both strategies based on the strikes, although early assignment adds risks.

The Iron Butterfly provides a higher probability of profit with lower capital requirements than straddles and strangles. Straddles/strangles rely on volatility expansion, unlike Iron Butterflies, which need low stable volatility. Straddles require significant stock movement, unlike Iron Butterflies, which benefit when the stock is stagnant. While both strategies have capped maximum loss, straddles/strangles face uncapped risk. Finally, straddles/strangles offer unlimited profit potential, whereas the Iron Butterfly profit is constrained by the wingspreads.

How does a Long Iron Butterfly differ from a Short Iron Butterfly?

The Long Iron Butterfly has a neutral bias, expecting the stock to trade range bound. The Short Iron Butterfly has a directional bias, betting on the stock breaking out above or below the wings.

The maximum profit on the Long Iron Butterfly is capped at the initial net credit received. The maximum profit on the Short Iron Butterfly is uncapped, with the stock moving beyond the wings.

Maximum loss is defined on the Long Iron Butterfly by the strike width less the credit. The Short Iron Butterfly has uncapped maximum loss if the stock expires between the wings.

The Long Iron Butterfly benefits from low implied volatility, keeping the stock range bound. The Short Iron Butterfly needs elevated implied volatility to drive a breakout beyond the breakevens.

The Long Iron Butterfly performs best in neutral trending markets. The Short Iron Butterfly is ideal for directional trending markets outside the wings.

The Long Iron Butterfly is a limited risk strategy. The Short Iron Butterfly is an unlimited risk strategy without a capped downside if the trade moves against the position.

The probability of profit is very high on the Long Iron Butterfly when constructed properly. The probability of profit on the Short Iron Butterfly is typically below 50%, given the directional assumptions required.

Time decay helps the Long Iron Butterfly as the short options expire worthless. Time decay harms the Short Iron Butterfly as the value of the wings erodes with the stock in between them.

How does Long Iron Butterfly differ from Butterfly Spread?

The Long Iron Butterfly involves being long a put, short 2 at-the-money puts, and long another lower strike put of the same expiration. The Butterfly Spread is simply long 1 in-the-money put, short 2 at-the-money puts, and long 1 out-of-the-money put.

The Long Iron Butterfly offers a maximum profit capped at the net credit received from the body shorts. The maximum profit on the Butterfly Spread is the difference between the wing strikes less the cost paid.

Maximum loss on the Long Iron Butterfly is defined by the strike width less the credit. The Butterfly Spread maximum loss is limited to the initial debit paid.

The Long Iron Butterfly has two breakeven points at the wing strikes. The Butterfly Spread has three breakeven points due to the structure.

The Long Iron Butterfly benefits from a contraction in implied volatility. The regular Butterfly Spread needs volatility expansion for the wings to become profitable.

The Long Iron Butterfly profits from range-bound price action. The Butterfly Spread has a directional assumption, profiting from the stock moving above the higher strike wing.

The Long Iron Butterfly is considered a limited, defined risk strategy. The Butterfly Spread also has limited, defined risk.

How does Long Iron Butterfly and Modified Call Butterfly?

The Long Iron Butterfly is structured as a long put wing, short put body, short call body, and long call wing. The Modified Call Butterfly simply has a long call spread plus a short out-of-the-money call.

The Long Iron Butterfly has a neutral bias, expecting a stagnant stock price. The Modified Call Butterfly has a bullish bias, anticipating the stock to trend higher.

The maximum profit on the Long Iron Butterfly is capped at the net credit received for the body shorts. The Modified Call Butterfly maximum profit is determined by the width of the call strikes.

The Long Iron Butterfly has defined maximum loss between the wing strikes less the credit. The Modified Call Butterfly max loss is limited to the net debit paid upfront.

The Long Iron Butterfly has two breakeven points at the wing strikes. The Modified Call Butterfly only has one breakeven point at the lower call strike.

The Long Iron Butterfly needs low implied volatility for a range-bound stock. The Modified Call Butterfly performs better with rising volatility driving the upside move.

The Long Iron Butterfly is a limited, defined risk strategy. The Modified Call Butterfly also carries defined, limited risk.

Time decay helps the Long Iron Butterfly expire worthless. Time decay hurts the Modified Call Butterfly without upward momentum.

Previous Article

Previous Article

26")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.